Focusing on the foundation: How digital transformation investments have changed in 2024

Deloitte’s year-over-year analysis of technology investments reveals material changes in priorities. Here’s what that means in the quest to accelerate digital transformation ROI.

Tim Smith

Gregory Dost

Garima Dhasmana

Diana Kearns-Manolatos

Iram Parveen

Saurabh Bansode

Last year, digital transformation possibilities seemed unbounded, with 44% of US leaders surveyed in Deloitte’s 2023 “Mapping Digital Transformation Value” survey using digital transformation to radically change their business. In 2024, it’s come back down to earth, with only 18% reporting the same. What’s driving the sea change?

We’ve built upon three years of Deloitte digital transformation research to better understand the changes taking place, surveying nearly 400 US respondents anew across five industries (see “Methodology”). This 2024 baseline illuminates the type of digital investments organizations are making, the technologies most important to enable, and the expected returns. It gives context to any leader initiating, funding, or delivering a digital transformation, and a feasibility check across a host of factors, from enterprise readiness to technology debt.

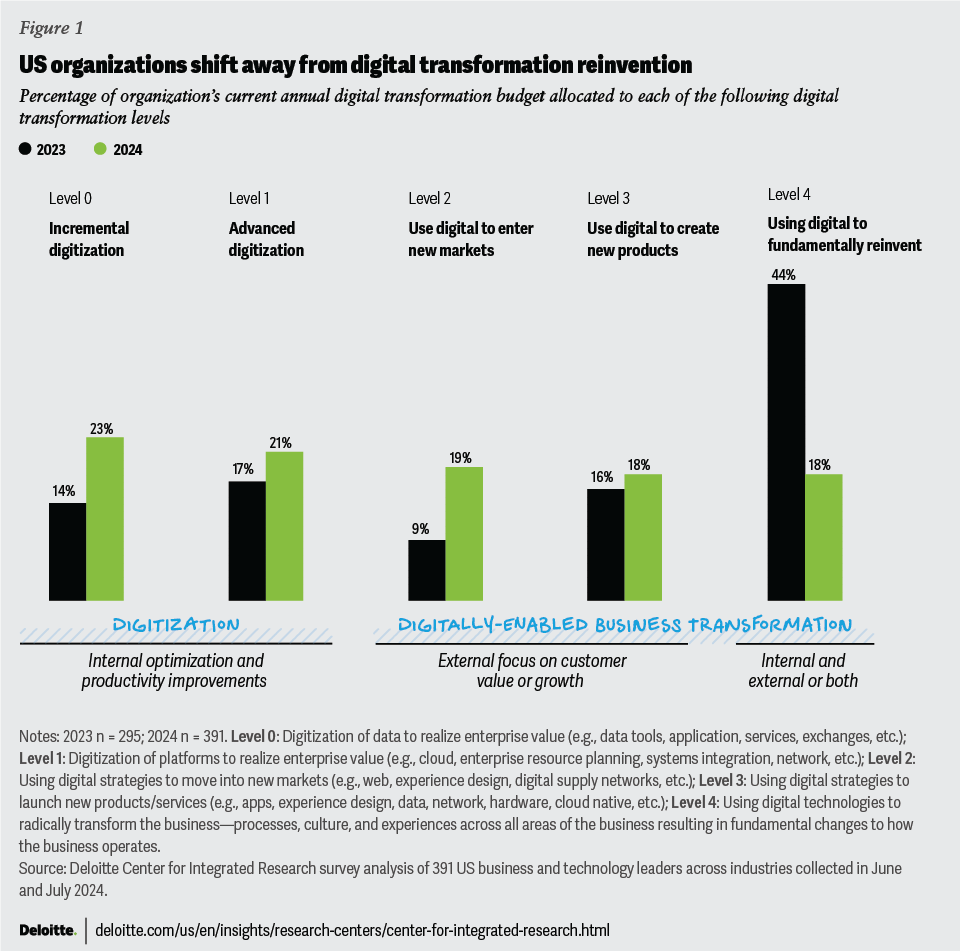

Digital priorities rebalance across the spectrum

Deloitte’s digital transformation spectrum identifies five levels, with an enterprise likely undergoing many simultaneously. Digitization of data and platforms—levels zero and one—focus on incremental optimization and productivity improvements. Digitally enabled business transformation—levels two through four—focus on new markets, products, or business model reinvention. These are more externally oriented, indexed on customer value and growth (figure 1).

