Achieving gender equity in the fintech community has been saved

Achieving gender equity in the fintech community Enlisting key stakeholders to drive change

11 minute read

02 October 2020

Despite some progress, the vast majority of fintech founders are still men. But it doesn’t have to stay that way. Learn how key stakeholders in the financial industry could create opportunities for women and for growth.

Key messages

A dearth of women founders

In the world of startups, the global fintech founder community is still dominated by men, with women making up just 7% of the total pool.1 If further progress is to be made, investors and the financial services industry alike will need to reconsider the efforts they’ve made before a more financially and socially equitable future can be realized.

Learn more

Explore the full Within reach? collection

Explore the Financial services collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

In this report, the fourth in our Within reach series, we study formation and fundraising trends in the fintech industry over the last 10 years across three categories of startups: women-founded, men-founded, and cofounded (startups with founders of both genders). Based on preliminary numbers, we also analyze the impact of COVID-19 on fintech funding activity during the first half of 2020 across the three categories.

The gender gap in funding is especially notable during times of uncertainty, such as the current pandemic and its economic aftermath. This is because women founders, perhaps because of the hardships they face in accessing funds, appear to be resilient and capable of generating higher returns on investment.2 Yet, in many cases, they are not provided equal access to opportunity.3 As with other industries, women in the fintech community are seeking opportunities to fill unmet needs. They are generating innovative ideas and creating solutions based on their own disappointing or frustrating financial services experiences.4 Ellevest, Tala, Policygenius, CapWay, and Honeybee were all founded to tap into consumers’ unmet needs.

Having greater representation of women and support from the fintech founder community would likely unleash more successful new ideas, products, and services.5 Similar to how the fintech industry blossomed after the 2008 financial crisis, the effects from COVID-19 and its disruption to the business environment could help level the playing field and offer a host of new opportunities for women entrepreneurs.

To make that aspiration a reality, though, three key stakeholders in the fintech ecosystem—investors, founders, and financial institutions—will have to join forces and commit to change. They will need to work together to help enable equal access to all forms of capital: human, financial, and social.

“This Deloitte report calls attention to a gaping investment opportunity to fund and collaborate with female founders of fintech enterprises. First, however, these women need to be highly visible to investors and networked to each other. Industry associations and organizations can play a helpful role with this, both in underscoring the mandate for greater diversity in investment capital placement and in elevating the female founder’s exposure within the industry.”—Amanda Pullinger, CEO, 100 Women in Finance

