Japan economic outlook, October 2023

Japan’s postpandemic recovery has been impressive, but future growth and monetary policy will hinge on its central bank’s stance, domestic demand, and wage growth.

Japan’s real GDP finally overtook its prepandemic peak—as of second quarter 2023—after rising a sizable 1.2% compared to the first quarter.1 Much of this strength was due to the external sector. A weakening yen supported export growth and helped push imports lower. Meanwhile, domestic demand remains sluggish and is plagued by relatively high inflation.2 For example, real household spending fell 1.4% from a year earlier in August, as inflation eroded purchasing power.3 In the near term, economic growth will likely slow down, as external demand wanes and domestic demand struggles to pick up.

The Bank of Japan (BOJ) remains committed to its highly accommodative monetary policy stance, suggesting that inflation will continue to run hot. Although wage growth picked up this year, there is little evidence that it will surpass inflation anytime soon. Workers will likely need to wait until next spring’s wage negotiations, or shunto, before seeing their inflation-adjusted wages rise again. A dovish BOJ will hold down the value of the yen, which will continue to support growth in exports. However, economic weakness in the rest of the world will limit the benefits of currency depreciation.

Bank of Japan avoids hawkish tone

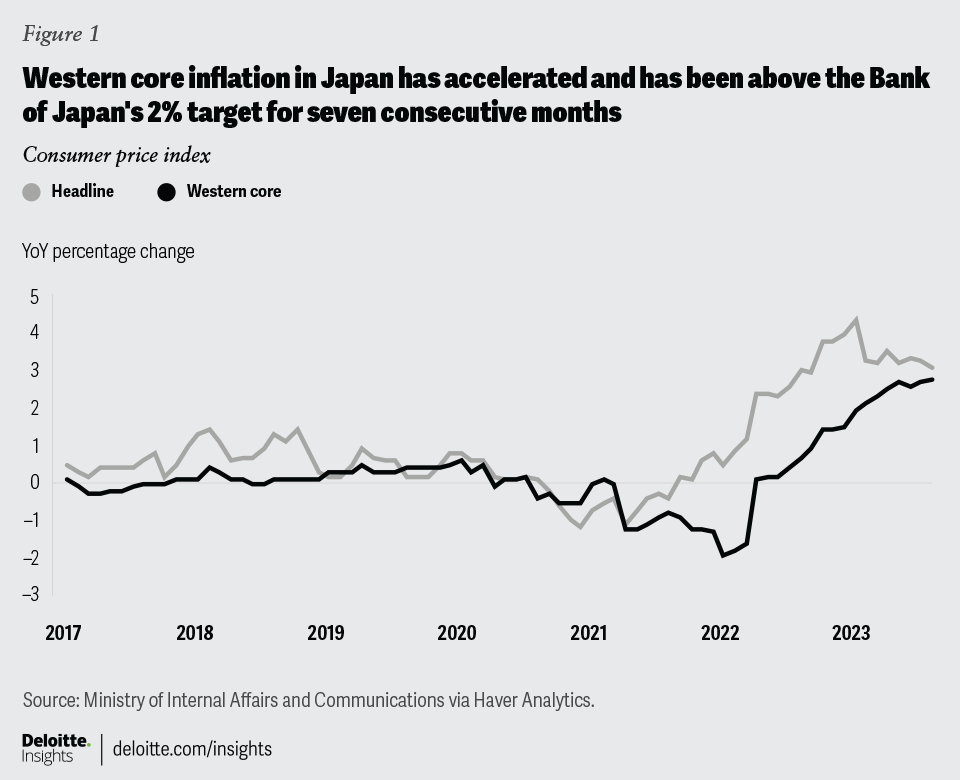

The BOJ left monetary policy unchanged at its September meeting—so the policy rate remained slightly below zero and the yield curve control policy fixed the 10-year yield at zero percent.4 Aside from a tweak to the yield curve control policy earlier this year, the BOJ has been the only major developed-economy central bank that has not significantly tightened policy. Compared to other developed economies, inflation in Japan arrived later and has generally been more muted. Even so, inflation has been running above the central bank’s 2% target.5 For example, headline inflation in August was 3.1% and has been running at 3% or above since August last year. Meanwhile, western core—which excludes both food and energy—accelerated to 2.8% in August and has been above 2% for seven consecutive months (figure 1).

Given the BOJ’s inflation target, it may seem odd that the central bank has taken such a dovish policy stance while inflation has persistently been above target. Indeed the BOJ seems much more cautious about undershooting its target than overshooting it after decades of below-target inflation. It wants to ensure that inflationary pressures persist so that it can finally abandon its negative interest rate policy, which will likely require several changes in economic data.

