The portfolio predicament How can upstream oil and gas companies build a fit-for-the-future portfolio?

10 April 2018

In an era of uncertain oil prices and higher shareholder expectations, developing a future-ready portfolio is likely to be a priority for O&G companies. However, with the myriad narratives and tools in the marketplace, this is easier said than done.

Executive summary

When the going got tough for many oil and gas (O&G) companies, most of them did whatever they could to weather the storm. In the extended downturn from 2014 to 2017, most upstream companies reduced costs, some high-graded their portfolios, others concentrated their assets, and still many struggled to adapt quickly enough.

While oil prices have since improved, companies that took actions to protect and transform their portfolios have not yet seen rewards. The stock prices of 73 percent of upstream companies worldwide has failed to grow in line with oil prices since January 2017.1 Even companies in some of the most promising resources and markets—for instance, the Permian in the United States―reported an average shareholder return of -14 percent as against a 25 percent gain in oil price.2

The lack of equity appreciation and continued weakness in financial results, despite operational and price improvements, suggest a need for deeper portfolio assessment, management, and restructuring by O&G companies. According to our analysis of the top 230 global upstream companies, the portfolios (consisting of producing, under-development, and discovered projects) of 77 percent companies could still face challenges in sustaining current production levels, funding future growth, and maintaining shareholder payouts in a $55 per barrel oil price scenario over the next five years.3

A deeper dive into the myriad portfolio narratives in the marketplace also indicates that at the heart of the matter lies the absence of a common understanding of what constitutes a “good” portfolio and a common tool to judge its effectiveness. With the help of a comprehensive portfolio analysis tool, companies can not only optimize their portfolio but also be in sync with how markets evaluate portfolios in this period of uncertainty.

This paper is part two in our series on portfolio optimization for O&G companies. To understand more about our research, read Seeking balance in the new normal, a look back at portfolio shifts and performance metrics over the past 10 years, using the Deloitte Upstream Diversification Index. The portfolio predicament updates the analysis, extends it to even more companies, and tests portfolio composition against potential future market conditions. |

In this paper, we set out to explore future readiness of O&G portfolios across price scenarios and identify certain traits exhibited by companies with future-fit portfolios. Companies that rank high in our analysis (top 30 out of 230) did the following five things that seemed to help them stand out from the crowd and in the eyes of investors:

- Actively managed portfolio within a consistent strategic framework

- Placed operational excellence over locational advantage

- Managed resources through the lens of investment cycles

- Grew in natural gas at a measured pace

- Followed a moderate risk-return investment strategy

Excellence, it seems, is therefore not happening by accident.

A gap in the narrative

Although the oil market remained highly volatile, crude oil prices (Brent) improved by about 25 percent between January 2017 to February 2018 as the extension of production cuts by OPEC-led nations and a recovery in demand reduced the three-year supply glut.4 But energy equities and indices, including both pure-play upstream and integrated oil companies, barely gained over the period. Global and US energy indices underperformed oil prices by 14–36 percent, especially when there was euphoria in capital markets worldwide (figure 1).5 In fact, the current stock price of 18 pure-play upstream companies, which have a combined market capitalization of more than $110 billion, is even below early 2016 levels when oil touched a 13-year low of $26/bbl.6

This underperformance came at a time when most upstream O&G companies were heavily focused on high-grading portfolios, lowering breakeven costs, and reducing capital intensity. According to our text analytics on over 200 unique O&G SEC filings per year, an average O&G filing cited words related to “portfolio optimization” about 1.5 times in 2016 and 2017, the highest over the past 25 years.7 Current breakeven in the O&G industry, in fact, is at a 10-year low and it has fallen across regions and resources.8 So, why is the market not rewarding the industry despite its laudable response? Or is there a disconnect between the actions of companies and the verdict of investors?

Is the stressed financial state and curtailed investment rate of O&G companies responsible? Partly yes, partly no. Although many companies are still sitting on a record pile of debt, about 70 percent of global upstream companies reported profits or positive free cash flows in the last quarter of 2017.9 Similarly, global upstream investment remains 40 percent below its 2014 peak but it rebounded modestly (about 2.5 percent) in 2017 and is projected to grow in 2018.10 The problem, in our opinion, is the multiple and piecemeal narratives and methods companies use to report their performance and assess their portfolios—that’s why most of them selectively highlight their peer-leading returns on certain assets while presenting quarterly results.11 This may neither be comforting nor convincing to investors.