Slow steps in the right direction

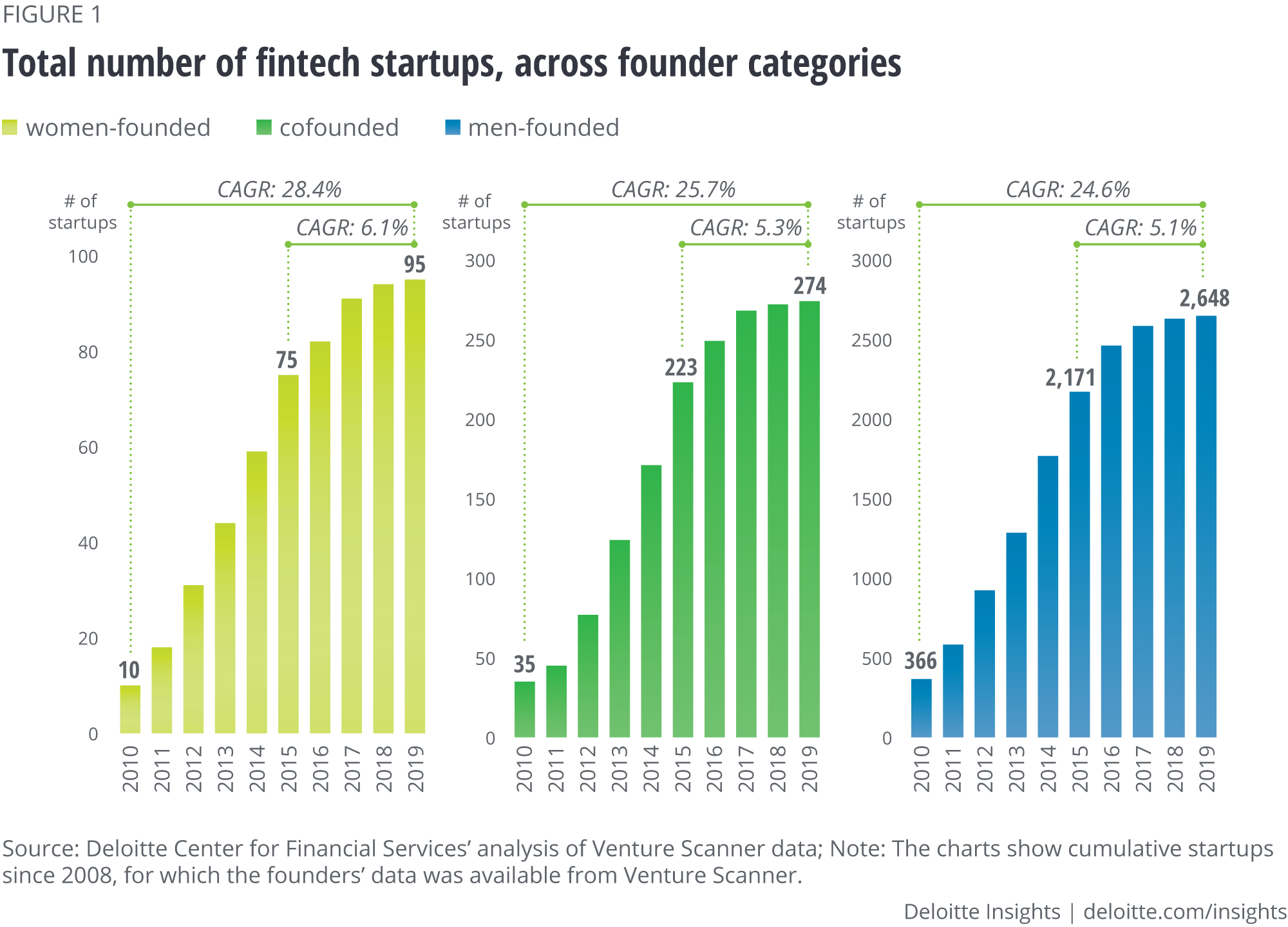

The fintech industry has made slow but steady progress increasing the number of startups founded by women. Since the start of this decade, women-founded and cofounded fintechs have grown at a slightly faster clip compared to startups founded only by men (figure 1; see sidebar, “Methodology” for more details): They reached 369 in 2019, growing eight-fold, while men-founded startups grew seven-fold. As a result, fintechs with women as founders or cofounders now comprise 12.2% of the total startups vs. 10.9% a decade ago. However, this is limited progress indeed. Startups with all-women founding teams accounted for 3.1% of the pool in 2019, a small improvement from 2.4% in 2010.

