{kind=link}

{kind=link}

{kind=link}

From one financial challenge to the next has been saved

The authors would like to thank Marcello Gasdia for his contribution to this article.

Cover image by: Sylvia Yoon Chang

United States

United States

Netherlands

United Kingdom

An enduring pandemic followed by a historic bout of inflation—The steady stream of shocks defining our collective global experience over the past few years have been far from easy on consumers’ finances. And that’s been particularly true for lower earners. Like the pandemic, inflation disproportionately impacts those who earn less. Higher prices for everyday purchases like gas and groceries simply mean something different for those who may already be living paycheck to paycheck.

In the previous edition of this consumer insights article series, we looked at nearly two years of financial sentiment data among US consumers to better understand how different income groups are weathering the storm. The data revealed a story of accelerating bifurcation.

Given the global nature of the pandemic and inflation, similar bifurcation stories are unfolding worldwide. Trends are, however, playing out a bit differently by country.

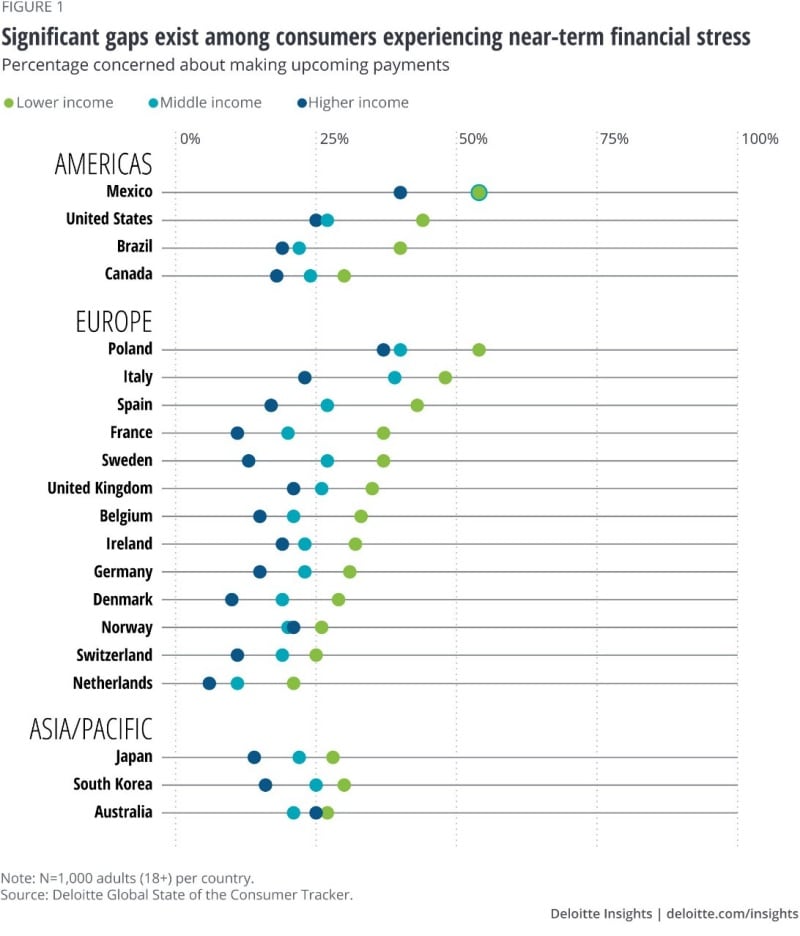

The percentage of lower earners concerned about making upcoming payments varies significantly across the world. Across study countries, the figure sits lowest in the Netherlands at just 21% (figure 1). In a handful of countries, including Mexico, the United States, Spain, Italy, and Poland, it more than doubles to roughly half. France, Sweden, and Brazil also measure in high at roughly four in 10.

Across the world, the current outlook for lower earners can range from fairly positive to outright bleak—even across developed countries. Longitudinal trends reveal even more differences.

