{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Consumers navigate financial ups and downs has been saved

The authors would like to thank Jim Eckenrode and Marcello Gasdia for his contributions to the article.

Cover image by: Natalie Pfaff

When Americans feel better about their finances, many would expect spending confidence to follow suit. But over the past year, financial well-being in the United States tells a story of resilience and recovery, while spending intentions tell one of calculation and caution.

For insight into these seemingly opposing trends, it’s helpful to look back on the roller-coaster ride of financial well-being sentiment in the United States—and what’s been shaping it—since the start of the pandemic.

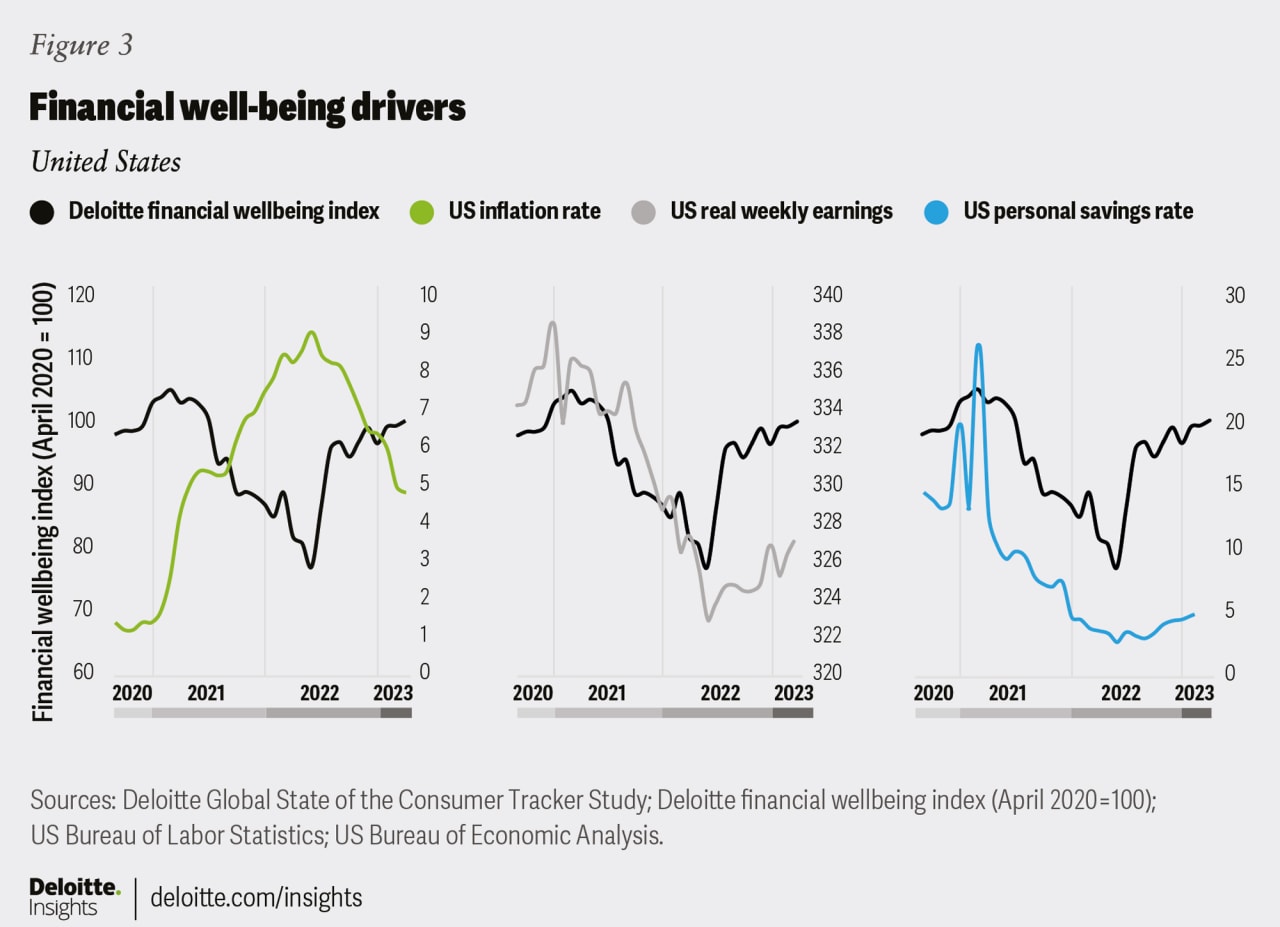

Surprisingly, financial well-being sentiment sustained an uptrend early on in the pandemic. In March 2021, Deloitte’s financial wellbeing index (FWBI) climbed to a three-year peak of 105.5 (figure 1).

A confluence of factors was likely the reason behind the trend. By early 2021, some of the early pandemic shock had worn off, even though health concerns were still high. People were adjusting to lockdown measures. Vaccines were rolling out. And with limited spending avenues, consumers were padding their savings. Perhaps more importantly, historic government stimulus programs provided immense financial relief. In March 2021, the US personal savings rate spiked to 26.3 (roughly 4x prepandemic rates) and the US government announced the US$1.9 trillion American Rescue Plan that extended and built upon the Coronavirus Aid, Relief, and Economic Security (CARES) Act from the prior year.1

Deloitte’s financial wellbeing index (FWBI) captures changes in how consumers are feeling about their present-day financial health and future financial security. Unlike consumer confidence indices, which often focus on consumer opinions about economic conditions (i.e., health of the economy or labor market), financial well-being focuses on the consumer’s own financial experience, where they’re the experts.

