Restructuring the supply base: Prioritizing a resilient, yet efficient supply chain

Resilience in supply chains held the spotlight for many years; however, the focus appears to be shifting back to efficiency as companies consider costs and margin pressures

Jim Kilpatrick

Lindsey Berckman

Alan D. Faver

Kate Hardin

Matt Sloane

Optimizing the balance between performance and cost

In the last four years, global industrial manufacturing and construction supply chains have experienced significant disruptions while being exposed to limited supplier options and intensifying competition. For many industrial manufacturers, the response of the supply network to the COVID-19 pandemic, geopolitical challenges, and natural disasters thrust supply chain resilience into the limelight. But the pendulum appears to be swinging back, with costs and margin pressures once again at the forefront as companies reevaluate their supply chains.

As of early 2024, supply chain pressures have fallen from the unprecedented levels following the COVID-19 pandemic.1 The National Association of Manufacturers (NAM) Manufacturers’ Outlook Survey for fourth quarter of 2023 revealed that, in the last two years, 86.2% of respondents have worked to de-risk their supply chains.2 Many companies are now prioritizing a resilient yet efficient supply chain. They are working to optimize the balance between performance and cost by restructuring their supply chain. These approaches include expanding to locations in the United States, or to locations closer to end consumers, and also working more closely with free trade partners of the United States.