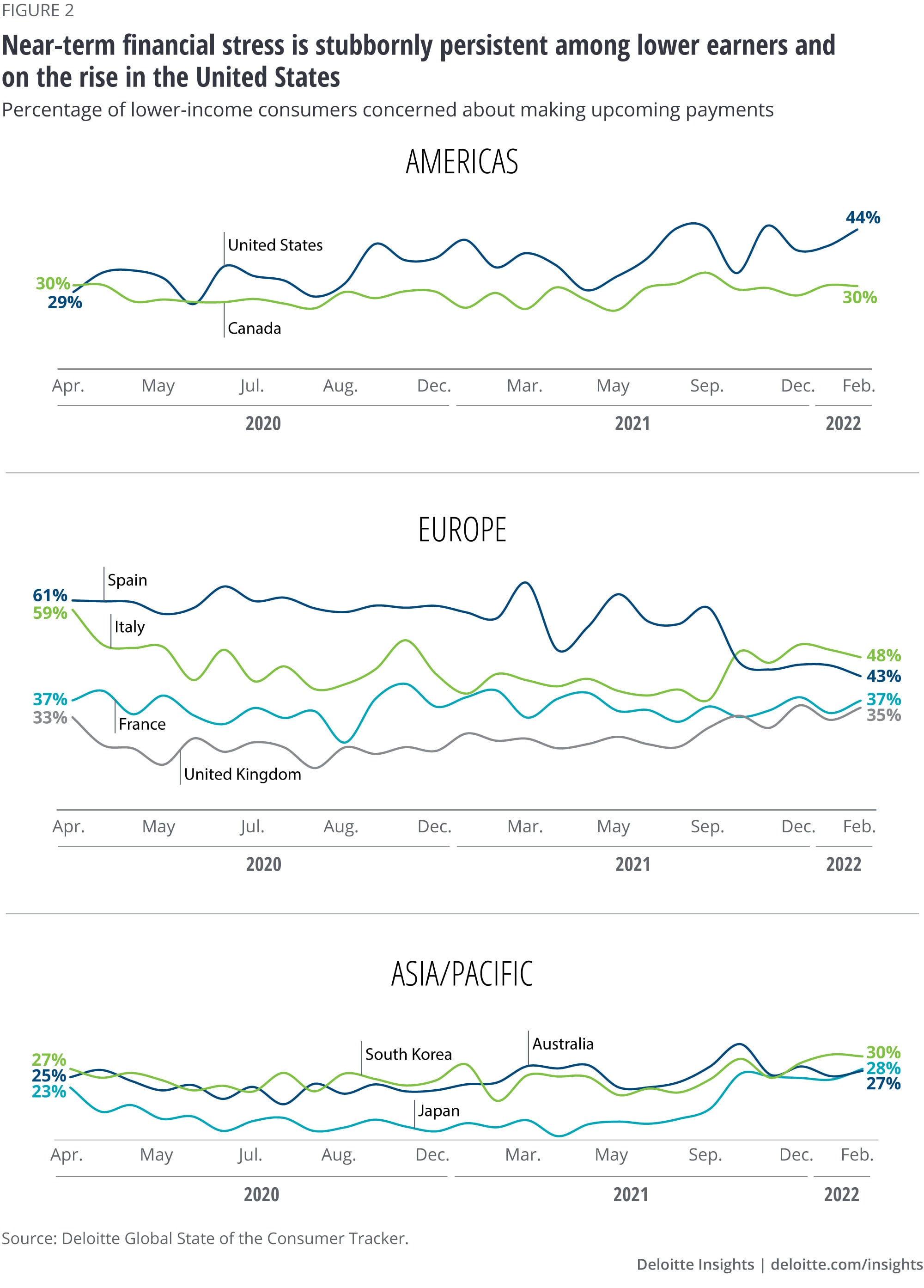

For example, the United States remains the only study country where financial stress among lower earners is climbing (figure 2). Since the pandemic’s early days in April 2020, the percentage of lower-earning Americans concerned about paying upcoming bills has soared from 29% to 44% (figure 1). Relative to the rest of the world, Americans seem more vulnerable to the economic shocks thrown their way.

While a number of other countries have a high proportion of lower earners struggling to make ends meet, no study country shows a comparable increase across the pandemic period (figure 2). In fact, in a handful of countries, including France, Canada, South Korea, Australia, and the United Kingdom, financial stress among lower earners has remained stable. And, in Spain and Italy, the figure has improved. Yet, stable and improved still means a third to nearly half of lower-income consumers in these countries are concerned about upcoming monthly payments, which remains a worrisome signal for overall financial well-being.

