{kind=link}

{kind=link}

{kind=link}

{kind=link}

When inflation concerns persist for too long has been saved

The authors would like to thank Marcello Gasdia for his significant contribution to this article.

Cover art by: Natalie Pfaff

United States

United States

United States

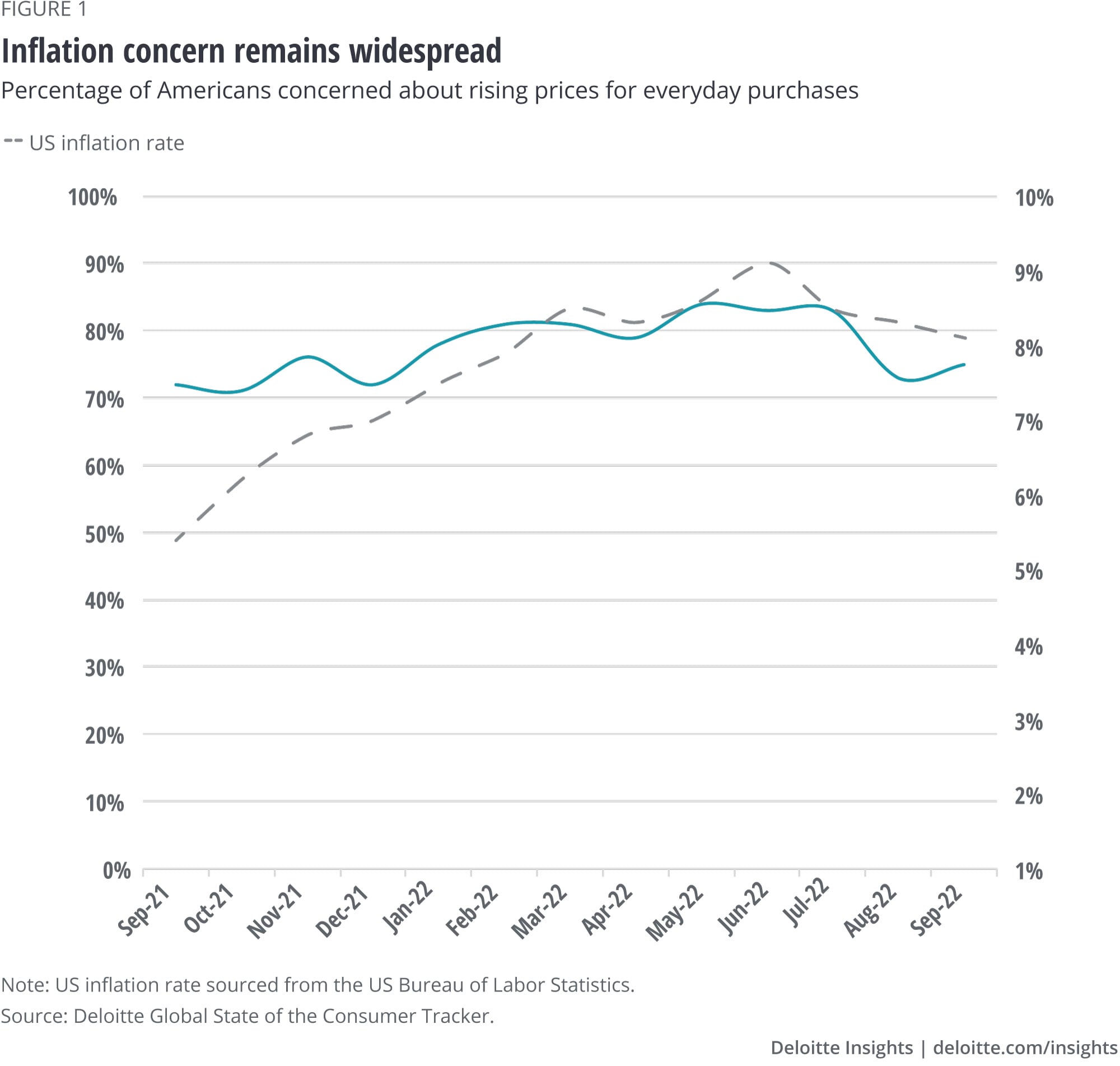

Many economists—and the Federal Reserve—thought that the initial price rises in the middle of 2021 were “transitory.” More than a year later, inflation is still high, and concern appears to be widespread—the percentage of Americans concerned about rising prices for everyday purchases has failed to fall below 70% this past year (figure 1).