Respondents are moving away from digital transformation as a “bet the business” reimagining (level 4) by 26 percentage points. The surplus is rebalanced across the remaining spectrum. Budgets are going toward more concrete business cases: entering new markets, launching new products, and modernizing the core.

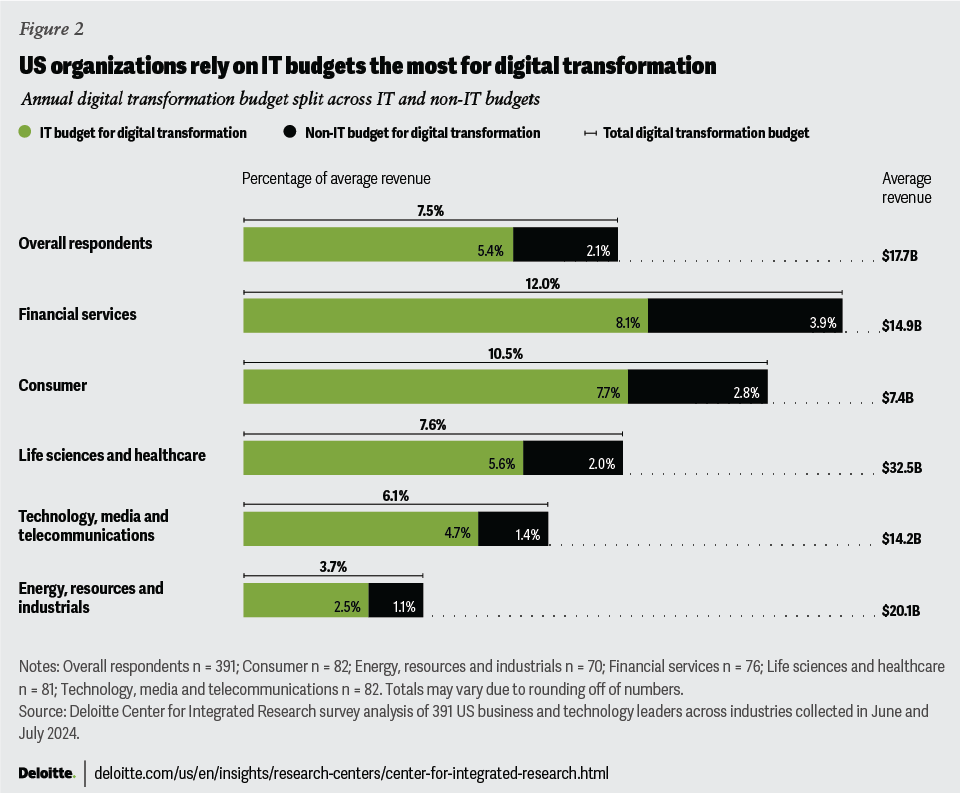

New to this year, we stepped back to get a big-picture view of the budget, from the relative size to who funds it. While not a comprehensive benchmark, this can serve as a proxy for the stakes of the transformation itself and who has the most on the line (figure 2).

On average, and across the spectrum, respondents are investing 7.5% of their revenue on digital transformation. Most of the budget comes from IT (5.4%), with the remainder from business functions like marketing, sales, and legal. These same dynamics apply across the five industries surveyed, with financial services respondents allocating the highest percentage to digital transformation.

