Putting a price on transparency How providers can win in a transparent market

15 minute read

26 August 2020

Christi Skalka United States

Christi Skalka United States Christopher Murray United States

Christopher Murray United States Laura Oman United States

Laura Oman United States Joey Glass United States

Joey Glass United States

As consumers increasingly shop for health care services, providers have an opportunity to build trust with their patients and differentiate their organizations by leading the way on pricing transparency.

Introduction

It's a story we’ve heard before. Maria was on a ski trip with her friends when she hit a patch of ice and fell, tweaking her shoulder in the process. She waited a few days to see if her mobility would improve, but it soon became clear that she will have to visit a doctor soon. Maria’s primary care physician provided multiple referrals, but she was surprised to discover that few of the recommended providers had price or quality information readily available on their website. Even when she called, she was only referred to a hard-to-interpret set of list prices and told to contact her insurer.

Learn More

View the related infographic

Explore the Health care collection

Learn about Deloitte's services

Go straight to smart. Get the Deloitte Insights app

Instead, imagine a world where Maria has at her fingertips all the information she needs to make a health care decision. Using her mobile device, she can pull up an app, enter her location and some basic qualifying information, and hit “search” to instantly review provider ratings and list prices and compare out-of-pocket (OOP) estimates. Everything is organized, clearly defined, and easy to understand. Once she picks her provider, she is directed to a patient portal where she can schedule an appointment, upload images, preregister, and even prepay for her visit to make check-in a breeze. In this utopic vision, Maria’s health care experience feels personalized and uniquely tailored to her medical and financial needs. It is the experience and validation many of us look for before making much less critical decisions such as which phone to buy or which hotel to stay in on vacation. This is a world in which Maria can quickly compare a handful of imaging centers in her area and make a decision based on meaningful information, all without leaving the comfort of her couch.

For many, this world seems like a distant fantasy. Today’s health care reality reflects the status quo of distrust, doubt, and uncertainty that many American patients experience every day.

There is a growing disconnect between patients wanting to shop for their care and hospitals fighting to keep prices a secret.1 Studies show that 60% of patients are more likely to choose a provider that publishes its prices in comparison to the local market,2 yet 75% of respondents in a recent Harvard survey said they were not aware of an existing resource that would allow them to compare costs across different providers.3 Not only was Maria frustrated that she couldn’t find price and quality data for the radiologists, she questioned the underlying reasons for its absence, wondering why providers seem to intentionally make it as difficult as possible. Patients aren’t just dissatisfied anymore—many are becoming fearful and distrustful of a system that seems to be purposefully obscuring information.

One way to regain Maria’s trust is to give her more control over her health care decisions,4 and achieving that level of control requires more information transparency on the part of health care providers. These changes in consumer expectations, paired with disruptive regulation, and even the recent COVID-19 pandemic, are forcing plans and providers to evaluate the intersection points of pricing with their patients. In order to drive meaningful patient engagement, providers should focus on leveraging their brand equity in the market and pair consumer-friendly pricing information with quality metrics and outcomes in a truly authentic manner. We believe the transparency imperative presents an opportunity for consumer engagement and can result in improvements to patient satisfaction and experience, rebuilding consumer trust, and, ultimately, increasing market share.

EXPLORE THE INFOGRAPHIC

The price transparency regulatory environment provides an opportunity

An executive order5 signed by President Trump on June 24, 2019 required the secretary of Health and Human Services to propose regulation that takes a critical step toward pricing transparency in health care. The new regulations, set to go into effect January 1, 2021, require hospitals to publish a list of all standard hospital charges, including patient responsibility estimates and negotiated rates with payors, in a consumer-friendly format. While many providers likely reacted in shock to the recent Federal judges’ rejection of the American Hospital Association lawsuit6 filed to dispute this requirement, initiating a legal battle or meeting the bare minimum requirement is only a short-term solution. It is important to take a step back and observe the larger market landscape: Information transparency efforts are intended to accelerate market disruption, and providers that ignore the new requirements may be caught in an unfavorable competitive position trying to regain market share from their more innovative counterparts. To address public trust and regulatory considerations, providers must drive toward greater transparency in their patient communications, their charge structures, and their overall pricing strategy.

