2025 Chemical Industry Outlook

In 2025, the chemical industry is expected to focus on innovation, sustainability, and resiliency to drive efficiency and growth

David Yankovitz

Kate Hardin

Robert Kumpf

Ashlee Christian

The chemical industry has made moderate progress in 2024, increasing year-over-year production above 2023 levels, and it is estimated that production levels will continue to rise as the destocking cycle wanes and demand rises across most products.1 However, to further support revenue growth, chemical companies have announced cost-reduction plans and begun to increase margins, while continuing to invest in decarbonization and innovation.2 In 2025, we expect the industry to continue its recovery, adjusting to new market drivers while balancing short- and long-term goals.

Since the COVID-19 pandemic began in 2020, the chemical industry has had to navigate turbulent market conditions. The pandemic led to weak demand, reduced production, and lower revenues in 2020. This was followed by a strong rebound in chemical production and revenues from 2021 to 2022, as demand rose, and fear of supply chain issues led to higher levels of inventory stocking. But by late 2022, supply chain issues began to wane, key end markets began destocking, and demand for chemicals declined. By the end of 2023, revenues decreased 8% year on year, operating margins fell to their lowest level since the Great Recession (2007 to 2009), and returns on capital dropped back to pre-pandemic levels.3 These dynamics highlighted a need for greater resilience spurring cost reduction programs. While these cost-reduction programs are still rolling out, margins began to rise in the first half of 2024 (figure 1).4

Table of contents

Looking ahead, moderate growth is expected to continue in the chemical industry in 2025. The American Chemistry Council (ACC) projects global chemical production to rise by 3.4% in 2024 and 3.5% in 2025, after increasing just 0.3% in 2023.5 However, even with chemical production improving and margins reverting to average levels, the industry still faces challenges and uncertainty. In the next year, chemical companies will navigate many of the same challenges as other industries: evolving macroeconomic conditions, shifts in policy and regulations across regions, changing customer preferences, and advances in technology. To help improve their positions in the face of these uncertainties, chemical companies could consider adopting strategies that help them weather uncertainty while positioning themselves competitively in the low-carbon, high-tech future.

To plan for the future, companies should consider developing an understanding of where they stand in the current scenario. This can provide them with a foundation for examining the emerging trends that may shape the industry’s trajectory in the coming years. Our 2025 Chemical Industry Outlook explores some of these trends and highlights the signposts leaders should consider while developing strategies.

- Cost efficiency: Improving operational efficiency through cost-reduction programs and asset rationalization

- End markets: Navigating uneven growth by focusing on high-growth areas and customer needs

- Innovation: Enhancing performance and sustainability through a multidimensional approach

- Sustainability: Accelerating decarbonization through enhanced clean-energy access, policy levers, and ecosystem value capture

- Supply chain: Building value chain resilience to navigate evolving regional dynamics

What our ‘multiverse’ analysis can tell chemical companies about their current position

