Closing the digital divide: IoT in retail’s transformative potential has been saved

Closing the digital divide: IoT in retail’s transformative potential The Internet of Things in the retail industry

15 January 2016

The Internet of Things is poised to transform the retail industry, virtually eliminating the choice/customization trade-off and redefining sources of competitive advantage. And the return on investment may be more compelling than some retailers appreciate.

Introduction

Nearly two decades have passed since the Internet began to fundamentally reshape the retail landscape. From the earliest dot-com vendors to the rise of e-commerce giants, retailers old and new have grappled with the ever-evolving ways consumers find and purchase goods. Today, at last, many businesses are coming to terms with Internet-enabled retail, adopting omnichannel models that provide seamless shopping with greater choices and lower prices across online, in-store, and mobile platforms.

Yet even as the Internet’s place in retail strategy has come to define the new normal, another suite of technologies—the Internet of Things (IoT)—threatens to reshape the competitive landscape again. Through the deployment of sensors and the collection and analysis of the data they generate, the IoT opens new avenues to influence and augment actions, from urging you to get up from your desk and move, to replenishing inventory when a store shelf empties. While elements of the IoT, such as product-level RFID sensors, have long been used to overcome specific challenges in retail,1 the confluence of recent technological advances—cheaper and smaller sensors, omnipresent wireless networks, increased computing power, more sophisticated machine learning—makes the IoT poised to have a broader and more transformational impact on business.2

One way to understand this change is in terms of the strategic choices retailers have made to create competitive advantage. Here, the IoT looks set to break the very trade-offs that many retailers had been relying on to differentiate themselves from their competitors, such as offering greater product choice or increased customization. But it also creates new strategic choices that savvy businesses can exploit, helping them to close the new “digital divide” between consumer expectations and retailers’ ability to deliver.

All of this comes as the retail industry is again in a state of flux. The pace with which market share is changing hands—a proxy for competitive intensity—has increased every year since 2009. Over the same period, market concentration has decreased, with the top 25 established retailers losing the equivalent of $64 billion in market share to smaller players.3 Those who can capitalize on emerging technologies and challenge established ways of doing business will be well positioned to create new value. To that end, this paper will explore the implications of the IoT for retailers, as seen through the twin lenses of strategy and innovation. It will help you think through your current sources of competitive advantage; identify which—if any—could be undermined by the proliferation of the IoT; and identify new possibilities to differentiate yourself from competitors.

But to think about the future of retail, we begin by looking at the recent past.

From strategy to innovation: The rise of Internet-enabled retail

Competitive position in retail, like in any industry, is based on embracing trade-offs (see sidebar “Identifying innovation”). A company can offer a full-featured product that allows it to command premium prices, hopefully securing higher margins but at lower volume since fewer customers can afford the good. Or it might provide a bare-bones offering at a correspondingly lower price, relying on unit quantity to compensate for lower margins through high inventory turnover.

Companies face myriad such trade-offs, the dimensions of which will vary with the specifics of each product market. In automobiles, some of the trade-offs can be obvious, such as fuel economy versus power, while others are more subtle, such as weight versus warmth in sleeping bags for backpacking. Which trade-offs are manifest in a company’s products and business model define its competitive strategy.

