East Africa economic outlook, February 2024

Despite internal conflict, inflation, and debt, in 2024, Ethiopia and Kenya not only show signs of economic recovery and resilience, but also growth.

Introduction

Amid a global economic landscape mired by supply chain constraints caused by conflicts and geopolitical tensions, the East African region continues to show signs of economic resilience and promise of growth. This is thanks to factors such as economic stimulus from various international organizations, renewed investor interest, infrastructure reforms, a healthy services sector, government efforts to nurture a healthy investor climate and to promote tourism after the COVID-19 pandemic, and good agricultural output.

Here are the economic outlooks for the region’s two largest economies—Ethiopia and Kenya—for the remainder of fiscal 2023 through fiscal 2024. Both show signs of slow but steady economic growth.

Ethiopia

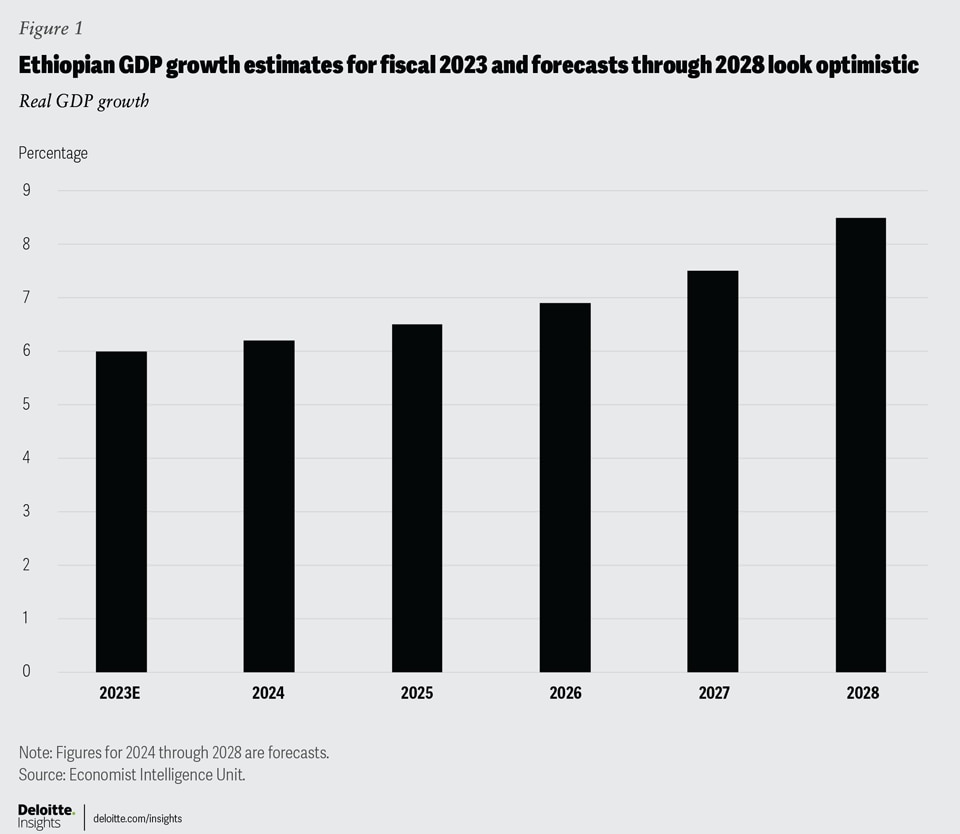

After various conflicts, including a civil war from 2020 through 2022, Ethiopia’s gross domestic product grew 5.3% in 2022 and is estimated to grow by 6.0% in 2023 (figure 1).1 In the medium term, the country—East Africa’s largest economy—is expected to average 7.1% GDP growth from 2024 through 2027,2 partly as it recovers from recent instability and partly due to the temporary debt-repayment suspension effected by its bilateral lenders, higher energy exports, and reform programs expected to attract foreign direct investment.

Similarly, a rebound in the services sector (which contributes about 38% of GDP)3—particularly in tourism—and the anticipated liberalization of the banking sector will be the primary drivers for this positive outlook.

For example, in 2024, tourist arrivals are expected to increase by about 12%,4 compared to 2023, boosting sector earnings by 35%,5 as travel restrictions ease and policies are implemented to integrate the tourism sector into the country’s regional economic strategy.