Consumer conjoint survey: Evaluating the drivers of provider selection decision-making

Evidence from many recent studies, including Deloitte’s 2020 Survey of US Health Care Consumers,7 suggests patients are exhibiting more traditional “consumer behaviors” each year, implying that more patients are actively shopping for their health care. We sought to go a level deeper and test which factors truly make or break health care decisions in the provider selection process. To understand in detail the impact of price transparency and the mechanics behind how patients, such as Maria, select providers for elective procedures, we conducted a discrete choice-based conjoint survey, supplemented by traditional survey questions about respondents’ health care and technology savviness, preferences, and experience.

A conjoint survey simulates a real-life purchase scenario by providing respondents with several “product” options with varying characteristics, from which they are asked to select their preferred option. Respondent selections are analyzed to identify patterns and understand which attributes contribute most significantly to decision-making. In this case, survey respondents were provided a randomized choice of three health care providers from which they could receive an MRI of the shoulder (see figure 1 for an example of a conjoint window.)

Each respondent was presented with different combinations of the following factors, or “attributes:”

- Quality (represented by Medicare star rating)

- Availability of an out-of-pocket estimate prior to the procedure

- Recommendation source

- Procedure list price

- Out-of-pocket (OOP) payment (i.e., patient’s personal liability)

Each attribute appeared in each conjoint question at one of three levels, as outlined in figure 1.

In addition to the three provider options, respondents had the option to select “None of these.” This selection would indicate that a respondent may prefer to defer care rather than receive the MRI from any of the three providers with the attributes offered for a given question. Respondent choices were used to analyze the utility of each provider attribute and level.

Inside the survey

An MRI of the shoulder was selected as the survey procedure as it is nonemergent, shoppable8 (defined by CMS as “a service package that can be scheduled by a consumer in advance”), and homogeneous across providers. We believe preferences indicated by the survey respondents are representative of other shoppable health care services, but the results may not apply to urgent, emergent, or highly complex procedures where patients do not have the ability to deliberately evaluate attributes before selecting a provider.

We distributed the survey to 1,263 respondents, with demographic screening to develop a relevant data set (e.g., excluded respondents under the age of 18 and those who had not received medical care in the last two years). Following this screening, 403 qualifying respondents completed the conjoint study, each responding to eight different randomized provider selection choices. To ensure a representative sample of health care decision-makers, respondents were prescreened to ensure significant representation across gender, age, income, marital status, health insurance status and type (high deductible health plan), and status as a primary caregiver.

Survey key findings and implications

Transparency can translate into patient volume

Each year, an increasing number of patients exhibit what we consider traditional consumer behavior when it comes to their health care decisions. Key findings from Deloitte’s 2019 Global Health Care Consumer Survey highlighted how the use of pricing and quality tools continues to rise as more consumers choose to proactively shop for their health care. Maria’s online search is becoming the norm: The percentage of health care consumers who look up cost information nearly doubled between 2016 and 2020, from 14% to 24%.9 In our own conjoint survey, 40% of the respondent population said they shop around when choosing a provider for their health care needs. Simply making meaningful price and quality information more accessible to consumers may be enough of a differentiator for providers to increase patient volume. This insight is particularly important as elective services are restored in the wake of the COVID-19 crisis and losses to disposable income drive further demand for predictable expenses. Our conjoint survey results support that providers offering new tools and technologies allowing customers to take control of their health care experience will be in a favorable position to increase market share and improve patient satisfaction.