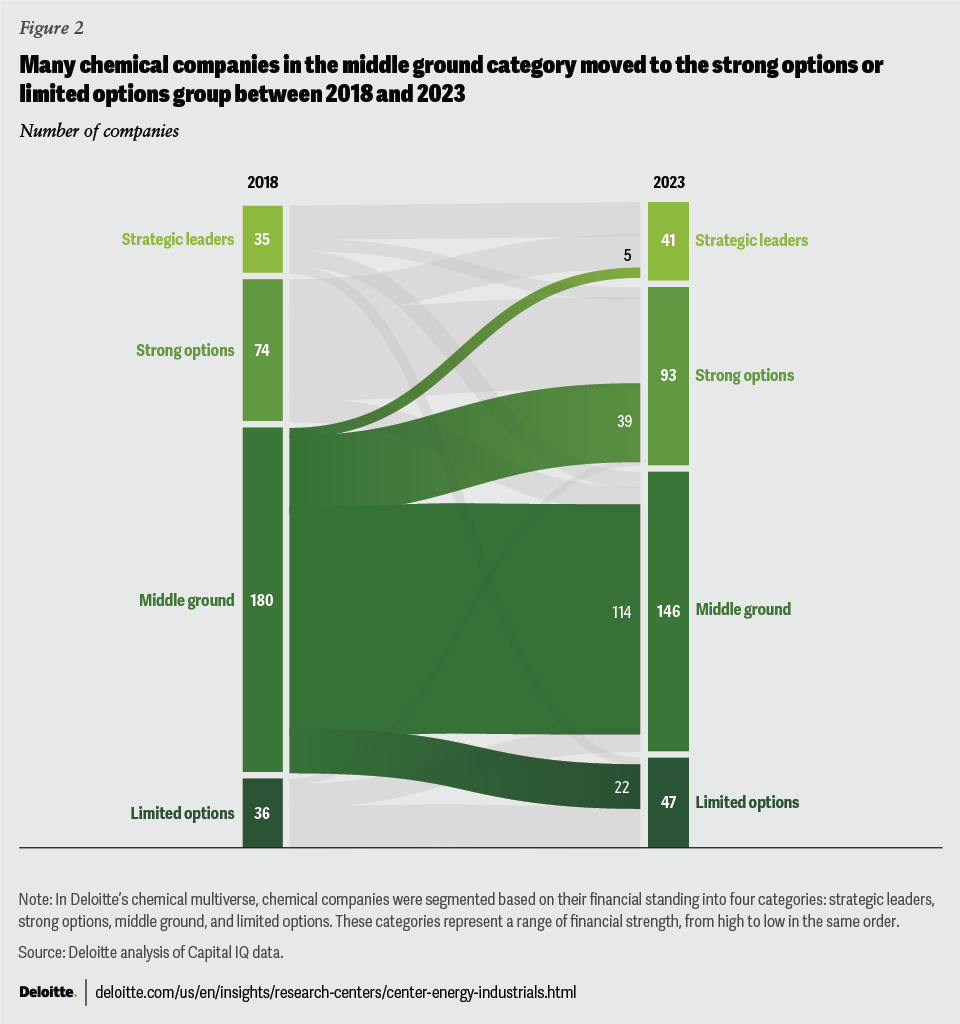

This year, Deloitte updated its chemical multiverse analysis with data through 2023 to take a closer look at how the track record of global chemical companies through recent turbulence may shape trends in 2025 and beyond (see “Methodology” below for more information on this tool). This longitudinal study tracks multiple financial variables across more than 300 global chemical companies over the past 25 years and, through a segmentation approach, assesses the current standing of each company. The chemical companies were measured on two dimensions—the financial resources at their disposal and their ability to generate returns using those financial resources—and plotted on a two-dimensional plane. Plotting the chemical companies on this plane can provide insight into their competitive positioning and could help them decide on a future course of action.

This analysis gave rise to four distinct strategic groups, which we termed: strategic leaders, strong options, middle ground, and limited options. Each group has its own unique characteristics, but overall, strategic leaders exhibit the highest financial strength, while strong options demonstrate relatively higher business performance compared to middle ground and limited options.

Due in part to the turbulence spurred by pandemic-related shutdowns, the number of companies in the middle ground group has declined, with more companies moving into stronger (“strong options”) or weaker (“limited options”) positions in terms of business performance (figure 2). Additionally, the following two notable observations also emerged from this analysis.

- Between 2018 and 2023, cash and securities rose across every group, even as earnings before interest, tax, depreciation, and amortization (EBITDA) fell for nearly every group. In fact, cash and securities rose 27% for multiverse companies, while EBITDA rose just 2.6% over the same period. It appears that all groups are focusing on holding liquidity to weather economic uncertainty and increase flexibility for future investments.6

- Companies in the strong-options group increased their investments in research and development and their net fixed assets more than any other group.7

In addition to the segmentation based on financial positioning, Deloitte’s chemical multiverse also categorized chemical companies based on their business model, rather than the traditional categorization based on product type. This categorization aims to better explain the strategic responses of different companies to long-term developments. Based on this approach, three categories of chemical companies emerged, which we called natural owners, differentiated commodities, and solutions providers. The strategic imperative of a company will differ based on the category it belongs to. Natural owners are companies that have access to or ownership of a strong advantaged feedstock position with a laser-sharp focus on achieving lower operational costs. Differentiated commodities often serve cyclical industries (for example, construction and automobile) and focus on enhancing capital efficiency and technology leadership. Solutions providers primarily focus on selling solutions involving systems-level design and engineering.