Identifying innovation

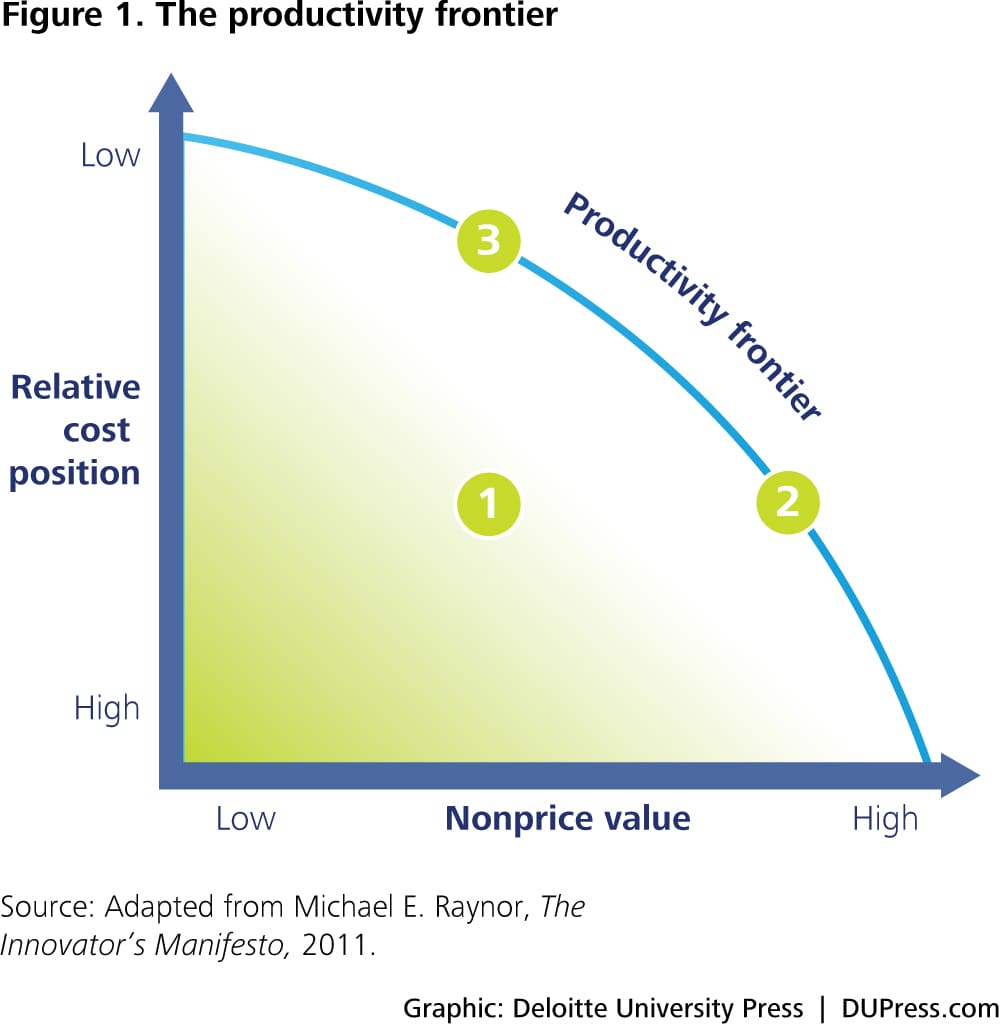

One way to define strategy is in terms of the trade-offs in the performance of the activities that define the value created by a business. The limits of what can be provided describe the “production possibility frontier” (PPF) for a business model at a point in time. To illustrate, in figure 1, at point 1, a firm can appear to deliver greater nonprice value without an increase in cost; that is, it can move “right” to point 2 (an increase in nonprice value) without moving “down” (an increase in cost). This is because a firm is merely wringing out inefficiencies that others already know how to avoid.

Once a firm gets to 2, however, that is as smart as it can work: The frontier defines the limits of what is possible at that moment. Of course, one could exploit different types of trade-offs, competing instead at 3 by moving “up” (a reduction in cost) from 2, but at the expense of moving “left” (a reduction in nonprice value). A company is strategically differentiated to the extent that it exploits a different set of trade-offs than its competition.

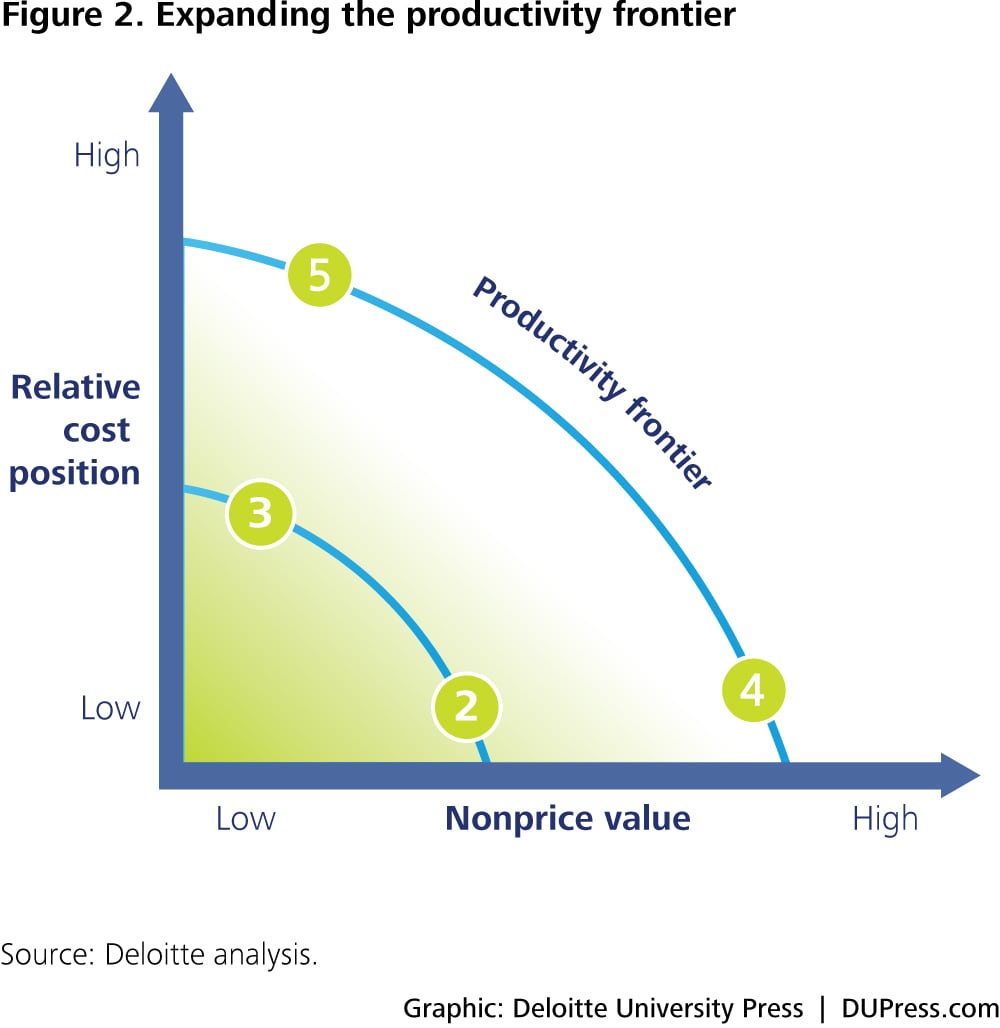

This model is powerful but essentially static, because it takes the PPF as fixed. But in most industries, these trade-offs have been broken over time, essentially “expanding” the frontier. For example, even the slowest CPUs today rival the power of top-of-the-line processors from several decades ago, even as prices have come down.4 A company competing based on nonprice value (point 4, figure 2) can offer more in absolute terms today than its similarly positioned counterpart (point 2) could in the past. The same holds for those competing on relative cost position. In short, the boundary of what is possible has expanded. Accordingly, we propose that strategy is defined by the trade-offs you exploit, while innovation is defined by the trade-offs you break.5