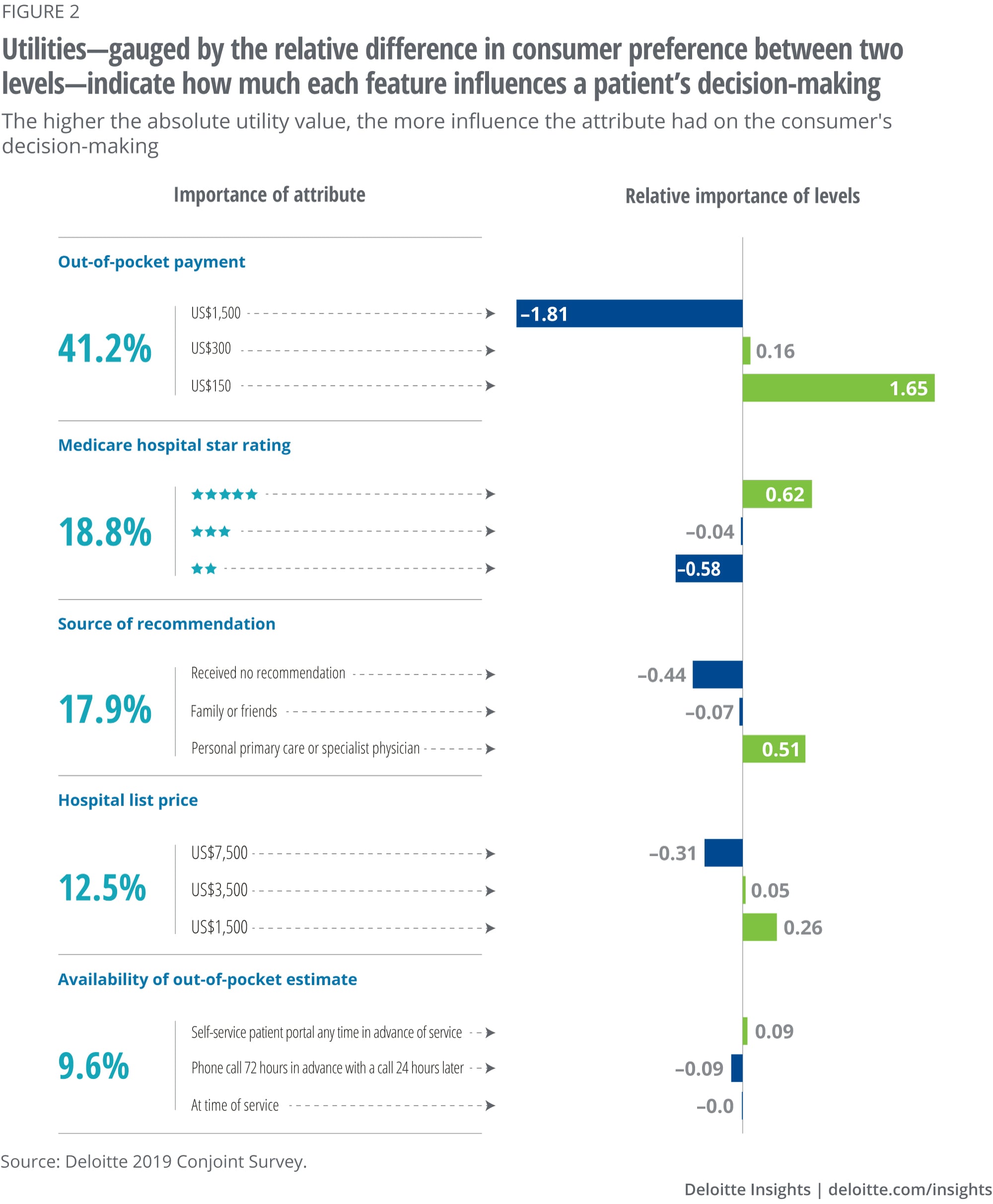

Patient liability is the most significant attribute for provider selection

It’s no surprise that patients care about costs. Of the five attributes tested in the survey, OOP payment carried the most weight with respondents, driving 41% of respondents’ decision-making. Let’s stop and reflect on this finding for a moment: The most significant decision-making factor for patients shopping for health care is the one most providers fail to provide in a consumer-friendly manner, as Maria found in her fruitless search. According to Deloitte’s 2020 Survey of US Health Care Consumers, a third of health care consumers are already engaging in consumeristic behavior such as shopping for deals and comparing quality information.10 As more patients shop for health care, providers and plans must implement new digital tools to respond to an increasingly demanding and sophisticated consumer.