1. Cost efficiency: Improving operational efficiency through cost-reduction programs and asset rationalization

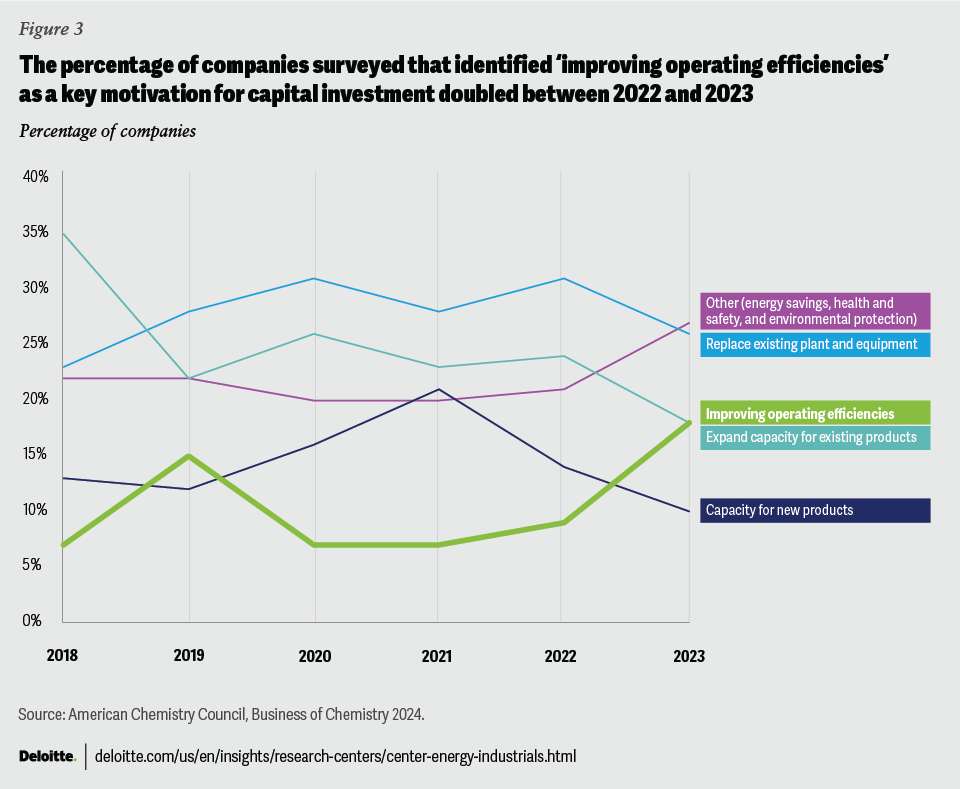

Many companies announced cost-reduction programs in 2023 and 2024, after facing challenges with higher operating costs and lower operating rates stemming from lower demand, high inventories, and overcapacity of some chemicals.8 These programs included measures for increasing efficiency in plant and back-office operations, redesigning processes, aligning spending levels with the macroeconomy, and undertaking workforce reductions and plant closures.9 In fact, in an ACC survey of its members, more than 18% of respondents said that the motivation behind their capital investments in 2023 was geared toward operating efficiencies (figure 3).10 Another 26% of respondents cited replacing existing plant and equipment as a key motivation, likely indicating that some companies took advantage of the low operating rates to conduct maintenance and upgrades.11 While many of these programs began in 2023, several announced that rollouts will continue through 2025 or 2026.12

There is a regional component to how much pressure these assets are under. Plants in Europe have encountered challenges with inflation and high energy prices in 2022 and 2023, reducing demand and putting pressure on chemical margins. In the European Union, inflation reached a high of 11.5% in October 2022, compared to the US peak of 10.1% in June 2022.13 And with most Europe-based chemical plants facing natural gas prices 70% higher than pre-crisis levels, the region continues to be cost-disadvantaged.14 Further, many of these companies also faced losses due to lower-than-expected demand from China.15 Asian companies were similarly affected by lower demand from China and volatile LNG prices.16 Moreover, while the industry fared better in the United States and Middle East where energy and feedstock prices are relatively lower, US-based companies still faced lower earnings, which they likely compensated with efforts toward efficiency.17

