{kind=link}

{kind=link}

The shape of consumer spending has been saved

The authors would like to thank Marcello Gasdia and Dinesh T for their significant contributions to this article.

Cover image by: Natalie Pfaff

Splurge or save? In recent months, consumers worldwide likely feel caught between two minds. As global anxiety around the pandemic wanes, many are eager to spend on sorely missed experiences like travel, restaurants, and entertainment. But built-up pandemic demand is hitting hurdles in the form of spiking inflation and persistent headlines warning of a potential global recession.

Which way consumers are leaning—spend on much-deserved joy or save for potentially more challenging times—can depend on where you look across the world.

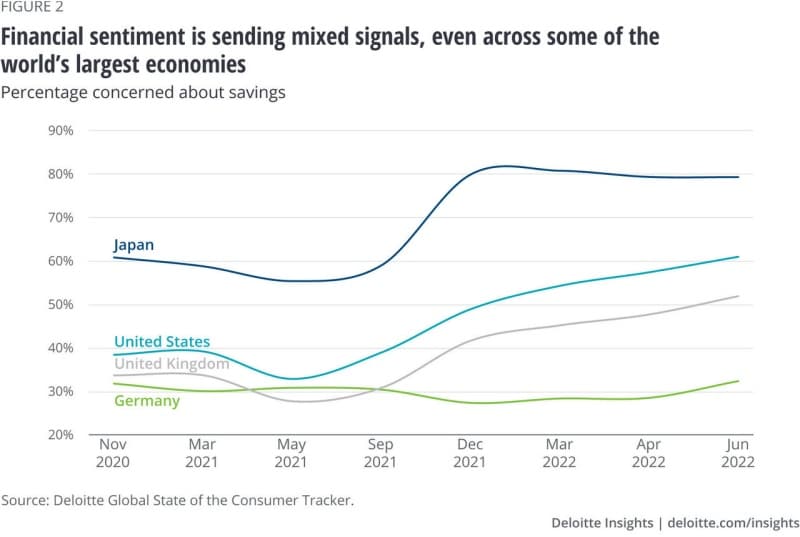

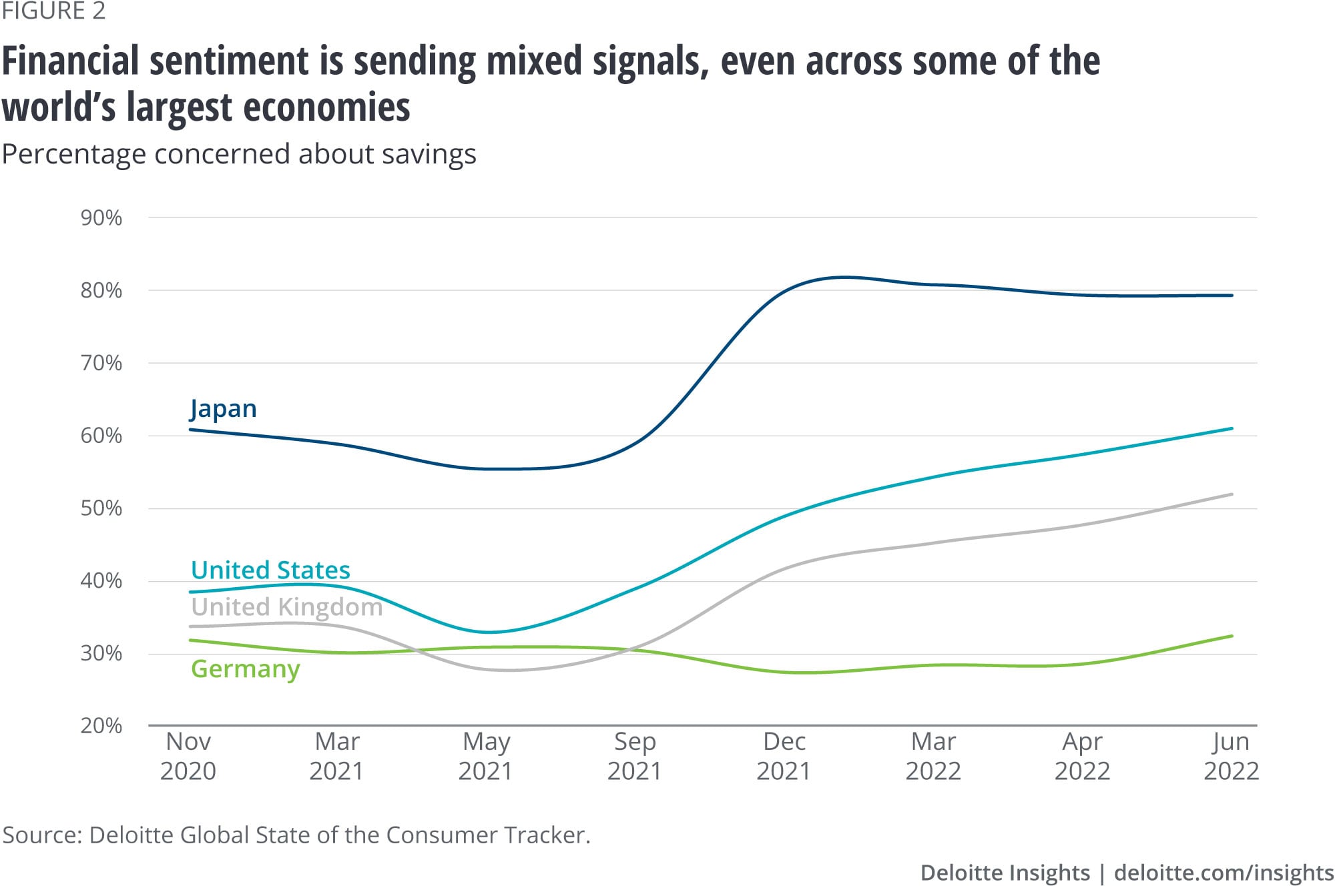

For example, spending intentions are beginning to paint a picture of dwindling consumer confidence in the United States and the United Kingdom. Considering their upcoming monthly budgets, the share of wallet consumers plan to allocate toward more discretionary categories has been slipping since September 2021 (figure 1). Planned pullbacks are more substantial among Americans, even hitting less discretionary categories like clothing and personal care. In both countries, housing (including utilities) and transportation remain the only categories grabbing a larger share of consumers’ wallets lately.

The rising cost of living is a likely driver of shifting spending intentions. Inflation has been high in the United States and the United Kingdom, hitting roughly 9% between May and June.1

Consumer confidence appears a bit stronger in some countries, such as Japan, where inflation remains relatively low.2 Compared to last September, Japanese consumers in June planned to allocate a slightly larger share of their monthly budgets toward categories like recreation and entertainment, restaurants, and leisure travel (figure 1). Over the same nine-month period, the Bank of Japan's Consumer Spending Index for Real Services jumped 10 points, from 88 to 98.3

The trends suggest that built-up pandemic demand is still winning the battle over saving in some countries. In Japan, the absence of spiking inflation is important to consider. At face value, it makes sense that consumers would feel more comfortable spending freely in a more price-stable environment—but the drivers behind spending are still murky. Consumers may still be reacting to global inflation more broadly, diverting more cash towards discretionary categories now with the expectation that prices could rise in the near future.

But there are also countries with high inflation, where spending intentions haven't changed much. In Germany, for example, inflation hit 8% in May—roughly on par with the United States and the United Kingdom.4 Discretionary spending intentions, however, have yet to show signs of budging (figure 1).

Globally, consumers appear to respond differently to strong inflation and the bleak economic outlook. Financial sentiment and key differences at the country level could offer some insight as to why.

Even across the world's largest economies, consumers’ capacity to absorb financial pressures like inflation and recession likely varies.

