Could artificial intelligence fuel the future of financial investigations?

AI can both facilitate and prevent financial crimes. Combating these crimes can require strategic resource allocation, robust risk management, and adaptability to evolving threats.

Ann Law

Tina Mendelson

Bruce Chew

Michael Wylie

Scott Holt

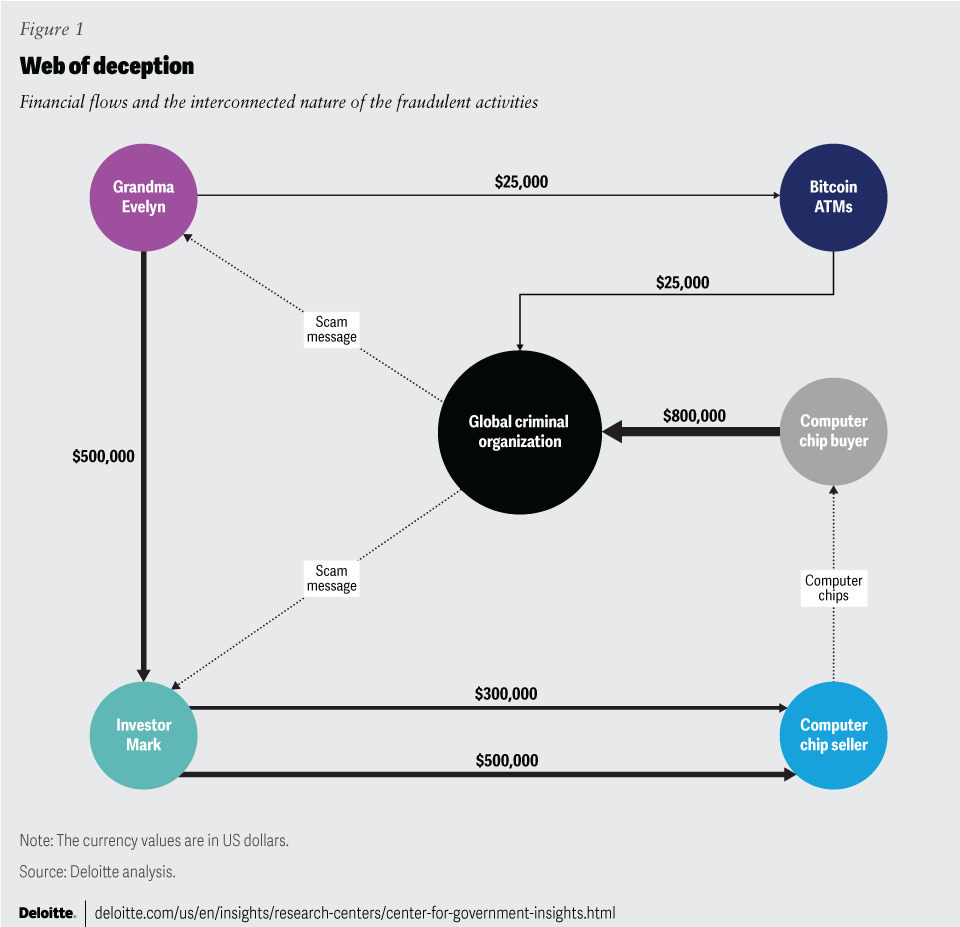

This hypothetical scenario begins in a small bungalow in a suburban town, a seemingly unlikely spot for a sinister plot to unfold. There, Grandma Evelyn’s evening crossword puzzle is interrupted by a soft ping from her tablet. The message claims to be from her beloved grandson, Ethan, who says he is stranded in a prison outside of the country and in desperate need of bail money. Heart pounding, Evelyn watches the attached video message. There, apparently, is Ethan, pleading for help. Without a second thought, Evelyn rushes to her bank.

Evelyn withdraws US$25,000 from her life savings and, as instructed earlier, deposits it into seven different Bitcoin ATMs scattered across town. Each transaction sends the cryptocurrency to wallets controlled by a faceless global criminal organization that has never laid eyes, let alone hands, on Ethan.