Financial well-being is measured across six dimensions of financial health:

Higher index values indicate stronger financial well-being.

Deloitte’s FWBI is part of a broader longitudinal study of consumer behavior, enabling financial well-being data to be linked to other behavioral data such as future spending intentions, as well as retail, leisure travel, and automotive purchase behaviors.

Financial well-being, however, quickly changed course. The pandemic persisted. Stimulus programs began to sunset. Inflation started rising.

By June 2022, FWBI values plummeted to a three-year low of 77.4. That month, inflation hit a peak of 9.1%, while the personal savings rate hit a historic low of 2.7%.

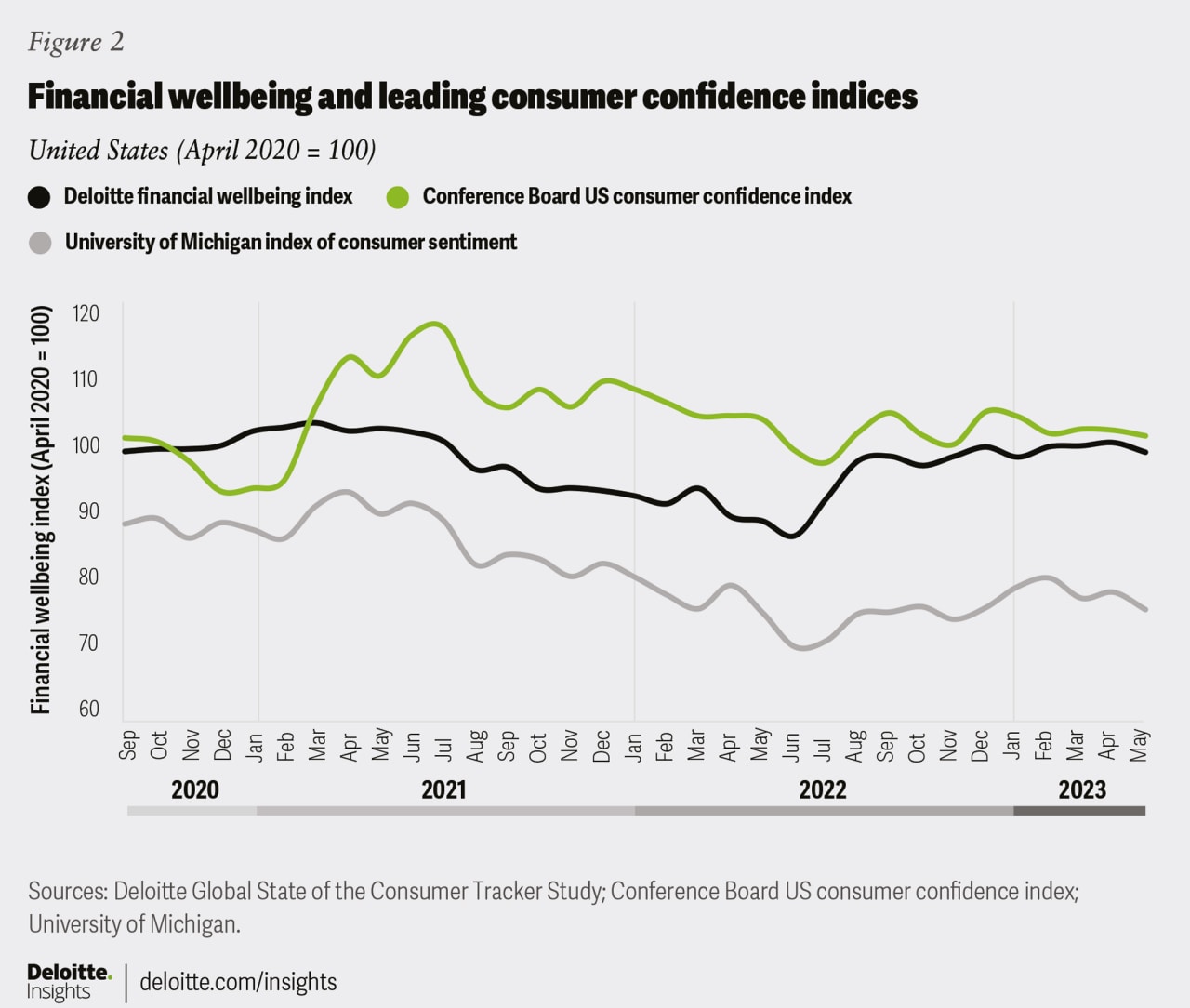

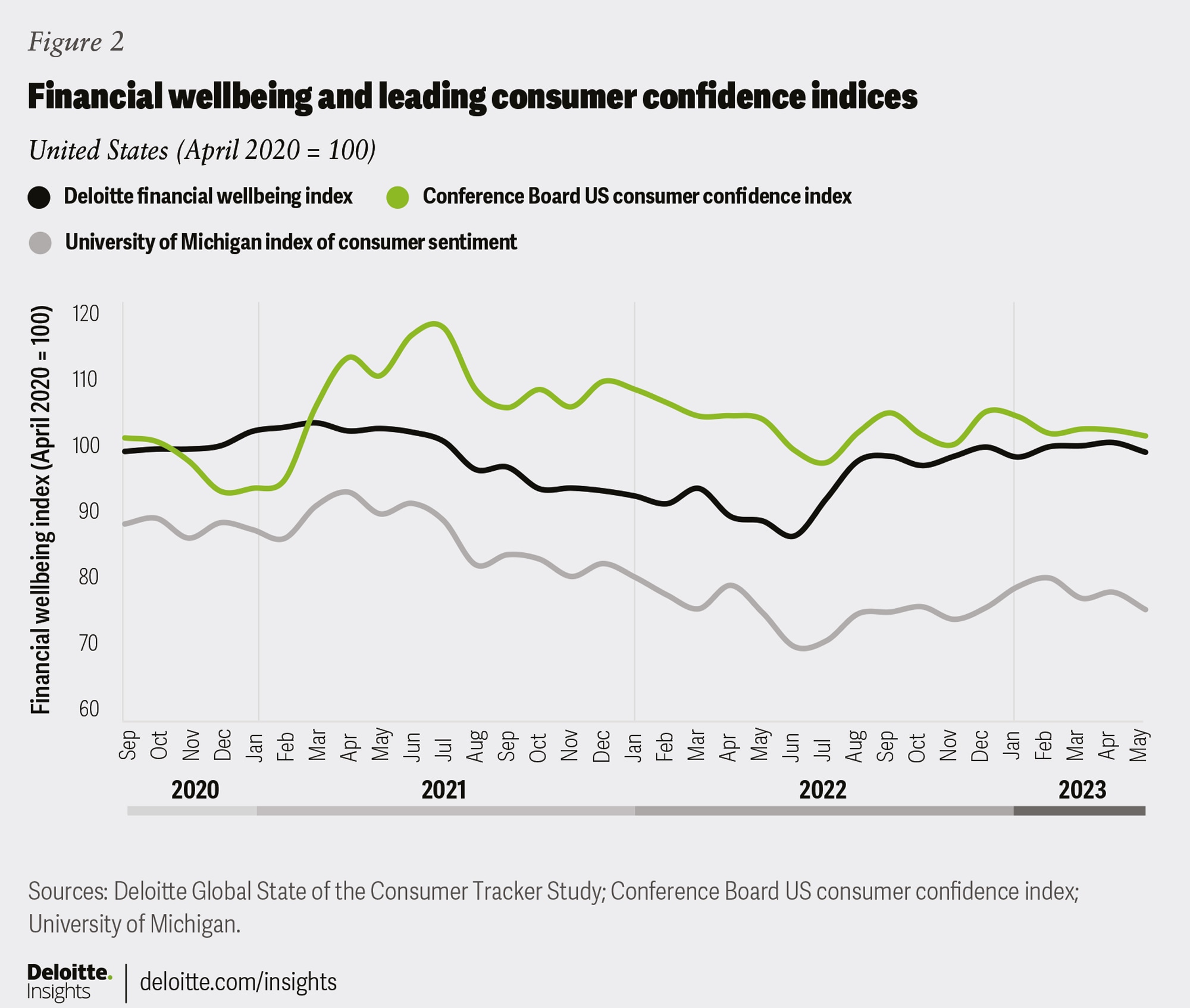

But despite prolonged financial stress, financial well-being sentiment has made a strong recovery over the past year. Since hitting its low in June 2022, FWBI values have returned to 2020 levels. Leading consumer confidence indices reveal similar recovery trends (figure 2).