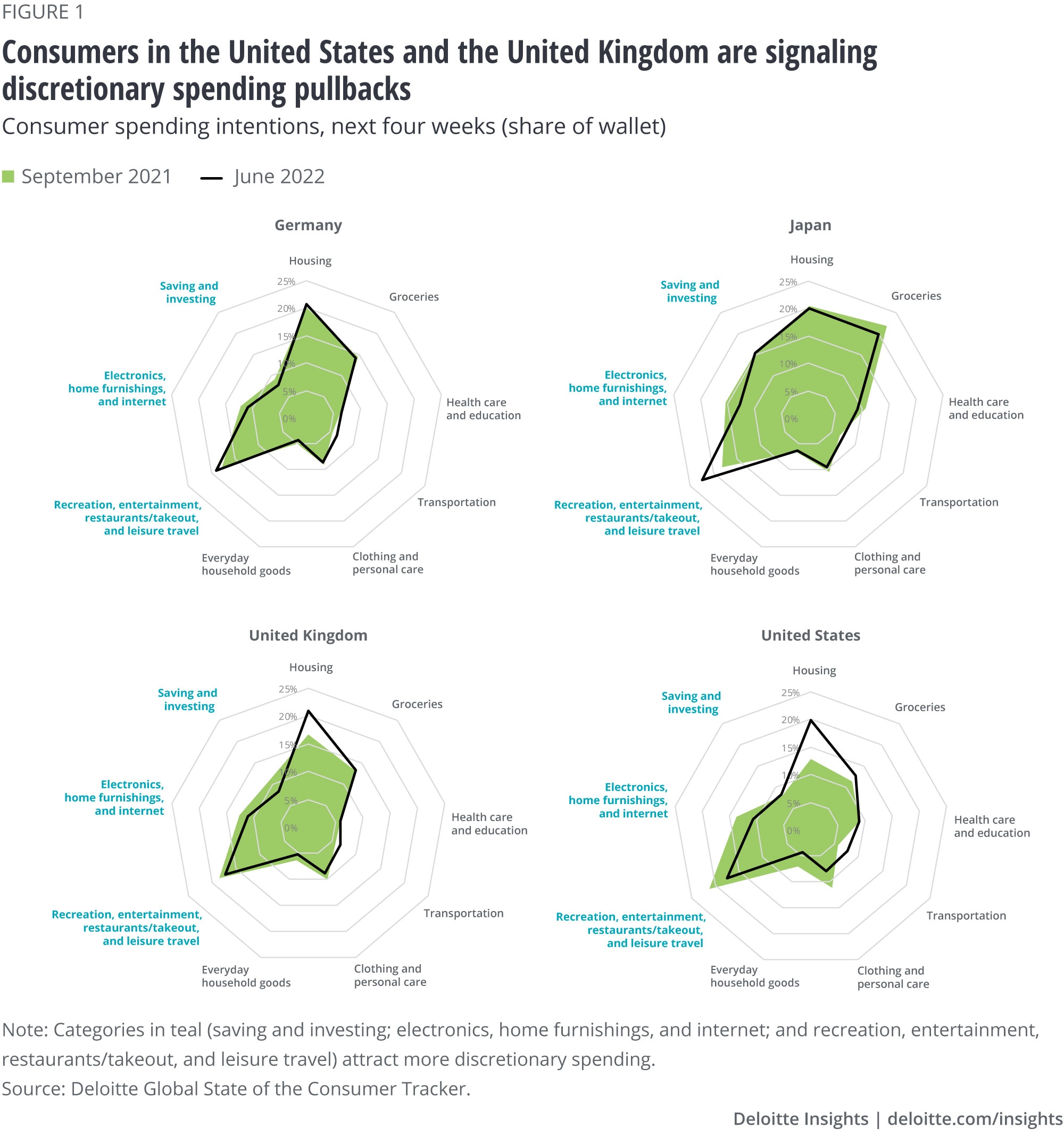

Financial sentiment among Americans, for example, has been flashing warning signals for over a year. In May 2021, the national Personal Savings Rate stood near record highs.5 At that time, only 33% of Americans expressed concern about their level of savings (figure 2).

But rising inflation quickly exposed a shaky financial footing. As rates climbed, in tandem with sunsetting pandemic relief programs, savings concerns followed suit. Nearly two-thirds (61%) of Americans now express concerns about their savings—with the Personal Savings Rate sitting at only 5%. Savings concern among consumers in the United Kingdom is following a similar trend.

More recently, concerns about credit card debt are rising among Americans (48%).6 And some trends, such as the number of lower-income Americans struggling to make upcoming payments, have been steadily increasing since the pandemic’s early days.7

In stark contrast, financial sentiment in Germany appears considerably stronger. Only 32% of German consumers express savings concern—a figure that’s remained steady for nearly two years. Additionally, fewer consumers in Germany cite concerns around credit card debt (32%).8 But compared to the United States, credit card use is generally less prevalent in Germany.

Beyond financial well-being, key differences at the country level could also be influencing consumers’ intention to splurge or save:

Pandemic-influenced consumer patterns rendered many historic demand models obsolete.

Persisting inflation; rising interest rates; ongoing supply-chain disruption; and slowing economic growth—these new pressures will continue to shape already altered consumer demand and preferences.

Complicating factors will be that demand and preferences will evolve unevenly and at different rates across the globe. Understanding consumers’ financial well-being may become key to regional and local market trends.

For example, income bifurcation has shaped consumer spending in the United States for quite some time. In turn, it has shaped strategies and business models. For example, revenue growth among price-based and premier retailers outpaced more balanced retailers for years.14 Airlines have been busy segmenting their cabins to create a broader mix of high- and lower-priced fares.

Just as the pandemic challenged conventional wisdom, consumer companies should expect the confluence of economic pressures to challenge the typical recession playbook equally. Consumer companies will likely want to include consumer financial well-being and increasingly granular consumer behavioral data in their models to remain agile and ahead of a dynamically evolving environment.