Global financial well-being: A robust recovery losing momentum

Consumers have demonstrated resilience in the face of global challenges. But are they hitting a collective turning point?

Leon Pieters

Anthony Waelter

Stacey Winters

Michel Elmaleh

Rajeev Singh

Stephen Rogers

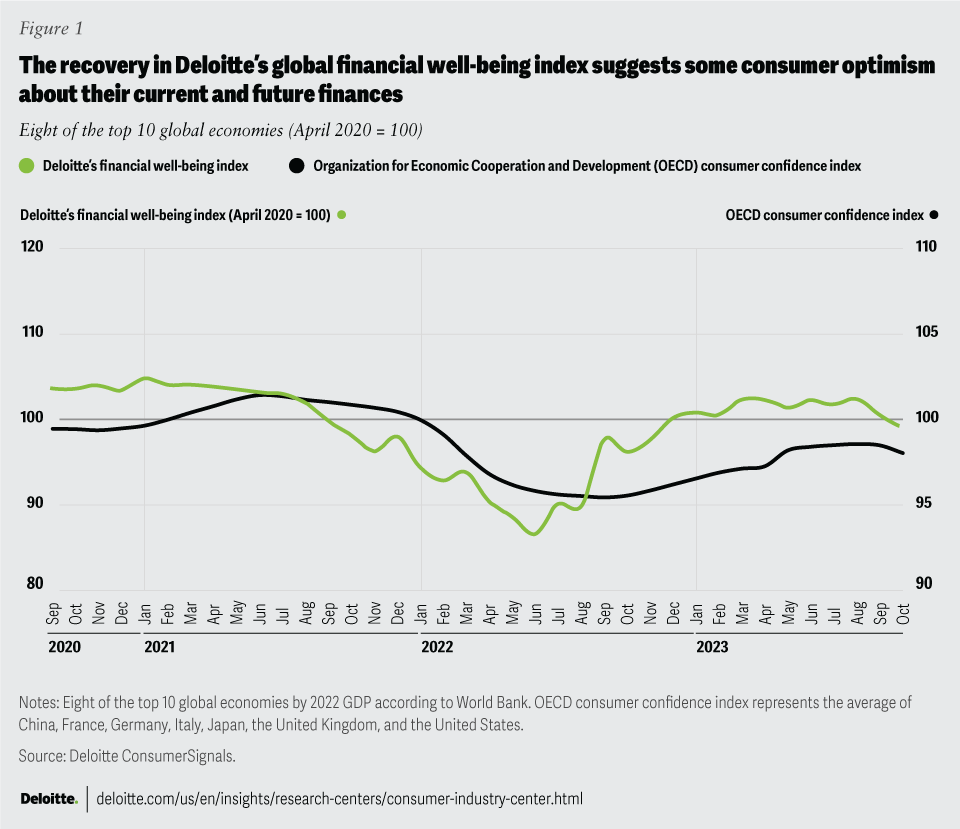

Deloitte’s financial well-being index (FWBI), which measures consumer sentiment across six dimensions of financial health, posted a solid recovery across many of the world’s largest economies1 since the summer of 2022 (figure 1; see sidebar, “Deloitte’s financial well-being index”).

Given the barrage of global challenges consumers have faced in recent years, the broader rebound in financial well-being speaks to incredible resilience.

In recent months, however, the index suggests that consumers are losing financial steam.

Financial well-being held up reasonably well during the early COVID-19 pandemic uncertainty of 2020 and early 2021 (figure 1). While consumer confidence (which also incorporates perceptions of external economic conditions) was shaken, consumers’ feelings about financial health didn’t wholly erode. And there may be good reasons why. Across 2020 and 2021, the world’s largest economies2 spent more than US$8 trillion on pandemic stimulus programs, offering a lifeline to many.3 At the same time, consumers had limited places to spend, helping savings rates soar in many countries.4,5 Amid pandemic lockdowns, the index moved slightly upward, hitting its three-year high of 104.8 in January 2021, as vaccines started to roll out across the globe.

{kind=link}

To some extent, global financial well-being was likely being artificially propped up. As stimulus programs sunseted and inflation climbed, sentiment fell quickly and sharply for a year (figure 1). The global index bottomed in June 2022 at 86.7; the same month, inflation rates peaked in the United States and Canada, with many countries quickly following suit.