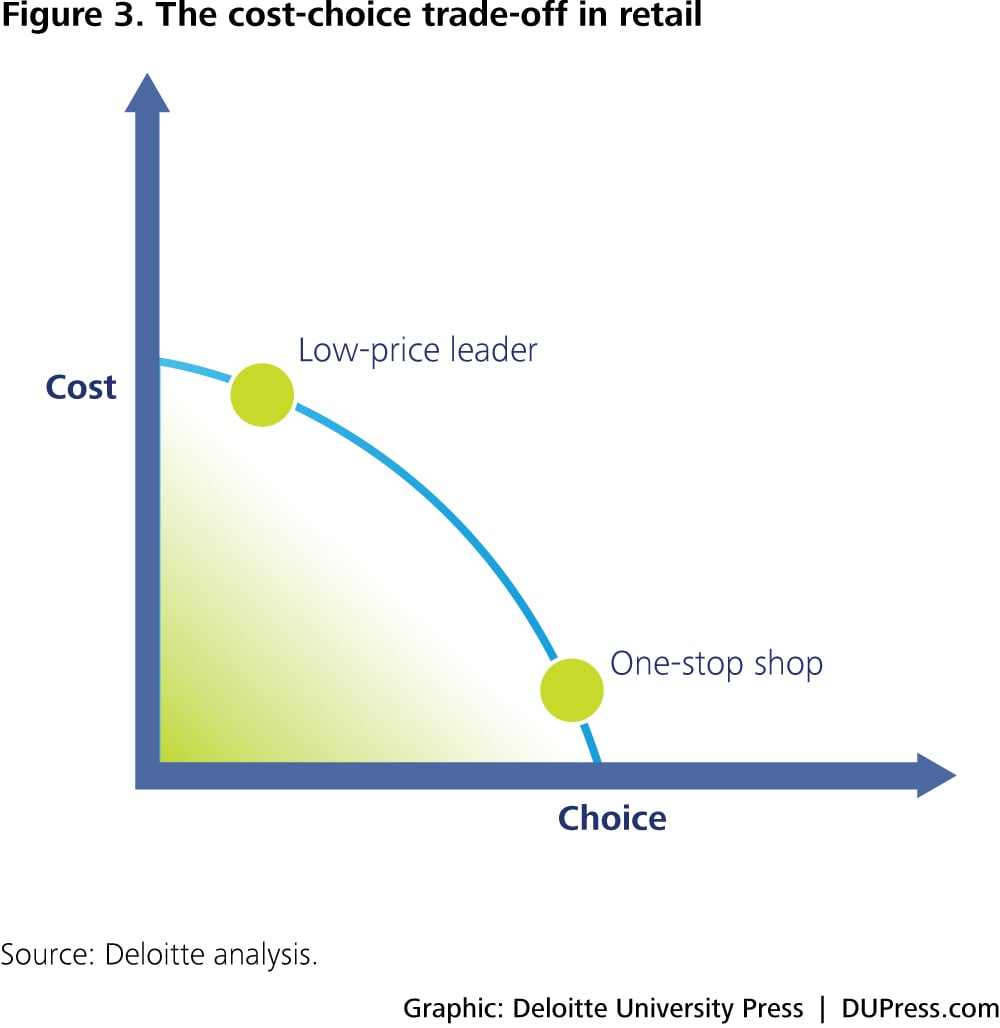

For most of retailing’s history, one important trade-off was driven by the costs and benefits of carrying inventory. Customers made purchases by selecting from the goods available on store shelves or in on-site stockrooms. Because retailers had few ways to accurately gauge who would want what when, the only way to provide customers with what “they” wanted was to physically carry the goods. Providing that higher level of choice necessarily meant increased inventory-related costs from sourcing, moving, and holding a larger variety of products. As a result, such retailers required higher margins, achieved through higher prices, to attain a comparable level of profitability as those offering fewer choices. (In reality, of course, such “high-choice” retailers would charge higher prices on “exclusive” goods and the same price as competitors on goods they both offered.) Alternatively, a retailer could provide fewer choices and enjoy lower overall inventory costs, which it could pass along to consumers in the form of lower prices or keep for itself with higher margins (figure 3). A company’s strategy was determined, in part, by how it chose to address this trade-off.

The cost-choice trade-off illustrated

To see how low-cost and high-choice strategies manifest, consider two prominent retailers: Costco and Target. Costco, representing the low-cost, low-choice approach, carried just 4,000 stock keeping units (SKUs) in 1995.6 Target, in contrast, had 65,000 unique products in stores the same year, suggesting a high-choice strategy (with correspondingly high inventory costs).7

These divergent strategies are reflected in the companies’ financial performance. Target was able to secure higher return on sales (panel 1 in figure 4)—driven by higher gross margin (panel 2)—relative to Costco; in short, it was likely able to charge higher prices in exchange for offering customers more options. That higher return on sales (ROS) helped compensate for its low asset turnover relative to Costco (panel 3), which was partly a byproduct of higher inventory carrying costs.

