Japan economic outlook, February 2025

Inflation seems to be Japan’s biggest hurdle on the way to economic recovery, despite tax breaks, energy subsidies, and strong wage growth

Japan’s recovery has been relatively slow: Despite growing by an annualized 1.2% in the third quarter,1 real GDP was still slightly below its pre-pandemic peak. Government consumption and exports were the only two major components of gross domestic product that reached new highs. Even with the upswing in consumer spending in the second and third quarters, domestic household consumption was still 1.4% below where it was in the third quarter of 2019.2 The recent rebound in consumer spending is, at least partially, driven by the one-off tax break implemented last summer.3 Residential and nonresidential investments have also yet to regain much of the ground lost during the pandemic.

Looking ahead, Japan’s economy is expected to improve. Another wave of government support will keep domestic demand moving in the right direction. In addition, a weak yen will continue to support goods exports and tourism. However, there are several key risks to this outlook. If inflation persists, it could prevent a fuller recovery in domestic demand. In addition, rising trade barriers in the rest of the world could restrain exports and exacerbate inflationary pressures.

Will consumption rebound?

Stronger domestic consumer spending is likely a requirement for Japan to sustain its inflation target and keep output growing. The good news is that consumer fundamentals have improved. Nonagricultural employment was up 1.1% from a year earlier in December.4 Meanwhile, contractual wages were up 2.5% over the same period—the strongest pace of growth since 1994.5 As a result, the real consumption activity index, after adjusting for travel, posted its second consecutive nonnegative year-over-year growth rate.6 Consumer spending is expected to pick up this year, assuming the next budget includes the promised tax breaks and energy subsidies.7

The main impediment to stronger domestic consumer spending is inflation. Even with such strong contractual wage growth, headline inflation was even higher, at 3.6% year on year in December.8 Energy and fresh food prices have been rising quickly. Energy prices were up 10.1% from a year earlier in December, while fresh food prices were up 17.3%.9

For consumer spending to rebound, wage growth needs to outpace consumer inflation. Fortunately, total cash earnings, which include bonus payments, grew faster than inflation in December. In addition, wage growth is expected to remain relatively strong. Early indications of this year’s shunto—the annual wage negotiations for Japan’s unions—show signs of another year of solid wage growth. For example, a major union, Rengo, is asking for a pay rise of 5% or more.10 Last year’s shunto ultimately yielded a 5.1% wage increase.11

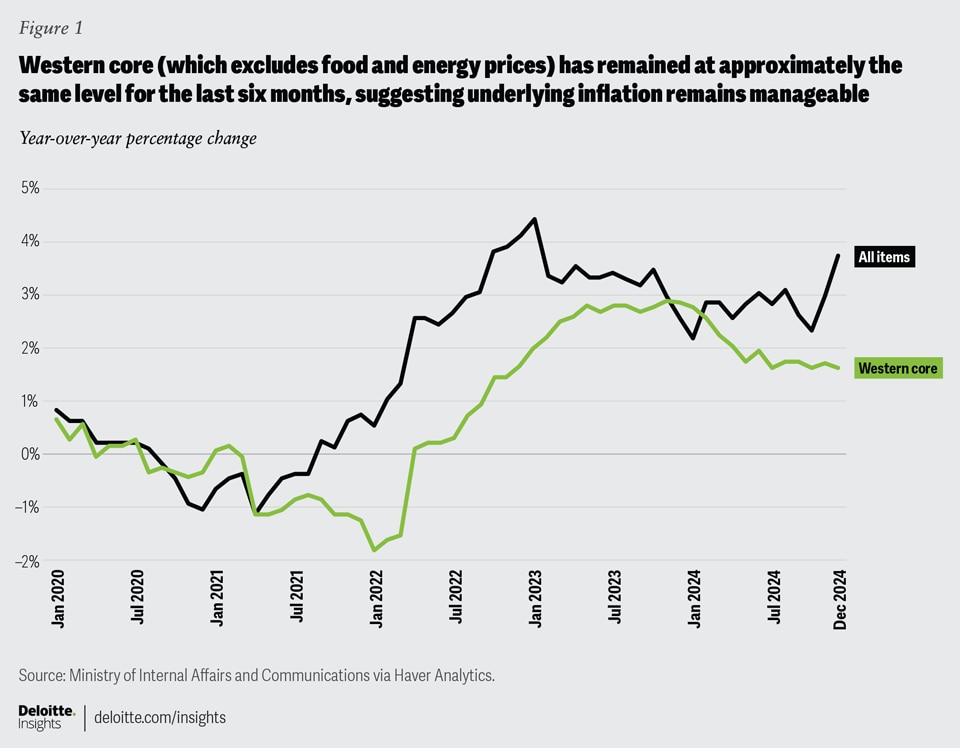

Inflation is also expected to move lower. Western core inflation, which excludes food and energy, was just 1.6% year over year—about where it has been for six months (figure 1).12 This suggests that underlying inflation remains relatively benign. However, getting food and energy prices under better control will be imperative to revive domestic demand. Japan is expected to release some of its emergency rice stockpiles to limit food inflation,13 but policymakers only have so much control over commodity prices. Given that these are globally traded commodities, events in other parts of the world, such as supply disruptions, can have outsized effects on their prices.

