Mobility in the eye of the storm has been saved

The authors would like to thank Marcello Gasdia, Benjamin Boyer, and Kelly Warner for their significant contributions to this article.

Cover image by: Natalie Pfaff

Meeting global demand remains an enormous challenge for the automotive industry. From the onset of the pandemic, the sector has endured a cacophony of supply challenges, from production shutdowns and debilitating semiconductor shortages to acute labor shortages and global supply chain bottlenecks.

Alongside supply challenges, consumer demand has likely never been more difficult to predict. Over the past two years, consumers’ daily transportation needs have been shaped by new forces like lockdowns, health concerns, and an evolving transition to remote work. Vehicle shoppers are encountering historically high prices for both vehicles and the gas to run them. And adding to the uncertainty, consumer preferences for electric vehicles (EVs) are rapidly evolving.

Vehicle demand is only likely to become more elusive. In the face of geopolitical instability and record inflation, rising commodity costs are driving up prices for vehicles even further. As the cost of living soars and potential recession looms, there’s a very real risk that more consumers will find themselves unable to afford big purchases or simply decide it’s not the right time to buy.

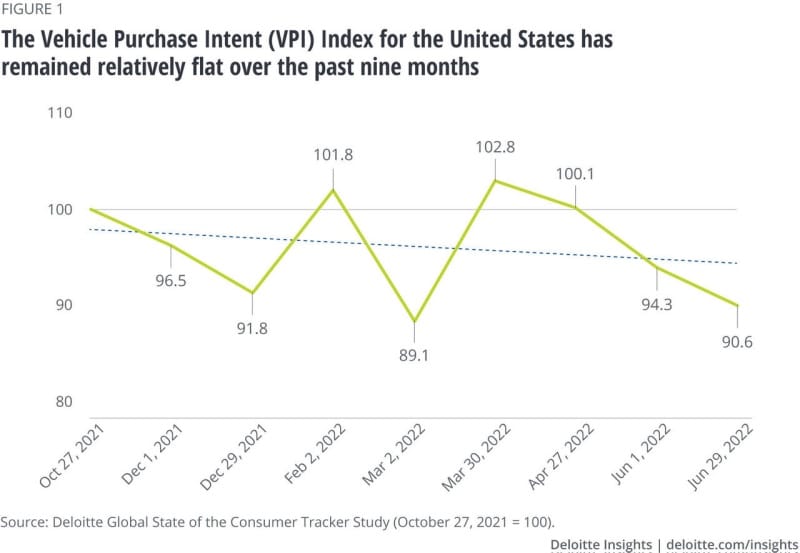

In an effort to shed some light on consumer buying intentions in these uncertain times, Deloitte developed the Vehicle Purchase Intent (VPI) Index, a forward-looking measure designed to track the percentage of people who intend to acquire a vehicle in the next six months. Looking at the trend in index values over the past nine months, the VPI for the US market is following a slightly negative trajectory commensurate with a drop in overall consumer sentiment tied to a growing concern over inflationary conditions (figure 1).1

But a lot is likely happening underneath the trend, as competing forces apply pressure to the top and bottom of the purchase intention curve.

In early 2020, the pandemic led to a sudden drop in vehicle demand as countries around the world went into lockdown, curtailing transportation, with the exception of essential goods. But as global economies gradually reopened, demand for new and used vehicles skyrocketed. Consumers who stayed away from dealer lots due to health concerns began to return. And the competition for a limited supply of vehicles was fierce. The pandemic likely drove a preference for the safety of personal vehicles over shared mobility options. Even now, eight in 10 Americans (~79%) plan to use a personal vehicle at “the same level or more” going forward.2 And about one-third (30%) plan to use public transport less often.

Strong demand spilled over to EVs. In 2021, US EV sales doubled from 308,000 units in 2020 to 608,000 units, while overall light vehicle sales grew just 3.4%.3 A strong desire to lower fuel costs, along with rising environmental concerns, likely drove consumer interest in EVs.4 At that time, the price of electricity was around a third of gasoline, making EVs a very compelling mobility option.5 Gasoline prices, which hovered between US$2 and US$3 a gallon for the last six to seven years, have since exploded to around US$5 per gallon in the wake of Russia’s invasion of Ukraine. With such a steep rise in gasoline prices, consumer interest in EVs is likely to continue along a growth trajectory. Maintenance costs for EVs are also relatively lower compared to internal combustion engine vehicles, as EVs have fewer moving parts and no need for regular oil and filter changes.

Even as global economies began to reopen, setting the stage for a swift recovery in vehicle demand, a lack of semiconductors (caused by the need to shutter assembly plants for obvious health reasons at the beginning of the pandemic) meant production had to be curtailed, effectively starving dealerships of new vehicle inventory. In the United States alone, semiconductor shortages resulted in a production loss of 1.5 million units in 2021 and will likely add another 233,000 units to lost production in the first half of 2022.6 In its latest forecast, S&P Global Mobility has also taken Russia’s invasion of Ukraine into account, revising global light vehicle production downward by 2.6 million units each for 2022 and 2023.7 Adding to the confluence of negative pressures, a resurgence of COVID-19 and subsequent lockdown measures enacted in China have led to significantly lower production volumes across a number of assembly facilities.8 These lockdown measures also resulted in the disruption of auto-related exports required to feed global vehicle assembly operations.