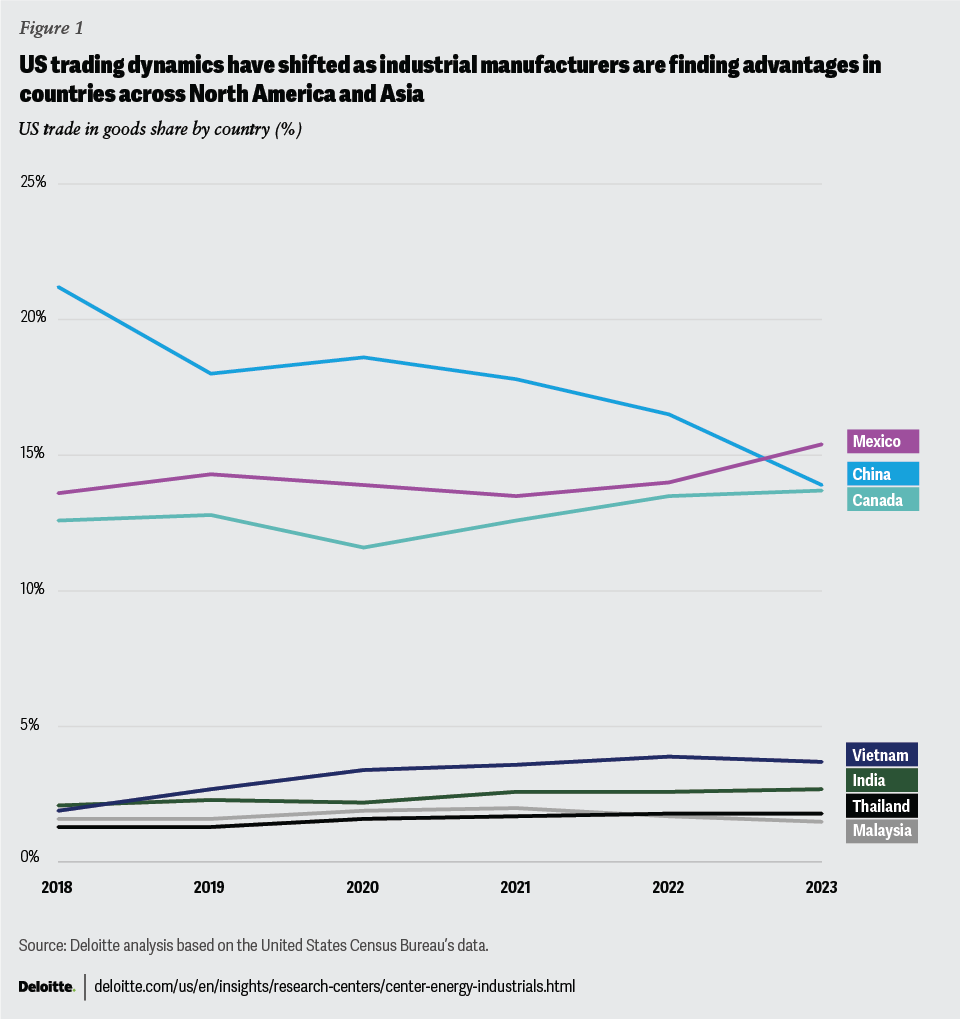

Industrial manufacturers are finding advantages in countries across North America and Asia. They are exploring both “nearshoring” options in Canada and Mexico and “reshoring” options in the United States. The share of US trade in goods with China has declined from 21.2% in 2018 to 13.9% in 2023. While Mexico has overtaken China to become the lead US trading partner, accounting for a 15.4% share (figure 1), Mexican trade with China has simultaneously increased.3 Now, manufacturers are likely exploring ways to ensure that their Tier 2 and Tier 3 supply networks are sufficiently networked to reduce their raw material and key component exposure.

Other nearshoring options such as Canada, as well as potential Asian trading partners like India, Malaysia, Thailand, and Vietnam, have experienced growth. This restructuring is occurring globally and is not exclusive to the United States, nor is it a North American phenomenon. In fact, at the end of 2023, 97% of companies surveyed in the Economist Impact’s “Trade in Transition 2024” project stated they were reconfiguring their supply chains in some way, as compared to 92% in 2022.4

These changes beg the questions: What are industrial manufacturing and construction companies considering with respect to performance and cost as they restructure their supply chains? And how are they doing the restructuring?

Supply chain efficiency is motivating industrial manufacturers to restructure their supply base

As global supply chains have normalized following the pandemic, chief executive officers are likely beginning to shift their strategic focus toward profitable growth.5 Part of the strategy for many, for maintaining healthy margins, is rooted in reducing company exposure to supply chain disruption while employing cost reduction techniques and capitalizing on government policies supporting domestic growth.

Geopolitical instability and disruptions keep the focus on delivery and lead times

