Positive on CAPEX, hiring and revenues

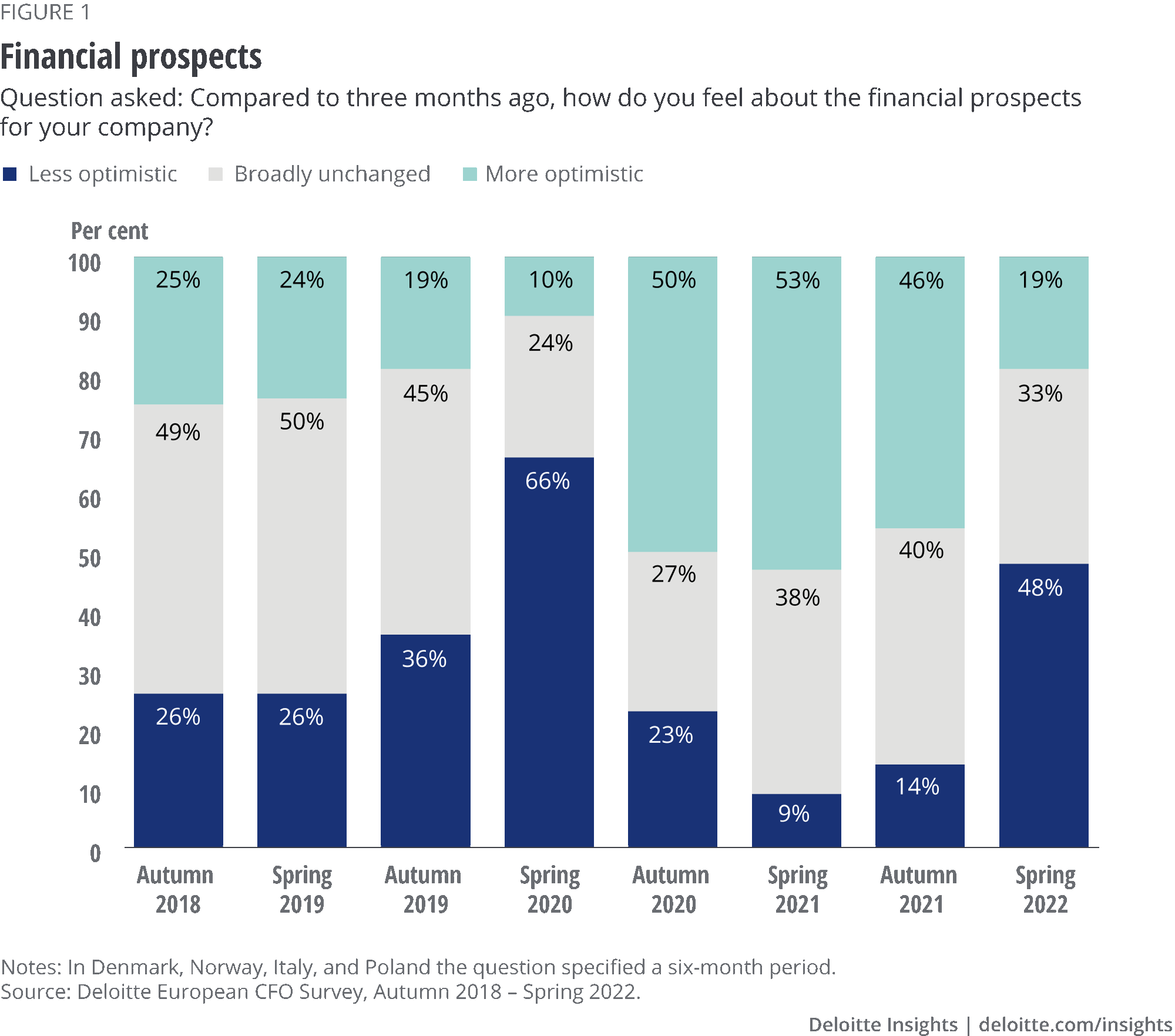

Despite worsening expectations about the financial outlook compared to the autumn 2021 survey, CFOs remain positive about revenue, CAPEX and hiring.