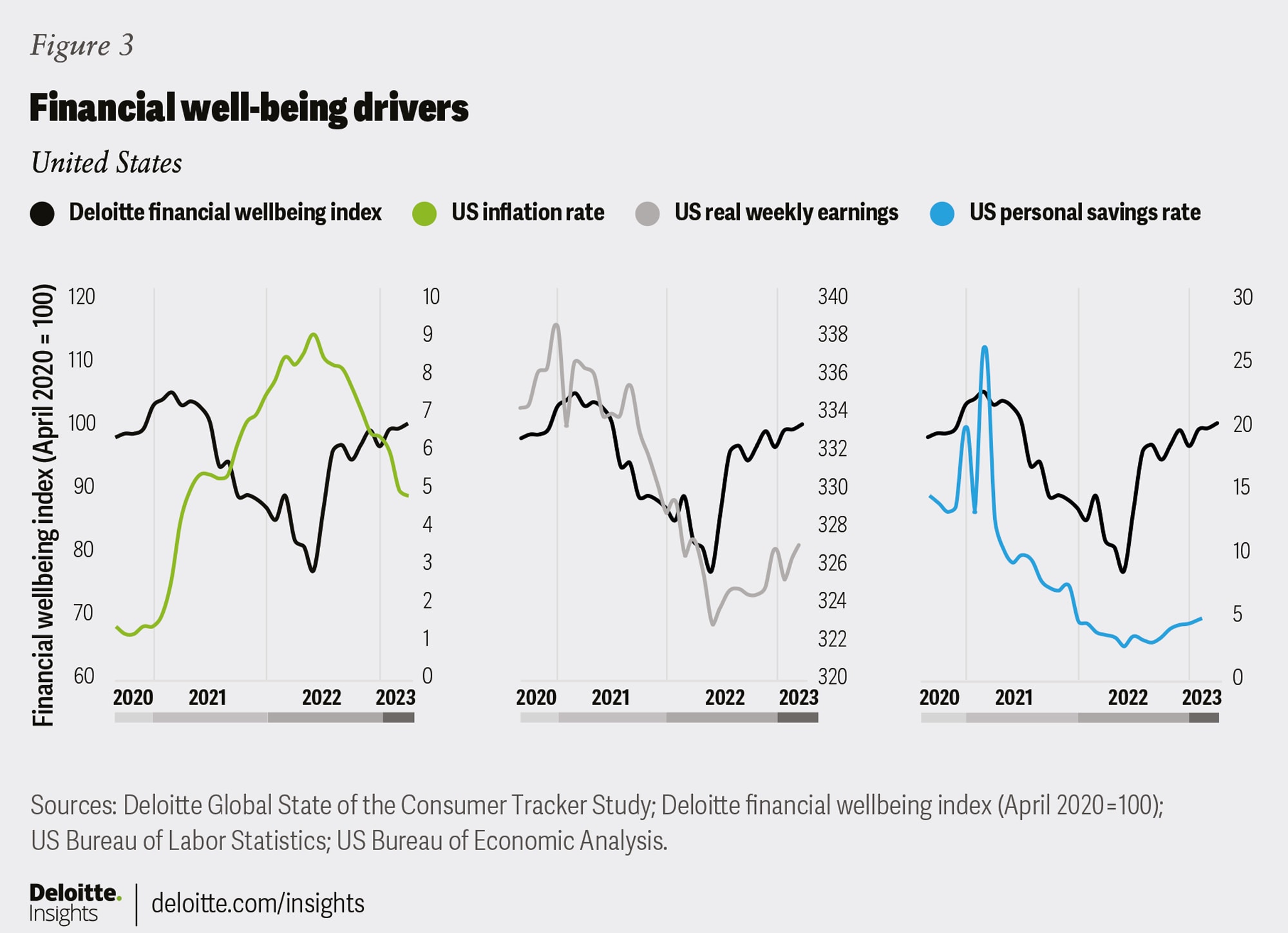

In the month that the FWBI flipped to positive, several key economic indicators did too (figure 3), suggesting multiple drivers are behind the current recovery:

While the FWBI has recovered to 2020 levels, it doesn’t necessarily mean consumers feel they’re back in the exact same place financially. Consumers’ perspectives about their finances likely changed a bit too. Historic inflation and pandemics don’t come around all too often. When people experience new, prolonged hardship, the return of some better fortune, even if only slight, can go a long way.