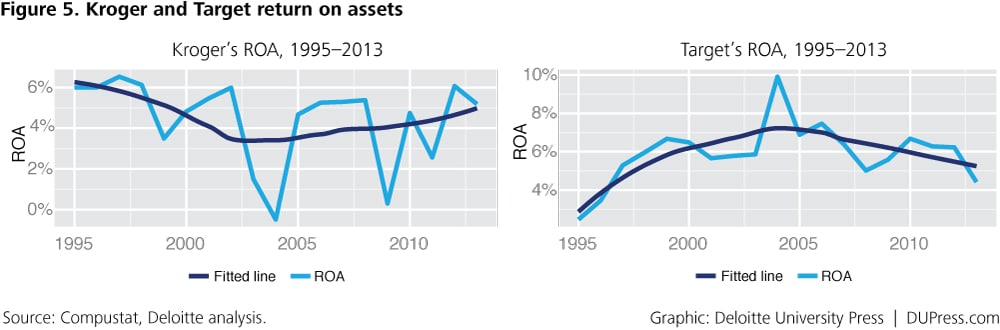

Finally, it is worth noting that neither strategy is inherently superior when it comes to overall profitability (panel 4). With the exception of a particular challenging year for Costco in 1994, the companies’ return on assets (ROA) largely track each other over time. When it comes to exploiting performance trade-offs, making a choice may be more important than the specific choice you opt for.

As the Internet has become nearly ubiquitous over the last two decades, the competitive advantage derived from either a cost- or choice-driven strategy has been steadily eroded. The Internet effectively broke the cost-choice limitation in the supply chain, contributing to the rise of omnichannel models, and even more fundamentally, blurring the line between digital and traditional retail. No longer is the customer limited to the stock on-hand; with the option to browse online, pick-up in store, or arrange delivery, every store effectively carries the products of the entire network. Now retailers can offer cheap with choice: the broadest range of products offered at the lowest possible price—a true innovation. Kroger, for example, carries 40 percent more SKUs today than it did in 1995. Target now offers 100,000 distinct items for sale in store; in 1995, that number was just 65,000.8 Yet, as figure 5 shows, neither company’s profitability has suffered systematically over that period.

Even more fundamentally, certain business models would scarcely be possible without Internet-enabled processes such as the ability to rapidly respond to shifting customer demand or effectively pool inventory across locations. In some cases, it allows greater choice at lower cost by increasing the speed with which products can be brought to consumers. For example, at “fast fashion” retailer Zara, clothing for each store is ordered and delivered twice per week, and only 50 percent of its designs for each season are finalized ahead of time (versus 80 percent at traditional clothiers).9 Zara headquarters consolidates customer feedback from across the globe, assesses patterns, and makes changes to clothing designs in as little as two weeks—a feat only possible thanks to the scale, scope, and speed of data transmitted via the Internet. Customers can now get the latest fashions at lower prices.

In other cases, the Internet increases the amount of time and space over which a given product is viable. Internet-enabled omnichannel allows retailers to offer more choices to more people at more times of the year. Because companies can have near-total inventory visibility and items can be shipped to and sold anywhere, they are no longer bound to a season-dependent stock. A retailer can carry shorts in California all year long, but still make them available to a customer in Buffalo in January. In a particular instance, Macy’s had 1,600 place-settings scattered across its stores—in ones and twos. Since dishes are typically purchased in sets of eight or twelve, the items were essentially stranded and likely to end up with deep markdowns. But because of store-level inventory visibility and online sales, Macy’s was able to piece together complete sets and sell them all at full price.10 The end result is more choice at lower total inventory cost. And for customers, it creates the opportunity to get whatever they want, whenever they want it.

The innovations spawned by the Internet in the 2000s help define the strategic frontier for today’s retailers. As consumers increasingly use digital technologies at every step of their retail experience, from initial inspiration to narrowing and validating choices through to purchasing and maintaining their new product, savvy retailers are embracing the seamless blending of the digital and brick-and-mortar experiences, focusing on reaching consumers during the “moments that matter.” To be sure, some retailers are farther along this transformative journey than others. But in our view, the retail environment of today—not tomorrow—is increasingly defined by the ability of companies to effectively capitalize on the innovations the Internet enables. In the early days, companies that embraced the Internet were able to separate themselves from the competition. Now, those who have not mastered Internet-enabled retail are increasingly being left behind.

The Internet of Things changes the game . . . again

As more retailers work to close the new “digital divide,” Internet-enabled models cease to be a source of innovation-driven competitive advantage and become simply table stakes. What choices, then, drive competitive differentiation in the Internet age?

While the Internet has done much to increase retailers’ access to consumers and their preferences, it still falls short of providing a “complete” picture of who wants what and when. This constraint is, in part, a product of the limited degree of connectedness between individuals’ online and offline lives. The Internet provides the customer the possibility of communicating their preferences to the retailer, but doing so often comes at a cost of time and effort. Because of this information gap, some retailers are focusing on offering the greatest degree of choice at the lowest cost to customers. Recall fast fashion retailer Zara, which introduces new products to its stores twice a week, rotating through over 10,000 distinct items in a year and prompting the average customer to visit 17 times per year (versus four to five for competitors).11 The challenge to such a strategy—and the irony of Internet-enabled “high-choice” retail—is that the ever-expanding set of available options may result in a less satisfying overall experience for customers, who face a form of “choice overload.”12 Indeed, a body of psychological research suggests that under certain conditions the proliferation of choices can leave individuals less content with the selection process overall and with the particular option they end up with.13

