Belfast Crane Survey 2024

The Evolving City

Key headlines

Market summary

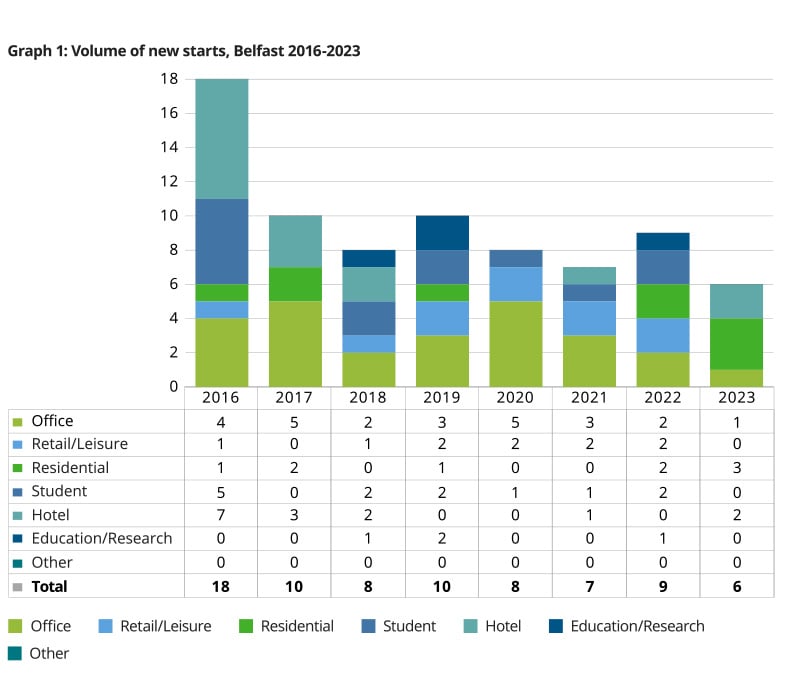

The overall picture is one of subdued development activity in the city centre, with fewer new starts and a reduced number of schemes under construction or completed during 2023 compared to previous years. Given the macroeconomic context, with high levels of inflation and rising interest rates, this is not an unexpected result. Despite the muted levels of activity, in the grand scheme there are continuing signs of confidence in Belfast – with a number of landmark schemes progressing.

The six new starts during 2023 included three residential schemes, two hotel schemes and one office scheme. The single office new start during 2023 is the smallest number recorded in the annual Belfast Crane Surveys to date, while the three residential new starts in 2023 represent the largest number recorded.[1]

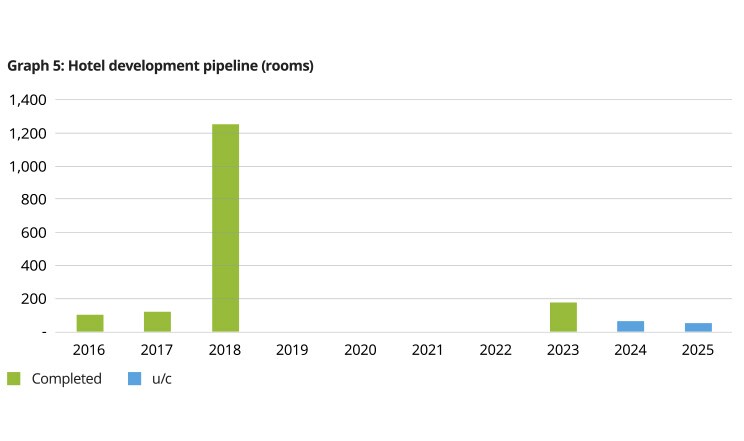

With this year’s survey recording the completion of a single hotel (Room2 Hometel on Queen Street) and two further hotel schemes starting on-site during 2023, there are indications that confidence and investor enthusiasm are returning to the hospitality industry. At the time of publication, planning permission has been granted for nine further hotel schemes across the city. Whilst the comprehensive reporting of visitor numbers has yet to resume following the disruption caused by COVID-19, encouraging statistical and anecdotal evidence is building that Northern Ireland is rebounding strongly. For example, the Central Statistics Office for the Republic of Ireland has reported that over 800,000 trips were made to Northern Ireland by visitors from the south during 2022 – representing a 50 per cent increase on the numbers in 2019, before the pandemic.[2]

For those arriving by bus or train, the Belfast Grand Central Station (also known by its working title, the Belfast Transport Hub) is due to be usable by passengers before the end of 2024, with works completing in 2025. Already very visible, the station is expected to cater for up to 20 million passenger journeys annually. Works have also continued on the redevelopment of Yorkgate Railway Station, representing a further improvement in the quality and capacity of facilities servicing the area in the vicinity of the new Ulster University Belfast campus.