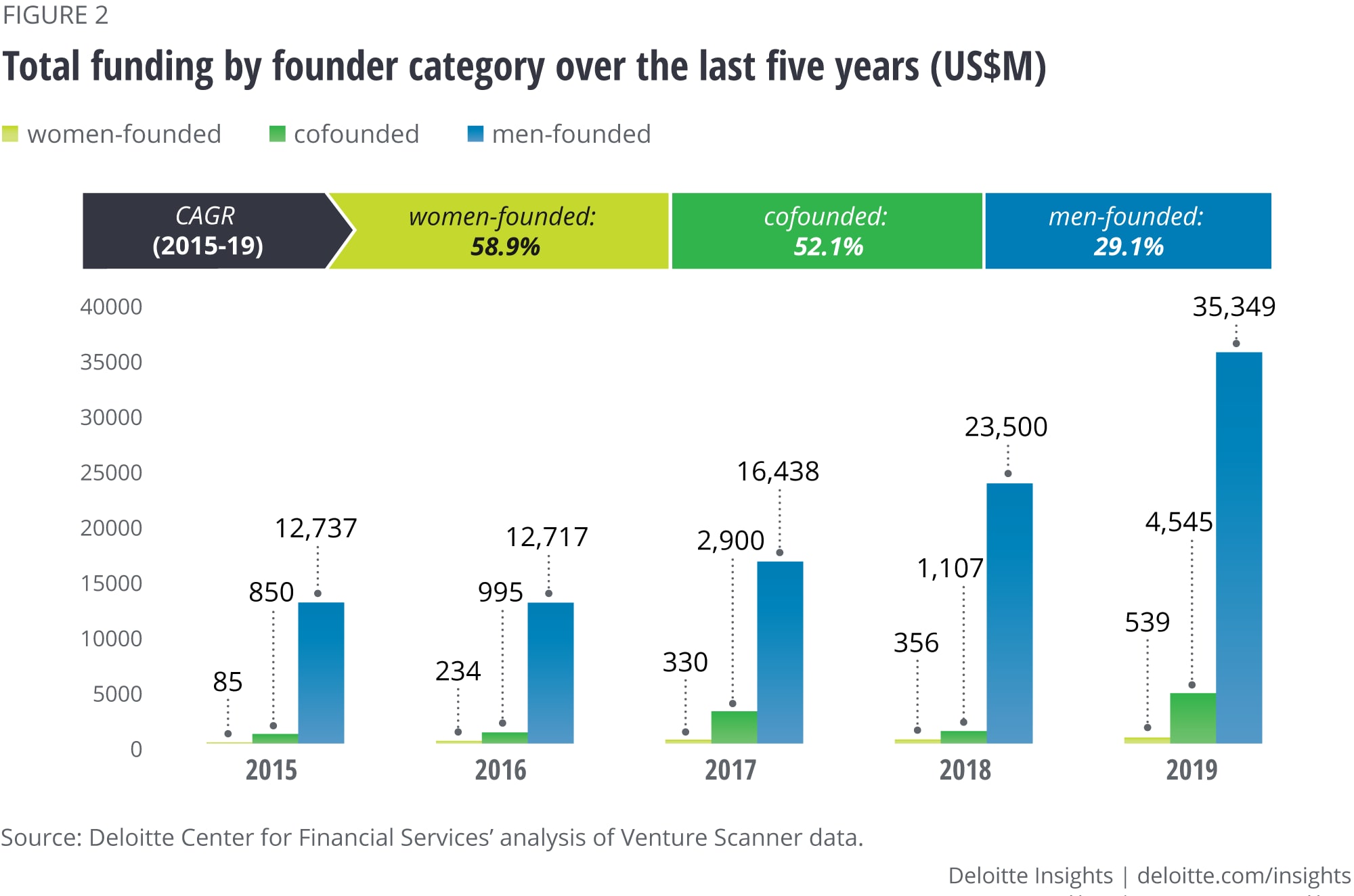

When gauging success in achieving gender equity, another key metric to evaluate is how the needle has moved on startup funding. Encouragingly, the numbers also show a shift in the investing landscape, with more dollars being directed toward women-founded and cofounded fintechs. Startups founded by all women teams have recorded a consistent increase in funding since 2014. Moreover, during the last five years, funding for women-founded startups grew at a compound annual growth rate of 58.9%, while funding for men-founded grew by 29.1%.

In fact, 2019 broke all records (figure 2):6 Startups founded and cofounded by women garnered a total of US$5.1 billion in funding—almost 60% of the total capital raised by these categories since 2009.7 Of that total, US$540 million was invested in startups founded only by women, up from just US$85 million in 2015. However, it should be noted that Starling Bank and Tala accounted for 60% of the total investment in fintechs with women-only founding teams in 2019. Similarly, the cofounded startups Kabbage and Lendable raised a combined US$2 billion during the year.

As a proportion of the total, just 1.3% of the US$40 billion funding raised in 2019 went to companies founded only by women, up from 0.6% (of US$14 billion) in 2015. Meanwhile, startups with at least one woman cofounder witnessed a more pronounced increase. Their share of the total investment pot rose by five percentage points over the last five years, to 11.2%—an improvement, but still a comparatively small share of overall funding.

