Rising debt in an expanding economy with low interest rates may not necessarily be a bad thing if companies are increasing investments as well. The data4 suggests that a sizeable share of companies is doing just that. And some of these investments may well add to productivity growth in the wider economy in the medium to long term.

Debt rose sharply in 2020 for nonfinancial businesses

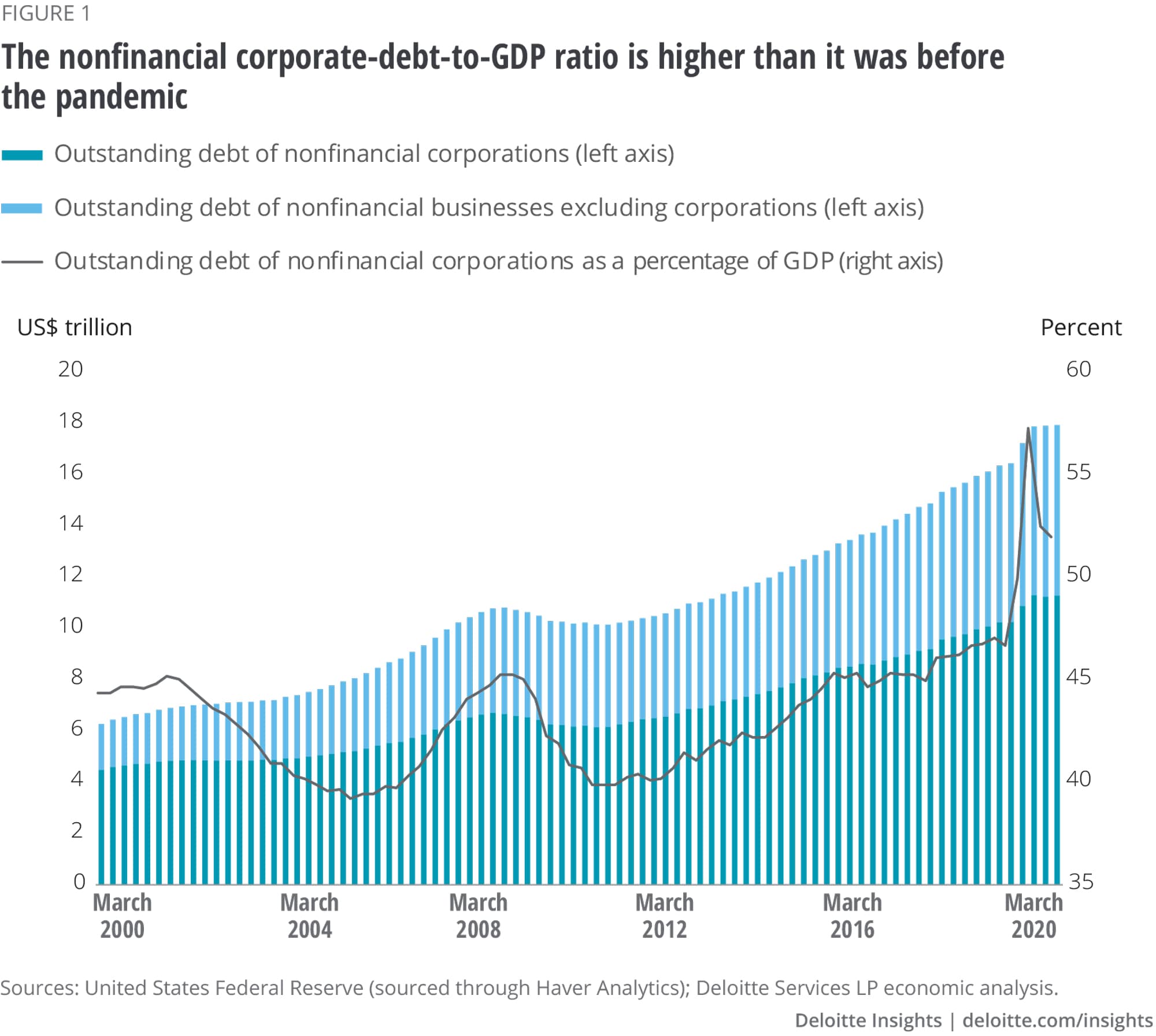

At the end of 2020, the total debt outstanding for nonfinancial5 businesses in the United States was about US$17.7 trillion. Between 2010 and 2019, debt grew at an average annual rate6 of 5.5%, but in 2020, growth jumped to 9.1%. The surge in debt in 2020 was likely due to at least one of three factors. First, some businesses were forced to borrow more to keep operations running as large parts of the economy slowed or shut down. Second, some businesses had to invest in technology to support remote work, wherever possible, while others had to reconfigure workplaces to ensure social distancing in jobs that required in-person work. Finally, not all businesses were worse off due to COVID-19. Key businesses in sectors, such as information technology, health care, consumer products, and communication services, witnessed strong demand growth, a trend that is likely to sustain at least in the near to medium term. Consequently, some of these businesses are likely to have borrowed more to expand the size and array of goods and services they produce.

No matter the reason, rising leverage last year added to already high levels of debt that existed before the pandemic. In Q3 2019, for example, nonfinancial business debt outstanding was about 75% of GDP, the highest ever at that time. With GDP declining sharply in Q2 2020, the debt-to-GDP ratio shot up during the quarter, before going down as an economic recovery took shape in the second half of the year. But, at 82.4% at the end of 2020, overall debt relative to the size of the economy is still high even by prepandemic standards.

Of all the debt outstanding of nonfinancial businesses in the economy, corporates account for the largest share—about 63% in 2020. And just like total nonfinancial business sector debt, corporate debt—both the level of debt and its size relative to GDP—has been edging up since 2010. The pandemic has made it a tad worse than what it was in 2019 (figure 1).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}