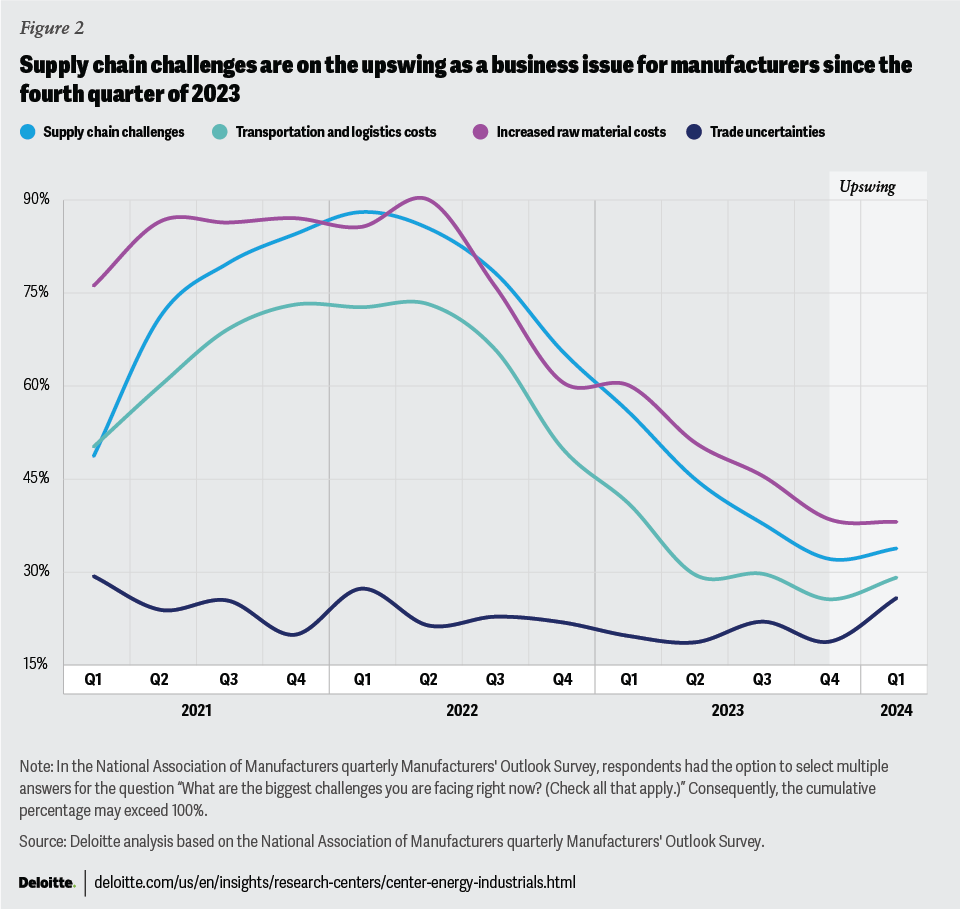

As CEOs look to keep their company exposure low, their concerns over the indirect impacts of geopolitical instabilities on supply chains have grown.6 And, after a period of decline, the end of 2023 and the first quarter of 2024 saw an uptick in supply chain challenges as a primary business issue for manufacturers (figure 2).7 This, in turn, has led to increased transit times worldwide.

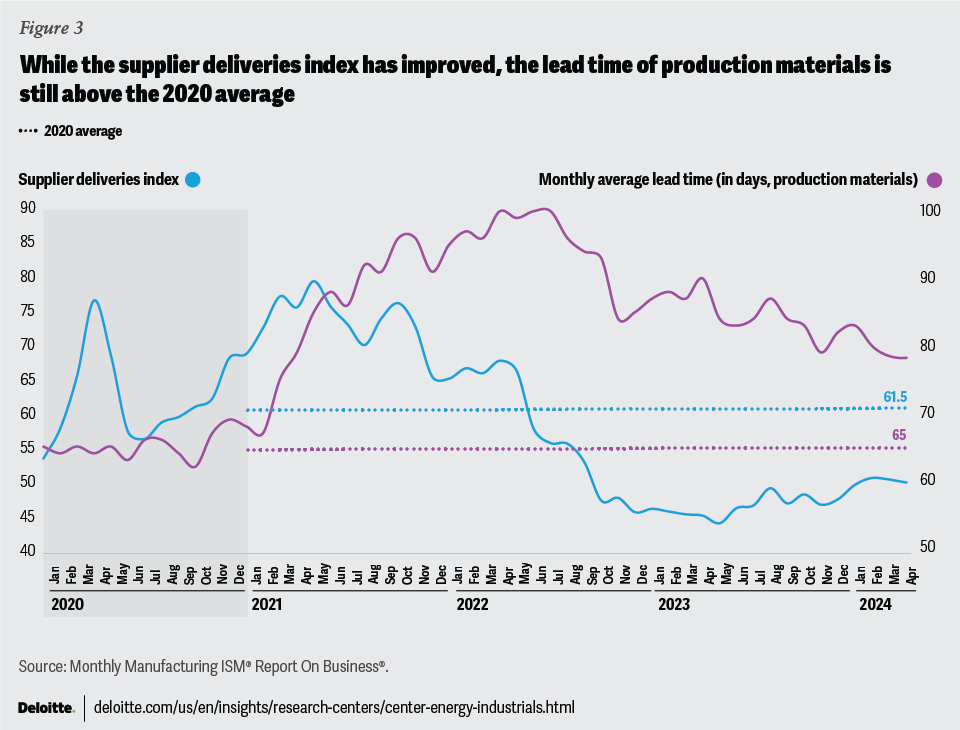

Industry leaders expect that global shipping may experience up to 20-day delays in deliveries in the coming months.8 Deloitte’s US economic forecast for the first quarter of 2024 suggests that the situation in the Red Sea may persist,9 potentially upending the progress made in lead times since 2022. In particular, the average lead time of production materials in April 2024 was 79 days. While this is a 21% reduction from the peak of 100 days reached in July 2022, it is still higher than 2019 levels, which averaged around 65 days (figure 3).10

Longer lead times can threaten manufacturing processes, and ultimately business continuity, for companies across the value chain. In the face of recent disruptions, the Manufacturing Supplier Deliveries Index rose to 48.9 in April 2024 from 47 in December 2023.11 The increase in the index signals a slowdown in the delivery performance of suppliers to manufacturing organizations, largely due to raw material supply chains.12 While delivery performance showed a trend of significant improvement with average delivery decreases of 72.8 in 2021 to 57.3 in 2022 and 46 in 2023, it increased in the first quarter of 2024 to 49.7.13 This increase will likely motivate companies to maintain focus on resilience.