High-quality providers can use transparency to attract consumers and command higher prices

While OOP liability is clearly a critical element of provider selection, consumers do take a holistic view of the options available to them. When we tested the trade-off between OOP payment and quality in a market share simulation, we found that respondents generally preferred lower-cost, lower-quality providers over higher-cost, higher-quality counterparts. However, when looking specifically at providers with the highest list prices, this effect reverses. Put more simply, respondents were willing to pay more out of pocket for quality if the corresponding list price was higher, anchoring the respondents at a starting higher price. This finding illustrates the value of providing transparent information, and when used effectively with other data points, list prices can serve as an anchor to highlight and attract patients to superior-quality providers. This result may also indicate that fears of a “race to the bottom” with price transparency are premature; rather, transparency provides an opportunity for high-quality providers to command higher prices by thinking strategically about how to share pricing information with patients in conjunction with other tools such as marketing and patient experience efforts.

All consumers may not value or understand health care prices similarly—patient education is key

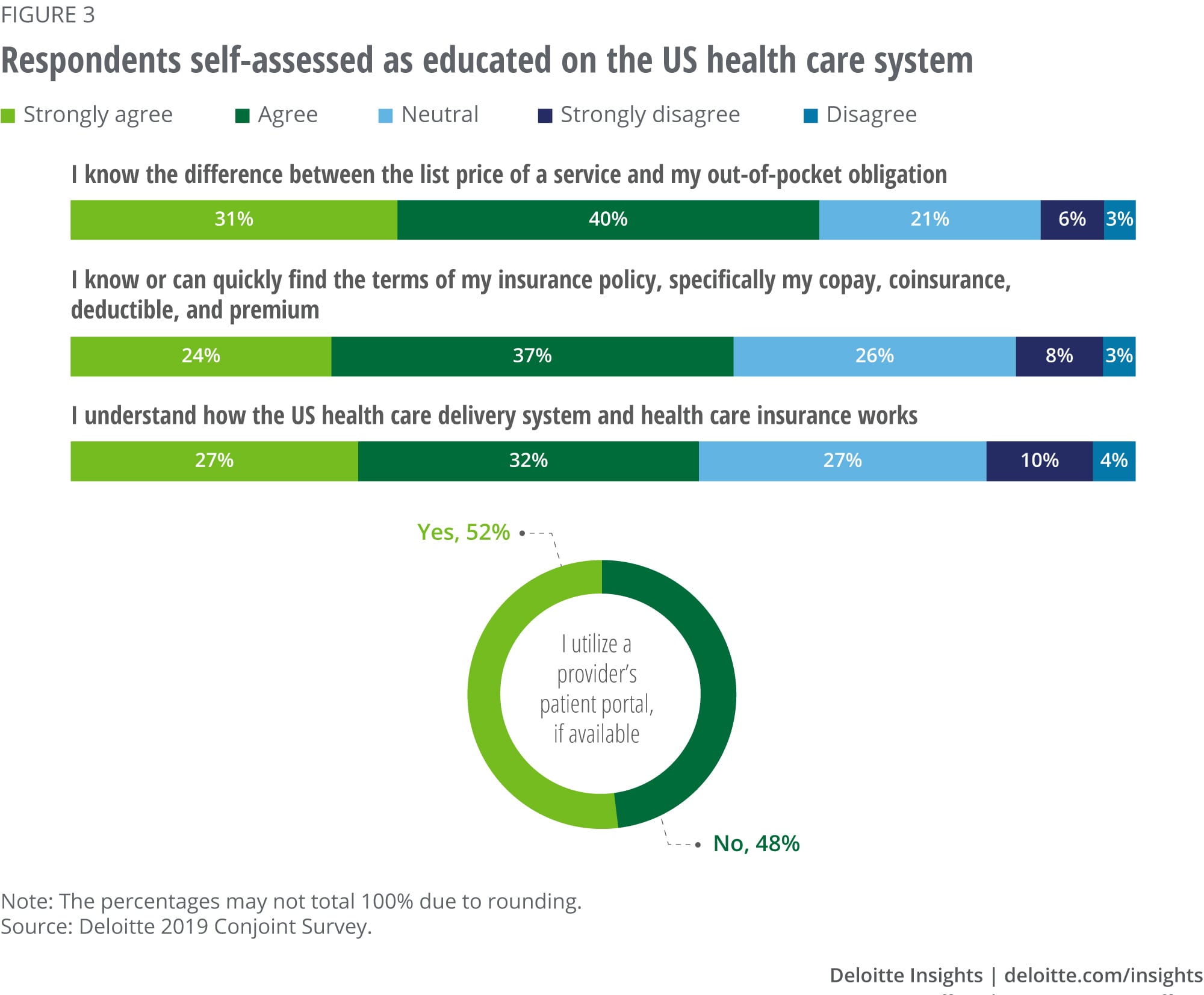

In our survey results, 62% of the respondent population indicated that they understand the difference between a hospital’s “list” prices and their own OOP payment. As evidence of this knowledge, list prices contributed just 12.5% to the decision-making process between different providers, indicating an understanding that list prices alone don’t convey the information they desire. The new rule on price transparency requires hospitals to post list prices (i.e., charges), but our survey results indicated that this charge information may not be particularly helpful, nor is it a large driver of the decision-making process. In fact, there is still a significant segment of the respondent population that acknowledged a lack of familiarity with these health care pricing terms (i.e., list price vs. OOP payment), and all else equal, survey respondents indicated a preference for lower list–priced providers. These results highlight the significance of educating the patient with meaningful price and cost information to have an authentically transparent conversation with consumers about the cost of care.