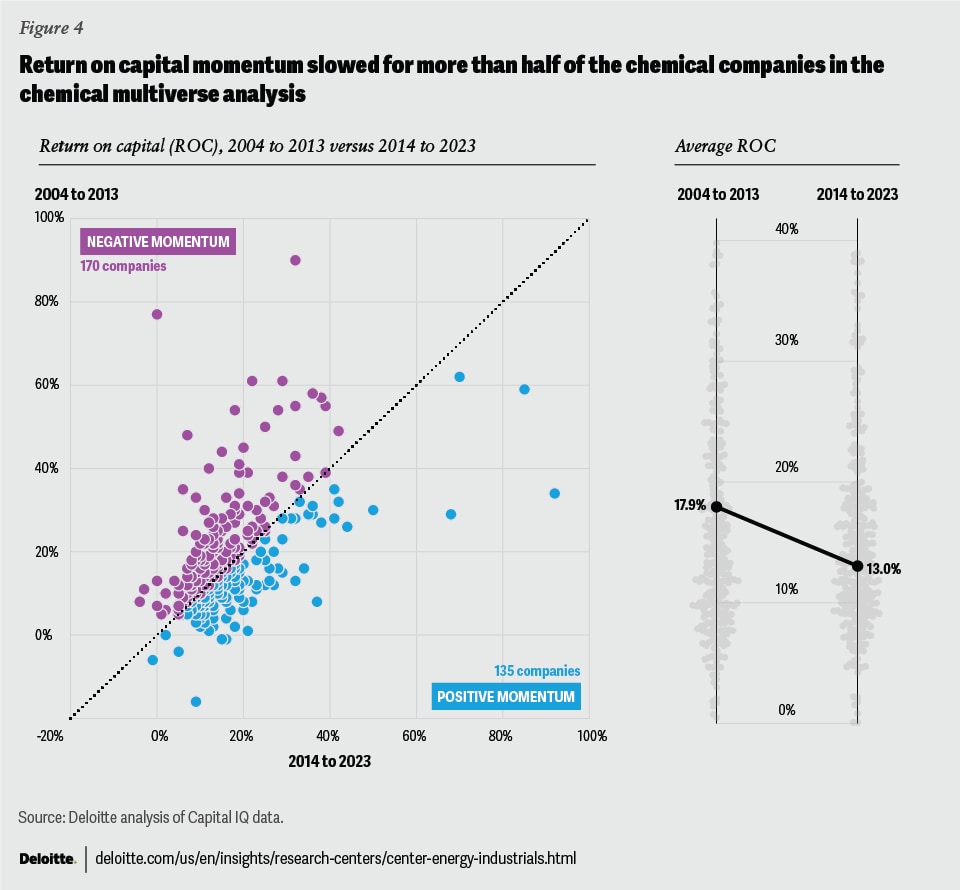

In the petrochemical sector, excess production capacity, in combination with lower-than-expected demand, has contributed to low operating rates. In Europe, ethylene operating rates were still averaging at 70% to 75% in early 2024, lower than the industry expectation of 80% to 90%.18 This overcapacity has contributed to the industry’s return on capital falling from an average of 17.9% between 2004 and 2013 to just 13% between 2014 and 2023 (figure 4).19 Partly, as a result of this, chemical companies began asset rationalization in 2023, which continued through 2024, with several companies announcing plant closures or job cuts across the Netherlands, Germany, and France.20 The impact of these closures are expected to reverberate through trade flows, with exports from the United States or the Middle East likely serving increased European demand in the future.

Asset rationalization is expected to continue through 2025 as companies acknowledge that a large near-term rebound in demand is unlikely and take the opportunity to reconfigure toward more cost-competitive supply- and growth-oriented markets. For companies in the limited-options or middle-ground categories, these types of measures could support improved performance and a move into the strong options category. Additionally, following the last few years of limited transaction activity, more merger and acquisition deals are expected to be announced in 2025 as interest rates moderate and companies search for growth and continue to reexamine their portfolios.

2. End markets: Navigating uneven growth by focusing on high-growth areas and customer needs

Global chemical production is projected to grow 3.5% in 2025.21 However, demand has remained soft in some markets, so far in 2024. In the United States, overall industrial production rose just 0.2% in 2023 and is estimated to stay mostly flat in 2024 before it’s estimated to rise to 1.7% in 2025.22 Amid this uneven growth landscape across chemical end markets, many companies are focusing on driving efficiencies in their core business while doubling down in high-growth areas. Companies are also focusing their efforts on increasing customer centricity, building customer loyalty, and tailoring solutions for customers.