Of course, women are starting up companies across all industries, and they are having some greater success in drawing investor interest than those looking to break into the fintech world. Specifically, women-founded startups have secured 2%–3% of overall funding during this decade,8 while women-founded fintechs have raised only one percent of total fintech investment. That said, when the overall percentage of women founders, including cofounders, is taken into account, fintech’s funding share is on par with that of other industries.

The long road ahead

Factors contributing to the rise of women in the startup world include an increased focus on gender equity, growth in the number of women entering the finance and technology industries, modest growth in the number of women in decision-making roles at VC firms, and greater focus on women-oriented mentorship networks.9 To understand more, we analyzed 36 VC firms with a mandate to invest in women founders. Of the 371 women-founded and cofounded startups covered in our study, 40% attracted investments from these firms. Among those startups, 27% were founded solely by women.

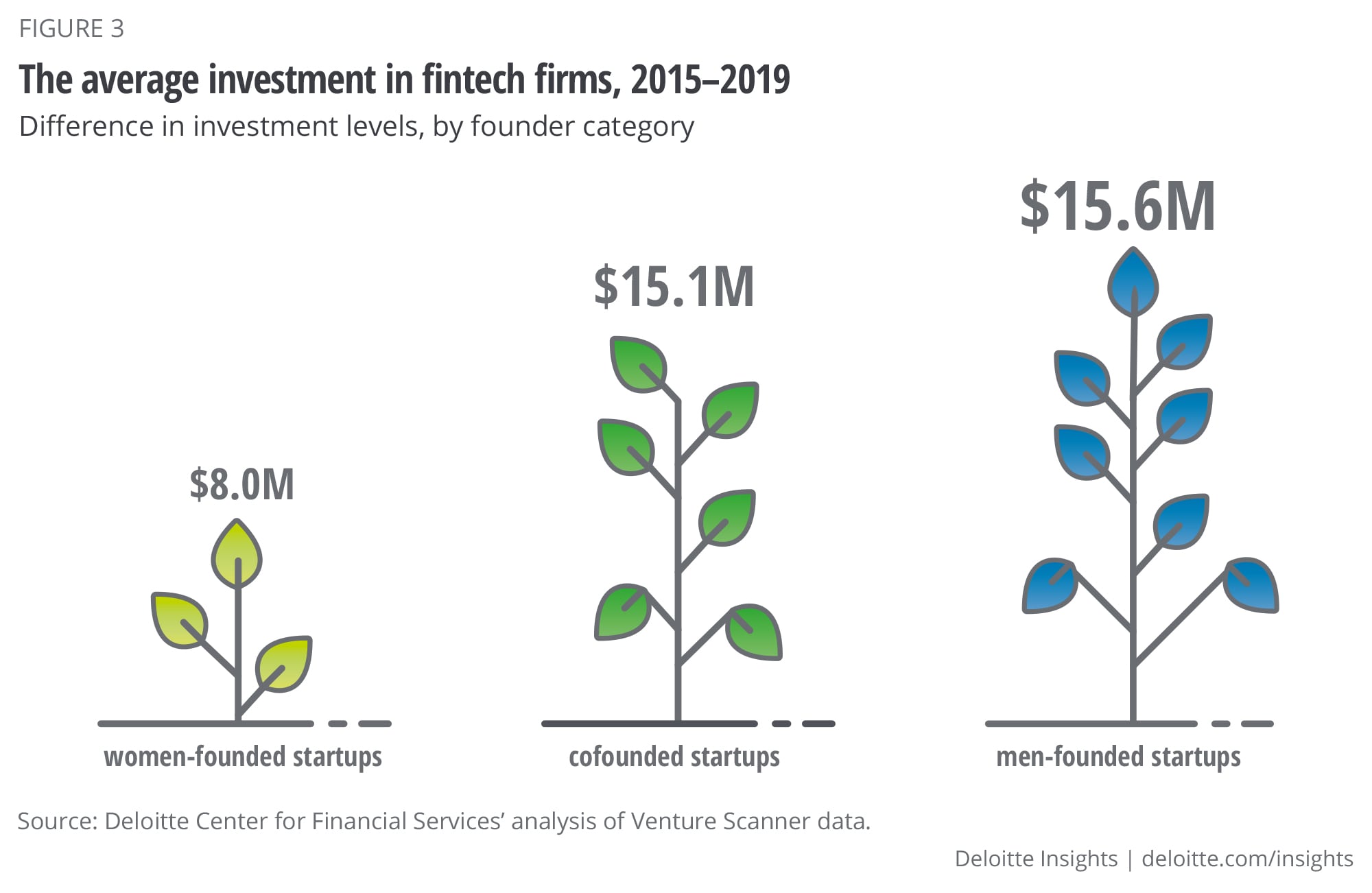

Despite this progress, inequitable funding, along with low representation in the founder community, remain key impediments for women in the fintech industry. A comparison of average funding over the last five years revealed that women-founded fintech startups raised 50% less capital than startups founded only by men. But founding teams with both men and women averaged just 3% less funding (figure 3).

One reason for this disparity could be gender bias in the VC pitching process. A 2014 study by Harvard Business Review concluded that investors often make funding decisions based on gender. The study revealed that, after listening to identical pitches given by men and women entrepreneurs, investors preferred pitches made by men.10 Another study found that venture capitalists often posed different questions to men and women entrepreneurs. Men were more likely to be asked about the potential for gains, while questions toward women focused more on the potential for losses. Interestingly, this happened whether the investors were men or women.11 Bias can take other forms as well, such as when women entrepreneurs are encouraged to bring men counterparts to investor meetings.12

Inequitable funding and lack of representation could be missed opportunities for investors. Women-founded or cofounded teams are more likely to understand the needs of women—an essential yet underserved customer segment for financial services in general.13 The VC industry, however, should continue to prioritize investing in women-founded and cofounded startups.14

A call to action

What could the three key stakeholder groups do to help improve outcomes and create more gender diversity in the fintech founder community? Below are actions investors, women founders, and financial institutions can take.

- Investors