Supply chain strategies to account for rising costs

To help reduce exposure to global disruptions and both maintain and boost margins, some manufacturers are looking to be strategic in their supply base restructuring by identifying and targeting specific components of a broader cost equation. Leading companies are exploring ways in which they can balance workforce requirements with labor costs and delivery times with shipping costs, all while ensuring the highest product quality.

Companies are still likely to heavily lean into labor costs as their main motivation for cost-based restructuring. This, of course, is not a new trend. In 1982, on average, US multinationals had 30% of their workforce abroad. Over the last several decades, companies have generally seen this percentage increase.14

In 2003, a Chinese employee in manufacturing made approximately 3% of their American counterpart while a Mexican employee made approximately 11%.15 As time progressed, Chinese manufacturing expertise increased and so too did accompanying wage rates. Between 2022 and 2023, a wage rate comparison reveals that a Chinese manufacturing worker makes the equivalent of approximately 26% of their American counterpart, while a Mexican worker makes approximately 14%.16 Today, workers in Malaysia and Thailand make approximately 1% and 15% of US hourly wages, respectively, and workers in India earn approximately 4-5% of US hourly wages.17

The inputs to the labor equation for companies have changed and so too have their supply chain practices. For instance, Mexico is currently proving to be a viable competitor to China as costs and trade policies are driving a growth of nearshoring for automotive and electronics manufacturers.18

Some companies are taking a methodical approach to capitalizing on labor cost advantages by gradually restructuring their bases. In such a scenario, these companies can achieve labor cost efficiencies while adding resilience to their supply base through expansion.

Many of the current cost-motivating factors are interesting from a labor arbitrage perspective. As the modern world of smart factories grows and expands, the role of labor costs will likely diminish as the entire cost equation changes. As organizations continue to incorporate automation and leverage sustainable technologies, they are likely to begin reconsidering the motivating factors for supply chain restructuring.

Finally, the most recent supply chain disruptions have spotlighted the costs associated with shipping and logistics. As of February 1, 2024, the rate for shipping from China to the East Coast of the United States was US$6,589 forty-foot equivalent unit, a 193% rate increase since October 2023.19 Additionally, these disruptions are likely to have ripple effects down the road. The NAM manufacturers’ outlook survey for the first quarter of 2024 indicated that raw material prices may increase by 2.38% over the next 12 months.20

The growing importance of industrial policy for profitable growth

Amid the exposure to increased delivery times, differing labor costs, and higher transportation costs, many companies are already shaping their restructuring approaches to take advantage of evolving industrial policy. Governments across the globe are actively adapting policy to favor domestic industrial activity and consequently incentivizing reshoring and nearshoring activities. These industrial policies are likely to continue to accelerate changes in supply chains21 and could play a major role in driving decisions regarding restructuring in the coming years.

Private fixed investment in manufacturing increased nearly 2.5 times in 2023 from 2021, to reach US$799.2 billion.22 As of September 2023, US$430 billion of this investment spike is attributed to several key pieces of US legislation—specifically, the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act, the Inflation Reduction Act (IRA), and the Infrastructure Investment and Jobs Act (IIJA).23

In January 2024, the US Department of Defense unveiled its National Defense Industrial Strategy. One priority of this strategy is the development of resilient supply chains enabling the nation to securely acquire products, services, and technologies for defense applications. Such government strategies can facilitate the restructuring of supply chains to meet both current and future needs at speed, scale, and cost.24

In fact, according to data from the Reshoring Initiative 1H 2023 Report, the top reason companies reshore or conduct foreign direct investment (FDI) is government incentives.25 From free trade agreements and tariffs to tax incentives and subsidies, the United States and a host of other countries are putting policy in place to entice companies and ensure the growth of domestic regional supply chains.