Policymakers have been challenged in taming inflation. But our data suggests that quelling Americans’ concern might prove even more difficult. Gas prices falling from their highs in early summer did little to take the sting out of broader inflation worries in our survey. Indeed, in recent weeks, gas prices have started to creep back up. Additionally, the nature of inflation concern itself may be shifting—with more factoring in a potential long-term impact on the economy, and not just a quick squeeze on household finances.

For consumer companies, paying attention to inflation perceptions might be just as important as inflation rates. Consumers’ perception of price increases doesn’t always match reality, particularly at the category level. And these perceptions have become a critical driver of spending confidence. Americans most concerned about inflation are signaling weaker spending intentions across several key categories—particularly more discretionary ones.

Amid an uphill year for many US households, Americans were thrown a few lifelines in recent months. The inflation rate decreased for four consecutive months between June and September, albeit slightly.1 But perhaps more importantly, spiking gas prices eased during this period.

Despite these optimistic signals, however, sentiment has struggled to improve. During those summer months, the percentage of Americans concerned about rising prices only fell from 83% to 73% (figure 1). And the positive trend was short-lived; by September, worry already seemed to be on the rise again, potentially as gas prices were on the rise again.

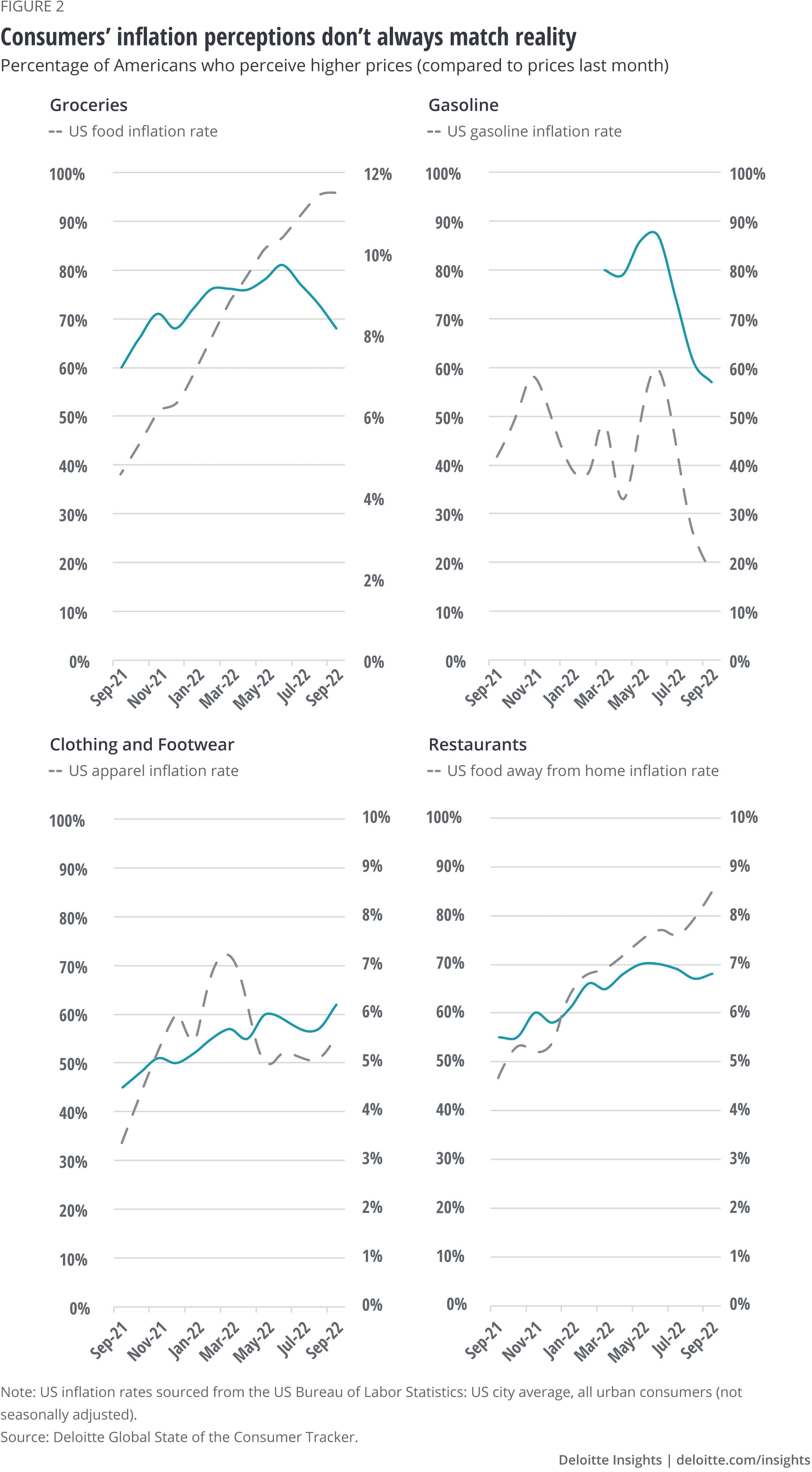

Inflation concerns remain highly elevated, even as significantly fewer Americans cite higher prices in major categories like gas and groceries. Since June, the percentage of Americans who felt prices were rising at the grocery store (compared to prices the prior month) fell considerably—from 81% to 68% (figure 2). Consumers citing the same for gas plummeted from 87% to 57%.