Price transparency has important population health implications

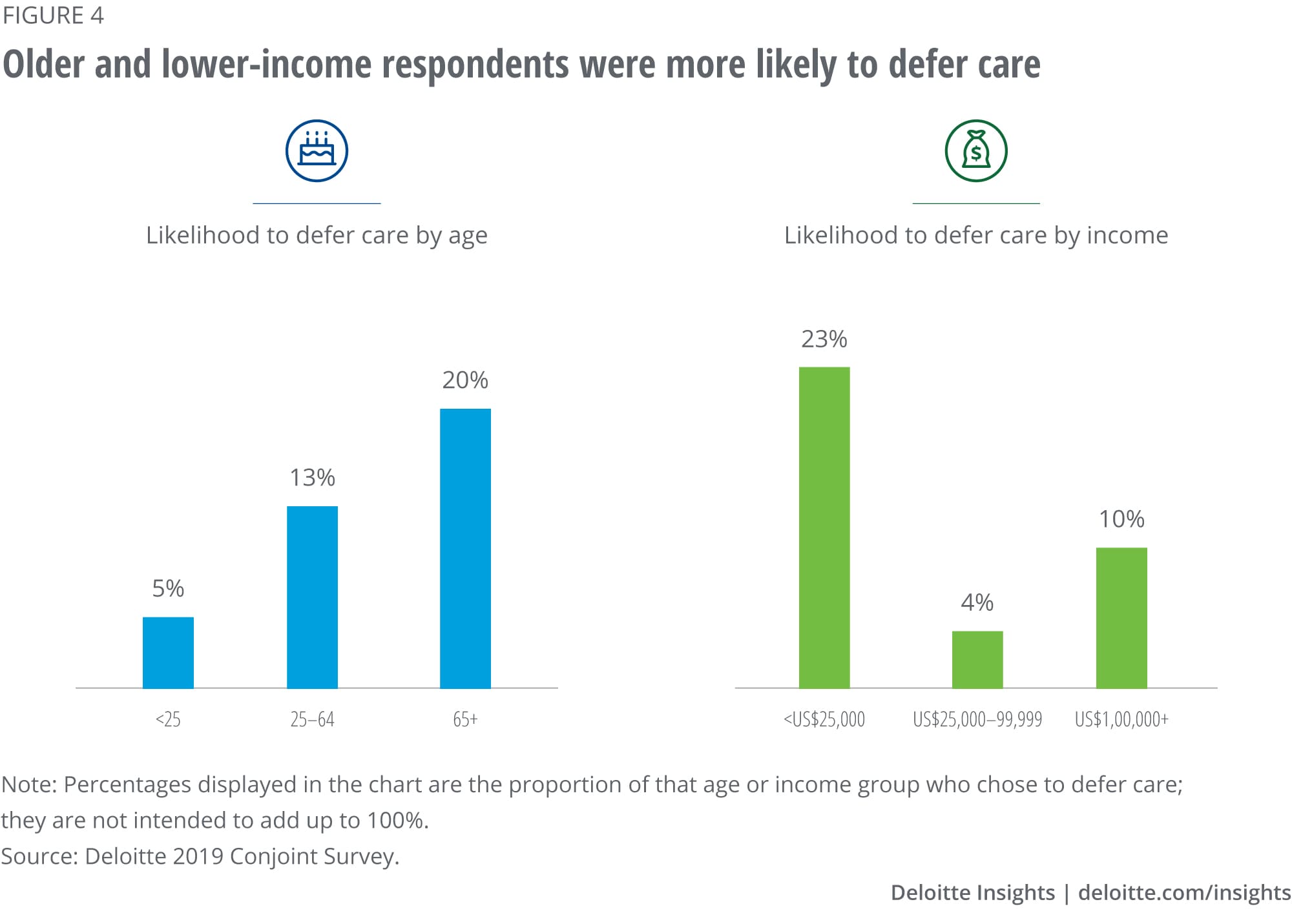

Based on the three provider choices made available, respondents chose to defer care (i.e., selecting the “None of these” option) 13% of the time. The choice to defer was often driven by the OOP payment choices available. When respondents were shown three randomized provider options, all of which included the highest level of OOP payment, they chose to avoid care a third of the time.

Our findings highlight a common issue: One in four Americans skip out on care because of cost concerns,11 which can undermine population health objectives and not only worsen health care outcomes, but also drive higher health care costs when unaddressed issues turn into emergency care needs. This trend has extended to COVID-19, with nearly 15% of Gallup survey respondents recently acknowledging that they would skip getting medical help even when exhibiting COVID-19 symptoms due to anxieties over cost.12 These findings underscore the need to align price transparency efforts with a thoughtful self-pay strategy including flexible financing to support affordability.

In the conjoint study, deferment of care appeared to be more common among potentially vulnerable populations. While individuals aged 55 and over made up 44% of the survey population, they accounted for 75% of the decisions to defer. Similarly, lower-income respondents were three times more likely to defer care than higher-income respondents. However, the conjoint survey results also showed that there appear to be actionable possibilities to change this outcome. Health care–focused ride-sharing technology and services are growing more common to improve access to care, and our survey results show that the right combination of transparent information can make patients more likely to obtain care. Respondents who chose to defer care at least once in the survey most frequently deferred only once (out of the eight questions provided to each individual), indicating that patients are deferring care based on addressable, specific provider information that can be tailored for an improved patient experience to encourage a visit.