Digital technologies are yielding higher value

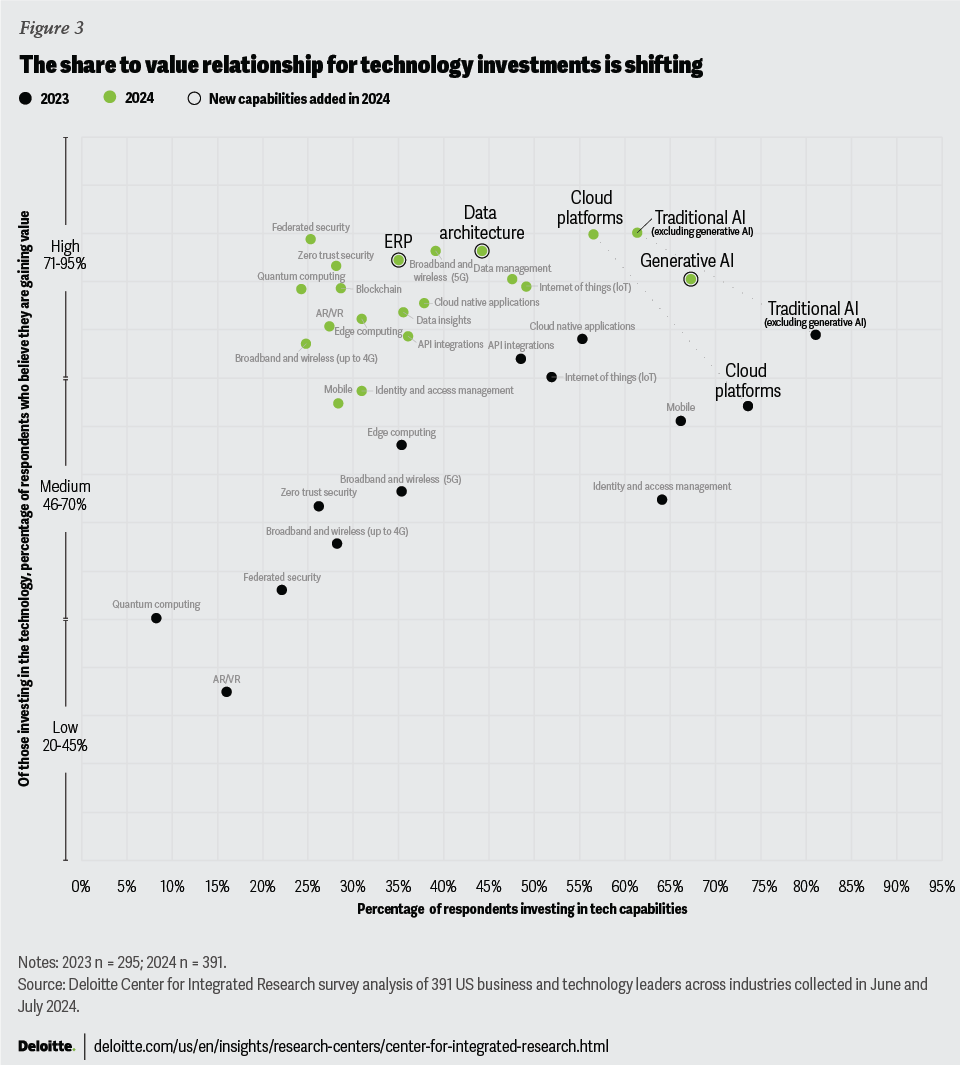

Last year, we surveyed across 21 technology investments. This year, we tracked the same with a few notable additions: data architecture, data insights, data management, generative artificial intelligence, enterprise resource planning, and blockchain (figure 3). Respondents were asked about both the extent of investment and the value gained for a given tech domain.

The investment portfolio for digital transformation technologies has shifted significantly. Whether due to new entrants, or capitalizing on foundations already built, notable trends emerge:

- The investment share: Seventy-three percent of technologies had fewer respondents investing in them. Their relative share decreased, likely due to fixed budgets, net new technologies (for example, gen AI), and new capabilities added for year-over-year tracking (for example, enterprise resource planning).

- The value potential: All technologies tracked in our survey were believed to drive higher value, gaining 16 percentage points on average. This logically supports the hypothesis that organizations may be getting more comfortable with digital transformation and their technology bets and would thus expect higher returns.

