The ‘bold change’ blueprint: Potential lessons from bold moves in mergers and acquisitions

Adjacent market M&A deals often show early promise as a foundation for bold change. But what approaches tend to pay off over the long term, and what can leaders learn from them?

Last year, in our publication “Behind the scenes of bold change,” we explored how and why some organizations are able to successfully enter into new sectors, industries, or entirely new business models, while others struggle to gain a foothold in a new area, lacking the ability to gain the support of both internal stakeholders and the market itself.

Given the breadth of bold change both in terms of scope and measurement, it can be difficult to define, prioritize, and quantify these all-encompassing initiatives. In this article, we focus our lens on one form of change that can help provide a clearer outward view of performance: a select set of “bold” merger and acquisition transactions that have the potential to fundamentally alter the course of an organization. Through this M&A–oriented lens, we can look for signals into potentially more universal lessons of what types of decision-making often lead to successful implementations of bold change—both inside and out of the realm of M&A.

What makes an M&A transaction “bold?”

At its core, any M&A transaction of note can impact an organization’s trajectory. However, some transactions carry—at least on paper—a bit more risk when companies step outside of their comfort zones by making substantial investments that can pave the way for them to enter new markets, acquire new skills or capabilities, and achieve greater efficiencies. These can be significant moments in a company’s history; a correct decision can lead to greater market share, profitability, and growth, while a wrong one can negatively impact the organization, possibly for years to come.

To explore this idea, we analyzed a sample of 321 M&A transactions from January of 2015 through March of 2023 that represent a significant deviation from business as usual for each of the relevant organizations (Methodology). Within these transactions, we identified three types of “bold” acquisitions to compare to one another and to the broader M&A market itself:

- Adjacent market deals: These transactions represent an organization that acquired a target from an adjacent market; for example, in 2016, technology company, Microsoft acquired the professional networking platform, LinkedIn.1

- Cross-industry deals: These are transactions where the buyer acquires a company in a completely different industry.2 In 2019, for example, biopharmaceutical company Merck acquired electronic materials company, Versum Materials, Inc., primarily for semiconductor and display production.3

- Large relative market capitalization deals: Within-market transactions where the buyer acquires a seller whose market capitalization is at least 50% of the buyer’s market cap. For example, in 2018, CareTech Holdings, a company that provides social care to children and young adults, acquired another healthcare company, Cambian Group, to expand its geographic footprint, at an acquisition cost of 96% of CareTech Holdings’ market cap at the time the deal was announced.4

While there are other types of bold M&A transactions taking place, these three transaction types enable us to clearly identify a variety of large-scale transactions (and importantly, may provide a helpful lens to other types of bold change).

Certainly, much can go into the behind-the-scenes success of an M&A deal that cannot be easily observed or measured, and success metrics can vary depending on the organization’s goals. For example, when we interviewed executives for our earlier analysis on bold change, we frequently heard that the success of many of these initiatives came down to a meticulous focus on leadership, culture, and funding over a multiyear time horizon.5

To complicate matters, short-term acceptance of change doesn’t always signal long-term success. For instance, an organization may experience a stock price bump at the onset of announcing a new product launch; flash forward three years, the product never takes hold in the market, and the only things left in its wake are excess inventory and debt—absent the benefits of increased revenue and profitability.

Still, when we dig into the most successful deals in terms of stock price change, we see two themes emerge that merit further exploration.6 First, while one might wonder if there are different risk-reward profiles among the bold play transactions, our sample consistently shows that adjacent deals significantly outperform the other transaction types over the first year. Second, time horizons matter; that is, when we expand our view to look at three years beyond a deal announcement, both the cross-industry and large relative market cap deals move from lagging the field to leap-frogging the broader sample of M&A deals. This could indicate that more resource-intensive transformations require more time to produce in the market.

Taken together, we see the benefits of bold moves tend to come with some important caveats that leaders may need to weigh when choosing a course for their organizations’ key change initiatives.