Belfast City Council has developed a programme of creative and cultural events for 2024 which will deliver several world-class events and community-led activities, further increasing reasons for positivity in the visitor economy.

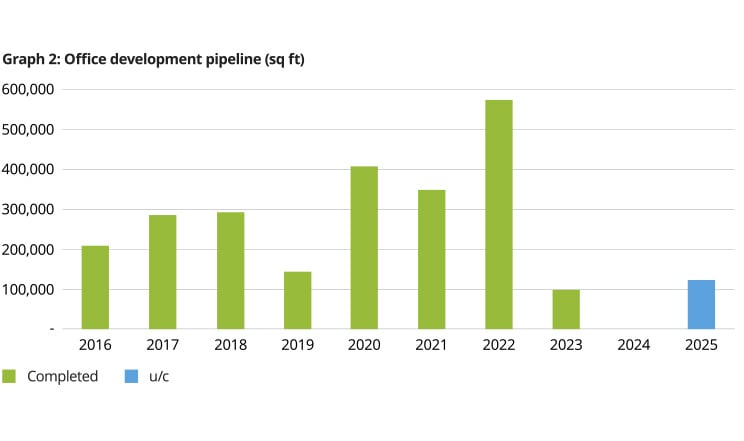

With just a single new office start recorded (and completed in year) during 2023, there has been a notable drop-off from the figures we have become accustomed to in Belfast. The volume of completed office floorspace during 2023 is the smallest volume recorded to date in our annual Crane Surveys, with three schemes totalling a combined 98,500 sq. ft. The continuing impact of changing working patterns combined with the availability of high-quality Grade A office space across the city centre is likely to impact the appetite for potential new schemes.

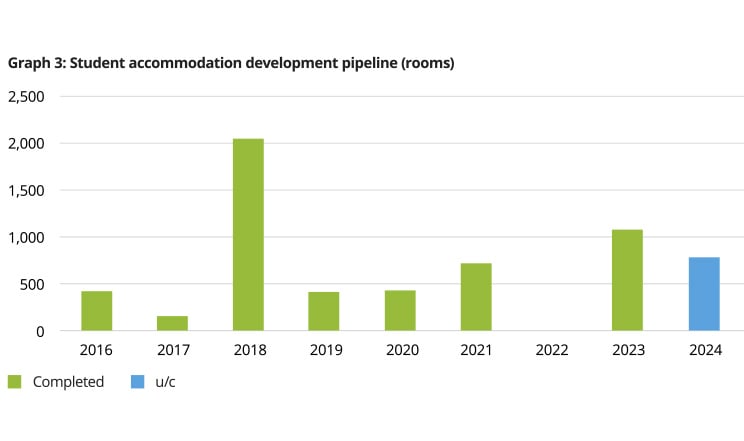

The completion of the Ulster University Belfast campus, significant investments in the Queen’s University estate, and a boom in student accommodation developments have seen over £1 billion invested in higher education in Belfast over the past decade. There are increasing numbers of students living in the city centre, including the international students which both universities are attracting Queen’s University Belfast (QUB) has almost 4,000 from over 90 countries, and Ulster University has in excess of 2,000 from more than 80 countries.