- The data estate: Forty percent of respondents are investing in the foundations for a robust data estate—data architecture, data management, and data insights. Fifty-seven percent invest in cloud platforms, whether as infrastructure or “full stack” solutions, and more than 60% in AI and gen AI. The question remains whether these investment priorities are in the right order. A gen AI solution is only as good as the data one curates. A proof of concept can only go into production if the foundations can scale.

- The cyber posture: Over the last year, cyber technologies like federated security, identity and access management, and zero trust have followed the same trend: investment share decreasing, value increasing. Cyber is an amalgam of multiple technologies and policies, so no one survey can capture all the investment dynamics. That said, the ultimate signal is how much these investments keep pace with broader digital transformation moves. As solutions bridge more operational and information technology, self-acting agents wash over platforms, and data is curated and governed at scale, new questions can emerge. What new attack surfaces and vulnerabilities open up? How much should cyber investments match or build ahead?

- The sector specifics: Certain technologies appear more targeted in their potential, at least for now. Blockchain and quantum computing fit that profile, with fewer than 30% of respondents investing, led by life sciences and health care for blockchain (42%); and technology, media, and telecommunications for quantum computing (32%). Diving deeper, they see real returns, with 76% of respondents gaining value in each, driven by energy, resources, and industrials (80%).

Digital journeys are getting harder for the unprepared

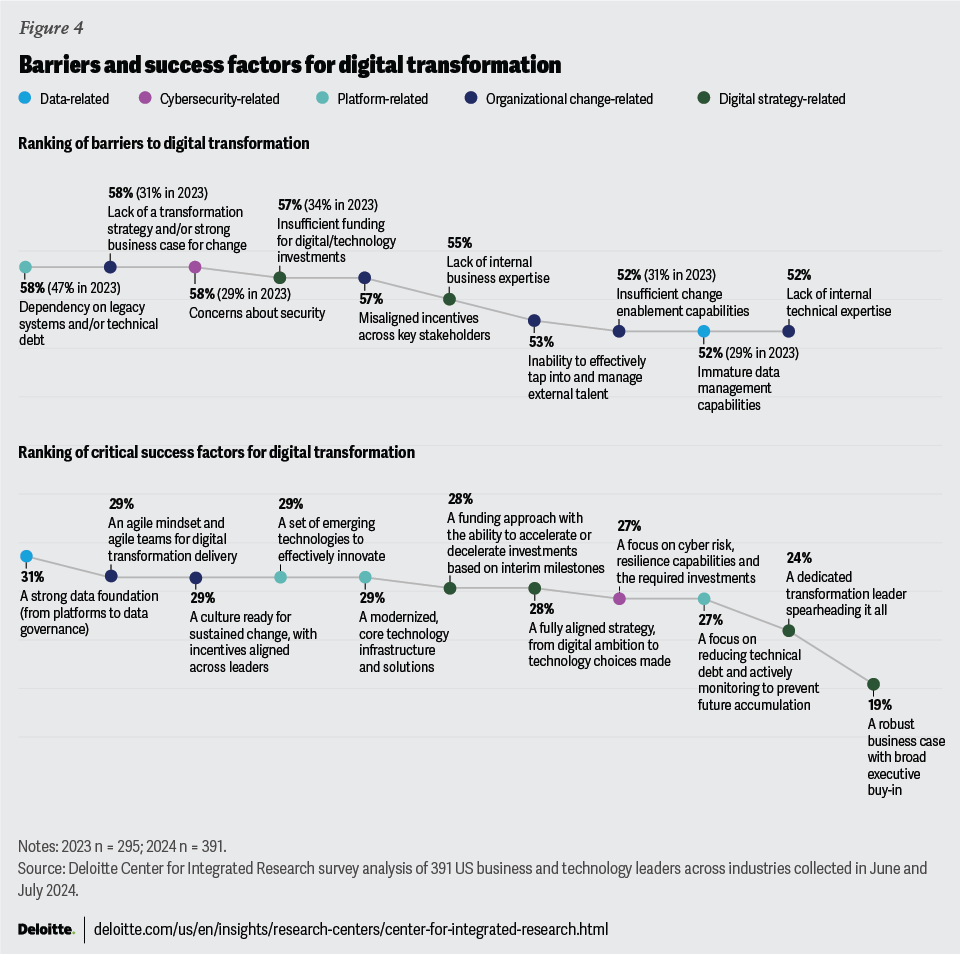

There’s no straight line to digital transformation success, even with a solid ambition, a ready enterprise, and a business case to match. Real challenges lurk and can get the best of any digital endeavor. Last year, we tracked six major barriers. This year, we enriched it all, with a focus on new constraints (figure 4).

Digital transformation barriers remain elevated, with many growing in intensity by at least 20 percentage points. Legacy systems and technical debt, the dominant constraint last year, is now on par with the lack of a transformation strategy and security concerns. Out of the new barriers, misaligned incentives rose to the top.

So how can one go beyond? We asked the inverse question: What contributed most to digital transformation success? (figure 4).

“Back to basics” wins again, with a strong data foundation at the top. But not far behind is a culture to sustain the change, and the willingness to pivot if the aspirations of the business case do not align with the reality under execution.

Shaping and sustaining is the name of the game

The 2024 index sets the stage for digital transformation leaders. Higher scrutiny on the moves, higher expectations on return on investment, and higher hurdles to overcome. What can be done to navigate it all?