Easing inflation brought a collective sigh of relief. And global financial well-being sentiment quickly responded. As the inflation rate eased in more countries, the global index climbed, hitting 102.4 in March 2023.

A subset of the six underlying index metrics drove the recovery. From June 2022 to March 2023, the percentage of global respondents concerned about making upcoming payments dropped from 31% to 22%.6 Similarly, the percentage of those concerned about their level of savings fell from 56% to 47%.7 Optimism about the future also improved slightly, with the percentage expecting their financial situations to improve in the next year increasing from 28% to 33%.8

Warning signals have emerged in recent months, however. After March, the index’s upward momentum began to stall. And from August to October, a sharp drop dragged the global index down to 99.1, a new low for 2023.

Pegged to the onset of the pandemic in April 2020, current values should perhaps well exceed the baseline to signal a proper recovery. And getting there looks to be an uphill battle. Easing inflation’s early psychological boost has likely run its course. More optimism is needed for the index to continue its run-up. And when global economic forecasts only point to slowing growth, those improvements could be hard-won.

Deloitte’s financial well-being index

Deloitte’s financial well-being index (FWBI) captures changes in how consumers feel about their present-day financial health and future financial security. Unlike consumer confidence indices, which often focus on consumer opinion about economic conditions (that is, health of the economy or labor market), financial well-being focuses on the consumer’s own financial experience, where they’re the experts.

Financial well-being is measured across six dimensions of financial health:

- Confidence in the ability to meet current financial obligations

- Comfort with level of savings

- Income relative to spending

- Delays in making large purchases

- Assessment of current financial situation relative to the prior year

- Expectations of financial situation for the year ahead

Higher index values indicate stronger financial well-being.

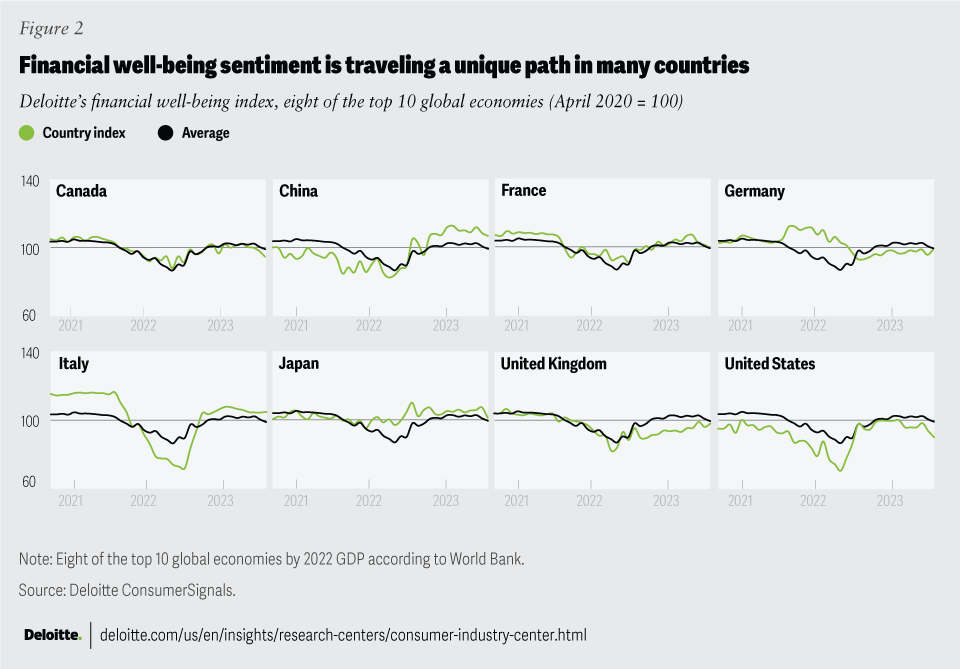

Traveling unique paths

Financial well-being mirrors global sentiment in some countries, such as France and Canada (figure 2). But many other countries are traveling slightly different paths.