Price transparency and the physician network can overcome a gulf in quality

Some of the attributes included in the conjoint survey are harder to influence; for example, it may take years of effort to improve Medicare star ratings or other perceptions of quality. However, the availability of price estimates is more directly and easily influenceable in the short term. The survey also tested the impact of providing an earlier OOP estimate in combination with a physician referral against different quality ratings and found that these two addressable attributes can attract patients to lower-rated providers. Our analysis showed that a greater proportion of patients would choose a provider with a two-star quality rating with a price estimate and a referral than a nonreferred five-star provider that does not provide an estimate. This effect reflects a health care reality that interpersonal elements of care have a greater influence on patient experience than harder-to-interpret quality data. In a recent study,13 more than two-thirds of surveyed diabetes patients and women who had recently given birth reported their physicians’ interpersonal qualities as an important factor in rating care as high quality, whereas less than half reported the same about various clinical outcomes. This reality may have been even more apparent in our survey results had we not used a simple quality metric such as stars. Judith Hibbard’s research on price and quality interactions has shown that patients make better choices with easy-to-interpret quality ratings than more idiosyncratic metrics such as length of stay.14 Influencing patients’ experience by focusing on referral networks and making it easy for cost-of-care questions to be answered can be key to building trust above and beyond what can be communicated through traditional quality metrics.