More recently, since the late summer and early fall of 2021, immediate financial concerns among lower earners have started climbing in the United Kingdom, Italy, and Japan. These increased concerns coincide with mounting inflation.

In the United States, while financial stress among lower earners climbs, it’s been stable among average- and high-income consumers. Two years ago, the difference between the number of low- and high-income Americans struggling to make upcoming payments was much less pronounced. As of February 2022, the gap across income groups (figure 1) is among the widest across study countries. If the trend continues unabated, the United States could have the widest gap across study countries in well under a year.

This furious pace of bifurcation is a uniquely US story. And it’s perhaps accentuated by the relatively smaller gap in financial stress in other countries—particularly Australia, Norway, Canada, and, to some extent, the Netherlands, Switzerland, and Ireland.

In some countries, particularly in Europe, larger public social welfare spending might be proving stronger safety nets for lower earners. In countries such as Denmark, Germany, Norway, and Belgium, where relatively few low earners report financial stress, public social spending equates to roughly 30% of domestic GDP (versus 19% in the United States).1 But while expanded health care programs, worker protections, and other social welfare programs likely extend a lifeline to many who need it, the many outliers to the trend hint at the complexity of the issue. For example, countries such as France, Spain, Italy, and even Sweden, all spend heavily on social welfare, yet all have a relatively high proportion of lower earners citing financial concerns. These countries also have some of the largest gaps in high- and low-income consumers citing financial concerns.

Despite significant public sector efforts across a variety of national programs prior to and over the pandemic, a portion of consumers continues to struggle. This suggests that the public sector alone may not be able to address this persisting challenge.