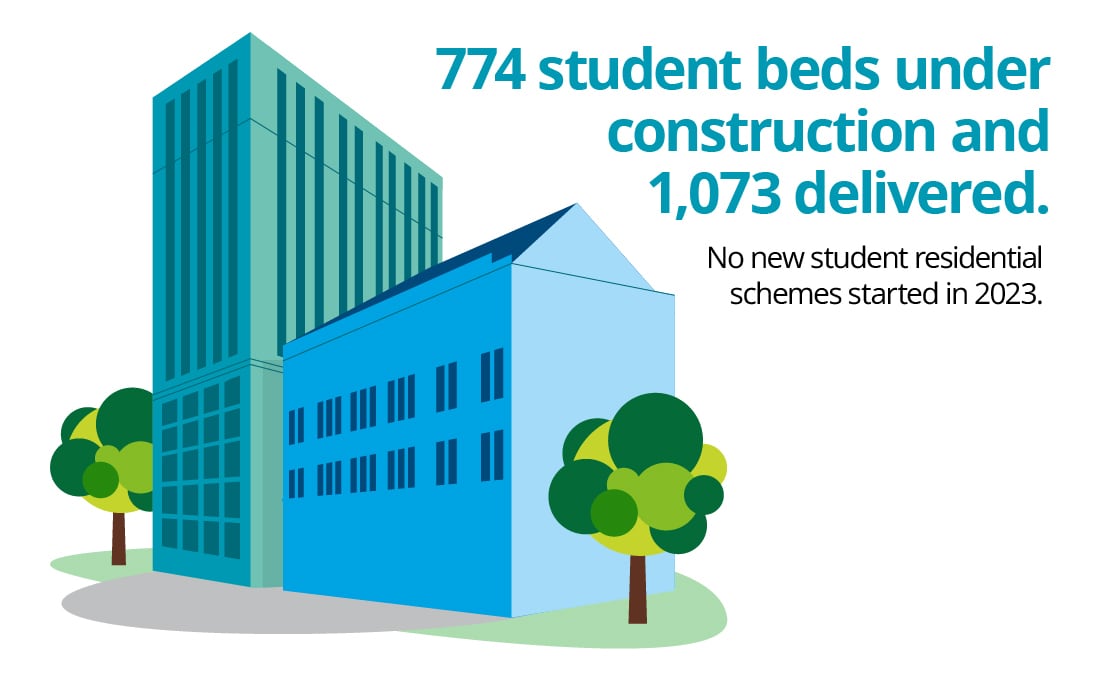

We recorded over 1,000 new student accommodation rooms completed during 2023 across four schemes, with an additional 774 rooms due to complete in 2024 (all located within the largest single complex to date on Nelson Street). High levels of investment are set to continue, with the Belfast Region City Deal programme containing a number of major education-orientated schemes and with the ongoing demand for student accommodation. Queen’s University has earmarked £100 million to help meet an estimated 3,000-room deficit in supply. There are three Queen's schemes currently in pre-construction – the development of 460 rooms on the Dublin Road, and two other schemes for sites on Laganbank Road and Brunswick Street which were purchased during 2023. Additionally, plans are being prepared for further private sector-led student accommodation investments in the Titanic Quarter and on Great Victoria Street.

Progress has continued on the ‘Living with Water in Belfast Plan’ through 2023.[3]

The Plan includes an aim to support economic growth by enabling development and maintaining essential drainage and wastewater assets. The current Belfast Wastewater Treatment Works is overloaded, and this has placed a constraint on development in the city, with new connections restricted as a result. An initial Phase 0 to provide an interim upgrade to the existing works was completed in 2023 and work is expected to commence on Phase 1 during 2024. Phase 1 will provide a further increase in capacity to cater for longer term growth as well as ensuring compliance with environmental standards. Phase 2 will further improve compliance with environmental standards and increase capacity. The Belfast Plan is part of overall NI Water total investment programme across Water and Wastewater for the PC21 period (2021-2027) forecast to be £2.7bn.

City centre living

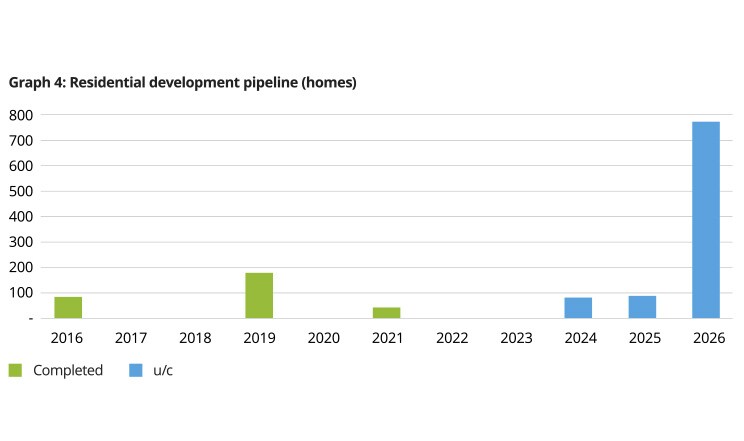

Belfast’s historically undersized city centre residential offering received a substantial boost during 2023, with a landmark scheme commencing in the Titanic Quarter. Loft Lines is the largest residential development in Belfast in over a decade, and one of the largest residential schemes currently on-site anywhere in the UK. Located on the waterfront in the Titanic Quarter it will be the first major build-to-rent scheme in the city and will combine private tenancy with affordable and social housing for a total of 778 new homes (627 build-to-rent, 151 affordable).