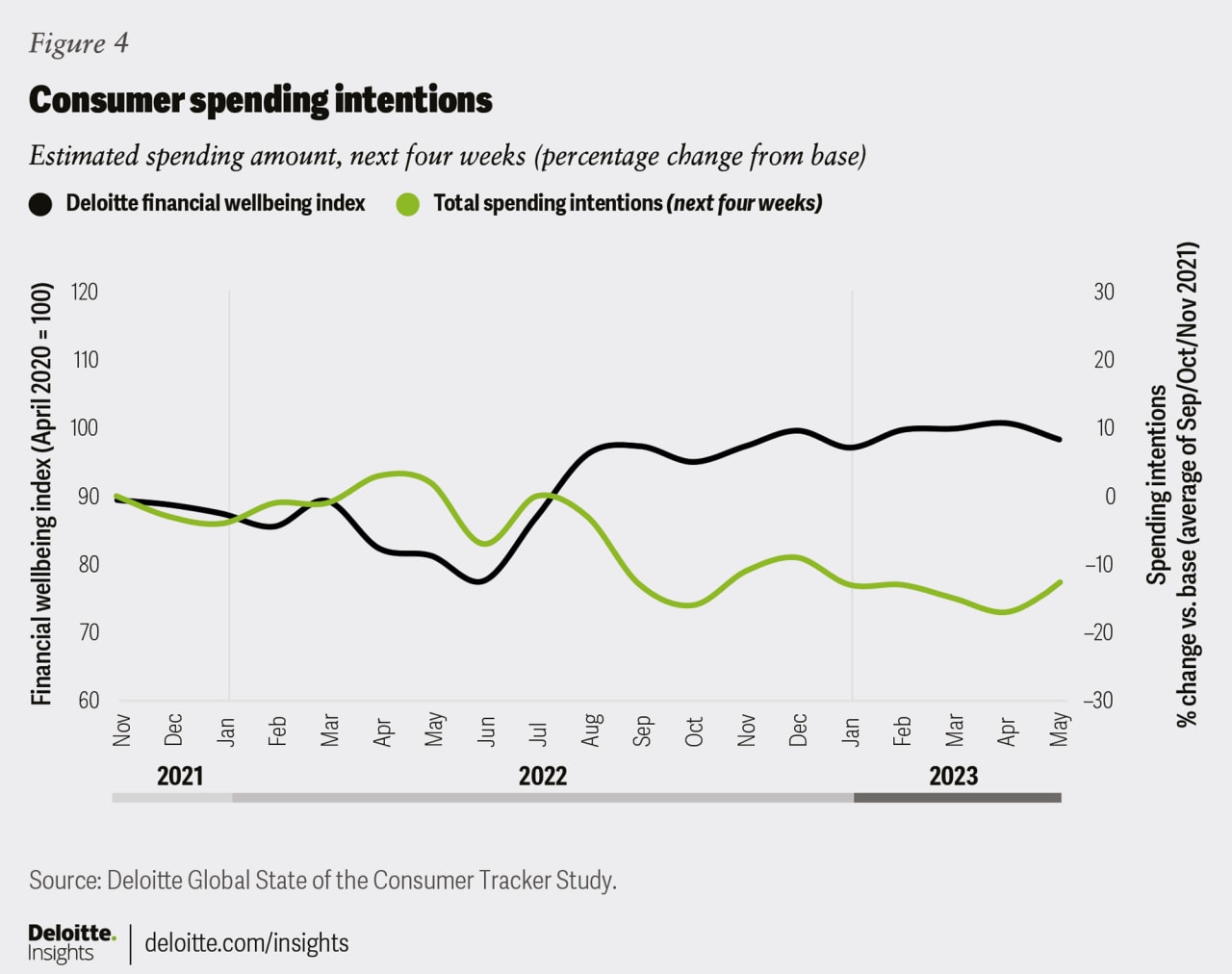

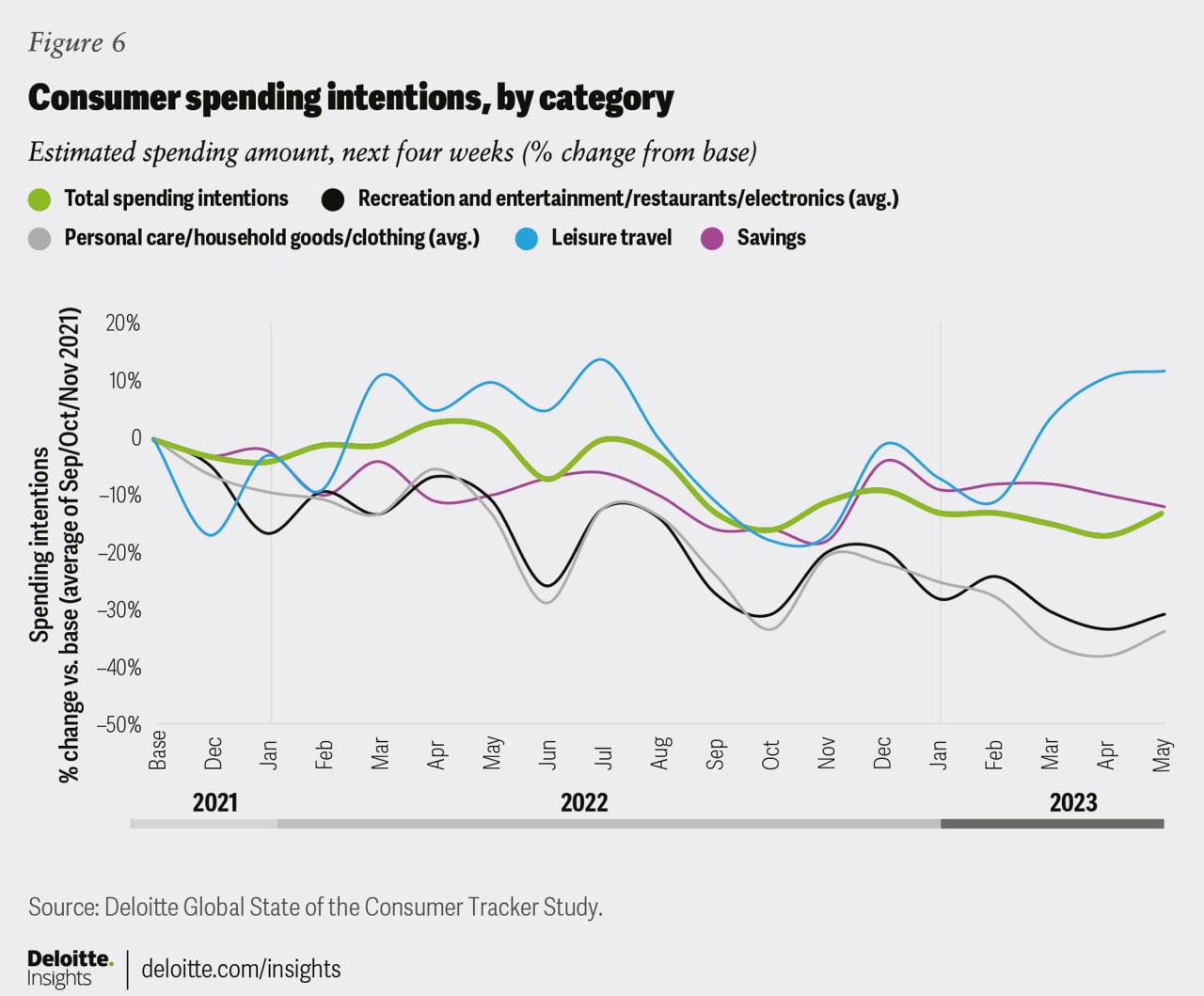

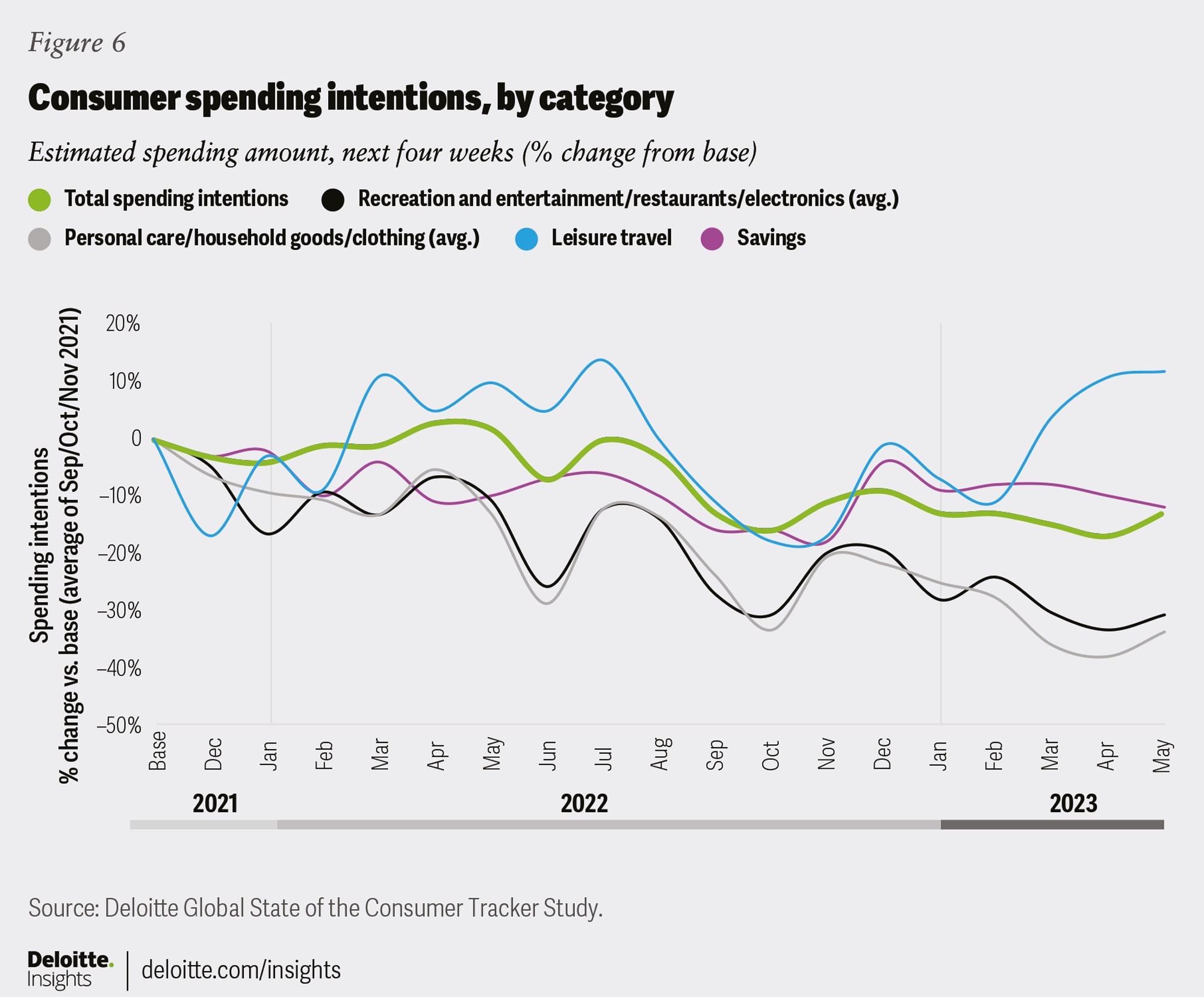

Spending intentions provide some evidence that Americans have yet to undergo a complete financial reset.