As Evelyn returns home, her relief is short-lived. Another message appears on her screen, this time demanding access to her computer. Before she can react, her device is hijacked, and Evelyn watches helplessly as her bank accounts and retirement funds are drained of US$500,000. The funds vanish into the depths of cyberspace, leaving her financially crippled and emotionally shattered.

But the story doesn’t end there. Across town, unsuspecting victim number two—investor Mark—receives a highly anticipated windfall in his accounts. Excited by what he believes to be his new partners’ co-investments, he prepares to consolidate the funds and sends them to a shipping company to initiate the delivery of his latest venture: computer chips.

Unbeknownst to Mark, his transaction is fueled by fraudulent funds orchestrated by the same criminal organization that preyed on Evelyn. Mark has been in conversation with a “friend,” Jennifer, whom he met on an “investment” social media group. Jennifer mentioned trade financing as an investment opportunity. Mark has already sent US$300,000 of his own money before receiving the windfall “co-investment” that was really Evelyn’s retirement account.

As the chips are shipped off, revenues for the shipment are paid to the masterminds, completing the cycle of deception and simultaneously triggering a chain of rapid and complex financial transactions enabled by nascent technologies that can make detection and recovery of the fraudulent funds all the more difficult (figure 1).

A US$2 trillion problem now fueled by artificial intelligence

Grandma’s and Mark’s ordeals serve as a reminder that new technologies offer new opportunities in the rapidly evolving world of crime. The ability to create artificial sounds, images, and videos that are nearly indistinguishable from the real thing expands the potential toolset of financial crime. For these criminal innovators, the new generations of AI can offer a lower cost for committing crimes at scale with the potential for higher returns.

Financial crimes, including money laundering, a pervasive concern, have reached unprecedented levels, with estimates suggesting a staggering 2% to 5% of the global GDP, equivalent to nearly €1.87 trillion, laundered annually.1