Many tools, too many results

Before the shale boom, most companies and investors used standard metrics such as reserves replacement ratio, finding and development costs per boe, return on capital employed, and net debt to capital for reporting and benchmarking performance. Further, O&G projects had a typical investment to production cycle of three to five years, following a natural breakeven progression12 from full-cycle (planning phase) to after-cycle (base decline phase).

Shales, however, seem to have changed the game, leading to a potentially more complicated investment and economic landscape. Breakeven progression in shales gets completed in 0–18 months, the project narrative has narrowed down to a single well level and skewed toward half-cycle, a large inventory of drilled but uncompleted wells has come into the picture, and the economics vary significantly across wells and over time. This has given rise to multiple breakeven nomenclatures (from half-cycle to full-cycle to corporate breakeven to cash neutral) and selective disclosures from companies (sharing breakeven of their best wells only).13

The shorter-cycle, capital flexibility of shale projects has also impacted conventional resources. Many producers are now prioritizing brownfield expansions over greenfield projects, following a parallel and integrated exploration and development approach in mega projects, and extracting more from their mature fields. As a result, the time-to-market of conventional projects is undergoing a significant change, with some offshore shallow and deepwater projects seeing first production earlier than many low-risk onshore projects (for example, the time-to-market for ENI’s Zohr project in the eastern Mediterranean with estimated reserves in place of 5.5 billion boe was less than 2.5 years).14

Put simply, the portfolios of most O&G companies worldwide are undergoing tectonic changes, making it more difficult to study and appraise them using standard portfolio evaluation metrics. The most talked about “breakeven point” published by producers has become highly incongruent, veiling the performance gap between premium assets and the overall portfolio of a company. Our study of top integrated oil companies (IOCs), pure-play exploration and production companies (E&Ps), and national oil companies (NOCs) reveals a breakeven gap of $19–33/bbl between their best assets and their overall portfolio (figure 2).15

Clearly, there is a need to simplify this complex landscape and achieve more consistency among diverse market narratives. The industry and its stakeholders would benefit from having a rigorous framework that statistically normalizes changes in a company’s portfolio across multiple dimensions and sums up all changes in one comparable number. Deloitte’s Upstream Diversification Index sets out to provide such a framework. (For more information, see the sidebar, “Deloitte’s Upstream Diversification Index.”)