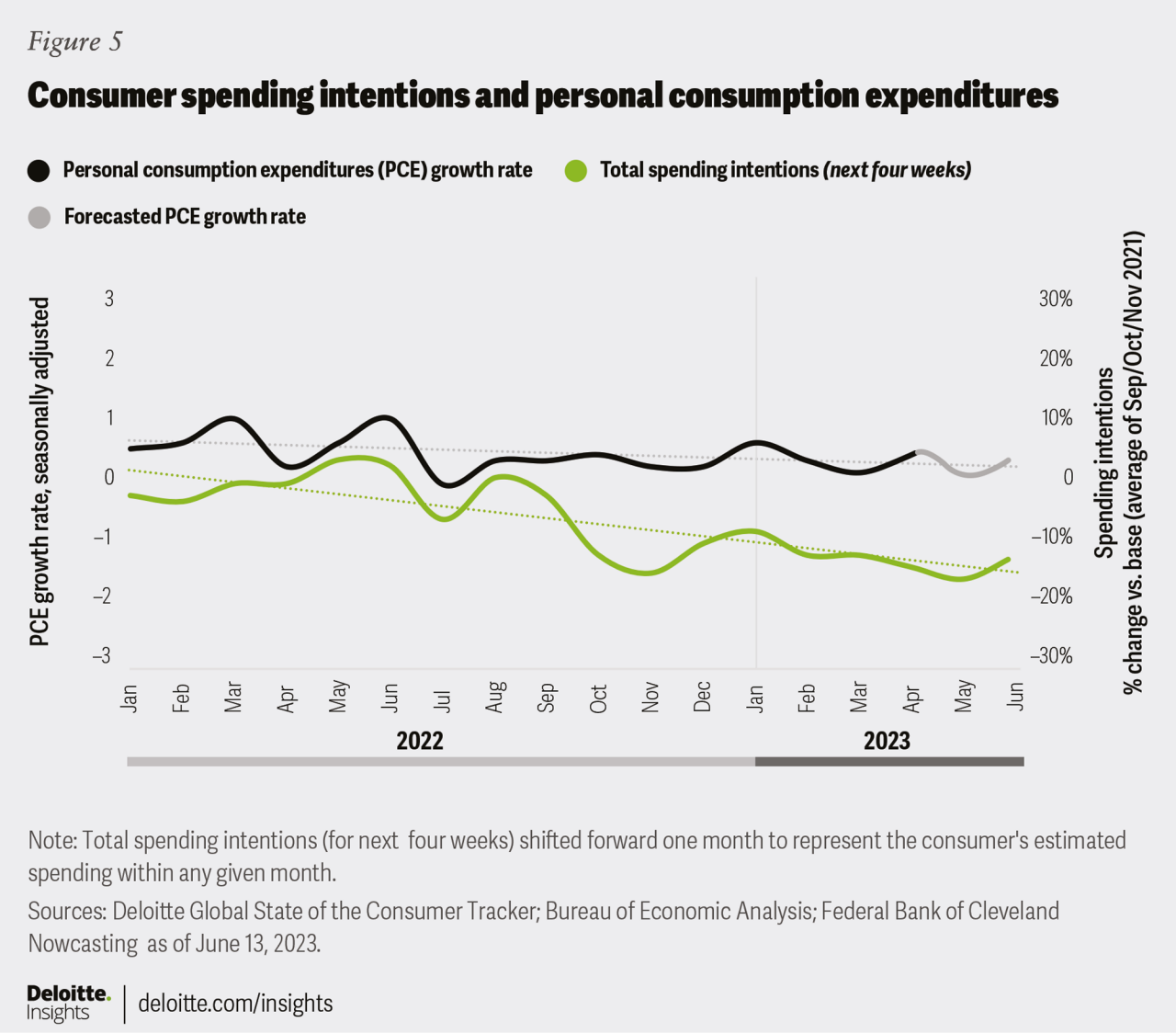

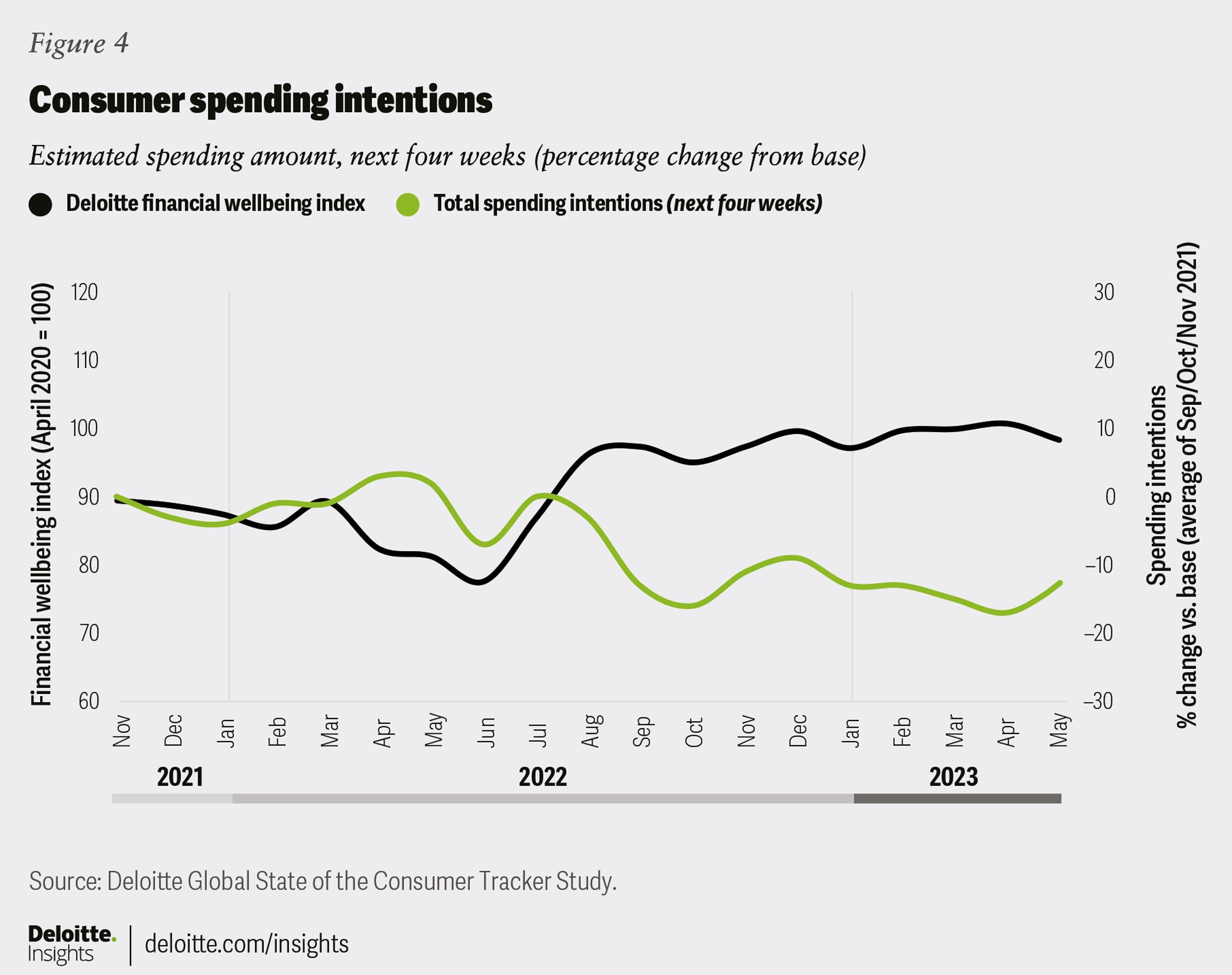

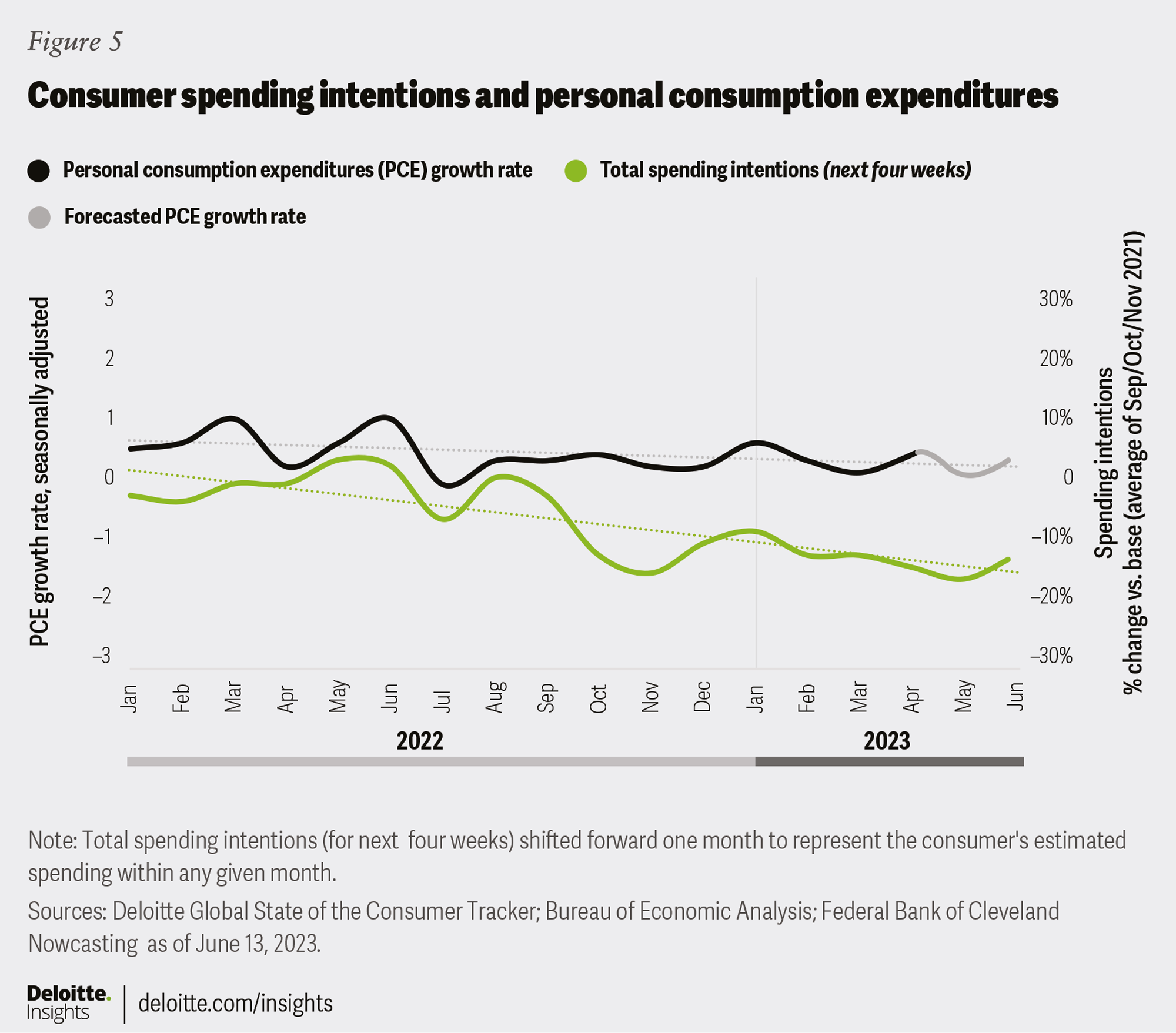

Even though financial well-being sentiment has recovered somewhat, spending intentions aren’t following suit. In fact, over the past year, spending intentions (measured as the amount consumers estimate spending in the month ahead) have slipped as financial well-being has improved (figure 4). Other consumer spending data, including personal consumption expenditure (PCE) from the Bureau of Economic Analysis also point to weakened spending confidence (figure 5).

While the trend seems counterintuitive, there are likely a few reasons why spending intentions have decoupled from financial well-being:

Improvements in Americans’ financial health are always a welcome trend. But it’s particularly critical now as strong headwinds to economic growth emerge on the horizon and a potential recession looms. Consumer spending accounts for more than two-thirds of US GDP.4 With Deloitte’s US Economic Forecast still showing the economy slowing down substantially in the second half of 2023 and economic risks such as high borrowing costs already leading to banking strains and weighing on economic growth, any dip in consumer spending may just be enough to tip the economy in the wrong direction.5

US Bureau of Economic Analysis.

View in ArticlePeter Caputo, Matt Soderberg, Eileen Crowley, Michael Daher, Maggie Rauch, Bryan Terry, and Upasana Naik, The experience economy endures: 2023 Deloitte summer travel survey, Deloitte Insights, May 22, 2023.

View in ArticleStephen Rogers, Justin Cook, and Leon Pieters, When rising prices break consumers’ trust, Deloitte Insights, May 20, 2022.

View in ArticleUS Bureau of Economic Analysis.

View in ArticleDaniel Bachman, United States Economic Forecast, Deloitte Insights, June 15, 2023.

View in ArticleThe authors would like to thank Jim Eckenrode and Marcello Gasdia for his contributions to the article.

Cover image by: Natalie Pfaff