The trouble with choice

At first blush, it may seem counterintuitive that providing customers with more choices can actually leave them worse off. After all, much of the promise of market-based capitalism is that it offers more choices to more people than alternative economic models. At a theoretical level, expanding a choice set has often been treated axiomatically as, at a minimum, not making an individual worse off.14

Psychologists, however, have long theorized and gathered evidence suggesting that increasing levels of choice can contribute to anxiety, confusion, and an inability to choose.15 For example, researchers presented shoppers entering a grocery store with an assortment of jams and provided a coupon toward purchase. Some were shown 24 varieties, others just 6. Nearly one in three who were shown the smaller number ended up purchasing one of the jams, while just 3 percent of those who saw the larger display did so.16 In other experiments, participants reported being less satisfied with their ultimate choices when confronted with a large number of options.17

While additional research has softened some of these findings and added important mitigating factors (if the choices are familiar or the individual is an expert on the topic, an increased number of choices does not appear to have a deleterious effect, for example), retailers should still be wary of an approach that assumes more is always better.18

In response, retailers can opt instead to provide a bespoke product, which promises a superior customer experience enabled by higher staff levels and a “high-touch” approach—but at correspondingly higher cost. With sufficient information about the consumer, they can be provided the precise item they are interested in. The customization strategy thus avoids—but not obviates—the “paradox of choice.”19 For example, Trunk Club, now owned by Nordstrom, offers personalized clothing suggestions picked by an individual stylist and delivered at home.20

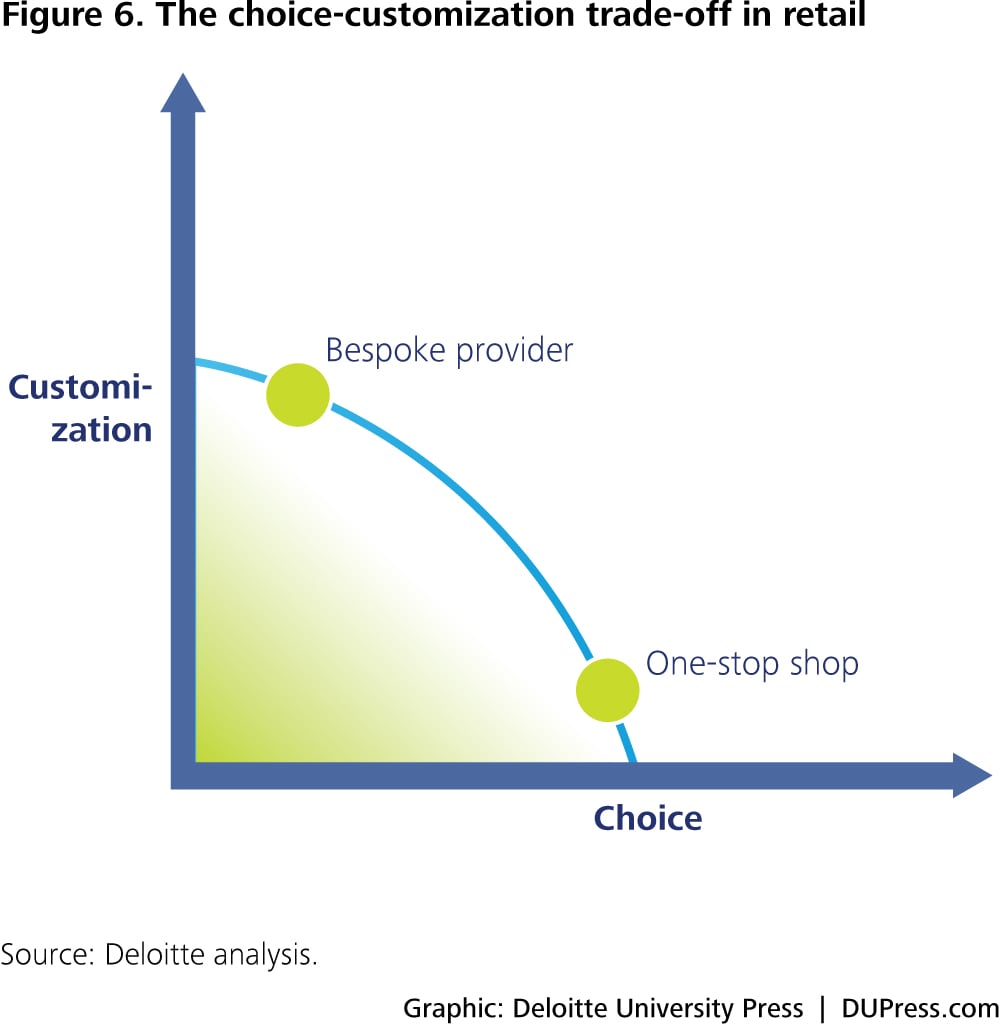

One newly important trade-off in retail, then, centers on the ability to offer increased choice on the one hand, and customized or tailored offerings on the other (figure 6). Yet even as retailers look to differentiate themselves along those lines, the Internet of Things looks poised to break that constraint as well.

To see how, note that the choice-customization trade-off is imposed by limitations in the collection, flow, and processing of information. Some data about the consumer, such as shopping patterns and preferences, can only be gathered at considerable cost to the retailer (via, for example, higher staff levels), the customer (who must volunteer said information), or both. Other types of data, such as knowing precisely when individuals enter a store and how they move about it, were effectively unavailable earlier. As a result, retailers could only make educated guesses about what a particular customer would want. High-choice retailers overcame this knowledge gap by offering a bit of everything, essentially making more “guesses” in the hopes that one would be right. Bespoke retailers responded by gaining intimate knowledge of individual customers; in effect, they made fewer “guesses,” but those guesses were better informed.