Deloitte’s Upstream Diversification Index

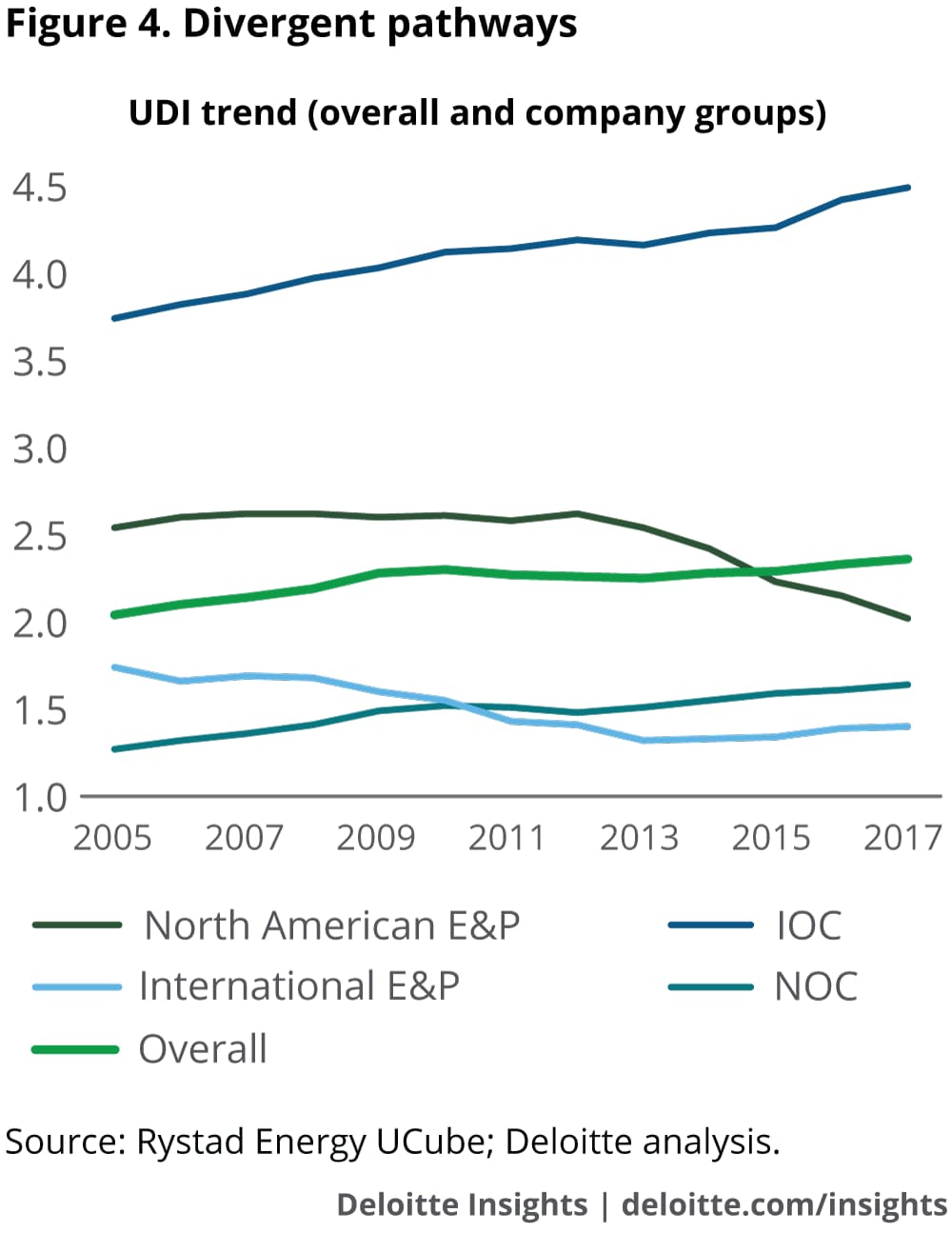

Deloitte’s Upstream Diversification Index (UDI), developed in 2016, is a framework that analyzes changes in an upstream portfolio across five dimensions: fuel, region, resource, basin, and investment cycle (figure 3).

The updated UDI, including the addition of 100 new public, private, and government entities that now covers 78 percent of global O&G production, reveals significant changes the industry and the portfolio of companies have gone through over the past 2–3 years.

Understanding the portfolio problem

While a volatile price and complex business environment is now the new normal for O&G companies, certain new trends appear from the most recent Deloitte UDI results, which can help us understand the “portfolio conundrum” in the industry.

- The industry’s focus on crude oil remains despite its lower price expectations and weaker demand outlook for the long term. About 58 percent of the companies in our analysis increased the proportion of oil in total production over the past three years. Put another way, the share of natural gas, which is projected by many as the fossil fuel of the future, in a company’s production grew for only 42 percent of the companies.17 In fact, some large players such as ConocoPhillips and Noble Energy have put several of their natural gas weighted assets in the United States for sale.18

- Most US shale producers are focused on building optionality in their portfolio—as reflected in the high standard deviation of their UDI scores and their growing inventory of drilled but uncompleted (DUC) wells. But, this optionality seems to be running ahead of, or coming at the expense of, optimization, as efficiency gains are moderating in shales despite all-time high proppant intensity rates. As shown in figure 5, production per well completed (shown as the gap between indexed production and well completion) has remained almost flat over the past 1.5 years despite advanced completion designs and a 100-basis-point increase in proppant intensity.19 Pioneer's CEO Tim Dove hinted at this moderation in efficiency gains when he mentioned that, “In the US, we are using a sledgehammer approach. We are using larger volumes of sand and fluids and pumping at higher rates . . . At some point you reach a peak on logistics, limits on sand, water volumes. That’s where we are getting to.”20

One tool to assess them all

Just as changes in a portfolio can be standardized using the Deloitte UDI, many companies would also benefit from having a simple yet comprehensive approach to assess and benchmark the future readiness of their portfolio. This is both important and challenging in this world of higher price uncertainty and more diversity of available performance metrics and benchmarks.