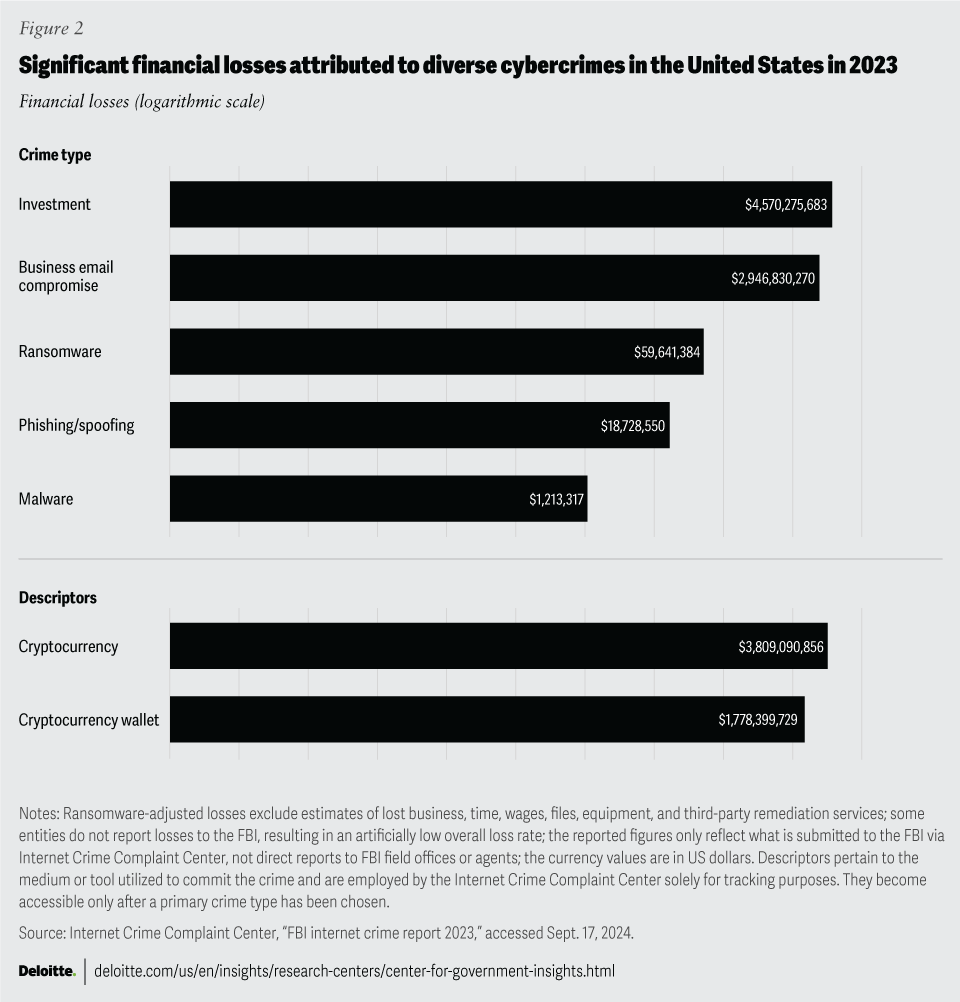

Criminals are increasingly using AI and machine learning to identify loopholes. These include elements that can help them evade detection, such as patterns in transaction behaviors and areas where regulatory oversight may not be as robust, as well as personal information that can be used for phishing and other fraudulent activities. By continuously scanning numerous data sources, including social media and deep web forums, they plan and perpetrate fraud before it is detected.2 Additionally, they are exploiting the growing use of digital assets and blockchain technology, taking advantage of the complexities and challenges in tracing transactions in these areas, which can make it difficult for regulations to keep pace (figure 2).3