Adjacent M&As lead early results

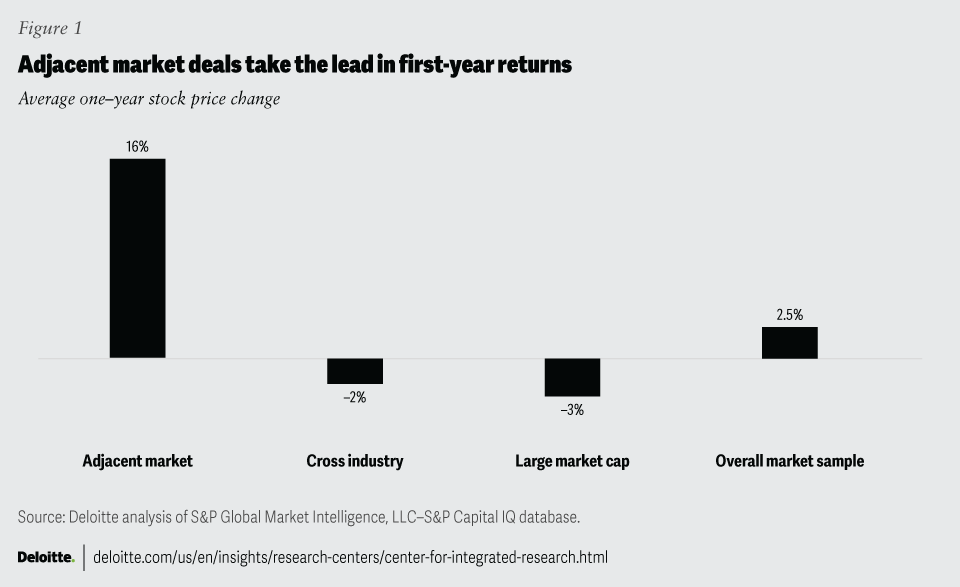

In our analysis, the adjacent market deals routinely outperform the other two bold deal types when comparing stock price changes over a one-year period (when testing statistical significance, the difference was significant at a 95% level of confidence).7 As seen in figure 1, while the adjacent deals average a 15.9% stock price increase, the cross-industry and large relative market cap deals both result in value erosion over the same time period (–2.1% and –3.0%, respectively). And adjacent deals also outperform other types of transactions, as the general sample of M&A deals averages 2.5% over the same time period.

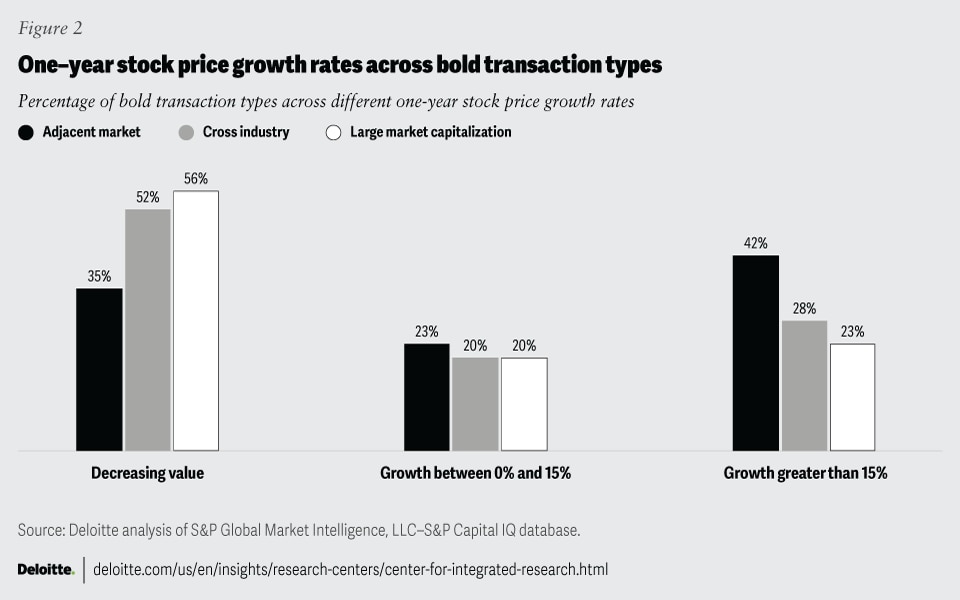

Given the relatively smaller sample of adjacent market transactions, it’s worth asking if just a handful of transactions are driving this difference in performance. However, when we look at the distribution of stock growth rates, we see these adjacent market deals have fewer instances of decreasing value over the one-year time frame and considerably more occurrences of growth rates exceeding 15% (figure 2). Interestingly, it’s the middle range of one-year growth rates between 0% and 15% where all three types of transactions produce similar frequencies of growth (that is, roughly 20% to 23% of all three bold transactions experience 0% to 15% growth). This may suggest the market doesn’t just view adjacent deals as less risky with lower floors; it also acknowledges the potential rewards of a higher ceiling after the first year than the other bold transactions.