Loft Lines is forward funded by Legal & General, representing the involvement of a major institutional investor in the Belfast residential market, and will be part of a nationwide ‘build-to-rent’ portfolio held by the company. The affordable housing aspect will be funded and operated by Clanmil Housing Association, and overall completion of the £155 million project is expected during 2026.

As might be expected for a development of such scale and ambition, the project has attracted both positive and negative attention. Concerns have been raised about drainage and sewage treatment, and that the building will not include any provision for parking, in addition to the impact on views of Titanic Belfast. Given the nature of the development is a first of its kind for Belfast, the performance of the ‘build-to-rent’ aspect of the project will be watched carefully by other investors as a potential model for replication. Loft Lines represents a major opportunity for Belfast, and it will be important for the city that the project should be a success.

Another new start within the Gasworks is being undertaken by Radius Housing. The first phase of development will bring to market 60 houses and 34 apartments, of which all are social housing. Further announcements on the Havelock House site and on long-time vacant land on the Great Victoria Street - Hope Street junction also indicate further social housing in the city centre.

Three new residential schemes started on-site during 2023 for a combined total of almost 1,000 homes. For comparison, our Crane Surveys have previously recorded a total of just 306 new homes built in the city centre since 2016, across eight developments. Loft Lines alone almost doubles this total. The new starts were the Loft Lines in the Titanic Quarter (778 homes), the Radius Housing development in the Gasworks (94 homes; 60 houses and 34 apartments), and an apartment block on Dublin Road (85 homes).

Increasing the city centre population has been a key feature in strategic documents published in recent years such as the Belfast Agenda[4] and the Belfast City Centre Regeneration and Investment Strategy[5]. With the problem now identified, Belfast City Council is measuring the size of the city centre population as one of its City Centre Strategic Indicators[6] and is seeking a long-term private sector partner to “fund, develop, and where appropriate, own and manage assets”[7] across several city centre sites. Increasing the number of people living in Belfast city is not just important for increasing its vibrancy and resilience. Providing new homes has enormous social importance, given the constraints on existing housing stock across the city area. The draft Department for Communities Housing Supply Strategy[8] and associated analysis of housing need and demand[9] by the NI Housing Executive indicate that there is a growing shortfall in housing stock, and the waiting list for social housing continues to increase. Figures for 2022/23 published by DfC[10] show that the total number of people on the social housing waiting list was 45,105, with over a quarter (12,175) of pending applications being in the Belfast area.

The building momentum in student accommodation developments over the past decade has continued into 2023. The four developments which completed in 2023, adding over 1,000 additional rooms, have brought the total number of rooms completed in the city centre since 2016 to over 5,000. This represents a major step change in the student offering in Belfast – in terms of location, volume and quality of accommodation, as well as student experience − and the impact on vibrancy and footfall is apparent across the city.

Demand is far from sated. Should the estimate made by Queen’s prove correct that about 3,000 more rooms will be needed in the next five years to meet demand, it is likely that we will continue to see further schemes across Belfast.[11] A pre-application notice has been filed that would see Fanum House on Great Victoria Street being demolished and replaced with a housing scheme for 610 students. A pre-application notice has also been filed in relation to a student accommodation development in the Titanic Quarter, which would be a first for that location. From a re-purposing perspective, the Catholic Chaplaincy has received planning permission to change its upper floors offices into over 40 student accommodation units.

The cumulative result of the large volume of student accommodation rooms built in the city, combined with modest increases in residential stock (pending the completion of Loft Lines in 2026) and the increase in hotel rooms, has seen a substantial increase in the number of people living and staying in the city centre – especially during term time. We have recorded a combined 306 residential homes, 5,225 student rooms, and 1,642 hotel rooms completed in Belfast since 2016 – a total of 7,259 additional units added. While encouraging a permanently resident population will be important to the long-term sustainability and success of the city centre, the short-term impact of increased footfall has at least partially offset the impact of post-pandemic working patterns drawing people out of the city and has noticeably improved the atmosphere in the city.