In the financial sector, deposit growth could reach nearly 27% in 2024,6 with the anticipated entry of international banks and other financial institutions likely to increase the adult population’s access to banks. This is also supported by growth in digital financial services underpinned by a growing telecommunications sector and Ethiopia’s digitization agenda.

Agriculture (which contributes about 32% of GDP)7 is expected to rebound, growing 4.7% in 2024,8 thanks to favorable weather conditions, adequate rainfall, privatization of state-owned sugar factories, and government initiatives in areas such as irrigation.

The industries sector (which contributes about 29% of GDP)9 is expected to be underpinned by the expansion of the manufacturing sector (about 12.5% in 2024)10 and driven by investments in industrial parks and transport infrastructure. Together with government investment and multilateral funding, this economic climate will also support growth in the construction sector. Investment in alternative energy sources (such as wind) will see energy production increase by about 14% in 2024, compared to a year ago, which will in turn boost energy exports.11

However, headwinds related to recurrent internal conflicts, a high cost of living limiting private consumption, fiscal pressures, challenges in doing business (extensive bureaucratic processes and limited access to foreign currency), and liquidity challenges weigh on the growth outlook.

Besides, inflation is another major issue for the Ethiopian economy. For example, inflation steadily increased to 33.9% in 2022, from 26.8% in 2021,12 mainly driven by the expansion in money supply and cost-push factors attributable to the global increase in fertilizer and fuel prices as well as supply chain disruptions in the country. Inflation is estimated to average 30.8% in 2023 (figure 2),13 as food and non-food price increases moderate.

While the inflation outlook is expected to improve from 2024 through 2027, inflation will still remain in double-digit territory.14 Factors like the depreciation of the birr, El Niño–related weather shocks, and internal conflicts continue to disrupt supply chains, posing upside risks to the inflation outlook.

Total household spending is expected to grow by 23.6% in 2023, driven primarily by high inflation. However, it is also forecast to contract by 5.7% in 2024, due to the depreciation of the birr and the effects of high inflation weighing down on the purchasing power of consumers.15

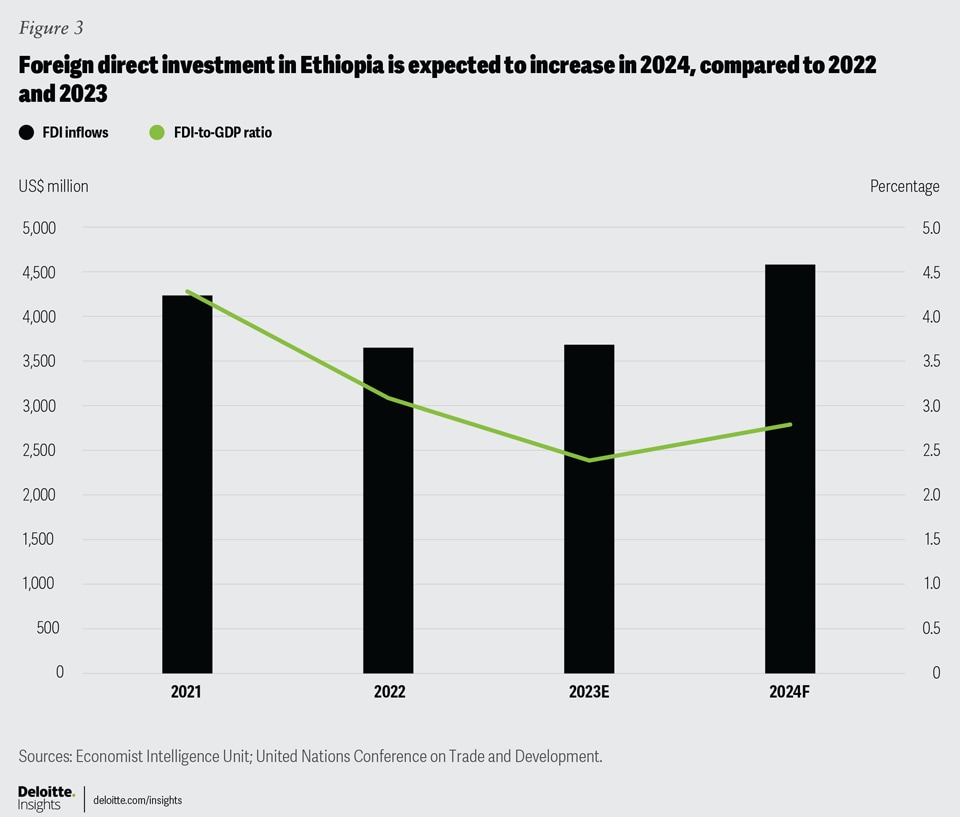

Ongoing investments in infrastructure and electricity and government’s commitment to economic reforms—including its privatization policy—are forecast to see foreign direct investment increase by over 24% in 2024 compared to 2023.16 This too will be supported by the development of special economic zones and the country’s focus on creating a safe investment climate.