- Widen the investment lens. Investors, especially venture capitalists, have the power to make meaningful change by coming to the table with an unbiased view. While making investment decisions, investors need to ask themselves: “Are we letting unconscious bias get the better of us?” and “Are we doing enough to understand the opportunity— product and market segment—before us?”

- Put the multiplier effect to work. Diversity within the VC community can help bring fresh perspective and accelerate the pace of change. Our earlier research found that with each woman added to the C-suite, there was a threefold increase in the number of women in senior leadership.15 Likewise, women VCs are twice as likely to invest in companies with a woman founder or cofounder at the earliest stage of company development.16 However, currently, just 12% of decision-makers at VC firms and angel groups are women.17 The investment community should be helping more women get to the other side of the table.

- Women founders

- Create the next big thing. Many business opportunities will unfold as the pandemic reshapes our future. With technology being a clear winner, women in fintech should actively scout and be ready to capitalize on the next big idea.

- Consider alternative sources of capital. Women are at an apparent disadvantage when it comes to traditional fundraising. But crowdfunding—raising small investments from a group of amateur investors—can be a very useful source of initial capital, especially during times like this, when securing traditional funding may be increasingly challenging. Moreover, these platforms often tend to favor women founders, whom participants in a recent study perceived as being more trustworthy.18

- Seek and develop mentorship opportunities. Peer-to-peer networks, sponsorship, and mentorship programs often help women achieve greater success, faster. Women founders should seek access to multiple mentors at an early stage. Meanwhile, they can also pay it forward by mentoring other women. Having gone through the fundraising process, experienced founders should provide coaching and guidance to early stage founders.

- Financial institutions

- Bolster gender diversity initiatives. Many institutions have incorporated gender diversity efforts into their investment strategies. For instance, Goldman Sachs’s Launch with GS initiative aims to invest US$500 million in gender-diverse companies and investment managers.19 Likewise, JP Morgan, in partnership with The Vinetta Project, recently launched an initiative to support women founders by providing them greater access to capital, networking opportunities, and advisory services.20 More initiatives such as these are needed for women entrepreneurs to thrive.

- Cultivate networks. Large financial institutions can play a key role in cultivating valuable networks. They can help women founders access an established network or create an informal one by introducing them to industry leaders, investors, and other women founders.