Broadly speaking, a fit-for-the-future portfolio would be one that shields itself from probable price downsides, best sustains performance in a lower-for-longer price environment, and scales up most quickly when prices move higher. In figure 6, we detail the characteristics of the shield-sustain-scale (3S) framework.

A bottom-up analysis of 32,000 global assets of 230 leading O&G companies by production (from Rystad Energy UCube database) provides some answers as to why the market has perhaps not rewarded O&G companies despite their claimed portfolio adjustments.

The following analysis evaluates the potential performance of portfolios over the next five years (2018–2022), a period where we have visibility into the development and production schedules, well profiles and economics, cost structures, etc., of these assets (for more details, see table 2 in the appendix).

These results are driven by asset economics and are independent of the capital and financing structure of a company. A company falling short on one or more parameters doesn’t necessarily imply a risk to its existence and continuity of operations. But it should be read by portfolio managers as areas of opportunity to further high-grade their portfolio for an uncertain future. Figure 7 lists detailed results by each parameter.

- Shield: Although recovering variable operating costs at $40 per barrel (2018–2022) would be less of a challenge for many, net profitability and operating cash flows would take a significant hit across the board. The key for companies would be to shield their stressed cash flows by minimizing the impact on production and lowering capex. According to our analysis, 80 percent of the 230 companies would likely face this challenge. In fact, many companies would likely face a double whammy of higher pre-productive capital commitments and falling production.21

- Sustain: At $55 per barrel over the next five years, about 40 percent of the companies would likely face challenges in sustaining their current production levels, funding new projects, and maintaining their distribution payouts from producing assets; however, the proportion rises to 77 percent when the entire portfolio of a company, including under-development and discovered assets, is analyzed. The remaining 23 percent that are sustainable at $55/bbl constitute only 27 percent of the production of our sample set, suggesting that the risk is not limited to small and medium-sized companies.22

- Scale: Recovery and stabilization of oil prices at around $65 per barrel would likely improve the profitability of companies; the key is how much and how early they can grow incremental free cash flows. According to our analysis, 62 percent of the companies would likely be left behind in monetizing the probable recovery in oil prices. About half of these companies, in fact, would likely register flat to lower gains in free cash flows even in a $65 price environment.23

This may explain why despite so many self-help measures, much could still be done by O&G companies to optimize their portfolios and give investors more confidence that the sector can thrive across a range of business conditions.

More positively, although each company has a unique portfolio and financial profile, the 3S analysis allows us to highlight a few common characteristics and traits of companies with the strongest future-ready portfolios.

Common traits of companies with a future-proof portfolio

To understand if there are any traits that sets apart companies with strong, resilient portfolios, we combined the analytical capabilities of the UDI with our 3S model. Using the 3S model, we selected the top 30 companies that likely have a fit-for-the-future portfolio and evaluated their collective traits using the UDI. While every company has its own priorities and goals, these characteristics can serve as a good starting point for those looking to optimize their portfolio in the long run (figure 8).

Patterns amid chaos: Following a consistent strategy and actively managing portfolio

Companies pursuing several resource options, selecting projects and buying and selling assets in the M&A market based on transitory market conditions, have ended up with a suboptimal and directionless portfolio. Similarly, companies that may have followed a more consistent strategy—but disregarded ongoing shifts in the industry—have been left with a less agile and future-ready portfolio. Being purposeful can be destructive, and doing nothing is not an option.

Companies with good portfolios, in our analysis, follow a consistent strategy (concentration or diversification) and manage their assets actively. About 75 percent of the top 30 portfolios have been consistent in either concentrating or diversifying their portfolio, with a healthy pace of change and churn in their portfolio. BP, for instance, has maintained its diversified portfolio (UDI of around 5.75 since 2012) and actively followed a “value over volume” approach after the Macondo incident.24

The “how” before the “where”: Prioritizing operational excellence over location

Most of the top 30 companies have refrained from the general trend of entering or acquiring acreages in the trending regions/basins/rocks. This is evident from the fact that the Permian basin, which has become known for its productivity gains and resilience to lower prices, is not a formative basin for many US companies that have built a future-ready portfolio. On the other hand, basins such as the Anadarko and Williston, which registered significant decreases in production in 2015 and 2016, are central to many companies that have built a robust portfolio, according to our analysis.25