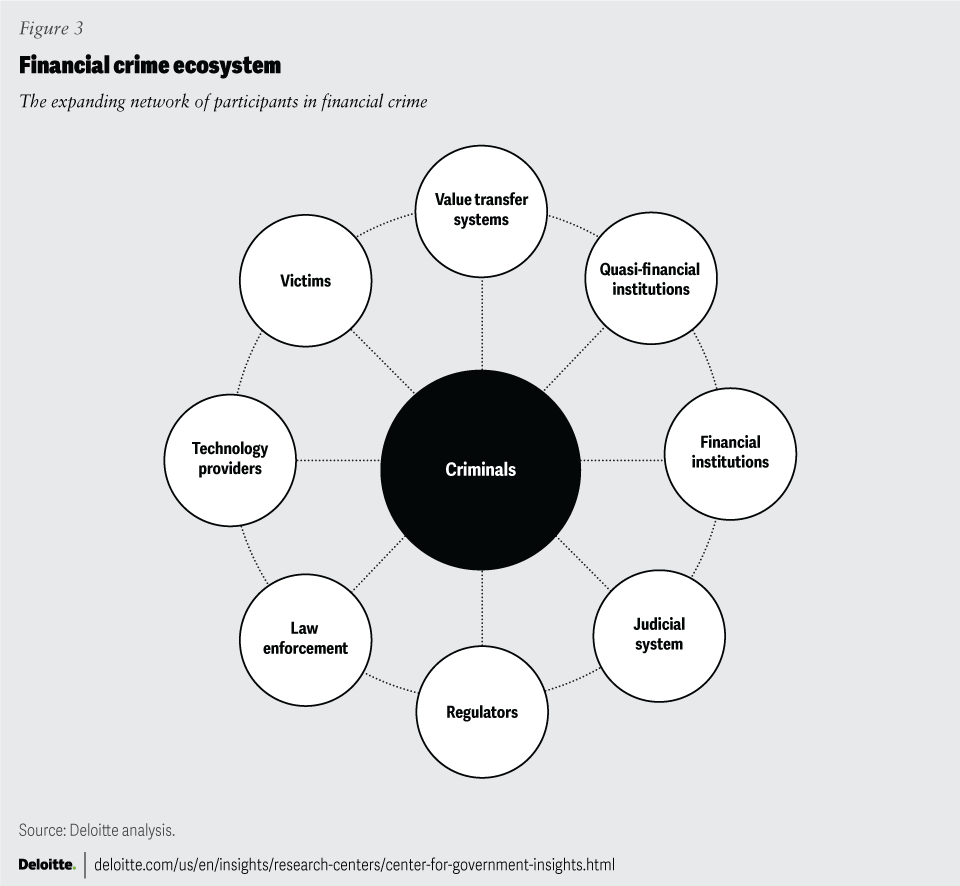

These technologies are being adapted and adopted to commit financial crimes. But another evolutionary aspect along a different dimension can also assist perpetrators and confound investigators: the growing ecosystem, including unwilling and unwitting participants (figure 3). As described in the hypothetical story above, a host of participants—each with their own interests and roles to play—are often engaged in the narrative of deception and deceit. At the heart of the matter, the criminals perpetrate their illicit activities driven by motives as diverse as their methods.

Yet, they are not the solitary actors in this tale. Their actions send ripples across society, leaving a trail of victims. Individuals, businesses, critical infrastructure, and markets can fall prey to their schemes, suffering losses both tangible and intangible.

Financial institutions such as banks and credit unions can inadvertently become facilitators of financial crime schemes through gaps in their compliance and monitoring systems. For instance, insufficient due diligence, weak Know Your Customer (KYC) processes, or inadequate transaction monitoring might enable illicit activities to go undetected. Quasi-financial institutions, including exchanges, payment processors, casinos, and sports betting platforms, can become unwitting accomplices, facilitating the flow of illicit funds. Meanwhile, value transfer systems like art, trade, and cryptocurrency can be conduits for money laundering and illegal transactions.4 Technology providers, law enforcement agencies, the judicial system, and regulators should navigate this increasingly complex labyrinth of deception together.

New technologies and rising complexity have often made it easier to plan and perpetrate crime and obfuscate the trail left behind. However, those technologies are also available to those who strive to prevent these crimes and bring perpetrators to justice.

Considerations for the future of financial investigations

In today’s rapidly evolving financial and technological landscape, the imperative for robust and effective financial investigations has never been more pronounced. As financial crimes become more sophisticated and globalized, and the amount of global gross domestic product related to money laundering and financial crime continues to grow, traditional investigation methods are proving insufficient to keep up with this pace.5 Hence, there’s a need for ongoing evolution in technology tools, investigative approaches, cooperation, and collaboration with regulators and other stakeholders (see “Cryptocurrencies: A case example of evolutionary response”).

The future of financial investigations could hinge on embracing a multilayered approach that incorporates harnessing advanced technologies, adopting modern and nimble methodologies for portfolio-based case management, and increasing collaboration within the investigative ecosystem. The following sections delve into these considerations, explaining their significance in shaping the future landscape of financial investigations and helping to ensure greater efficacy in combating financial crime.

Cryptocurrencies: A case example of evolutionary response

The rise of digital and cybercrimes, such as darknet criminal marketplaces and cyberattacks against critical infrastructure, require advanced digital forensic tools and training. One can look at how the US Department of Justice has evolved its understanding and approach regarding cryptocurrencies over the past decade.

In the early stages of the criminal adoption of cryptocurrency as a means of value transfer and money laundering, law enforcement lacked the appropriate tools and technology to deanonymize and track these transactions effectively. Traditional investigation methods often proved inadequate due to the lack of centralized governance, regulation, and industry responsiveness to law enforcement inquiries, especially since many cryptocurrency exchanges fell outside US jurisdiction.

Significant milestones in the regulatory landscape include the issuance of important directives pertaining to cryptocurrency within a legal framework. These regulatory measures have played a crucial role in shaping the compliance and operational standards for cryptocurrency entities.

- Financial Crimes Enforcement Network, FIN 2013-G0001, required cryptocurrency issuers and exchanges to register as money service businesses.6

- Internal Revenue Service Notice (2014 to 2021) defined the appropriate tax treatments of cryptocurrency as those applicable to any appreciable asset.7

- Securities and Exchange Commission Report of Investigation 34-81207 clarified that some public initial coin offerings and exchanges required registration with the commission.8

Through trial and error, investigators were able to set the foundation for future institutional knowledge of blockchain technology and devise strategies to disrupt abuse by bad actors. Gradually, investigation protocols for cryptocurrency investigations, seizure, and forfeiture were developed and disseminated throughout federal and state law enforcement agencies through training.