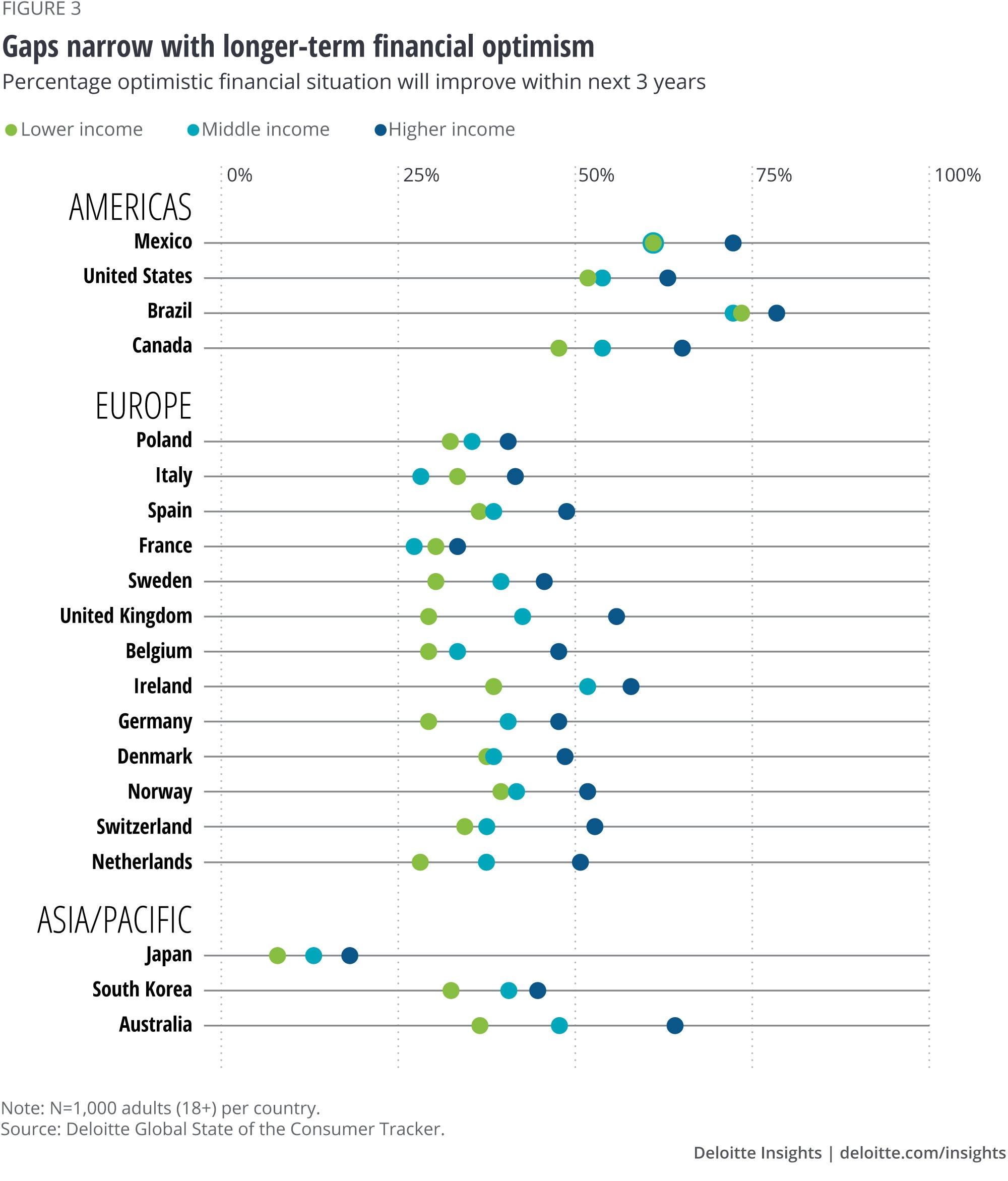

Compared to current financial concerns, optimism around future finances shows much less variation across countries and income groups. To some extent, this trend could be driven by the fact that optimism is fairly low across the world. For example, across European countries, roughly half of consumers are optimistic that their financial situation will improve within the next three years (figure 3). The differences many would expect to find between low and high earners are present but are far less pronounced compared to current financial concerns. Additionally, optimism among the continent’s lower-earning Europeans is extremely consistent by country, even though immediate financial concerns vary considerably.

Of course, there are always exceptions to sweeping global trends. Again, the United States remains an outlier. Despite the recent rise in immediate financial concerns among lower-earning Americans, they remain relatively optimistic about their future. And over the past few months, optimism among higher-income Americans has decreased, potentially driven by a slowdown in financial markets and geopolitical events.

Trends around consumer bifurcation remain an important space to watch. For decades, economic observers have linked trends such as income inequality to chronic weakness in demand and slowed economic growth.2

In our own research data, we’re beginning to see signals that correlate rising bifurcation with weakening spending intentions. More specifically, countries where lower earners are showing glaring signs of financial stress are also beginning to show weakened discretionary spending intentions. The United States and England are two key examples. Since the fall of 2021, both countries have seen some of the sharpest increases in financial stress among lower earners. They also remain among the only study countries where discretionary spending intentions around categories such as recreation and entertainment, restaurants, and leisure travel have dropped since the fall.3

Beyond weakening demand, intensifying bifurcation has had a hand in shaping commercialization strategies for consumer companies. In this K-shaped recovery, many consumer brands are expanding their offerings that cater to the economic spectrum, spanning from product diversity to greater airline cabin segmentation. Having both high- and low-end offerings can facilitate tradeoffs within a company’s brands, so that businesses don’t lose consumers completely as prices go up or economic viability goes down. At the same time, consumers of all income levels appear to place a high value on convenience and efficiency, driving brands to meet those needs through digital customer service and curbside pickup, among other means.

However, these are shorter-term tactics. Does business have a role in a longer-term solution?

Over the last 50 years, millions, if not billions, of lower-income consumers have joined the global middle class or have risen out of poverty. And, while public policy may have created the conditions, it was the private sector that made it possible.4 But some percentage of the world will always comprise lower-income consumers. Businesses should therefore strive to make a more equitable playing field for more consumers across the spectrum. Further, the pandemic, stressed supply chains, global inflation, and recent geopolitical events are all stark reminders of the interconnectedness of our modern global economy. With all this in mind, how can employers and global community leaders make our interdependence more resilient and help ensure the financial well-being of their consumers is on firmer footing?

Some skeptics still believe there is an inherent tradeoff between purpose and profit, as well as values and value. However, several private sector leaders, from chief executive officers (CEOs) of multinationals to those who control access to capital, are calling for answers to these questions. Many global financial firms are making pledges to bring billions of people into the digital economy. Many leading car manufacturers and airlines, among other sectors, have announced new talent commitments to create more diverse, equitable, and inclusive workforces. But with the world on the tipping point of even greater change, businesses may need to do more than just fiddle with the dials.

To explore global spending intentions and other consumer trends, visit our Global State of the Consumer Tracker.