{kind=link}

Germany: Germany was the only country to climb as the global average declined in late 2021, suggesting a financially stronger footing for German consumers. The German economy did grow by 1.6% in the second quarter of 2021, thanks mainly to domestic consumer spending as pandemic lockdowns were relaxed.9 But ultimately, Germany’s uptick was short-lived. As soon as inflation spiked, financial sentiment quickly joined other major economies in a downward trend. Germany’s index low of 92.9 coincides with inflation’s local peak of 8.8% in October 2022.10

Financial well-being sentiment in Germany has stagnated for much of 2023. Relatively high inflation rates in Germany could be playing a role. The impact of higher interest rates to tackle inflation continues to put additional pressure on households and businesses.11

Japan: Conversely, Japan has remained incredibly steady, with barely any peaks or valleys. Perhaps not coincidentally, inflation rates in Japan have been relatively tame, rising to only 3% to 4% for a brief period in late 2022 before showing signs of easing.12 More recently, Japan’s economy has shown signs of strength, recording growth of 6% in the second quarter of 2023, its third consecutive quarter of expansion.13

However, some warning signals remain. Economic observers report that Japan’s recent economic expansion was fueled by solid exports and inbound tourism, with a decline in domestic consumption leaving room for concern.14 Japan remains a country to watch, particularly because its index dropped six points to a new annual low in October.

Italy: Italy’s index is a bit of a rollercoaster. Extreme early highs gave way to steep lows. Early highs may be driven by the index’s April start date. In April 2020, when daily COVID-19 deaths in other countries were only starting to peak, numbers in Italy were already declining.15 Early on, the index may have caught Italian consumers during a strong upswing in sentiment from a very fragile low.

Italy’s index dropped to 72.2 in the summer of 2022, a low only matched by the United States. High inflation could be among the drivers. Inflation peaked in Italy at 12.6%, the highest rate across the world’s top 10 economies. Easing inflation rates throughout 2023 has likely helped boost financial sentiment. However, the index has struggled to sustain upward momentum in recent months.

United Kingdom: Relatively high inflation likely weighed heavily on UK consumers. For much of 2022 and 2023, the UK index traveled well below the global average.

Months of steady increases helped the UK index close the gap with the global average in October as inflation rates simultaneously fell to a two-year low.16 The momentum could continue if inflation is further tamed.

United States: The United States has the weakest index line across major economies. Trillions in pandemic stimulus likely helped to alleviate some financial stress from lockdowns in 2020 and early 2021. Even so, the US index traveled well below the global average. The US index tumbled further as stimulus programs sunseted and prices simultaneously began to climb. The index hit a low of 70.7 in June 2022, coinciding with peak inflation of 9.1% that month.

Consumer sentiment quickly recovered as inflation eased. But the upward trajectory was short-lived. The index remained flat throughout 2023, and has started dipping again in recent months. Overall, the three-year index conveys some financial fragility among Americans.