Free trade agreements may enable and encourage supply chain restructuring

Economic data indicates that free trade agreements, such as the United States-Mexico-Canada Agreement (USMCA, replacing the North American Free Trade Agreement), are likely driving greater regionalization of supply chains as there are increased incentives for sourcing goods and materials in North America.

Since USMCA’s origination in 2020, FDI into North America has grown 134% to approximately US$219 billion.26 FDI in Mexico landed at nearly US$19 billion in the first quarter of 2023, a 48% year-over-year increase.27 Of this investment, 53% was in the manufacturing sector (compared to 24% in the first quarter of 2022),28 which emerged as one of the top two industries for direct investment in both the United States and USMCA.29 Nearly half of the total FDI was led by North American companies from automotive, aerospace, electronics, and telecommunications.30

Inclusive of Mexico and Canada, the United States has free trade agreements with a total of 20 countries.31 These agreements are intended to provide opportunities for global industrial manufacturing and construction companies to benefit from reduced tariffs on an array of goods and strengthen supply chains on the most critical items.32

For example, with the US-Japan Trade Agreement and the more recent agreement on strengthening critical mineral supply chains, the United States is encouraging companies to restructure their supply bases into Japan. These agreements provide companies access to more favorable tariffs for industrial goods such as machine tools and steam turbines and better access to tax incentives for mineral-based technologies.33

Finally, governments may use tariffs as a lever to help encourage diversification away from certain markets, thereby driving restructuring activity. In combination with free trade agreements like the USMCA, these tariffs have likely led to global supply chain restructuring and new trade activity. Three years following the enactment of the USMCA, the total value of North American trade in 2023 had grown by nearly US$500 billion.34 At that point, North American trade exceeded US$1.57 trillion, placing Mexico and Canada as the top trade partners with the United States.35

Government incentives and investment opportunities for advanced technology supply chains

The US government is incentivizing businesses across the industrial manufacturing and construction sector to reshore their most advanced operations with a number of tax and investment opportunities. Many of these incentives fall under bolstering critical minerals, green energy technologies, and advanced manufacturing.

The IRA, a US$370 billion investment program, demonstrates the US government’s commitment to domestically advance clean technology manufacturing, ranging from clean energy and clean vehicles to sustainable construction materials and advanced manufacturing.36 This includes US$2.1 billion for the US General Services Administration to use materials and products with low embodied carbon37 and an advanced manufacturing tax credit to incentivize domestic production of solar and wind energy components, qualified battery components, and up to 50 critical minerals.38

The IRA opportunities range from direct funding to tax credits. These opportunities are attracting new investments in the United States. For example, in February 2023, Holcim Limited, used a US$1.29 billion purchase of a US roofing system company to expand its presence the United States.39

Separately, with the passage of the CHIPS and Science Act, the US government committed US$52.7 billion of investments into domestic chip production and advanced semiconductor research and development.40 The legislation further incentivizes a push for companies in advanced manufacturing for semiconductor technology through a 25% tax credit on eligible capital investments.41

The impact in developing a domestic semiconductor supply chain was immediate as a number of chipmakers, including foreign companies, are building fabrication facilities. Leveraging incentives from the CHIPS Act, America’s Intel Corporation announced plans to spend US$20 billion to build two fabrication plants in Ohio.42 Additionally, a Taiwanese chipmaker is building two fabrication plants in the United States43 in a move that not only enables greater access to customers but can also help de-risk supply chain operations.

Beyond the United States, both Japan and India are using their own governments’ subsidies to incentivize regional production of semiconductors. And much like in the United States, these incentives are resulting in investments.

In Japan, a major chipmaker is using significant subsidies from the Japanese government to help build two semiconductor fabrication plants.44 Further, a Taiwan-based foundry, in collaboration with a leading precision and electronics manufacturer from India, is utilizing Indian subsidies of approximately US$15 billion to expand its semiconductor fabrication. This expansion aims to satisfy local demand in India and build supply chain resilience for global end users.45

Companies deploy differentiated strategies to help achieve supply performance

Many global industrial manufacturing and construction companies spent years employing resilience strategies like overbuying to help reduce production delays, often to the detriment of margins. Now they are employing everything from traditional strategies to advanced technologies in a quest to realize value in their supply chains.