- Rightsize the ambitions. Digital transformations should, by definition, go well beyond one business function or group. The impacts should as well, along with the mindset of finding value. This can mean forming a business case with metrics reaching across financial, customer, process, workforce, and purpose measures. We asked respondents how many of the 47 digital transformation key performance indicators (see Methodology) were leveraged to ascribe value or measure returns. Those using over 80% were 22 percentage points more likely to have gained value from their investments. There’s a well of untapped potential for any digital transformation.

- Pressure test the plan. There’s no absolute right way to undertake digital transformation. There are, though, warning signs of being on the wrong path. Leaders should ask the tough questions at the onset, during execution, or for any requests for top-up funding. Are we truly reinventing the enterprise? If so, do we have to? If not, should we? Do we have the foundations right? Do we understand the interconnected nature of chosen technologies? Are the common barriers surmountable? Gauge feasibility early and often.

- Reward the right behaviors. Stakeholders may stack hands at the beginning, but incentives may drift. Never underestimate the power of change management to understand stakeholder motivations, rewards, and propensity to stay for the journey. Misaligned incentives were identified as the second most important barrier to transformation. Make sure those involved are ready to adjust their teams’ goals (or their own) to keep it on track over months and years.

- Prepare to pivot. Agile tenets hold true, even in the face of digital transformations at scale. Building minimally viable solutions, failing fast, and fostering a culture of iterative learning can be paramount. This optionality, and ability to redirect capital in-flight, increases the odds that your digital transformation is built to last.

The clarion call is to think differently about digital transformation. The types and the technologies are known. The challenge is investing wisely in an ever-expanding tech estate to maximize and sustain the returns. The stakes ask for nothing less.

Methodology

Deloitte’s Center for Integrated Research surveyed nearly 400 US business and technology leaders from five commercial industries—consumer; energy, resources, and industrials; financial services; life sciences and health care; and technology, media, and telecommunications—in June and July 2024. Respondents were from organizations with annual revenue of US$500 million and above, including both public and private for-profit companies across the United States. The survey aimed to better understand how US commercial organizations have been navigating changes in the economic and tech environments as reflected by year-over-year changes in their IT priorities, digital budgets, and technology investment strategies.

Responses were compared with a similar sample from the 2023 Mapping Digital Transformation Value survey to understand what’s changed and where US respondents are reporting the most ROI from their technology investments.

Methodology for the index: Respondents using more than 80% of the KPIs (at least 38 or more KPIs out of 47) were classified as high measurement-focused group whereas respondents using below 80% of the KPIs (37 or less out of 47) were classified as moderate measurement-focused group.

{kind=link}

{kind=link}

{kind=link}

{kind=link}