The first change the central bank likely needs to see before raising rates is stronger services inflation. Most of the above-target inflation seen last year has been due to goods. For example, goods inflation reached 7.3% in January while services inflation was running at 1.1%. The central bank correctly assessed that much of the goods inflation would prove to be transitory, as goods inflation eased to 4.2% in August. However, services inflation has picked up just as goods inflation came down. In August, services inflation was 2%—the highest reading since 1998.6

Even if services inflation continues hovering above 2% in the coming months, it is unlikely to be sufficient to warrant a change in monetary policy on its own. Stronger wage growth will likely need to accompany higher services inflation. Indeed, during the press conference following the last central bank meeting, Governor Ueda noted the importance of wage growth in determining the persistence of inflation and therefore future monetary policy changes.7

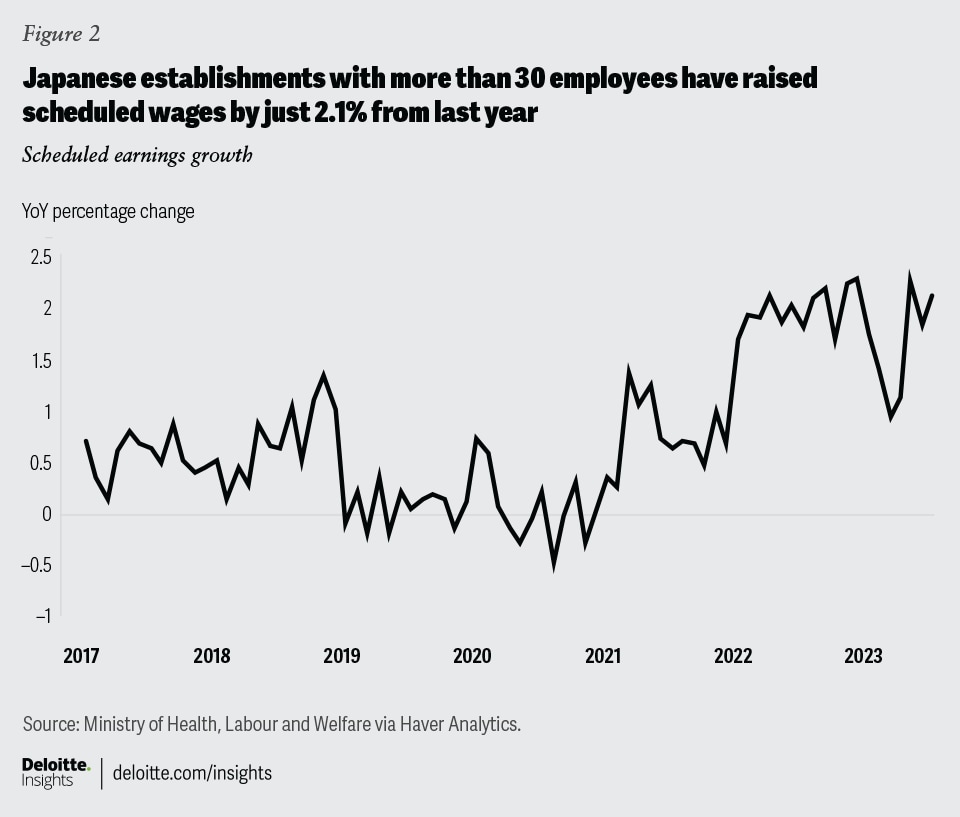

As we mentioned in our previous Japan economic outlook, wage growth perked up after the annual shunto. However, scheduled wages, which exclude overtime and bonus payments, were up just 2.1% from a year earlier in July for establishments with at least 30 employees (figure 2). Wage growth for smaller establishments was even lower. Although this is a notable improvement from previous years, wage growth is still running below inflation and will likely need to move higher for central bankers to feel confident about sustainably achieving their mandate. This contrasts with what other developed central bankers are experiencing. In the United States and Europe, inflation adjusted wages are rising, which has put additional pressure on their central banks to take a more hawkish stance.

It is future productivity growth that will determine how much higher wages need to go. Pinpointing how strong labor productivity growth will be is notoriously difficult. Over the last year, labor productivity growth in the services sector has averaged about –0.7%.8 But this rate of growth is likely suppressed by the rebound in hiring in this sector in anticipation of stronger demand. Labor productivity growth could be substantially higher in the future. During the two years ending September 2019, services labor productivity growth averaged about 1.3%.9 If central bankers expect labor productivity growth to return to 1.3%, they would need wage growth to jump above 3% before feeling confident about inflation persisting above 2%. In practice, central bankers are likely looking for signs of acceleration in wage growth before hiking rates. They will also likely want to wait until next year’s shunto to get a better idea of how wage growth will develop over the subsequent year.