Capitalizing on high-growth areas

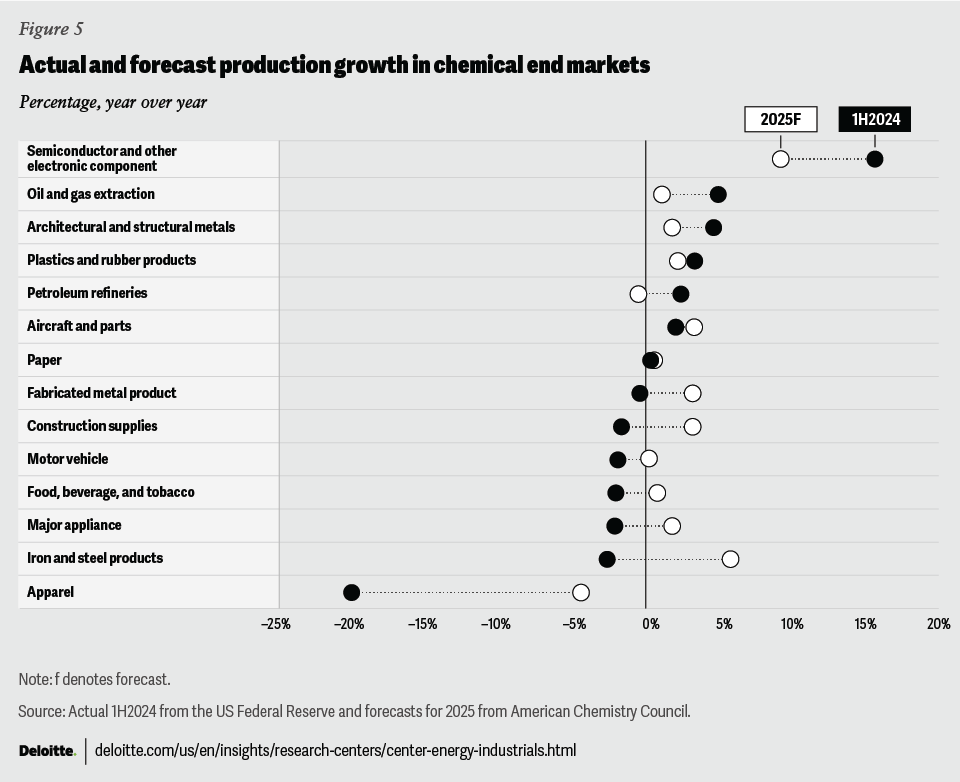

Chemical companies are investing in high-tech, clean energy—and other high-growth areas. So far in 2024, data from the Federal Reserve Board indicates that semiconductors and electronic components, oil and gas extraction, architectural and structural metals, and plastics and rubber industries have experienced the most growth.23 Moving into 2025, ACC forecasts that semiconductors will continue driving demand, followed by computers, iron and steel, aircraft and parts, motor vehicles and parts, and construction supplies (figure 5).24

- High-tech: Semiconductors have been the fastest-growing end market for the chemical industry, so far in 2024.25 They are an essential component of all electronic devices, including those used in communications, computing, health care, transportation, and clean energy. This growth is led by rising demand for automotive electronics as well as increased demand for data centers driven by the increased use of AI.26 In the United States, the CHIPS and Science Act, signed into law in August 2022, has spurred a number of chemical companies to invest in plants for the production of specialty gases or chemicals, that are used in the manufacturing of semiconductors.27 This is because many of these chemical companies were likely eligible for funding under the CHIPS and Science Act.28

- Clean energy: Chemical companies can play a significant role in the energy transition, as they supply materials for clean-energy solutions such as battery storage, clean hydrogen, and industrial coatings and lubricants for other technologies. The Inflation Reduction Act, signed into law in August 2022, has contributed to the construction of a number of new manufacturing plants.29 This is reflected in the increase in the production of architectural metals, which has grown 1.7% in 2024 and is expected to grow 3.2% in 2025.30 While some construction may have slowed due in part to high interest rates, the slowdown is expected to be short-lived, especially if interest rates are cut over the next couple of years. In addition, global sales of electric vehicles (EVs) are expected to increase over the next couple of years.31 EVs require 85% more chemistry (by value) than internal combustion engines and could play a role in additional demand for plastics, composites, and other chemicals.32

Prioritizing customer-centricity

As customer needs and preferences continue to evolve, chemical companies are often focused on strengthening customer relationships by adopting more customer-centric business models. With this focus and insight, companies may be better able to address customer needs through tailored solutions. For example, several chemical companies have an increased propensity to collaborate with customers to develop new products.33 Digital transformation is reshaping the way companies engage with their customers. Leveraging AI and data analytics can now enable personalized buying experiences and improve transparency throughout the supply chain. This can help chemical companies maintain competitive advantage and drive profitability.

While many chemical companies are expected to improve efficiency in their core businesses, expand into higher-growth markets, or implement customer-centric models, the strategies employed will differ depending on the company’s strategic imperative. Natural owners and differentiated commodities are more likely to announce cost-reduction programs, while solution providers are more likely to focus on customer co-innovation in high-growth areas.

3. Innovation: Enhancing performance and sustainability through a multidimensional approach

Chemical business leaders are at a juncture—one where innovation may be required to improve operational efficiencies and enhance product performance while meeting new sustainability goals. Consequently, despite revenues dropping 8% in 2023, capital expenditures and investments in R&D of the companies grew 6% and 2%, respectively (figure 6).34 These R&D efforts are being further amplified by digital technologies like AI and predictive analytics that can help accelerate breakthroughs. While capex growth is expected to slow to just 2.4% in 2024 due in part to high interest rates and market uncertainty, it is expected to rise to 3.5% in 2025 as companies continue to focus on cheap feedstock-advantaged projects in the United States, clean energy, and circular solutions.35