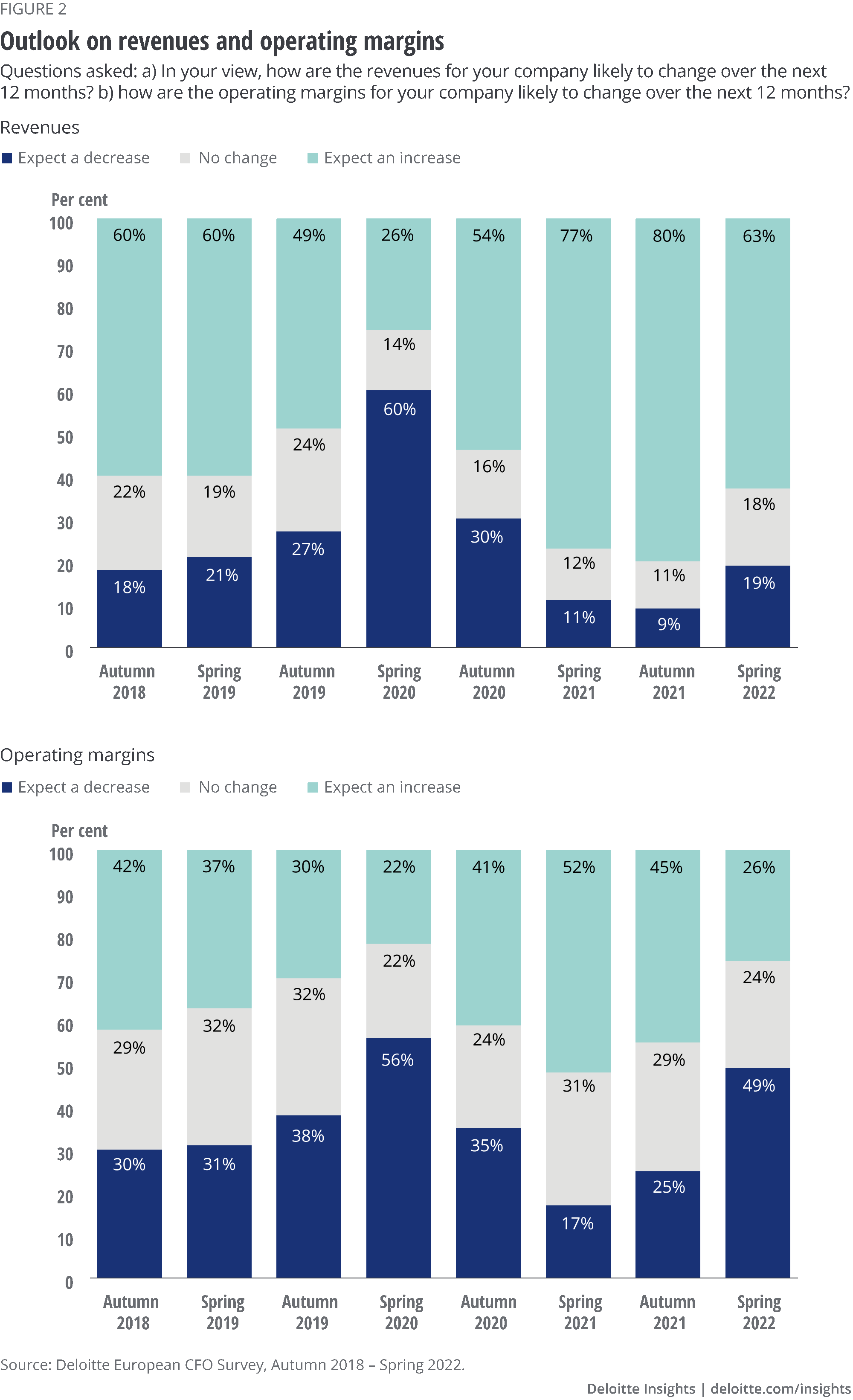

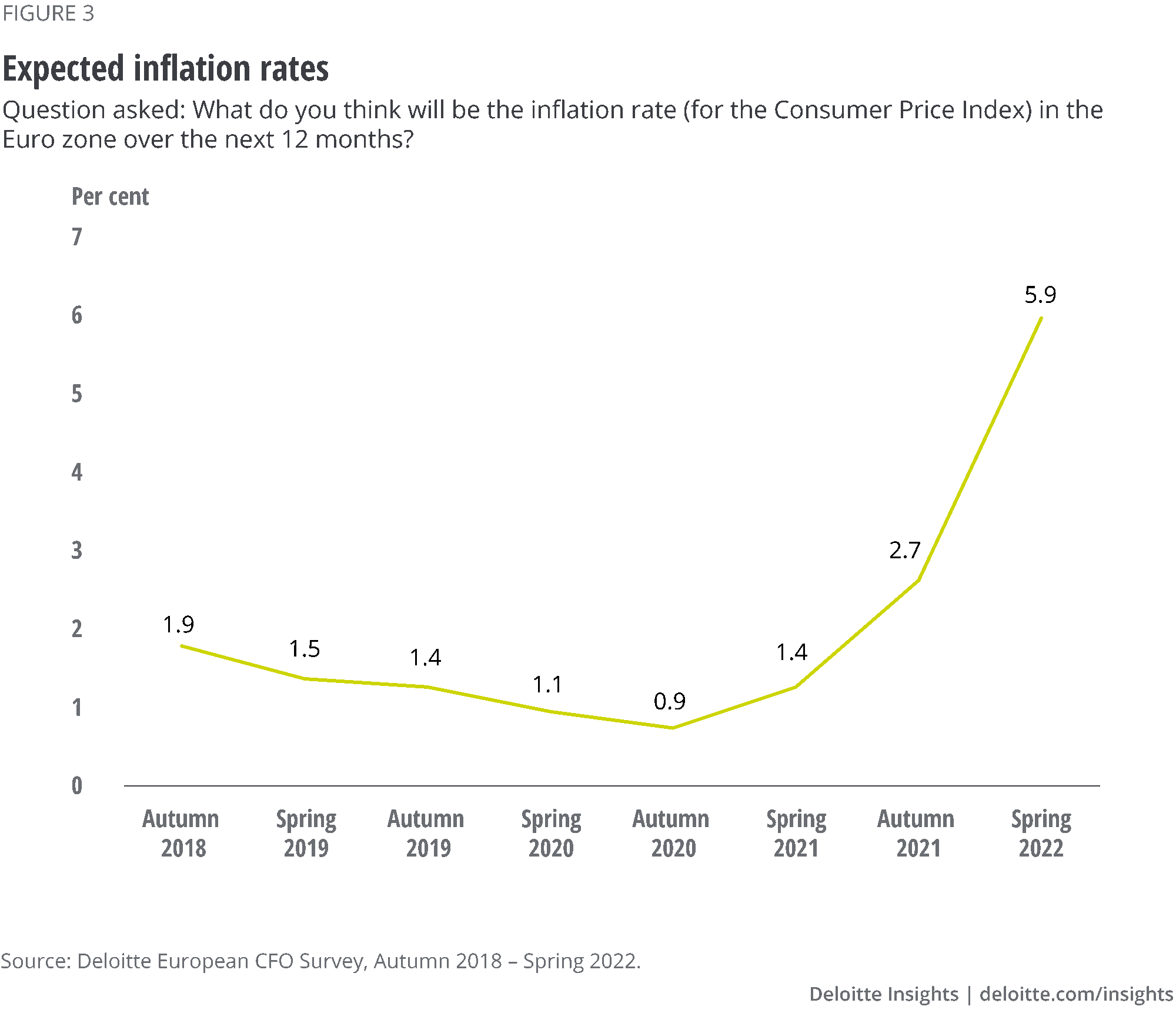

Faced with a more uncertain economic climate and surging operating costs, CFOs anticipate a sharp deterioration in operating margins. Almost half (49 per cent) believe operating margins will decline over the next year. This figure has doubled since the previous survey. The reasons include high inflation across European countries caused by rising commodity, energy, operating and transport costs. The net balance of expectations concerning operating margins (the difference between the share of positive and negative responses) declined from 20 per cent in the autumn to -23 per cent in spring 2022.

CFOs in the consumer goods sector, faced with persistent supply chain disruptions, labour shortages and rising costs, are the most pessimistic, with 64 per cent believing that operating margins will decrease over the next year. At the other extreme, CFOs in the tourism & travel sector are the most optimistic: half (49 per cent) believe their margins will increase.

Although most CFOs remain optimistic that revenues will increase over the next 12 months, the net balance of expectations has decreased from 71 to 44 per cent. Despite this, 63 per cent of CFOs believe revenues will increase in the next 12 months while only 19 per cent feel revenues will decrease.

Similar trends can be observed across all sectors. CFOs in the business and professional services sector are the most optimistic, with 89 per cent expecting revenues will increase in the next 12 months. CFOs in the automotive industry are the least optimistic, with just 41 per cent expecting revenues to increase over the same period.

The net balance of expectations about capital expenditures (CAPEX) over the next 12 months has declined sharply, from 38 per cent in the autumn to 10 per cent in spring 2022. Despite this, a third of CFOs across Europe remain optimistic that they will increase CAPEX spending during the next 12 months.