Similarly, a few of the top 30 have also built robust portfolios in regions such as the North Sea, which has a mature production profile or is not seen as a promising region by many. Although 80 percent of the top 30 are concentrated in just one region, a few of the top performers (those with a UDI of more than 3) also have a regionally diversified portfolio. The general notion of reaping benefits by mastering in one holds true, but achieving mastery in all is not out of the question.26

Through a different lens: Manage resources by focusing on investment cycles

Many O&G companies have historically sought consistent reserves and production growth over time, with attaining a balance in exposure to investment cycles as more of an afterthought or next step. However, the top 30 companies in our analysis seem to have overturned this notion, by optimizing their resource portfolio using the lens of investment and cash cycles.

Most of the top performers have built significant investment flexibility in their portfolio, either by focusing on short-cycle projects or reducing the time-to-market for mid- and long-cycled projects. US performers in our analysis are complementing their shale-only strategy by having the shortest and most flexible investment cycle. On the other hand, performers outside the United States are reducing their risk of concentration in a resource or a project by shortening their time-to-market for mid- and long-cycled projects by 1–2 years and prioritizing smaller projects and resource sizes.27

A balanced mix: Exposure to gas is important but not central yet

Although 25 out of top 30 portfolios have an oil-heavy hydrocarbon mix, the share of natural gas in their overall production is not less than 25 percent.28 This suggests that gas is essential to a fit-for-future portfolio, but has yet to take a mainstream role. The five companies that are gas-heavy are small-sized and operate in niche markets outside the United States.

Most of the top portfolios, however, have maintained their oil-gas mix over the past five years—neither did they aggressively buy into the premium oil story nor did they take expanded positions in the fuel of the future (natural gas and LNG). Companies owning these portfolios tend to closely follow the changing demand patterns in both the fuels, where oil’s weaker long-term demand growth potential and gas’s overpromised near-term outlook because of infrastructure constraints have been translated into a fairly stable mix.

Not two sides of the same coin: Understanding that strong financials need not necessarily mean a future-ready portfolio

Of the 61 O&G companies listed worldwide with a low net debt to capital ratio of less than 25 percent, only 6 make it into the top 30 list.29 Conservative investments and/or higher shareholder payouts seem to be moderating their growth potential and flexibility quotient, while a strong balance sheet and minimal pressure from creditors appear to be concealing inefficiencies in select portfolios.

Most companies in the top 30, in fact, have a moderate yet disciplined net debt to capital ratio of 25–55 percent.30 The majority of the top performers seem to have used the low interest rate environment to channel more debt finance into promising projects, allowing them to balance short-term financial priorities with longer-term value creation potential. A point worth noting: Our analysis doesn’t minimize the importance of having a strong balance sheet and maintaining a relentless focus on shareholder returns. But it reiterates the importance of having the right balance of growth and return and weakens the notion that the strongest balance sheets translates into the strongest portfolios, and vice-a-versa.

Solving the portfolio predicament

The nascent recovery from a long period of market downturn is a phase of adjustment amid continued uncertainty for upstream O&G companies. Delaying the adjustment does not seem like an option, but nor would randomly shuffling a portfolio lead to success. Likewise, standard portfolio assessment tools are challenged by the new dynamism in the market, while the selective narrative of companies has not convinced investors or equity markets.

Upstream strategists—already disoriented by four years of turmoil—would benefit from having a simple yet consistent, relevant, and comprehensive approach to make their portfolio fit for the future and explain their strategy to the market, perhaps avoiding the systemic underperformance experienced by the sector in the most recent past.

Although the approach should be tailored to match each organization’s size, financial, and operational capabilities, and its strategic priorities, the following six steps can serve as guiding principles for every company to transform their portfolio:

- Ascertain the direction, magnitude, and speed of changes in current portfolio

- Analyze portfolio shifts and validate portfolios’ alignment with strategy

- Evaluate the portfolio’s ability to shield, sustain, and scale up across price decks

- Benchmark to identify successful traits and characteristics of a future-ready portfolio

- Learn and transform by playing to strengths

- Communicate strategy and portfolio choices using the consistent language and the metrics of future-proofing

Appendix