- Seek partnerships with women-founded companies. Financial institutions regularly partner with fintech companies. They can create more equitable opportunities by actively seeking out women-founded startups for these partnerships.

COVID-19: Catalyst for growth?

The 2008 financial crisis created huge demand for faster innovation in the financial services industry, which likely contributed to the rise of the fintech community. Could a similar disruption in the business environment due to COVID-19 be an opportunity to level the playing field for women?

When facing a global economic downturn, every dollar is important. As companies aim to recover from the financial impact of the COVID-19 pandemic, they will need to run a tight ship while exploring all viable options for growth. This should include investing in women entrepreneurs, who have proven themselves to be as capital-efficient and capable of generating high returns as are men, if not more so.21 And a recent study of executives across genders found that women were also perceived to be more innovative and resilient—important skills during these challenging times.22

“The pandemic can be an opportunity for change and catalyst for growth for women in fintech, as indicated in Deloitte's research. Female fintech founders have excelled during this crisis, in part because of their ability to handle uncertainty, collaborate with others in the ecosystem, and home in on the needs of the customer. Peer-to-peer networks, where female founders exchange ideas, explore business opportunities, and importantly, motivate and inspire one another, can speed the rate of change.”—Carole K. Crawford, CFA, managing partner, fincap360 and Chair, 100WFinTech Committee

So far, however, this hasn’t happened: Women-founded and cofounded startups appear not to be faring well during the pandemic. In the first six months of 2020, they raised a total of US$875 million in funding across 20 startups compared with US$3.5 billion seen in the first half of 2019 across 56 startups. Meanwhile, 243 men-founded startups raised around US$12 billion in the first half of 2020, compared with US$17 billion raised over the same period in 2019 across 473 startups.

Investors should take note of this and act accordingly. Otherwise, they could risk missing out on a key growth opportunity.

Methodology

In this report, we defined “fintech” as the ecosystem of (perhaps initially) small technology-based startup firms that provide financial services to the marketplace or primarily serve the financial services industry. The analyses in this report are based on data, including founders’ classification, from Venture Scanner.

Our study covers 3,017 global fintech startups, approximately 53% of the broader fintechs we track, for which founder data was available from Venture Scanner.

We use the following terminology in this report:

- Women-founded startups: Startups with only women founders.

- Men-founded startups: Startups with only men founders.

- Cofounded startups: Startups with both men and women on the founding team.

Fintech companies studied for this report are limited to those founded since 2008. All data, except that for founders, are as of June 30, 2020. Data on founders are as of May 2020. Note that we excluded The We Company (or WeWork), a cofounded startup, from our funding analysis as it was an outlier, with approximately US$20 billion in total funding.

About the Deloitte Center for Financial Services

The Deloitte Center for Financial Services, which supports the organization’s US Financial Services practice, provides insight and research to assist senior-level decision-makers within banks, capital markets firms, investment managers, insurance carriers, and real-estate organizations. The center is staffed by a group of professionals with a wide array of in-depth industry experiences as well as cutting-edge research and analytical skills. Through our research, roundtables, and other forms of engagement, we seek to be a trusted source for relevant, timely, and reliable insights.

Get in touch

- Alaina Sparks

- US fintech leader, Global Financial Services Ecosystem & Alliances program leader Managing director

- Deloitte Services LP

- alasparks@deloitte.com

- +1 415 783 4838

Related content

Explore the Financial services collection

-

The path ahead Article4 years ago

The path ahead Article4 years ago -

T. Rowe Price's Céline Dufétel on overcoming the confidence gap Podcast4 years ago

T. Rowe Price's Céline Dufétel on overcoming the confidence gap Podcast4 years ago -

US consumer payments in a post-COVID-19 world Article4 years ago

US consumer payments in a post-COVID-19 world Article4 years ago -

TransUnion's Swati Shah on moving from intention to action Podcast4 years ago

TransUnion's Swati Shah on moving from intention to action Podcast4 years ago -

Confronting the crisis Article4 years ago

Confronting the crisis Article4 years ago -

Reshaping the cybersecurity landscape Article4 years ago

Reshaping the cybersecurity landscape Article4 years ago