While many of these strategies are not new, recent external supply chain risks have made them a primary focus for industrial manufacturing and construction companies. These strategies can help ensure business continuity by reducing bottlenecks, balancing cost opportunities with innovation potential, and allowing access to the most favorable regulatory environments.

Techniques to diversify sources and reduce concentration issue

Industrial manufacturing companies are using dual sourcing, or “supplier + 1,” to reduce their supply chain reliance on a single supplier or country. This is achieved by incorporating an additional supplier from the same or a different location to satisfy a portion of the supply requirement. According to a Gartner supply chain survey, 57% of industrial manufacturers with operations in China are considering the “supplier + 1” strategy.46

In some instances, companies are working to achieve extensive risk mitigation and diversification by employing a multi-sourcing strategy, where they employ three or more suppliers to satisfy a supply requirement. (To see how multi-sourcing is helping shape the advanced air mobility industry, see sidebar, “Emerging industries have an opportunity to build resilient supply chains from scratch.”)

Emerging industries have an opportunity to build resilient supply chains from scratch

Evolving industries like advanced air mobility have an opportunity to both develop and shape resilient, robust, and efficient supply chains of the future. Learning from electric vehicle industry experiences, Lilium, an electric vertical takeoff and landing (eVTOL) manufacturer, is mitigating risks associated with battery production by adopting a multi-sourcing strategy.47

Further, Archer, another eVTOL manufacturer, has signed a Space Act Agreement with NASA to study high-performance battery cells for advanced air mobility and space applications. Archer anticipates that this study will drive progress in the evolving supply chain for electric aircraft.48

To mitigate the risks associated with quality and lead time, industrial manufacturing companies are gradually building capacity at new supplier locations while reducing capacity from an existing supplier. These approaches can help address business continuity challenges during uncertain times and diversify away from existing dependencies. Such measures can also enhance the overall capabilities of the particular destination country, setting the stage for future operations opportunities. Additionally, these strategies may provide companies greater access to end users or governmental incentives.

A trifecta of restructuring options

In addition to expanding their supply bases through dual-or multi-sourcing strategies, industrial manufacturing companies are employing mergers and acquisitions (M&A), strategic partnerships, and new supplier investment agreements, and expanded internal capabilities to restructure and build resilience into their supply chains.

M&A strategies can expand supply access and control

Horizontal integration, by merging or acquiring other companies, can help companies expand their supply base as well as their customer base, while gaining access to new markets, increasing their market share, and potentially benefiting from economies of scale.

Vertical integration can be useful when manufacturers seek greater control of certain stages of the supply chain, from sourcing raw materials to delivering the final product or after-sales services. For instance, at the end of 2022, First Aviation Services Inc. acquired Associated Aircraft Manufacturing & Sales, Inc. (AAMSI). This move provided First Aviation the ability to access and integrate AAMSI’s machining and electronics manufacturing operations into its supply chain.49 In the global market, AERO Vodochody AEROSPACE a.s. has bought one of the major suppliers of its new L-39NG aircraft, Technometra Český Brod a.s.50

Achieving efficiency through partnerships and new supplier agreements

As M&A is typically capital intensive, some companies are exploring strategic partnerships and supplier investments to expand their supply bases. Strategic partnerships with new suppliers can facilitate shared strengths, mitigate risks, and are often accompanied by cost reductions and increased innovation. To ensure supply chain resilience, manufacturers may further invest in the growth and development of their suppliers. This investment can be in the form of technology transfers or financial investments.

New supplier investment agreements can mitigate risks with existing suppliers by enhancing internal capabilities and flexibility. These agreements can enable companies to address material flow and business continuity more readily. (For considerations in the construction industry, see sidebar, “The construction industry may be able to emphasize collaboration and digital technologies to address supply chain issues.”)