Americans’ sense of price changes also revealed another important insight. Inflation perceptions don’t always align with actual price action. That observation is important for consumer companies to consider within their pricing strategies. In the case of groceries, many Americans believed prices were stabilizing when they weren’t (figure 2). Likely, optimism from falling gas prices (much more discernable) spilled over into other everyday categories like groceries. Some consumers may have also assumed that falling fuel prices relieved manufacturers’ cost pressures. Meanwhile, consumers cited higher prices in different categories like clothing and footwear, even when clothing inflation rates dropped significantly.

Whether influenced by emotion or consumers filling in the blanks based on broader trends or news cycles, perception doesn’t always align with reality. And there are likely good and bad implications around price perceptions being so erratic. On the positive side, consumers have demonstrated that inflation sentiment can quickly improve—particularly in the presence of even slightly optimistic signals. On the negative side, recent signs and news headlines only seem gloomier or mixed at best. The strengthening narrative of a potential global recession is likely already contributing to the persistence of broader inflation worries.

There are other potentially less obvious drivers behind persisting inflation worries. The nature of the concern itself is likely changing. The more inflation proves challenging to tame, the more likely consumers are to grow anxious about the long-term impact on the economy. A short stint of inflation was likely tolerable for Americans flush with pandemic savings. But with each month, the chances of Americans starting to assume that inflation will persist in the long run rises. Inflation concern is likely becoming more than just about the immediate strain on pocketbooks.