Tourism

The tourism sector in Northern Ireland is rebounding and regaining momentum following the lifting of travel restrictions put in place to counter COVID-19. The impact of the pandemic on visitor numbers and spending was dramatic across the globe and the industry in Belfast experienced considerable disruption. An estimated 2,100 jobs were lost in the hotel sector in 2020, with corporate earnings decreasing overall by 90 per cent compared to 2019.[12] The Northern Ireland Tourism Alliance estimated that, as of March 2021, total visitor spending had fallen by £800 million since the start of the pandemic in early 2020.

Plans to re-energise and rebuild the visitor economy have emerged. Visit Belfast's ambitious three-year tourism plan, Rebuilding City Tourism, was published in 2021, aiming to rebuild Belfast’s tourism economy and exceed pre-pandemic visitor numbers and spend levels by 2025.

The Department for Economy's ten-year tourism strategy anticipates that 2023 visitor numbers will reach 90 per cent of 2019 levels.[13] The number of visits from Northern Ireland's closest neighbour, the Republic of Ireland (ROI), has been particularly high. In 2022, trips from the ROI exceeded one million for the first time, with record levels of nights stayed and spending. Tourism footfall from docking cruises brought 250,000 tourists into the city centre in 2023, 20 per cent up on the previous record in 2019.

Continuing developments in the tourism offering in Belfast will attract visitors and improve the lives of citizens through better public spaces, hotels, public transport as well an enhanced events programme[14]. The proposed £100 million investment in Belfast Stories[15] will be key to sustaining momentum for the tourism sector, while also regenerating a key site on the route connecting City Hall with the new Ulster University campus.

A total of 2.46 million hotel beds were sold in NI in 2022, bringing the sector almost back to the record levels of 2018, and in January – August 2023 hotel room occupancy has been three per cent higher than in the same period last year), a promising sign for the hotel market.[16]

Belfast is very much on the radar for investment by hotel operators looking for opportunities. This positive outlook can also be seen in the completion of Room2 Belfast located on Queen Street, followed by two new hotel schemes starting on-site with the extension of the Flint and the Scottish Mutual Building, a total of 113 new beds due to enter the market.

The pipeline is also very healthy with planning permission granted for nine further schemes as of November 2023. Alongside the traditional hotel offerings, there will be a continuation of diversity in the market with the emergence of aparthotels and short-term rental options already evident from the recent openings of the smaller scale Regency and Balmoral Buildings, while the Scottish Mutual Building development will deliver 40 bedrooms alongside two bars, two restaurants and 10 serviced apartments all on offer within the one site due to come to market, early 2024. There is also evidence of what were office buildings being repurposed into hotels.[17]

As in other cities in the UK and Ireland, a gap has been created by slow returning workers and office vacancies. While the student population and the slow growth in resident population will help, visitors may become more important for the life and vibrancy of the city centre in the coming years, a trend that researchers have already picked up on.[18]

Waterfront

Like other industrial cities in the past, Belfast had somewhat turned its back on the river. Recent decades have seen this change, during the 1990s through the Laganside Corporation, and more recently via developments in the Titanic Quarter and City Quays.

The Titanic Quarter, with Titanic Belfast at its heart, successfully blends tourism, leisure, office, education and retail developments. The ongoing Loft Lines development will produce a significant residential riverside development, with plans approved for an adjacent hotel.

Belfast Harbour’s City Quays development has already delivered the 188-bed AC by Marriott hotel, 430,000 sq. ft. of office space and an accompanying car park. Two new City Quays plans are being pursued by Belfast Harbour. City Quays 4 is a proposed 256 home build-to-rent residential development, and City Quays 5 is a proposed mixed use office, retail and gallery development. Work has just commenced on City Quays Gardens, a new ‘green garden’ with environmental sustainability at the core of its design, a reminder of the desire for a city centre with more green spaces.

Upstream, there are still significant spaces and sites to be developed. For example, on the east bank of the river, work is ongoing on how to use Queens Quay,[19] a site owned by the Department for Communities. Just further up the river the Waterside,[20] on the old 'Sirocco Site,' a 16-acre area with plans approved for up to 1.75m sq. ft. of mixed-use development, has not progressed visibly. On the opposite bank, Queen’s University has purchased a site on the Laganbank Road and will be developing housing for staff and post-graduate students.