Along with adaptations in law enforcement, the growing market capitalization, systemic economic importance, and regulatory scrutiny of cryptocurrency incentivized the industry to develop stronger know-your-customer and customer due diligence programs designed to reduce liability and exposure to unlawful activities. In parallel, financial technology stakeholders seemed to recognize the need for the ability to trace blockchain transactions and developed heuristic models that could distill data into more readable, graphical depictions and attribution techniques, allowing both industry and law enforcement stakeholders to track the movements of cryptocurrency and exposure to darknet markets or other unlawful activity.9 By redefining the regulatory, investigative, and prosecutorial strategies, authorities can navigate the intricacies of contemporary financial crime with greater efficiency, effectiveness, and cost-effectiveness.

Harnessing advanced technology: A necessity, not an option

In the face of escalating financial crime, adopting and enhancing cutting-edge technologies is no longer a matter of choice but a pressing necessity. AI has emerged as a dual-edged sword, serving as a powerful tool for both businesses and criminal enterprises. Just as technologies have advanced to lower the barriers to business creation and operation, the same technologies are exploited by criminal enterprises to operate, facilitate, and hide among legitimate businesses. AI-generated deepfakes and synthetic identity fraud have been used to commit crimes and fabricate realities, potentially impacting national security.10

Synthetic identity fraud, the fastest-growing financial crime in the United States, involves creating new identities with stolen or fabricated data.11 The financial sector, already a prime target for such frauds, reported a 700% increase in deepfake incidents in 2023 alone.12 Advances in generative AI now make it easier to create realistic images and videos, enabling crimes and potentially threatening national security.13

With generative AI, fraudsters can now execute large-scale schemes targeting multiple victims simultaneously, significantly amplifying potential losses. On the other hand, AI is pivotal to managing the voluminous data associated with financial crime. For instance, in one investigation by the Federal Bureau of Investigation, six petabytes of data were collected, equivalent to over 120 million filing cabinets filled with paper.14 This volume of data is nearly impossible to sift through manually and in a timely fashion. AI can help by automating this process rapidly identifying relevant information for agents to act on. As businesses adapt and evolve, criminal enterprises adapt and evolve as well; regulating and enforcing the laws should adapt and evolve with it. The following are some ways advanced technology, including ethical AI, can be adapted to accelerate financial investigations now and in the future.

Generative AI for text summarization can condense large amounts of data from various legally obtained sources like emails, phone calls, text messages, images, invoices, bank accounts, wires, blockchain, trade data, IP addresses, in-app messages, geotagging, interviews, corporate registries, and internet domains. This can be beneficial in law enforcement investigations. It can also automate open-source intelligence reporting and generate reports based on descriptions or pictures of the relevant subject. These advances can offer opportunities to enhance productivity in the public sector by driving decision-making, reducing costs, and fostering innovation. However, while AI can transform business functions and increase efficiency, it is essential to maintain a human in the loop. This can help ensure that AI’s integration into systems is done thoughtfully and responsibly, allowing for ongoing review and adaptation.

The United States Department of Justice has historically emphasized careful implementation and societal impact assessment when adopting new technologies, a practice that should continue as AI becomes more embedded in its operations. Maintaining human oversight is crucial in ensuring that AI advancements benefit all stakeholders while safeguarding ethical standards and equity.15

Virtual assistants, enabled by generative AI, can allow investigators to query datasets with plain language, providing personalized responses to queries. Imagine an investigator asking the dataset how much money was sent from Evelyn to Mark. When did the transactions occur? Were there others who sent money to Mark? Investigators may have access to this information through some form of summarizing in spreadsheets or notes. A virtual assistant can answer those questions and allow for deeper probing by the investigator. It can also facilitate faster onboarding and training of investigators and help them be more effective and efficient.