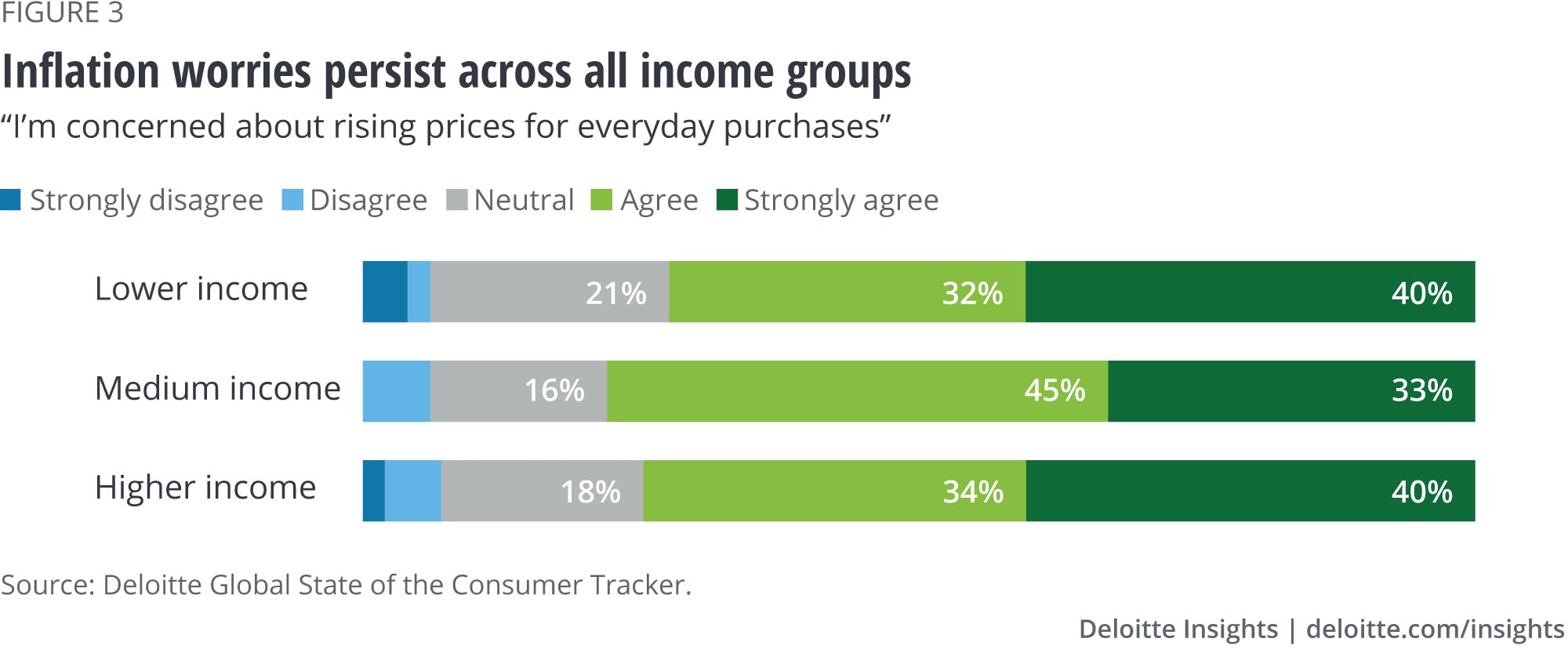

Looking at inflation concerns across income levels supports the trend. Anxiety around inflation is pervasive across all income groups (figure 3). Higher earners are just as likely to be concerned about inflation as lower-earning Americans.

But, more importantly, inflation concern has increased significantly among higher earners over the past year. The percentage of higher-income Americans very concerned2 about inflation has grown from just 29% to 40% since September 2021.3

Among high-income Americans, rising inflation concern is less likely to be driven by rising prices for groceries and other purchases—at least relative to lower earners. Roughly one in four higher earners have immediate financial worries like concerns about making upcoming payments (compared to nearly half of lower earners).4 And this figure has generally remained stable over the past year.

For affluent Americans, recent spikes in inflation concern could be driven by broader economic concerns.