But as everyday objects are increasingly able to communicate information about their condition, and as that information is wed with other sources of data, companies can gain an increasingly fine-grained understanding of their supply chains and their customers. With the IoT, data that were either costly to collect or completely beyond reach can now be generated, collected, analyzed, and acted upon autonomously. For retailers, the growth of data—at scale—on specific customers and their habits and preferences, in particular, is enabled by the IoT. Coupled with new dimensions of information, such as a user’s location, and advanced analytics and artificial intelligence, retailers can guide consumers through a seemingly bewildering array of choices to the precise items they want, thus solving the “paradox of choice.”21

Now, for example, using real-time and historical information on a shopper’s whereabouts, history, and preferences, it is possible to offer a customized experience while still providing the broadest possible array of options. Imagine a customer walks into a store. A beacon at the entrance triggers the store’s app on her smartphone, prompting a customized welcome message to appear with several options, including “exclusive offers.” Selecting it, she sees a customized coupon based on her shopping and browsing background, as well as a “live” map directing her to the applicable products in the store. Using sensors to know when she has reached the relevant aisle, her app may highlight trending products. In the dressing room, a smart mirror allows her to see how the item pairs with other products. Once she’s made her choice and proceeded to the checkout, her smartphone—again triggered by sensors tracking her location—asks if she wants to apply the exclusive offer to her purchase. Finally, as she exits, a beacon triggers her app to thank her for the purchase and offers a complimentary music download.

For higher-end retailers, the IoT also creates opportunities for more powerful clienteling. In many cases, customers have done extensive browsing and research before ever setting foot in a store.22 By equipping store associates with that data, along with information about how frequently a customer visits the store, what they purchased on their last trip, and their typical spend, they can build deeper, more effective relationships. Picture the scenario above, but instead of a personalized message from an app, the customer is greeted by name by a staff member, who can personally deliver the customized offers, guide her through the store, and suggest options based on her previous purchases and browsing data.

Coming full circle

The IoT can break the customization-choice trade-off by enabling companies to create, collect, and act upon new sorts of data. To be sure, it is not the only trade-off that information can alleviate; for example, the tension between staffing levels and customer wait times can be mitigated by faster, more accurate data on store traffic patterns. But regardless of the specific trade-off being broken, the question for companies is: How to create value from this new information?

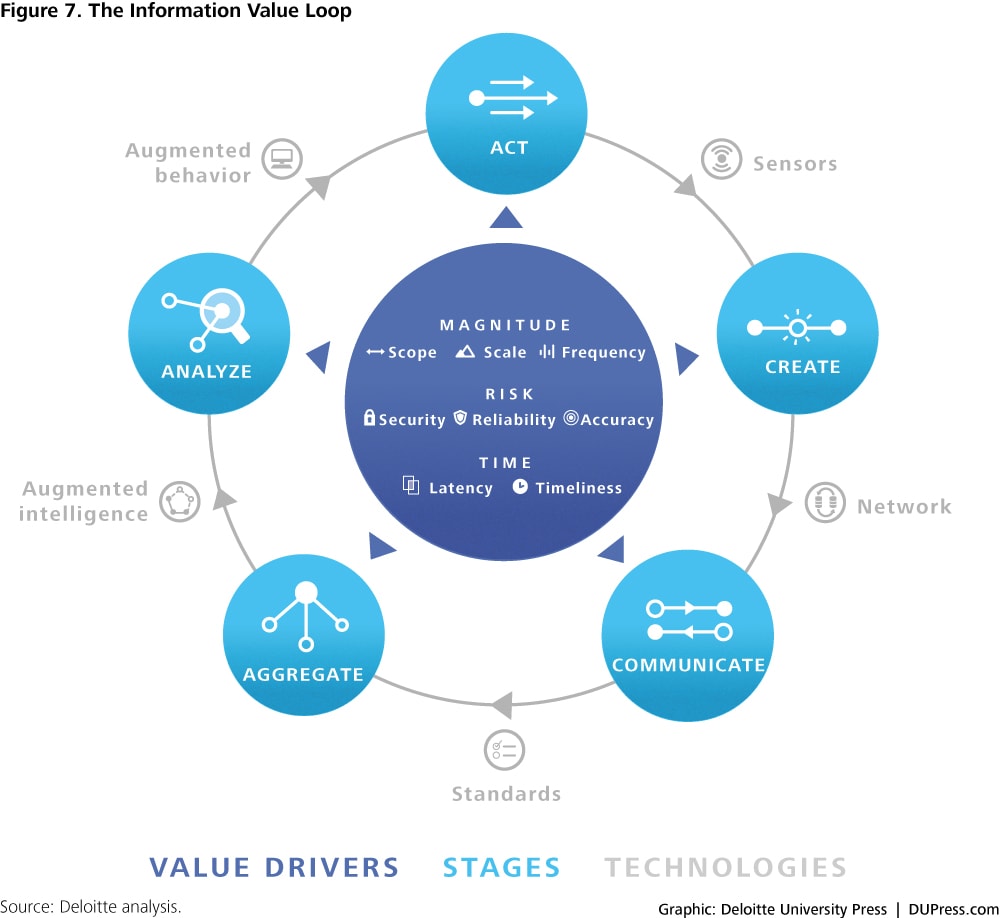

Information generates value only when it is used to modify future action in beneficial ways. Ideally, this modified action gives rise to new information, allowing the learning process to continue. Information, then, creates value not in a linear value chain of process steps but, rather, in a never-ending value loop. In completing a circuit of the value loop, from action back to altered action, information is communicated from its location of generation to where it can be processed.23 Information is aggregated over time or space in order to create data sets that can be analyzed in ways that generate prescriptions for action.24 These prescriptions guide modifications to actions. New action is then sensed, which creates new information, starting the cycle anew. We capture the stages through which information passes in order to create value with the Information Value Loop, shown in figure 7.25