Virtual reality can be used for training opportunities, offering specialized training, and placing the user in various simulated situations for better learning. Imagine officers honing their skills in simulated high-pressure situations, from questioning individuals in the field to special response teams serving a warrant. Virtual reality provides a safe and controlled environment for officers to practice specialized skills and tactics, make split-second decisions, and experience the emotional weight, pressure, and confusion of these encounters. This immersive training can lead to more confident, prepared, and effective investigators.

Anomaly detection with AI can identify patterns and anomalies at a speed that outpaces human-led data analysis efforts, which can be crucial in identifying suspicious activities or trends in law enforcement. Data-heavy investigations often require sifting through mountains of information to find leads. Algorithms can analyze vast datasets at superhuman speeds, identifying patterns and deviations from the norm that human analysts might miss. This can help law enforcement to pinpoint suspicious activities or emerging trends much faster. Imagine spotting a sudden surge in financial transactions linked to a known criminal organization or identifying unusual traffic patterns near a potential target in near real time. By deploying anomaly detection AI tools, investigators can move as fast or even stay ahead of criminal actors.

Ethical AI is of broad concern. But it is of particular concern where specialized intelligence’s outputs and methods may need to be defended in court. AI can be used safely and securely, reflecting transparency and accountability while maintaining and protecting privacy. This means working to ensure algorithms are free from bias and produce fair results. Additionally, clear accountability structures should be established to identify and address errors or misuse. Keeping a human in the loop is essential to determine that AI decisions align with ethical standards and societal values. Human oversight allows for the detection and correction of any unforeseen issues, helping to maintain trust and responsibility in AI applications.16 It is vital to prioritize and protect individual privacy throughout the AI life cycle, ensuring data is used responsibly and only for legitimate purposes. This ethical approach fosters public trust and demonstrates that AI is a powerful tool for good use in law enforcement. It also provides clear, transparent avenues for court adoption.

A portfolio-based approach to case management

While embracing AI and advanced technology could certainly accelerate aspects of cases, a portfolio-based approach to overall case management can lead to better prioritization, resource allocation, risk management, and adaptability. There are often many variables associated with any investigation, including timelines, available information, available personnel, complexity, specialized knowledge requirements, and the constant change of each.