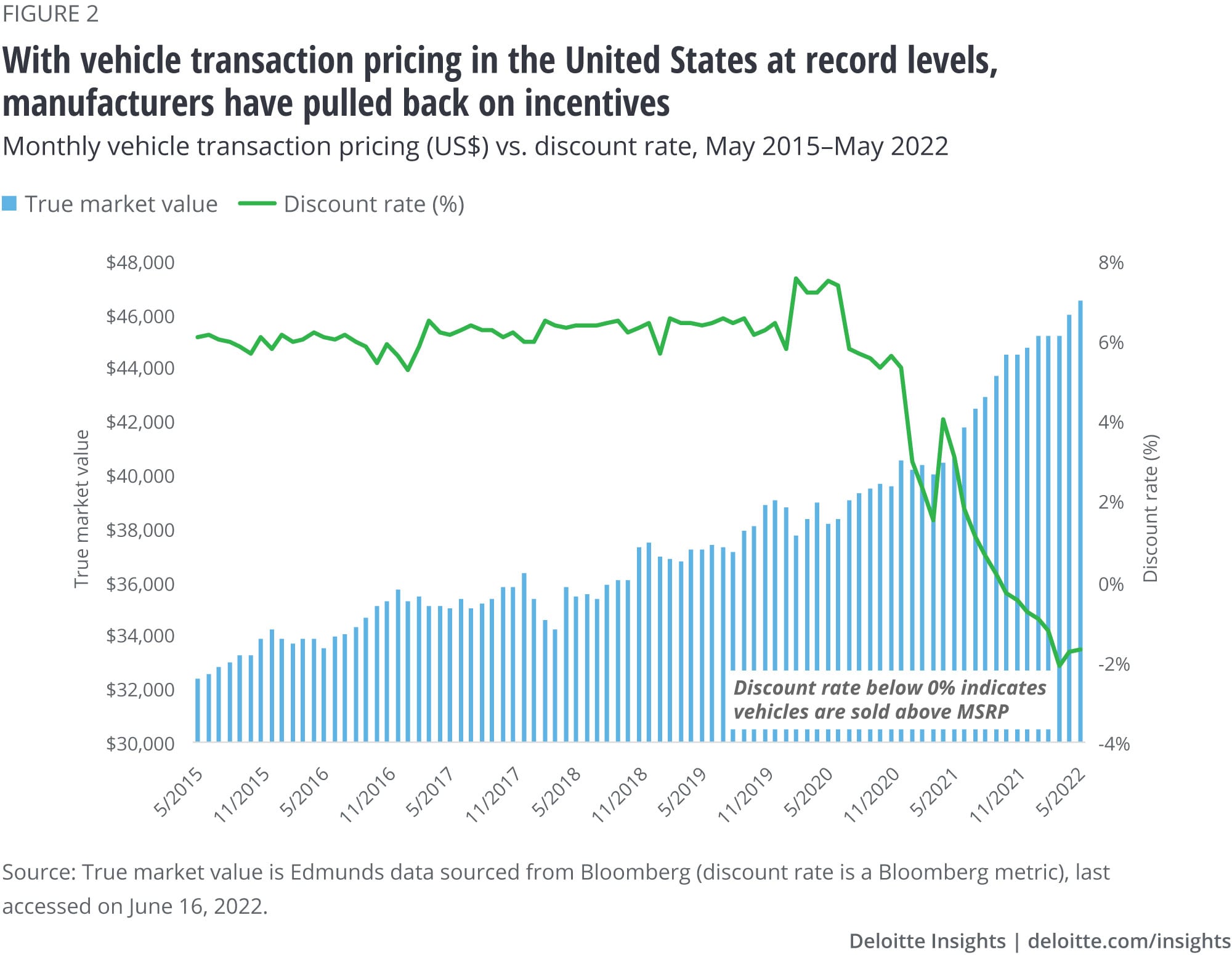

Back in the United States, the effect of production declines hit retailers almost immediately in the form of severe inventory shortages, which caused vehicle prices to spike. New vehicle transaction prices in the United States are currently at record levels, allowing manufacturers and dealers to also pull back on incentives. In fact, there have been many documented reports of vehicles being sold well above the manufacturer’s suggested retail price (figure 2).9