The value of the yen will also be important in getting these prices to come down. A very weak yen has translated into much higher prices for imported commodities, such as food and energy. The Bank of Japan can raise interest rates to provide upward pressure on the value of the yen. However, monetary and fiscal policies in other countries, notably the United States, can also affect the exchange rate.

For example, a more hawkish US Fed has led to a stronger dollar relative to the yen. Expansionary fiscal policies could add to the hawkish bent in US monetary policy. Plus, the implementation of tariffs in the United States could also lead to a stronger dollar and a weaker yen.

Slow rate hikes for now

So far, the Bank of Japan has taken a relatively cautious approach to monetary policy, raising rates from –0.1% to 0.25% in 2024. It then raised rates by another 25 basis points in January 2025.14 Despite several hikes, the policy rate in Japan is still far lower than it is in most developed economies. The central bank’s tentativeness around hiking rates likely reflects competing signals. On one hand, headline inflation has been running above its 2% target since April 2022.15 At the same time, the labor market has tightened, with wage growth accelerating. Higher rates would help get inflation back down to target by weakening demand and strengthening the exchange rate.

On the other hand, the economy remains relatively weak. Real GDP was just 0.4% higher than a year ago in the third quarter of 2024 and was still below where it had been five years earlier.16 Plus, the recent upswing in growth has partially been due to fiscal stimulus, which likely raises concerns about the health of the underlying economy. In addition, after removing the volatile food and energy components, inflation has been below the Bank of Japan’s 2% target since April 2024. Raising rates too quickly could weaken the economy further, and cause inflation to undershoot the central bank target.

The Bank of Japan is expected to continue raising rates, but its approach will likely remain cautious in the near term. During his press conference following the January meeting, Governor Ueda admitted that the central bank’s monetary policy stance remained accommodative, suggesting additional rate hikes can be expected. However, he also would not say that Japan had defeated deflation, hinting that additional monetary tightening would be relatively slow.17 The Bank of Japan has also expressed uncertainty about how US policy will affect the Japanese economy, adding to its tentative stance. Once the central bank has greater clarity on US policy, it may need to raise rates more aggressively. The yen barely appreciated after the rate hike in January,18 suggesting faster rate increases may be necessary to strengthen the yen and bring inflation under better control.

Trade can’t fuel growth forever

The benefits of a weak yen appear to be fading. Goods exports were up just 2.8% from a year earlier in December.19 For comparison, goods exports were up an average of 9.0% year over year for the first six months of 2024. Although the yen remains weak, it is not continuing to depreciate, limiting export growth. In addition, economic growth in its two largest export destinations, China and the United States, is expected to slow this year. Exports to both countries in December were lower compared to one year earlier (figure 2).20

Japan also runs a sizable trade surplus with the United States, which amounted to US$62.6 billion for the first 11 months of 2024.21 Policymakers in the United States have cited trade imbalances as a reason to use tariffs against them. As a result, Japan could find itself in a similar position. Indeed, the Reuters Tankan Survey in January revealed that manufacturers were concerned about US trade policy. Manufacturing sentiment in the survey increased slightly in January but remained very modestly positive.22

The slowdown in export growth is reflected in other manufacturing indicators. For example, manufacturing production was down 1.9% from a year earlier in November.23 Ongoing challenges in the auto sector contributed to a 9.6% year-ago decline in motor vehicle production.24 Although still positive, production growth of integrated circuits has fallen dramatically in October and November. In addition, the manufacturing purchasing manager’s index slipped to 48.8 in January—its lowest reading since March 2024.25 New orders fell at the fastest pace in six months. All of these point to a modestly negative outlook for Japan’s factory sector.

Japan’s economy has shown evidence that it is on the brink of stronger growth. Real GDP is rising, wage growth is accelerating, and the government continues to provide support to households. However, elevated inflation stands in the way of a stronger recovery. Meanwhile, the Bank of Japan has been hesitant to forcefully tighten monetary policy. In addition, gains from trade have slowed, and US trade policy threatens to restrain exports further while exacerbating the yen’s weakness.

{kind=link}

{kind=link}