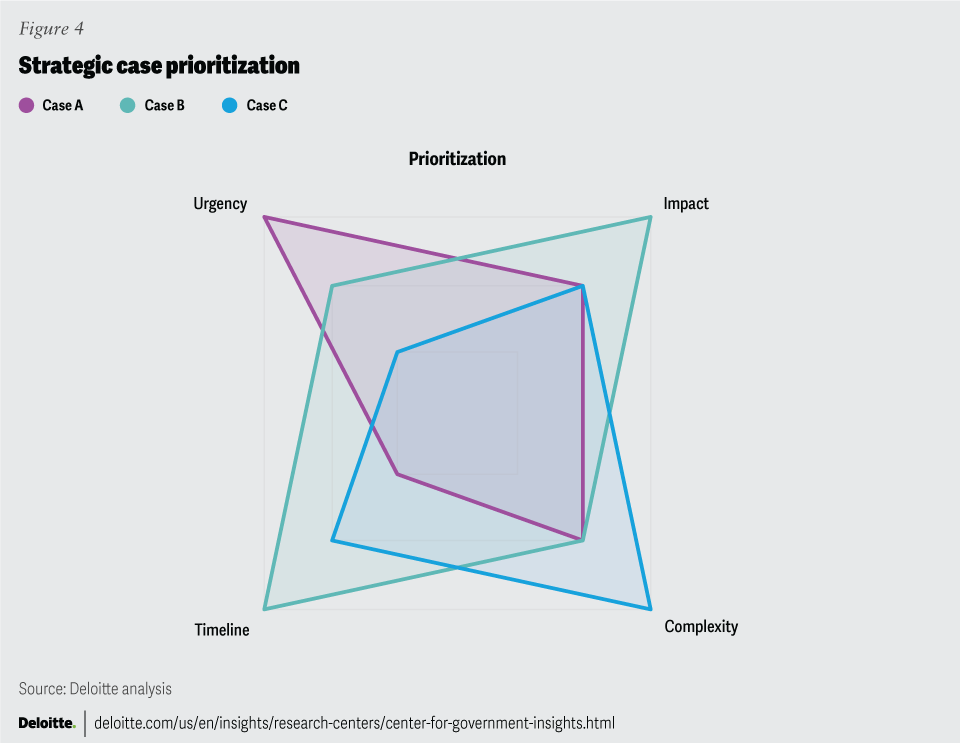

Case prioritization: An effective portfolio approach to investigations involves strategic prioritization of cases based on various factors such as urgency, impact, and complexity. As shown in the prioritization diagram (figure 4), cases have different profiles across these critical dimensions. To help prioritize, it may be necessary to assess the project on each dimension, recognize that these assessments may change during an investigation, and determine how to weigh them to provide a useful comparison.

Interestingly, this is another area where AI may be useful. AI can assist in efficiently allocating resources, ensuring that high-priority cases receive the necessary attention and resources while less critical cases do not consume significant resources. This approach helps ensure that significant resources are focused on the most critical cases, enhancing overall effectiveness and efficiency in investigations. For example, an AI-based system modified to analyze specific factors of a case early in its life cycle against established criteria can determine whether to drop or pursue the case. With a dynamic and ever-evolving financial crime landscape, it becomes crucial to recognize the importance of timeline, urgency, and impact in prioritizing case management. Of course, portfolio management is not as simple as “score and pick a winner.” It’s also important to factor in the necessary resources required and continuously refine the approach as lessons learned emerge.

Resource allocation and workforce transformation

Harnessing the technology often takes many forms, one of which is workforce transformation to understand whether the investigative team has the requisite skills to thoroughly and ethically use the available technologies. In addition to investigators, this should include data scientists, AI experts, software engineers, and cyber and crypto experts, among others.

Resource allocation: Resource allocation is another aspect of a portfolio approach to case management. Factors such as the availability of personnel, their current caseload, specialized knowledge, and skills, as well as geography and venue, can influence the allocation process. Through assessment of these elements, resource optimization can enhance case results, centering on AI utilization. Simultaneously, an investigator can concentrate on validating outcomes—instead of identifying them—or handling more complex tasks that necessitate human inquiry. In the near term, law enforcement agencies might continue to prioritize upskilling existing staff or hiring new resources who are better versed in emerging tech (see “Resource allocation and workforce transformation”).

Risk management: Investigations involve some level of risk due to pressing timelines, increased complexity, and resource turnover. Therefore, a portfolio approach to case management should include incorporating robust risk management strategies. By identifying potential risks early in the case, investigators can develop suitable mitigation strategies, thereby reducing the likelihood of negative outcomes.

Adaptability: The portfolio approach to case management requires a high degree of adaptability in the dynamic world of financial investigations. This involves continuously evaluating and rebalancing the portfolio based on the evolving circumstances of each case. As new evidence emerges, it may require significant changes to the direction of a case.

Additionally, AI can reveal previously unnoticed connections or patterns across the portfolio of cases. Consequently, what seemed less urgent as a stand-alone case may become more critical within the broader context of the entire portfolio. As the investigation progresses, resources may become available, and new risks may become apparent. Adaptability enables investigators to refocus cases and shift priorities to stay one step ahead in the fight against financial crimes.

Increasing collaboration within the ecosystem

There are various existing coordination efforts involving law enforcement agencies, including regulators such as the Financial Crimes Enforcement Network, financial crimes and anti-money laundering compliance units within financial institutions, and organizations like the global Financial Action Task Force. Additionally, increasing levels of fast and agile collaboration will be essential to help counter the rapid evolution of international crime.

Better technological integration is a key consideration. Interoperable data platforms, for example, can enable participants to collectively leverage information to tackle difficult problems and seek global solutions. However, it is crucial that these efforts are supported by robust data and privacy protections to help ensure that sensitive information is handled responsibly and in compliance with legal standards. This could be largely a behavioral and, in some instances, legal shift rather than a technical one.