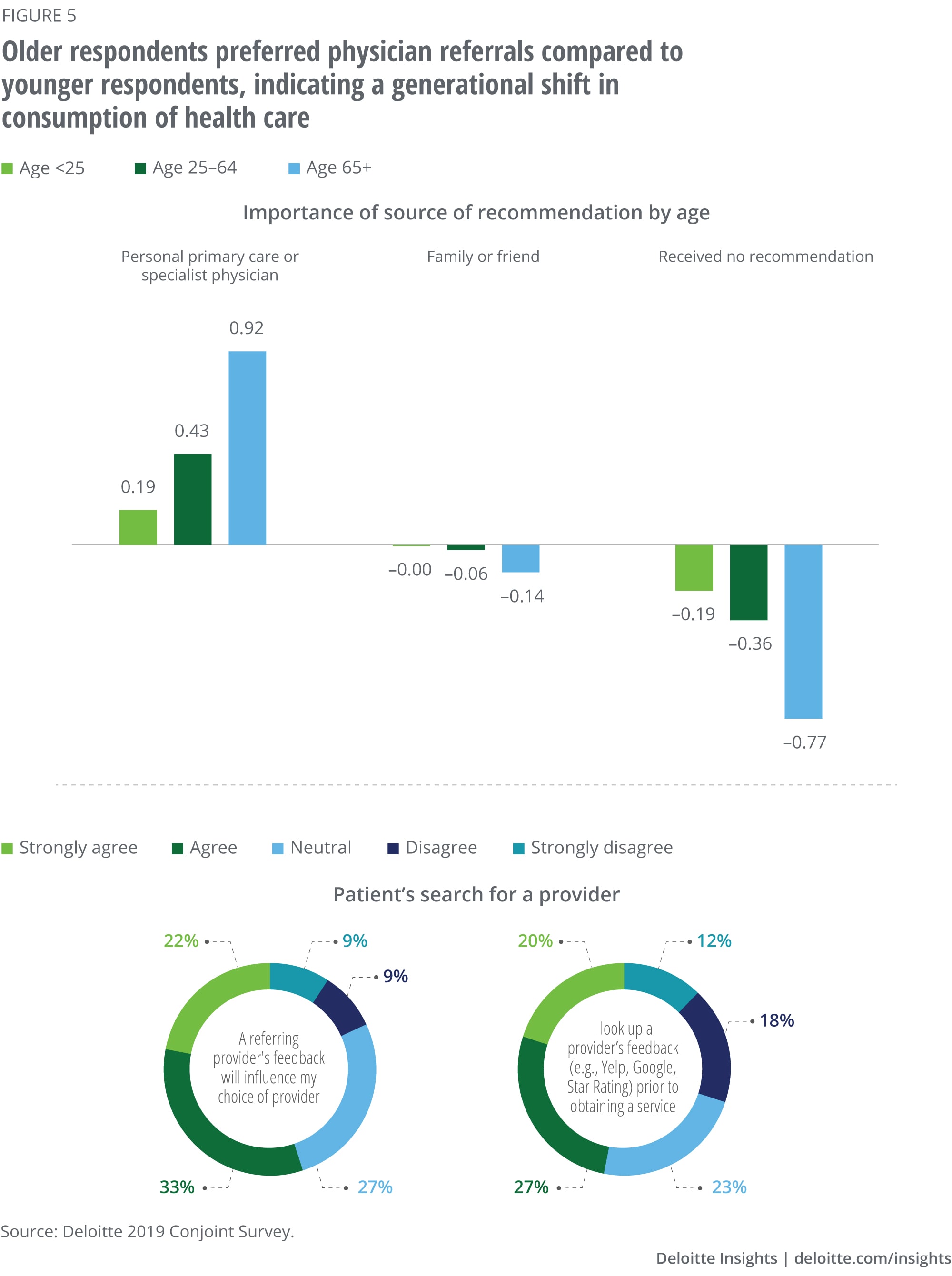

There may be a generational difference in how individuals consume health care

Our survey results showed a clear distinction in how older versus younger individuals responded to survey questions. Older populations (55+) preferred provider profiles that included a referral from their primary care physician (PCP) rather than those without, regardless of the availability of an OOP estimate. Younger populations (18–24), however, favored a provider that gave an OOP estimate either through an advance call or at the time of service over health care providers recommended through their PCP. This survey result is reflective of how many millennials are consuming health care. They typically prefer quicker, efficient services and transparent information rather than a long-term, trusted relationship with their PCP. A Kaiser Foundation poll found that 45% of 18- to 29-year-olds did not have a PCP compared to only 12% of 65+ year-olds.15 Younger individuals also often prefer “alternative” health care delivery options, such as virtual telemedicine and urgent care with weekend and evening hours. This difference is bound to become more prominent due to the spread of COVID-19 as virtual health care options become front and center. This change in health care consumption across generations provides an opportunity to shape the pricing strategy.

Conclusion

Maria’s experience is just one example of how consumers today are looking for greater control over their health care experience. The demand for transparency has been further accelerated by the coronavirus crisis. In April 2020, in the midst of the pandemic in the United States, Deloitte surveyed 1,159 health care consumers. Seventy-seven percent reported feeling uncertainty or a lack of control regarding their health care; and yet, 46% of consumers with health insurance said they now have a better understanding of their health insurance benefits since the pandemic began.16