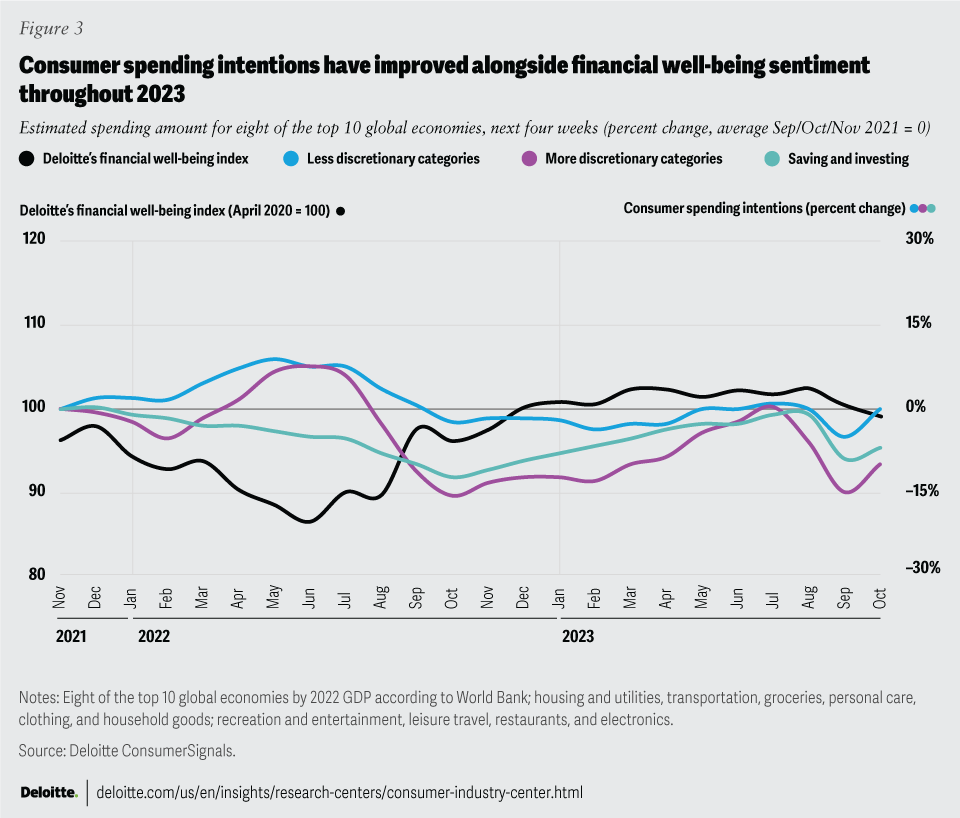

Spending with rationality (and maybe some emotion, too)

The relationship between financial well-being sentiment and spending confidence hasn’t always played out logically over the past few years. Spending confidence and financial well-being sometimes moved in tandem. Other times, there’s evidence of consumers spending with more emotion, potentially driven by built-up pandemic demand.

When financial well-being sentiment started to weaken in 2021, consumer spending intentions (or how much consumers estimate spending in the month ahead) fell too, particularly across the more discretionary categories (figure 3).

{kind=link}

However, as global inflation climbed and financial well-being sentiment weakened further, consumer spending intentions unexpectedly increased across more and less discretionary categories. Rising spending intentions for less discretionary categories like housing and utilities, transportation, and groceries perhaps aren’t too surprising. Consumers were easing into the shock of surging prices. And many had little choice but to pay more.

But rising spending intentions for more discretionary categories amid weakening financial well-being sentiment may be counterintuitive. Spending intention data at the category level reveals that leisure travel drove the trend almost exclusively.17 2022 was the first summer in three years that consumers likely felt they had the pandemic firmly in the rearview mirror. And that pent-up demand likely led to an explosive summer travel season. International air arrivals in some of Europe’s most popular leisure destinations almost reached prepandemic levels.18 Some destinations like Greece and Turkey even exceeded them.19

Falling spending intentions for savings suggest consumers were stretching their wallets to afford it (figure 3). And ultimately, the trend was short-lived. Once summer 2022 ended, spending intentions quickly came crashing down.

By late 2022 and early 2023, sustained months of easing inflation paved the way for a recovery in financial sentiment. And spending intentions soon followed suit. Climbing for roughly 10 months, spending intentions for savings and more discretionary categories returned back to baseline during the summer of 2023.

More recently, financial well-being and spending intentions have started heading south again. After a prolonged recovery, the trend suggests global consumers have collectively reached yet another turning point.

Where to from here…

The resilience shown by consumers is encouraging. But warning signals remain. As the recovery in global financial well-being sentiment starts to stutter, weakening spending intentions reinforce the theme of uncertainty among consumers.

With the boost from easing inflation likely already factored into the global index, improvements from here will probably be a more arduous uphill climb. While some of the index’s underlying metrics, such as financial expectations for the year ahead, are more susceptible to emotionally driven swings driven by factors like gas and energy prices to stock and job market fluctuations, others boil down to hard dollars and cents. For example, meaningful improvements in a population’s ability to make upcoming payments or earn more than they spend likely require more substantiative progress in economic conditions.

As a result, many consumers may have hit their limits with price increases, their pandemic savings, and budget stretching. At the same time, the global economy is shifting from goods back to services. In this environment, select consumer products companies may need to slow their price-taking or face declining volumes. The automotive market may face an affordability challenge. And, while many consumers continue to travel, it’s a sizeable discretionary expense they might curtail in a pinch.

Visit Deloitte’s ConsumerSignals Interactive Dashboard for global monthly updates to Deloitte’s financial well-being index and underlying metrics, as well as key consumer insights across retail, consumer products, automotive, and travel.