Getting information around the value loop allows an organization to create value. How much value is created is a function of the “value drivers,” which capture the characteristics of the information that makes its way around the value loop.26 The value of information inheres largely in its flow: from being created through sensing action back to informing more effective action. As with any flow—say, cash—information’s value is a function of magnitude, risk, and time.27 All else equal, more information, generated at lower risk, and over a shorter time period will increase the information flow’s value. Different value drivers will have different levels of importance based on the specific value loop in question. For example, data collected on a customer’s movements about a store, transmitted over a network, aggregated, and analyzed might allow a retailer to generate value in the form of improved store layouts. Data on more customers, handled with increased security, and captured seasonally rather than annually are even more valuable. To be a true innovation, the IoT must alleviate the information constraint that has historically plagued retailers by moving data from its initial creation through to action.

Making the most of the Internet of Things

Today, the IoT’s impact on retail is in its infancy. Just 8 percent of retailers reported having already implemented or having plans to implement an IoT solution as of 2012, the lowest percentage of more than a dozen industries surveyed.28 But companies should not mistake a slow start for an indicator of the technologies’ full potential; the IoT of today and tomorrow is not simply a redux of earlier RFID experiments. As sensors proliferate, it seems inevitable that competitors will work to leverage its capabilities to undermine current sources of strategic differentiation. And with market share already changing hands more quickly than in the past—to the detriment of the largest retailers—the importance of thinking creatively and expansively about how the IoT challenges current sources of competitive advantage and opens new ones may be greater than ever.29 What can retailers do to not only avoid the pitfalls of this IoT-fueled transformation, but to capitalize on it?

Ask the hard questions

First, companies should be clear-eyed about the strategic choices they have made. What is your source of competitive advantage? Do you offer superior levels of choice, bringing customers a “one-stop shop?” Or does your primary source of differentiation lie in customized selection and service? What are the other relevant strategic trade-offs aside from choice-versus-customization, and where does your company fall on the spectrum of those options? Most importantly, determine which of these choices could be made obsolete by the Internet of Things. Just as the seamless blending of digital and physical commerce has erased the competitive advantage derived from offering lower prices at the expense of customer choice, the IoT will similarly undercut the value proposition of offering the broadest selection of products without a bespoke experience (and vice versa). In short, be prepared to have your source of differentiation eroded.

Test and learn, but don’t miss the forest

To date, most retailers have taken an incremental approach to adopting the IoT, using it to address specific problems, create targeted efficiencies, or tweak the customer experience. A test-and-learn tack can be an effective strategy, allowing a company to familiarize itself with IoT capabilities while keeping costs in check. It can also lay the groundwork for expansion into new areas of the business. Kroger, for example, recently installed sensors in its grocery stores’ refrigerators, creating an automated system that alerts store employees when temperatures spike, ultimately limiting spoilage. While the company sees an immediate return on investment, it also creates a springboard for further IoT applications. Kroger CIO Chris Hjelm sees “a pipeline of innovation, such as a mobile shopping system with laser scanners and network-connected LED lighting sensors, that [the company] believe[s] will take advantage of this infrastructure investment.”30 Consider which areas of your business would benefit from an immediate application of IoT technologies, and how you might branch out from there.

That said, the greatest value is likely to be created from more fundamental transformations of business strategies and models. Increasingly, deploying incremental IoT applications will be a necessary condition for keeping up with the competition, just as the ability to present a seamless online and in-store experience is today. But in our view, to separate from the competition requires a more holistic approach that integrates the IoT and its data with all aspects of the business, from sourcing to inventory management to customer experience. How, precisely, these more sweeping changes will manifest remains uncertain. But several important choices, discussed next, are likely to confront retailers willing to make the journey.

Where will you start generating data?

One important decision confronting many retailers arises at the initial create stage, where sensors generate the basic building blocks of the IoT. Creating data is easy, but a key consideration is how and what information is collected. Do you seek greater visibility into your supply chain and inventory, your customers, or both? If the latter, how will you collect the data? For many retailers, the easiest point of entry into the IoT may be to take advantage of the array of sensors most customers—and employees—are already carrying in their smartphones. But that raises other difficult questions. Are data generated only on an opt-in basis, or is blanket collection used to sweep up all customers’ information? The latter has appeal in that it likely generates greater quantities of information, and that information is less likely to be biased toward a particular type of shopper. However, the undifferentiated collection of data poses real risks, especially when coupled with limited levels of individual consent; some companies have rolled back IoT programs in the face of customer resistance.31 Consumers may be willing to surrender increasing amounts of personal information to companies, provided they feel they are capturing sufficient value to make the incremental loss of privacy worthwhile.32 It is incumbent upon retailers to demonstrate how IoT-generated data benefits not only companies, but customers.

Importantly, consider how you will use the data you collect—before you collect it. If your answer starts with, “To better understand…,” you may need to think harder about how the data can be used to augment behavior.

Are your data fast enough?