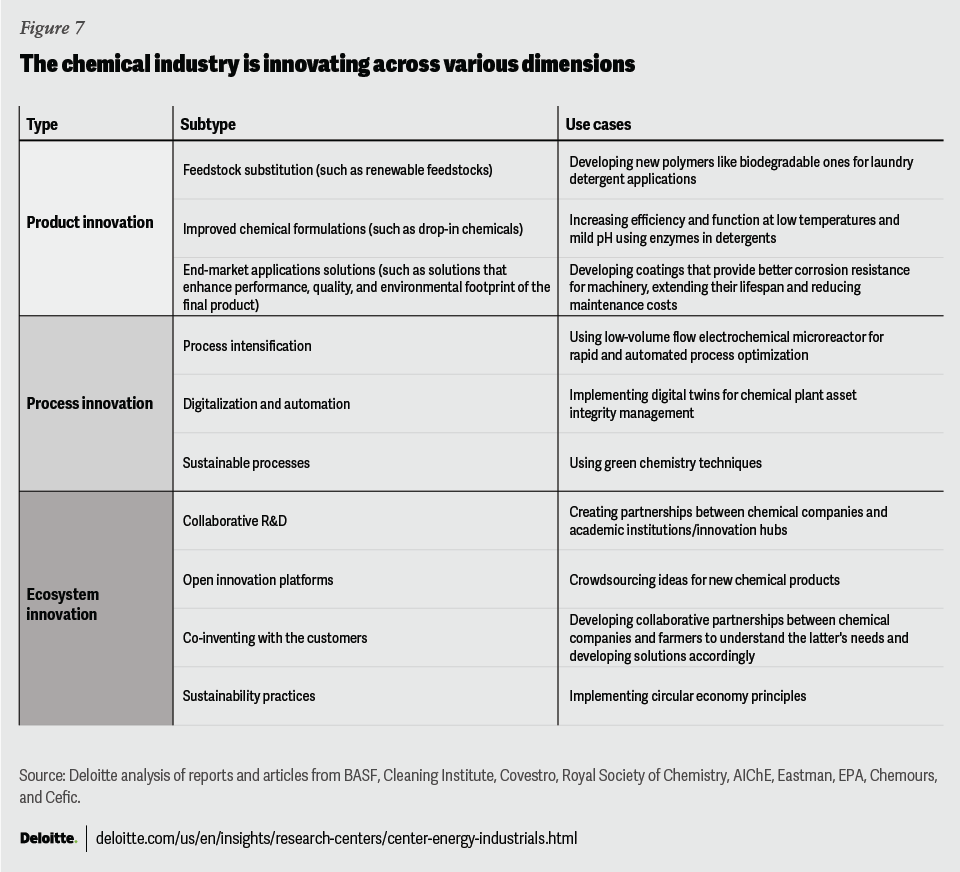

To stay competitive in a low-carbon economy and meet regulatory requirements and consumer demands, some chemical companies are prioritizing innovation across three key dimensions: product, process, and ecosystem (figure 736).

Product innovation

Chemical companies continue to increase product innovation as they work toward developing products that can enhance both performance and sustainability. Some of their key focuses for innovation include feedstock substitution, drop-in chemicals, additives, and end-market applications. For instance, Deloitte’s Future of Materials highlights that some companies are developing drop-in chemicals, where traditional chemical processes are modified to produce bio-based alternatives without significant changes to existing infrastructure. The drop-in chemicals can then be utilized downstream without making changes to their processes. For instance, bioethylene from the dehydration of ethanol from sugarcane can be integrated into existing polyethylene production lines, improving the product’s carbon footprint.37

Process innovation

Process innovation can be equally crucial, as it focuses on enhancing efficiency and sustainability through various methods, including process intensification, digital automation, and sustainable processes. Process intensification aims to make chemical processes more efficient and less resource intensive. A recent example is the use of digital automation to transform operations. Some companies are implementing AI-driven analytics to optimize production processes and minimize waste.38

Ecosystem innovation

Ecosystem innovation is reshaping how chemical companies collaborate and implement sustainable practices. It involves companies collaborating and coinventing with industry players, research institutions, and startups to develop new solutions. It also includes working with stakeholders across product value chains. For instance, the CIRCULAR initiative led by major chemical players focuses on developing circular economy practices, promoting recycling and reuse of materials.39 These are intended to not only enhance innovation but also position companies to meet regulatory requirements and consumer preferences for sustainable products.

For chemical companies to improve their competitive position, continued innovation will likely be critical in 2025. Historically, natural owners have utilized capex to increase process innovation, while solutions providers have engaged in R&D to shape product innovation. While these trends will likely continue, many differentiated commodity companies are beginning to employ both strategies. Similarly, companies across segmentations can invest in ecosystem innovation as strategic leaders with the financial resources available continue to invest in circular solutions such as advanced recycling and bio-based feedstocks.

4. Sustainability: Accelerating decarbonization through enhanced clean-energy access, policy levers, and ecosystem value capture

The chemical industry is involved in 96% of all manufactured goods.40 Consequently, reducing scope 1, 2, and 3 emissions of this industry likely impacts nearly all product value chains. The chemical industry’s greenhouse gas intensity dropped by 7.4% and its energy efficiency improved by 6.9% between 2018 and 2022.41 Over the same time period, the number of chemical companies reporting scope 1 and 2 emissions rose by 46%, encompassing more than 50% of the entire industry, and scope 3 emissions reporting rose by 83%, covering more than 30% of the entire industry (figure 8).42 The drive towards decarbonization may be influenced by several factors, with three key elements likely to be pivotal in 2025: availability of round-the-clock, cost-effective clean energy, policy changes, and capacity of chemical companies to harness value across ecosystems to bolster sustainable investments.