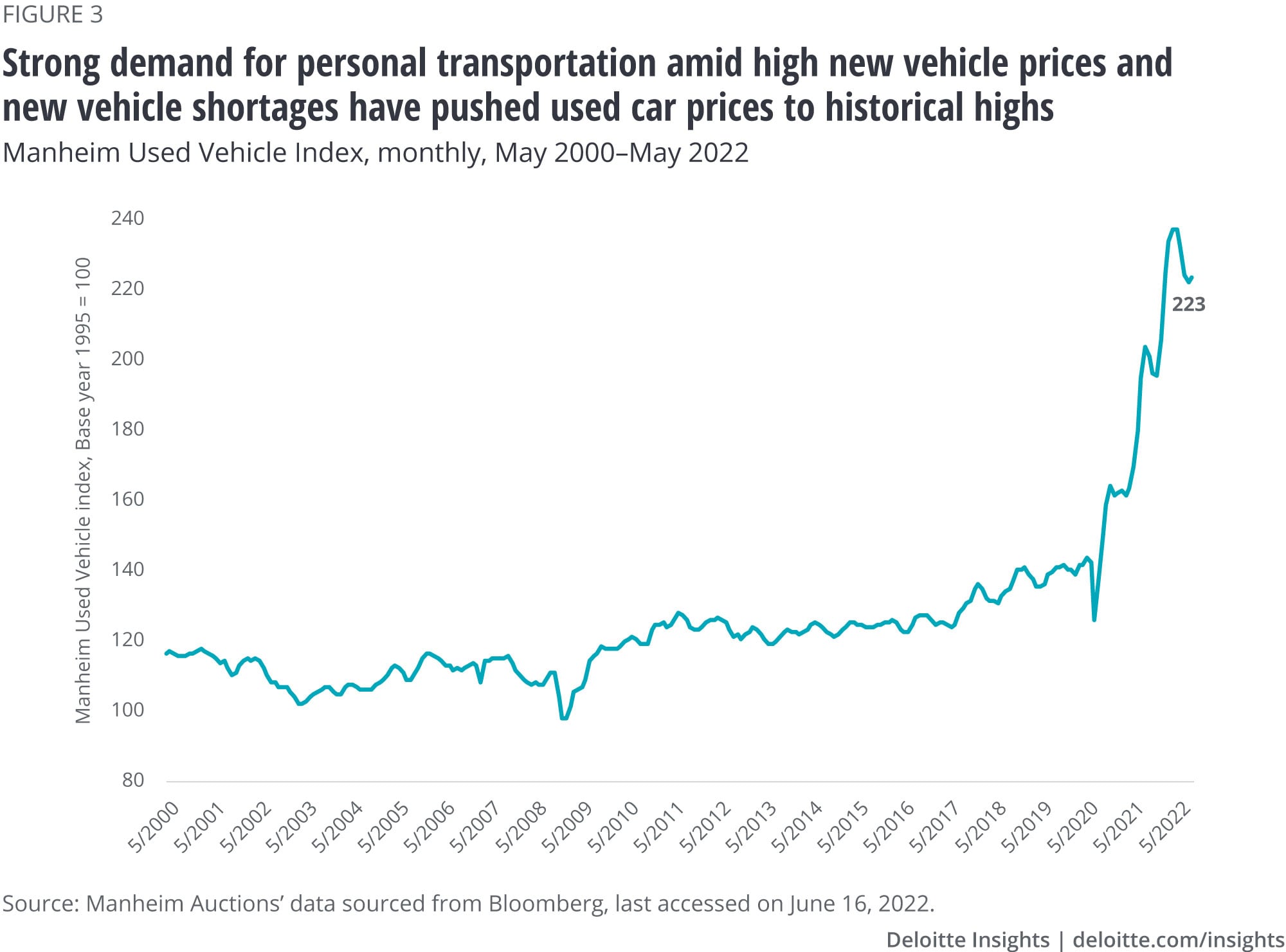

Given the strong demand for personal transportation and all-time high new vehicle prices, cost-conscious consumers flocked to used vehicles, only to be met with similar price hikes. Though used vehicle prices have cooled somewhat in the last three months after touching record highs in January, they remain at historically high levels (figure 3).

Together, new and used vehicles accounted for 9.2% of the US Consumer Price Index (CPI)10 and are one of the main reasons for the recent surge in inflation. Overall, rising vehicle prices present a very real risk to car demand. In recent months, financial sentiment has already started to flash warning signals in the United States. More than eight in 10 (84%) Americans are now concerned about rising prices for everyday purchases—up from 72% in September. Concern around savings and credit card debt are on the rise. And the since September, the number of Americans delaying large purchases increased from 42% to 53%.11

So, what does this mean for automotive sector stakeholders?

What started as an initial blip in vehicle production has lasted far longer than first anticipated and has had many unexpected impacts on the global auto sector. At the same time, the world continues to reopen, and employees are returning to the office. This may cause some to revert to old mobility patterns, kickstarting a return to public/shared transportation as people are jolted back to the harsh reality of the traffic congestion that plagued densely populated urban centers in prepandemic times. As we emerge from these tumultuous times into a “new normal,” industry stakeholders will likely be eager to understand what consumers will be happy to leave behind and what they are prepared to carry forward.

{kind=link}

{kind=link}

{kind=link}