The drastic shifts COVID-19 has made to our collective reality coupled with consumer-centric sentiments and regulations present providers with an opportunity for introspection and reevaluation of patient engagement strategies. Our analysis demonstrated that OOP costs were the most important decision-making factor of the five attributes tested and suggests that OOP cost information combined with other meaningful quality data can directly influence patient satisfaction and decision-making and minimize care delays due to cost concerns. Providers that prioritize authentic information transparency stand to benefit from the shift to consumer-focused health care, particularly as online shopping for health care transitions from being the exception to the rule. To lead in this new paradigm, providers must rebuild trust in the health care system as a whole by engaging patients in an authentically transparent dialogue around their health care liability and the true cost of care.

Deloitte Consulting Health Care Pricing Practice

Deloitte Consulting LLP’s Health Care Pricing Practice leads our provider, physician practice, and planclients through a full suite of pricing services with a goal of improving the affordability of health carethrough information transparency and data-driven decision-making. As a core part of our end-to-endRevenue Cycle solution, our work includes traditional strategic pricing solutions, managed carecontracting analytics, chargemaster standardization, and full pricing transformations.

Learn more

Get in touch

- Christi Skalka

- National Provider Pricing lead

- Managing director | Deloitte Consulting LLP

- cskalka@deloitte.com

- +1 512 689 0167

© 2021. See Terms of Use for more information.

Related content

More on health care

-

-

Clinical leaders' top concerns about re-opening Article4 years ago

Clinical leaders' top concerns about re-opening Article4 years ago -

The future of virtual health Article4 years ago

The future of virtual health Article4 years ago -

Medicaid in 2040 Article5 years ago

Medicaid in 2040 Article5 years ago -

-

Health care Collection

Health care Collection