Despite these efforts, Belfast’s waterfront remains an under-developed and under-utilised asset. Developing it will be both a priority and an opportunity going forward. The Bolder Vision for Belfast, published by Belfast City Council and the Departments for Infrastructure and Communities, includes plans to enhance the area, encourage better use of the River Lagan and strengthen connections between the river and city centre. In response, a Belfast Waterfront Task Group[21] has been established to enable the Waterfront to reach its full potential.

The Task Group launched a framework for future development along the River Lagan in December 2023. At its core is a ten-kilometre connected waterfront promenade, supported by a toolkit of interventions - from boardwalks and bridges to heritage and habitats, with outcomes for communities, climate resilience and city growth. It includes a bridge connecting Sailortown and the Titanic Quarter as well as the one planned at Ormeau Park. The Task Group’s vision is a helpful contribution to what the Belfast Waterfront could become, unlocking housing and commercial development adjacent to the river, which is critical to Belfast’s growth ambitions.

Outlook

The most significant development next year will be the opening of Belfast Grand Central Station to passengers before the end of 2024, with works completing in 2025. As the terminal for the Dublin Enterprise train link, it will be an important new gateway to the city. Accompanied by new public realm (Saltwater Square) and plans for Weavers Cross mixed-use development, the bus and train station will create a new dynamic west of the city centre, with potential to better connect and reinvigorate adjacent inner-city communities in Sandy Row and Lower Falls.

Development along the banks of the River Lagan will continue, not least with the prominent Loft Lines residential development in the Titanic Quarter, alongside plans for further hotel, office and student accommodation across multiple sites. It will be interesting to see how the Waterfront Task Group’s vision is received and taken forward, and how it shapes and accelerates planned development along the river.

The question about residential is whether momentum can build, not least on the back of the Loft Lines development and efforts by City Council to work with a strategic partner to accelerate city centre residential development. As well as strengthening the city centre, this could alleviate wider pressures on housing supply. The granting of planning approval for almost 700 new apartments across four schemes in January 2024 is a positive indicator that Belfast is on the cusp of a notable change in the quality and scope of the residential offering available in the city centre.

Higher Education will continue to play a key role in the city centre development with further purpose-built student and staff accommodation, alongside City Deal-supported education and innovation facilities. The visitor economy will also be influential, with multiple hotel and short-term accommodation developments planned. Belfast City Council investment in a significant cultural programme and the City Deal supported Belfast Stories will continue to encourage this sector. While there are notable plans for offices, for example the new Kainos Headquarters in the Linen Quarter, it will be interesting to see whether other speculative office developments progress as quickly as planned, given the wider context of working from home and the availability of quality office space.

Overall, although in-year activity has been more limited than in the recent past, developments that are underway point to a city centre that is evolving in fascinating ways. The question remains whether the current efforts will be sufficient to address the challenges, realise the opportunities and accelerate the changes necessary to meet the ambitions for the city.

Data in detail

A summary of all data across all development sectors can be accessed using the interactive Development map, Development activity and New start charts below, allowing you to explore all development projects, their location and what this means in terms of overall development activity.

The Report

Why?

A report that measures the volume of development taking place across central Belfast and its impact. Property types include residential, office, leisure, hotels, retail, student accommodation, education and research facilities, and healthcare.

Where?

The City Core, Waterfront, Titanic Quarter, Transport Hub, Inner North, Linen Quarter and Southern Fringe.

What?

Developers building new schemes or undertaking significant refurbishments exceeding the following sizes: office – 10,000 sq ft; retail and leisure – 10,000 sq ft; residential property – 25 units; education, healthcare, and research – 10,000 sq ft; hotel – 35 rooms.

When?

Data for the Crane Survey was recorded between 3 January 2023 and 3 January 2024.

How?

Research for this report was undertaken by Deloitte’s Northern Ireland team, based in Belfast. The Deloitte Real Estate team have also been closely involved in the development of Belfast over recent years. In addition to our in-house knowledge and field research we have used a variety of sources to collate and validate our research. These sources include the Northern Ireland Planning Portal, local media and trade publications, and construction and development industry contacts.

[1] The Belfast Crane Survey was first published in February 2017, covering the calendar year 2016.

Contacts

Marie Doyle

Partner, Consulting

Simon Bedford

Partner, Real Assets Advisory - Development