This group comprises Joint Chiefs of Global Tax Enforcement.

- Australia: Australian Taxation Office

- Canada: Canada Revenue Agency

- The Netherlands: Fiscale Inlichtingen-en Opsporingsdienst

- United Kingdom: HM Revenue & Customs

- United States of America: Internal Revenue Service Criminal Investigation

The Joint Chiefs of Global Tax Enforcement (J5) provides a useful example of how this type of deeper collaboration is both possible and effective. J5 is a global joint operational group formed in 2018 to combat transnational tax crime. Its members (see “Joint Chiefs of Global Tax Enforcement”) develop strategies for gathering information and intelligence, communicate regularly, and conduct joint investigations.17 An example of its effectiveness is the SafeMoon Indictment, in which investor funds were allegedly misappropriated for the personal use of the company leaders.18 This type of collaboration provides for data-driven decision-making, trend-sharing and identification, and breaking down jurisdictional barriers. J5 collaboration can be considered as a model across investigative agencies.

The collaboratively shared data can become even more powerful when combined with AI. Data-driven decision-making, backed by advanced analytics, can help financial institutions and law enforcement agencies identify patterns, trends, and anomalies crucial for the early detection and prevention of financial crimes. This approach shifts the focus from reactive measures to a proactive stance, enabling authorities to stop criminal activities before they cause significant damage. Financial crime actors have no border consideration, and this data-sharing approach across the ecosystem to fight crime is often a necessity.

A case in point is the Danish Business Authority’s use of AI to identify fraud and highlight material errors in financial statements accurately and rapidly. This AI-driven system conducts comprehensive analyses of over 230,000 financial statement filings received annually, highlighting the profound impact of advanced analytics on fraud detection.19

The exchange of intelligence, insights, and leading practices allows for a more comprehensive understanding of financial crime trends, methods, and risk factors.20 This, in turn, can facilitate more effective anticipation and response to threats. Resource allocation can also be optimized by using AI to enhance the identification of financial crime trends and to direct efforts toward addressing the most significant threats and highest-risk areas. To achieve this increased collaboration, clear communication channels should be established with regular meetings, secure information-sharing platforms, and joint training exercises to help build relationships and facilitate ongoing communication.21

By breaking down existing organizational and digital silos, regulatory bodies, law enforcement agencies, and financial institutions can establish a unified front to confront the multifaceted challenges presented by modern financial crimes.22

Key strategies for advancing financial investigations

The events that befell Grandmother Evelyn and investor Mark were once the stuff of dystopian science fiction novels. But, with advances in the capabilities of AI and advanced technologies occurring in exponential leaps and bounds, this stark future is already a reality. Harnessing new and emerging technology to aid in defeating these threats is imperative and can allow investigators to keep up with emerging and evolving risks. In order to successfully operationalize emerging technology, law enforcement agencies can be guided by several considerations, including:

- Generative AI can provide opportunities to process and query large volumes of information at unprecedented speeds, making investigators more effective and efficient.

- Beyond investigators, the need to use AI at scale may call for a specially trained financial crime workforce—including data scientists, AI experts, software engineers, and cyber specialists—to be paired with investigators.

- AI analysis can provide opportunities to address minor issues before they become big problems.

- Ethical AI can provide transparency into the process and increase viability in enforcement and judicial processes.

- AI-enabled and criteria-based portfolio management in a case management system can increase the overall impact and effectiveness of investigations.

- Global interoperable data platforms could help lead to better data-sharing and investigative cooperation, allowing the right data to be put into the right hands at the right time.

As financial criminals continue to adapt and evolve with new technological advancements, it is important that the approach to combating these illicit activities does the same. Investigators should continually innovate and refine their strategies, striving to keep pace with the evolving landscape of financial crime.

In today’s AI-enabled digital era, the economic cost of financial crimes is rising exponentially, requiring regulations, investigations, and prevention and mitigation measures to evolve alongside. This can allow the financial community to not only combat current challenges but also prepare for and anticipate the future of financial crimes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}