CFOs in the automotive sector are the most pessimistic: it is the only sector to show a negative net balance in CAPEX spending intentions in spring 2022. The net balance of CFOs responding that CAPEX investments will increase declined sharply from 20 per cent in autumn 2021 to -13 per cent in spring 2022. Meanwhile the proportion of CFOs in the automotive industry who believe CAPEX investments will decrease has doubled, from 16 per cent in autumn 2021 to 37 per cent in spring 2022.

As with other critical metrics, the net balance in CFOs’ hiring expectations has also declined, from 42 per cent in spring 2021 to 28 per cent in autumn 2021 – but it remains higher than one year ago. The survey results also reveal that CFOs have revised up their plans for future employment considerably more strongly than for CAPEX. More than 40 per cent of CFOs expect to expand the number of employees over the next year, nearly three times more than those who expect a decrease (15 per cent) over the same period.

CFOs in all other sectors except automotive plan to increase hiring in the next 12 months. CFOs in the business and professional services sector (75 per cent) and tourism & travel (72 per cent) are the most confident that they will be increasing the employee headcount over the next 12 months. In contrast, a significant portion of CFOs in automotive (33 per cent) plan to decrease the employee headcount over the next year, the highest across all sectors.

One reason for the strength of corporate hiring plans is the pronounced shortage of skilled labour. This has been identified as one of the top three business risks in spring 2022.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}