Access to low-carbon electricity

Despite the substantial growth of renewable energy in the global generation mix, some companies have cited limited access to renewable electricity as an impediment to meeting their emissions goals.43 To meet net-zero emissions targets, a significant increase in renewable electricity capacity is required, tripling global installed renewable energy capacity to 11,008 GW by 2030.44 These requirements may rise further if the demand for electricity grows more quickly than expected. For instance, the expansion of data centers, driven by new AI applications, is leading to higher-than-expected demand in the United States. In fact, the Electric Power Research Institute estimates that, by 2030, data centers could consume up to 9% of US electricity annually—up from 4% in 2023.45 Some chemical companies have begun building onsite clean-energy electricity generation.46 However, this requires capital investment and sometimes has a lengthy permitting process.

Changes to policy

The policy and regulatory environment can influence chemical companies’ investments in R&D and capex, including those necessary to lower emissions and innovate new, sustainable products and processes. In the United States, permitting processes and policies related to circular solutions and renewable feedstocks can impact these investments. Similarly, global regulations in Europe or other measures in Asia are expected to continue to impact investment decisions in those regions.

Capturing value across ecosystems

Chemical companies upstream in the value chain continue to decarbonize their products and processes; however, they still face the problem of tracking carbon emissions across their product value chains. As a result, companies upstream that need to make significant capital investments to reduce emissions can struggle to capture a premium that customers may be willing to pay for environmentally sustainable solutions toward the end of the value chain or aggregate the downstream demand to rationalize upstream investments. This problem is exemplified by the fact that while scope 3 emissions account for about 75% of the average chemical company’s total emissions (with 50% coming from upstream activities), only around 30% of chemical companies currently report their scope 3 emissions because of the challenge of tracking emissions across their value chains.47

While many standards have been created to help companies across industries track their value chain emissions, there are still gaps that need to be clarified for the chemical industry. Consequently, companies are left to navigate this complex landscape by exploring innovative strategies to capture value, such as long-term contracts with buyers, product carbon-footprint assessments, and book-and-claim agreements. Some companies are using digital platforms that utilize blockchain, digital twins, and AI to monitor low-carbon products throughout the supply chain in a transparent and efficient manner.48 These technologies can facilitate real-time tracking, traceability, and compliance with environmental standards.

There has been some slowdown in decarbonization investment announcements in 2024, likely in part due to high interest rates, uncertainty in global markets, and a hesitancy to increase investments before better understanding the return on investment from previous projects.49 However, chemical companies should work to continue to make progress as demand for more sustainable products grows. The innovative ways that companies find to navigate these three challenges could contribute to their future success.

5. Supply chain: Building value chain resilience to navigate evolving regional dynamics

In the dynamic landscape of global supply chains, chemical companies are encountering both significant challenges and new opportunities. Geopolitical disruptions, climate disruptions, and regional changes in policies and regulations, in addition to shifts in supply and demand, have made supply chain resilience, including visibility, agility, and flexibility, increasingly imperative for chemical companies. At the same time, the chemical trade has increased over the past six years.50 And this trend will likely continue over the next decade, with the International Energy Agency projecting continued growth in chemical production and trade through 2030.51 Currently, China and the United States are leading the charge in this growth (figure 9), but other regions could emerge as major producers, such as India, Southeast Asia, or the Middle East.52 Similarly, other countries could begin to drive demand for chemicals. These shifts in consumption and production are expected to continue to be influenced by factors such as geopolitical and climate risks and regulatory differences.

Geopolitical and climate risks: Geopolitical and climate events impact chemical companies all around the world. For instance, the reduction of Russian natural gas supplies to Europe increased natural gas prices in the region, compelling firms to reassess their sourcing strategies.53 Conversely, disruptions in the Red Sea have rendered certain European chemicals economically viable once more, which also underscores the importance of agility in supply chains.54 Beyond geopolitics, drought conditions caused a reduction in traffic through the Panama Canal in 2023 and 2024, impacting trade routes and shipping costs.55

Policy and regulatory differences: Regional policies and regulations are also impacting global competitiveness and trade flows. Whether it’s import tariffs, emissions regulations, or tax incentives, these policies continue to impact company decisions on investments and supply chains. For instance, companies are still understanding and preparing for the impacts of Europe’s Corporate Sustainability Reporting Directive and the Carbon Border Adjustment Mechanism on the chemical industry.56 Compliance with these regulations requires flexibility in supply chain management to adapt to changing policies.

Regional shifts in supply and demand: The sources of supply and demand will continue to shift. For instance, while China’s economic growth is projected to slow, other areas such as Southeast Asia and parts of Africa are experiencing an acceleration in growth.57 On the production side, plant closures in Europe58 could lead to increased imports from the United States or Middle East for certain products. Additionally, there has been some regionalization of the manufacturing of some products. For instance, although China has been leading battery manufacturing, policy incentives in the United States may increase production in the country over time.59

The importance of supply chain visibility, agility, and flexibility

As 2025 approaches, the chemical industry will likely continue to grapple with challenges stemming from geopolitical tensions, climate risks, and regulatory and policy changes. While the chemical logistics sector has not fully rebounded to pre-pandemic levels, demand is expected to grow considerably over the next decade. To capitalize on this growth, companies likely need to enhance the flexibility and agility of their supply chains by leveraging digital technologies and strategic partnerships. The benefits of these measures would span all chemical company categories, strengthening their ability to weather future disruptions or shifts in geographical supply and demand fundamentals.