Once data have been generated, the timeliness and latency with which it is communicated will often determine how valuable it will be in breaking the choice-customization trade-off. For example, a sales manager wants to be able to influence customer decisions, and that can require knowing what customers want now and here. This can require information with higher frequency, accuracy, and timeliness so that the retailer can influence customer action in real time—through, for example, complementary products or incentives. This can require near-instantaneous responsiveness; having a system in place that anticipates and responds to customers on the spot represents a big step beyond, say, mailing coupons days after a purchase, but even these can be irrelevant or not timely enough.33

Can you make sense of IoT data?

As important, retailers need to carefully consider the aggregation and analysis challenges that come along with the IoT. Companies are already struggling to make use of the data at hand. Over half of retail CIOs surveyed in 2015 reported that “turning massive amounts of data into usable business insights” was among the five greatest challenges, according to the National Retail Federation and Forrester.34 How will you gather and store—safely—the increased quantities of data the IoT generates? Do you have the analytic resources to quickly make sense of it?

Where will you reach the customer?

Finally, influencing action may be the critical stage for most retailers; after all, if customers fail to respond, all of the information created by the IoT is of little practical value. Here, companies need to consider which point or points in the shopper’s journey they seek to influence, and how the IoT can make that influence more effective.35 Some interactions might happen before a customer has fully realized their want or need; imagine knowing that a person has recently increased the frequency and distances of their runs based on data from a personal activity tracking device, allowing the retailer to push targeted advertising about running shoes and apparel. At other points, retailers might seek to reach a customer as they narrow down their choices. For example, as our newly committed runner peruses sneakers in the store, sensors on the shelf can trigger product information and reviews to appear on his app as each shoe is lifted from the shelf. Later, triggered by a sensor at the point of sale, an item-specific coupon can be pushed to the customer’s smartphone. And the opportunities for IoT-enabled retail continue beyond the day of purchase with “smart” goods that can monitor their own condition and alert the user—and the retailer—when service or replacement is recommended. Consider sensor-equipped sneakers that can track your runs and let you know when it is time for a new pair.

Of course, there are multiple ways retailers might address the challenges and opportunities presented by the IoT; there is no “one size fits all” solution. But when a company can successfully complete the Information Value Loop, it can create a powerful experience for its customers, bolster loyalty, and generate greater nonprice differentiation for itself.

The business case for the Internet of Things

One consistent barrier to wider adoption of the IoT by retailers arises from the costs involved. These include not only the deployment of sensors, but also the maintenance of networks and storage space to communicate and collect the data they generate and the investment in analytic tools and skills to make sense of it all. For a low-margin business like retail, these costs may seem prohibitive and can deter companies from taking the IoT plunge. Earlier forays into RFID, including some well-publicized setbacks, can leave retailers questioning the return on an IoT investment.36

But the technology today is not the technology of even a few years ago. The price of sensors, for example, has declined dramatically; an accelerometer that cost $2 in 2006 costs just 40 cents today.37 What’s more, consumers are already carrying an array of sensors—their mobile device—that retailers can tap in to. The price of moving data across networks and securing storage space have also plummeted, and there is little reason to think the costs of IoT technology will not continue to decline.38 Likewise, the return on investment may be more compelling than some retailers appreciate. In a 2014 survey of large soft-line retailers, 40 percent of those who had implemented RFID for inventory accuracy and replenishment reported a gross margin improvement of 5 percent or greater.39 And anecdotal evidence from retailers employing smart mirrors in dressing rooms suggests the technology is helping to secure higher conversion rates.40

Conclusion

The Internet fundamentally reshaped how retailers operate. As the long-standing trade-off between inventory-related costs and customer choice weakened, old sources of differentiation disappeared and new competitors emerged. Today, with the near-ubiquity of digital influences on customers’ retail experiences, “e-commerce” has become simply “commerce,” with customers increasingly expecting a seamless interface between their online and in-store experiences.41 As retailers have grappled with this challenge, some have sought to maximize the choices available to consumers, while others have brought a more tailored approach to giving customers what they want.

Even as retailers have begun to come to grips with a new set of strategic choices, another technological innovation—the Internet of Things—seems set to undermine some of today’s sources of competitive advantage. The automated collection, aggregation, and analysis of new sorts of data provide a way for retailers to offer a customized experience for consumers while still drawing from a large pool of product options.

To take advantage, retailers should be honest with themselves about the strategic choices they have made, and think hard about which of those choices might be rendered obsolete by the spread of IoT technologies. A “more options” approach might be received coolly by customers who increasingly demand an individualized experience built on their own history, preferences, and needs. Similarly, bespoke providers could see consumers asking for options beyond what they are prepared to provide. But along with the critical assessment of current strategic choices, retailers should also consider how the IoT can create value for them and their customers.

Our own thinking on the Internet of Things in retail continues to evolve, and we expect to share additional perspectives in the coming months. But one thing seems clear: Companies able to address the thorny problems the IoT poses around data management, privacy, analytics, and other areas will likely be well-positioned to separate themselves from competitors. To truly build value from IoT investments, retailers should be expansive in their thinking, considering innovative applications and the use of supporting technologies, such as augmented intelligence.

Deloitte’s Internet of Things practice enables organizations to identify where the IoT can potentially create value in their industry and develop strategies to capture that value, utilizing IoT for operational benefit.

To learn more about Deloitte’s IoT practice, visit http://www2.deloitte.com/us/en/pages/technology-media-and-telecommunications/topics/the-internet-of-things.html.

Read more of our research and thought leadership on the IoT at http://dupress.com/collection/internet-of-things/.