The construction industry may be able to emphasize collaboration and digital technologies to address supply chain issues

Construction input prices increased by 1.4% in February 2024, 0.4% in March 2024, and 0.5% in April 2024, with overall construction costs remaining approximately 2.3% higher than the previous year, primarily due to persistent inflation, energy costs, and escalating supply chain issues. Further, as of April 2024, the prices of crude petroleum, unprocessed energy materials, iron and steel, fabricated structural metal products, and steel mill products have surged by more than 50% compared to February 2020.51

Moving forward, construction companies can collaborate closely with suppliers to understand risks well in advance, seek alternative sourcing options, and implement digital technologies. In the short term, some construction companies (particularly global companies) are considering local vendors for sourcing options. Additionally, while typically project-specific and not a historical trend, construction firms may purchase supplies across projects to unlock more competitive pricing by sourcing common materials from a smaller, consolidated supply base.

Implementing digital supply chain technologies can allow construction companies to connect with suppliers in real time and can provide greater visibility and control over the supply chain by streamlining internal processes and improving overall efficiency. These proactive approaches can potentially address downtime during disruptions and manage lead time, finances, and customer confidence.

Companies are expanding their internal capabilities to work to meet potential demand

Finally, industrial manufacturing companies are, in a sense, expanding their supply base by making substantial investments in their own capabilities. On the one hand, companies are adding new manufacturing sites or capacity to meet potential demand. On the other, they are enhancing their product capabilities and demand responsiveness by investing in new equipment and technologies, including advanced machinery such as 3D printers and specialized machines.

Enhancing product capabilities goes beyond hardware as companies are introducing an array of software solutions. Industrial manufacturers are using technologies and digital solutions to enhance operational and supply chain resilience and increase visibility across the value chain.

Manufacturers are building digital twins of the supply chain for essential components, which can assist in identifying alternative suppliers or boosting robustness and agility to reduce dependency. As supply chains restructure, manufacturers are likely to find digitalization critical to help ensure visibility throughout supplier tiers. Deloitte’s 2023 “Exploring the industrial metaverse” revealed that 21% of those companies surveyed are incorporating metaverse technologies to improve their supply chain ecosystems.52

Diving into specific technological applications, a study conducted by Augury revealed that supply chain management and optimization is the top use case for artificial intelligence, as reported by 41% of surveyed respondents.53 Further, the 2024 Material Handling Industry Annual Industry Report showed that respondents identified logistics, shipping and transportation, supplier selection and due diligence, and inventory management as the top three applications of AI.54

The modernization of existing facilities, incorporation of advanced technologies (both hardware and software), and support for suppliers to meet current demand are strategic moves that can help strengthen the supply chain for manufacturers and suppliers. (For thoughts on the aerospace and defense industry, see sidebar, “The aerospace and defense industry may further embrace agile supply chains digital technologies to meet projected demand increase.”)

The aerospace and defense industry may further embrace agile supply chains digital technologies to meet projected demand increase

The aerospace industry faced significant challenges in meeting post-pandemic demand due to supply chain disruptions. Suppliers may need to be more agile moving forward to capture demand and may consider investing in emerging technologies and smart factory solutions to address supply chain challenges and optimize production capacity.

Investing in digital technologies can also provide greater supply chain visibility, foster innovation, and strengthen stakeholder relationships. These investments could improve efficiency and competitiveness, ultimately leading to cost and operational benefits.

The next phase of supply chains: Maximizing resilience while maintaining margins

The restructuring of the industrial manufacturing supply base reflects the sector’s resilience and adaptability, particularly in the face of external uncertainties. Companies across the sector are continuously seeking opportunities to maximize resilience while keeping margins high. They are finding motivations for restructuring through delivery performance, cost reductions, and government incentives, all aimed at profitable growth.

As technology continues to advance, industrial manufacturing and construction companies are maintaining one eye on the future while working to ensure their supply systems of the past. Many new government policies are incentivizing advanced technology or products for future demand. However, these companies should maintain their procurement processes for legacy items. To do this, industrial manufacturing and construction companies are leveraging a multitude of strategies, ranging from diversifying their suppliers and seeking new agreements to bringing capabilities in-house and implementing digital technologies, all in an effort to help create resilient and efficient supply chains.

{kind=link}

{kind=link}

{kind=link}

{kind=link}