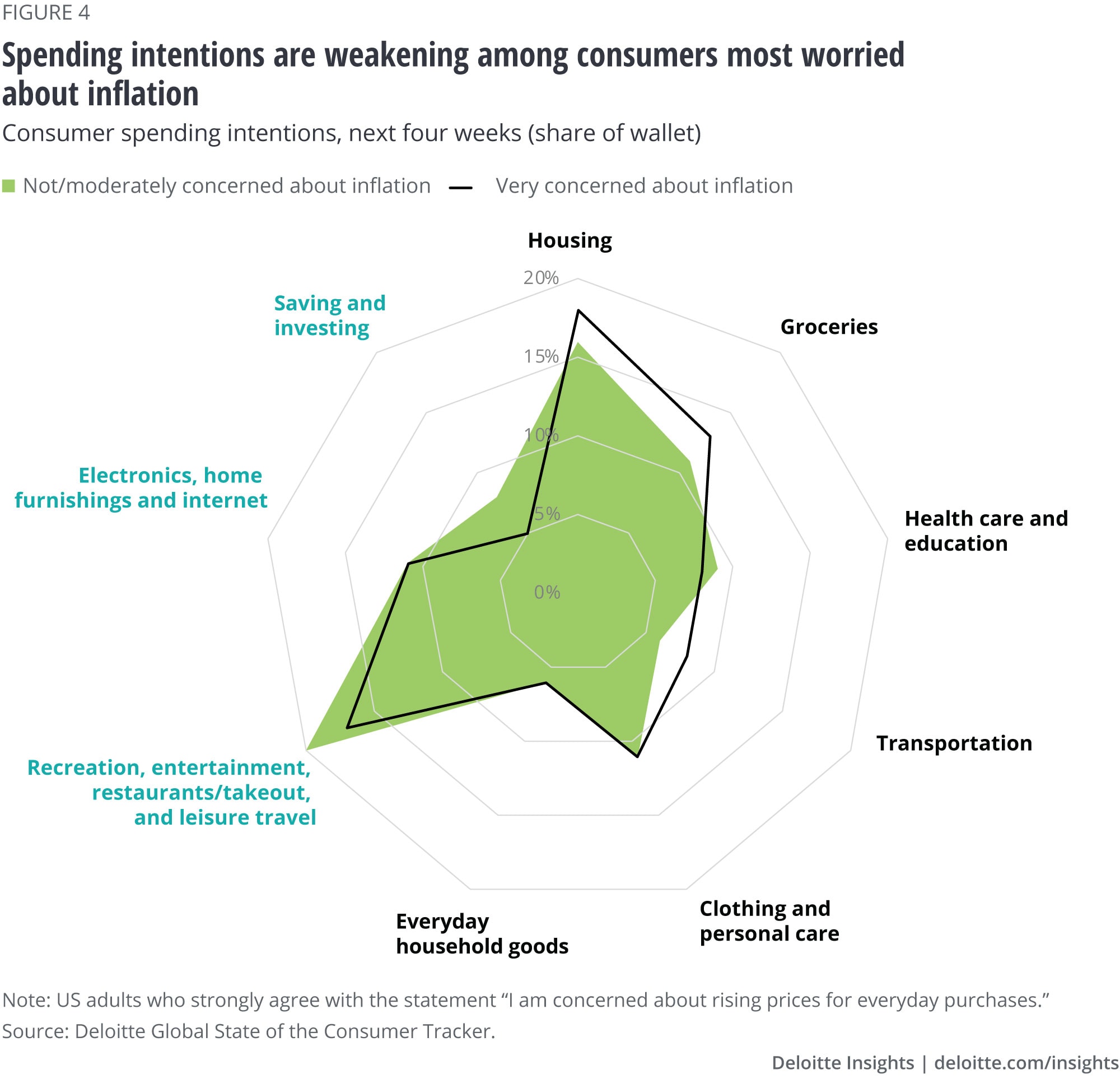

Inflation perceptions are essential to understand. They likely play a key role in consumers’ spending confidence. Among surveyed Americans most concerned about inflation, spending intentions for the month ahead signal weakening confidence, particularly across more discretionary categories such as recreation and entertainment and leisure travel (figure 4). When considering their budgets for the month ahead, concerned Americans see a significantly larger share of their spending going to essential categories, including housing, groceries, and transportation.

Saving and investing plans also take a significant hit in the survey. Data strongly suggests planned cutbacks are impacting the investing side rather than traditional savings. Between February and July 2022, Americans planned to allocate significantly less of their total monthly savings and investing budget (25% vs. 16% earlier) toward riskier asset classes like stocks, mutual funds, and cryptocurrencies.5 Cash savings stole most of the share—from 45% to 52%. Overall, the shift away from riskier assets supports the earlier notion that long-term confidence in the economy is likely waning.

Again, the longevity of this current spell of inflation raises important questions. Short-term spending shifts that consumers may use to weather the inflation storm run the risk of cementing into longer-term habits. While consumers have demonstrated that inflation perceptions can quickly change, it remains to be seen how quickly spending confidence can recover.

Bureau of Labor Statistics.

View in ArticleHigh-income Americans choosing “strongly agree” for the statement, “I’m concerned about rising prices for everyday purchases.” for everyday purchases.”

View in ArticleThe authors would like to thank Marcello Gasdia for his significant contribution to this article.

Cover art by: Natalie Pfaff