We currently expect the BOJ to raise rates in the first half of next year. However, it is possible that the labor market will not be tight enough to warrant the pay increase the central bank is hoping for. Although the unemployment rate was at 2.7% in July, it remains half a percentage point above where it was in December 2019.10 In addition, the total number of employed persons remains slightly lower than the number employed in January 2019. Plus, the ratio of active job openings to active applications, which is an indicator of labor demand relative to supply, has been sliding this year. That ratio was just 1.29 in July, down from 1.36 in December, and well below the 1.63 reading in April 2019.11

The yen takes a tumble

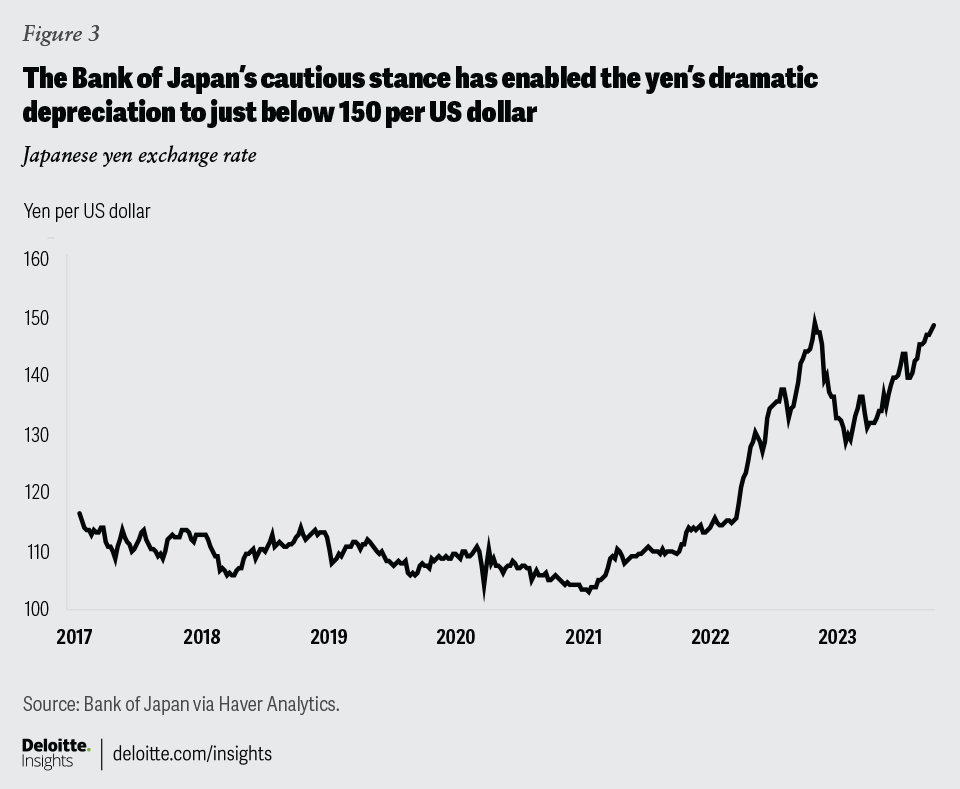

The BOJ’s dovish stance has had a clear effect on the value of the yen. The yen depreciated to 149.32 against the US dollar on September 28, stopping just short of the psychological threshold of 150 (figure 3). For reference, the exchange rate at the start of the year was a considerably stronger 130.3.12 While the BOJ insists on maintaining its dovish stance, other developed-economy central banks have grown more hawkish. Notably, the Fed raised its outlook for its policy rate over the next year.13 The widening gap between Japan’s interest rates and those in other countries has weighed significantly on the yen.

This strong depreciation has raised the probability of authorities intervening to support the yen from weakening much further. Indeed, Japan’s finance minister has indicated that Japan has been communicating with foreign authorities about quelling “excessive volatility.”14 Such an intervention would likely require using foreign currency to purchase yen, which would reduce money supply and tighten monetary conditions—exactly the opposite of what the central bank is currently trying to do.

Such interventions are also only temporary fixes, however (Japan has a limited amount of foreign reserves that can be used to buy yen currently). Japan intervened in currency markets in October 2022, when the yen had reached a similarly weak value.15 That intervention helped generate some strength in the yen for the remainder of 2022, but the yen has consistently depreciated since January 2023. Indeed, policymakers are likely trying to buy themselves some time. The Fed’s own projections suggest that the United States will cut rates (albeit modestly) before the end of next year.16 Plus, the BOJ may raise rates next spring once it has a better sense of wage negotiation outcomes. Should these events come to pass, the yen should strengthen around the middle of next year.

Japan’s economy will likely slow now that it has recovered the output it lost during the pandemic. Slower economic activity will allow the BOJ to maintain its dovish monetary policy stance into 2024. However, we expect negative interest rates will keep upward pressure on both prices and wages and allow the BOJ to finally raise rates in the first half of the year. The change in policy is expected to come only once policymakers are reasonably sure that next year’s shunto will lead to clear acceleration in wage growth in 2024.

{kind=link}

{kind=link}

{kind=link}