Digital transformation: Companies are increasingly adopting AI and analytics to enhance visibility and streamline operations. This digital shift can help enable better demand forecasting, real-time tracking, and more informed decision-making.60 For example, one company has implemented a digital supply chain platform that integrates data from various sources to provide real-time visibility and improve decision-making.61

Decentralization and diversification: The pandemic has highlighted the risks associated with centralized supply chains. Firms are now focusing on diversifying their supplier base and decentralizing operations to build resilience against future disruptions.62

Collaborative planning: Collaborative planning with suppliers and customers can help foster transparency and alignment, reduce uncertainty, and enhance overall supply chain performance.63

Monitoring supply chain resilience: Utilizing metrics that measure the adaptability of inter-firm relationships can provide insights into how firms can better navigate regional market dynamics.64 Research indicates that firms with a balanced approach to flexibility and stability are more likely to thrive in turbulent markets.65

How can chemical companies position competitively in 2025 and beyond?

While the companies’ approaches will depend on their strategic imperative, leaders should consider looking out for the following signposts while making decisions in the upcoming year.

- Macroeconomics: Moderate global GDP growth is expected to continue in 2025.66 As inflation falls, interest rates are expected to be cut, making the borrowing environment more inviting for new business investments. However, growth is not expected to be even across countries or regions,67 making some areas more attractive than others. Similarly, another slowdown is not out of the question, and companies will likely do well to continue increasing efficiencies and shift their focus to high-growth areas when possible.

- Policy and regulation: Regional policies and regulations will likely continue impacting chemical companies, both directly and indirectly, whether it be through end-market growth incentives, emissions reporting requirements, tariffs, or incentives for domestic investment. Macroeconomic conditions may also impact policy. For instance, while US policies have incentivized investment in manufacturing, factors such as market conditions, slowing demand, and policy uncertainty have reduced the momentum of these investments.68 Chemical companies have proven their agility in adapting to the changing regulatory environment over the past several years, but this ability will continue to be tested through 2025.

- Global risks: Geopolitical and climate risks will continue to impact supply chains, commodity prices, trade flows, and plant competitiveness for chemical companies. Continued investments in supply chain optimization and visibility will likely prove essential for success in the future.

- Portfolio transformation: Chemical companies are expected to continue their cost reduction measures through 2025, including the possibility of more divestitures. Consequently, this year could also bring an uptick in merger and acquisition deals, joint ventures, and other partnerships as chemical companies strengthen their portfolios and move into higher-growth markets. Additional activity could also emerge as energy companies look to vertically integrate and increase their exposure to chemical markets.

Methodology

Conventional approaches to segmenting the chemical industry into commodity, integrated, and specialty chemicals categories do not fully explain financial performance. This is mainly because many chemical companies are not in pure-play chemical segments. Consequently, a new initial segmentation approach was identified in November 2010, during the writing of “The chemical multiverse: Preparing for quantum changes in the global chemical industry.”

Deloitte updated this segmentation for the 2025 chemical industry outlook. In doing so, Deloitte plotted all publicly traded chemical companies with an annual revenue of more than US$1 billion on a two-dimensional plane with “Availability of financial resources” on the Y-axis and “Quality of businesses” on the X-axis (figure 10). While the former captures static resources that can only be spent one time (like cash, debt-paying capacity, or pre-paid assets), the latter measures company performance using these financial resources based on metrics like return on assets (ROA), return on capital (ROC), return on equity, and profit (EBITDA) growth.

The weighted score of “Availability of financial resources” comprises the following metrics:

- Cash and securities, based on balance sheets as of Dec. 31, 2023

- EBITDA, based on 2023 data

- Interest coverage ratio, calculated as earnings before interest and taxes (EBIT) divided by interest expense for the 2021 to 2023 period

- Maintenance capital turns, calculated as EBIT divided by depreciation and amortization (a proxy for maintenance capital), for the 2021 to 2023 period

- Enterprise value, based on 2023 data

The weighted score of “Quality of business” comprises the following metrics.

- R&D expenditure, calculated as a percentage of revenue from 2014 to 2023

- ROA, calculated as net income divided by total assets for 2014 to 2023

- ROC, calculated as EBIT divided by total capital for 2014 to 2023

- EBITDA growth, based on 2014 to 2023 data

The scores for each of these metrics are based on thresholds, using appropriate statistical methods. In cases where there was a significant correlation, a linear line fit was used to calculate scores. In cases where the correlation was weak, thresholds were set based on a normal curve fit, using a step-function scoring system.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}