Yet, despite strong inflows of expected foreign direct investment (figure 3), the Ethiopian birr is forecast to depreciate further—from an expected 56.4 per US dollar in 2023 to approximately 70 per US dollar in 2024.17 This is mainly due to increased imports, increased demand for the dollar, and higher global commodity prices. In 2022, Ethiopian foreign reserves and import cover decreased to reach only half a month’s cover at US$1.2 billion, pressurizing the foreign exchange market and widening the gap between the official and parallel market rate.

Ethiopia’s total debt stock grew by 10.8% in 2022, yet total debt as a share of GDP declined to 56.1% in the same year—down from 63.9% the previous year—driven largely by high inflation and sustained government borrowing.18 In December 2023, Moody’s downgraded Ethiopia’s foreign currency debt (foreign debt accounts for about half total debt), sending it into the “junk” category. This downgrade will increase the country’s cost of borrowing, further exacerbating the current liquidity crunch, even as the country received a temporary debt relief from its bilateral lenders. This scenario, following an initial downgrade in September 2023, occurred as the country defaulted on a US$33 million coupon payment on its international government bond.19

Kenya

Kenya’s real GDP growth rate decelerated from 7.5% in 2021 to 4.9% in 2022 and is expected to further decrease to 4.5% in 2023 (figure 4).20 This deceleration has been largely on account of global supply chain shocks, predicated by the Russia-Ukraine conflict, a global economic slowdown, and domestic constraints.

The country’s GDP is forecast to accelerate to 5.2% in 2024 and average 5.8% between 2025 and 2028 (figure 4),21 anchored by improved agricultural production and related exports, as well as growth in the services sector.

For example, agriculture, which is pivotal to Kenya’s economy as it still employs about 40% of the population and contributes about one-fifth of the country’s GDP, is expected to grow moderately by 1.7% in 2023 and subsequently by 4.5% in 2024,22 as it recovers from a contraction that occurred in 2022 and benefits from favorable weather and sectoral reforms.

In the services sector, tourism recorded a 62% growth as tourist arrivals23 surged after the relaxation of COVID-19–induced restrictions in most countries and due to ongoing government efforts to promote tourism. In tandem, international earnings from tourism increased and are expected to more than double from 2022 levels to US$1.8 billion in 2024.24 The country is investing in the development of transport and accommodation infrastructure and global marketing campaigns that are expected to boost the industry. Similarly, financial services have remained resilient and so there has been observable growth in the information technology sector as well—both linked also to the adoption of mobile-money services.

Growth is supported by improvements in access to electricity, and a focus on electrification in rural areas, with more than 87% of electricity generation coming from renewable sources.25

However, slower global economic growth, heightened debt levels, increased tax rates, interest rates, and fuel prices, and inflation pose significant headwinds to overall economic recovery, consumer spending, and investment.

Inflation accelerated to 7.7% in 2022 from 6.1% in 2021 due to high commodity and food prices and poor local agricultural performance that year.26 Fuel inflation remains the main driver of headline inflation, owing to the gradual increase in pump prices. This is expected to drive inflation to an average of 7.8% in 2023, before decelerating to an average of 6% between 2024 and 2028 (figure 4),27 as global supply chain constraints resolve, and food inflation abates due to government’s agriculture reforms.

The country’s central bank continues to implement tighter monetary policy aimed at bringing inflation down to within its target band of 2.5% to 7.5%. In December 2023, the Central Bank of Kenya hiked its policy rate to a record 12.5% from 10.5% set in June 2023, necessitated primarily by downward pressure on the shilling.28

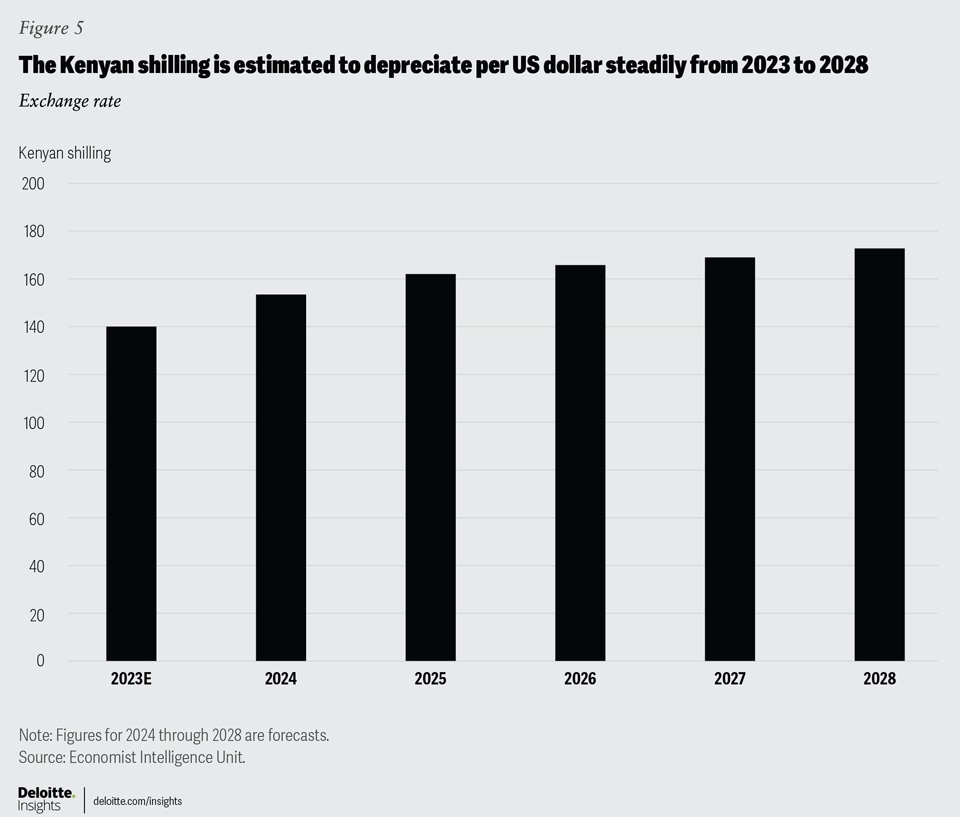

A stronger US dollar—thanks to the United States’ monetary policy–tightening stance—and increased demand for dollars from investors drove the shilling’s depreciation in 2023 (figure 5). The country’s central bank hopes that the higher lending rate will counter capital flight and help mitigate currency depreciation. As such, the shilling’s rate of depreciation should decline from 9.8% between 2023 and 2024, to 2.1% between 2027 and 2028,29 depending on the expected monetary policy–stance shift across major global economies, improved balance of payments, and reduced inflation.

Related to the above, inflows of foreign direct investment declined in 2022, driven by investor preference for more lucrative assets in developed markets. However, these inflows are expected to increase to US$611.5 million in 202430 due to improved investor confidence in the second half of 2023—anchored by recovering foreign exchange reserves, ongoing fiscal consolidation, and continued capital injection from the International Monetary Fund, the World Bank, and the African Export-Import Bank. Further, the successful implementation of ongoing structural reforms will boost investor confidence, increasing foreign direct investment to a forecast annual average of US$724.1 million between 2025 and 2028.31

Kenya’s debt-to-GDP ratio dipped to 67.3% in 2022 from 68.1% in 2021 and is expected to further decline to 67.0% in 2023, as the government looks to reduce borrowing. Total debt stock, as in June 2023, stood at KES10.2 trillion, of which KES4.7 trillion was externally sourced, while KES5.5 trillion was raised locally.32 Total debt is expected to increase to KES9.6 trillion in 2023 due to anticipated government borrowing to cover budget deficits in fiscals 2023 through 2024. The country has been implementing structural reforms, introducing new taxes, scrapping subsidy programs, and adjusting tax brackets, in a bid to raise internal revenues and reduce external debt burdens. These reforms saw lender confidence improve, and, as a result, the country unlocked funding worth US$0.9 billion from the International Monetary Fund in November 2023.33

In closing

Due to government efforts, both nations can be expected to not only grow and climb economic ladders, but also attract investors, which would in turn enable their governments to implement much needed systemic and structural reforms, especially in infrastructure and industries. While headwinds are still at work, our outlooks for 2024 for Ethiopia and Kenya remain cautiously optimistic.34

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}