Key takeaways

Zooming out beyond the realm of M&A, some leaders acknowledge entering adjacent markets of customers, talent, and capabilities as potentially powerful change catalysts.8 By expanding their lens and moving slightly out of their comfort zones, they look to adjacent capabilities as an effective means to creating and scaling ideas that closely align with their core culture and competencies.

Consider the earlier mention of Microsoft’s LinkedIn acquisition. At the time of the deal’s announcement, Microsoft stated their motivations for executing the transaction were to more effectively reach “LinkedIn’s massive user base and put Microsoft’s sales and distribution heft behind what was already the world’s largest and most successful social network.”9

In comparison, while cross-industry deals often seek a similar goal (that is, expanding into new realms of opportunity), there may be more inherent risk to effectively assimilating a greater set of unknown variables, such as understanding a completely new customer base or market. And while large relative market cap deals keep companies within their markets, the investments to acquire and unlock synergies are often more resource-intensive.10 This may signal that being bold does provide clear opportunities, but there is real value in starting with an assessment of where the organization’s strengths reside and seeking the adjacent areas of the business that empower the organization to more effectively capitalize on those strengths and competencies.

Weighing the present against the future

While delivering results in the first year of any transaction is important to establishing results and building credibility behind the decision-making,11 these bold initiatives almost certainly will be analyzed over a longer-term time horizon. For this reason, we also measured how these deals do over a three-year horizon.

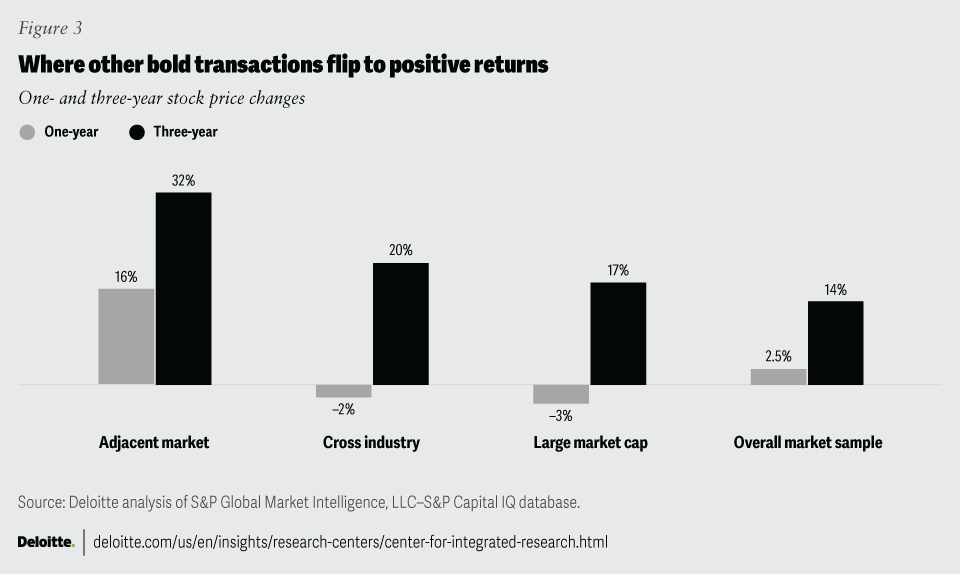

When afforded more time, all three bold transaction types outperformed the general sample of M&A deals. In fact, both the cross-industry and large relative market cap transactions experience a positive turnaround. Where both transaction types were negative in the first year, the cross-industry deals experienced a 20% increase in stock price over a three-year period, and similarly, the large relative market cap deals grew 17% (figure 3). This is especially interesting as these transactions leap-frogged the general sample of transactions, which still grew over that time frame (nearly 14%), but not to the degree of the two bold transactions analyzed.

Key takeaways

It’s likely a promising sign these other bold transactions eventually experience positive growth. For leaders weighing a multitude of potential paths to spurring real change, it’s an important reminder that some large-scale initiatives may need more time to yield positive results. It is also worth asking how much time the market—or various internal and external stakeholders—can afford to net the potential gains of an initiative before those stakeholder pressures push the organization in another direction.

Leaders interviewed in our first bold change study indicated that having a congruent, long-term vision of where the organization should head will likely be largely dictated by the stability of the leadership team.12 That doesn’t necessarily mean the same leadership team would be in place over a multiyear period, but rather that the vision and priorities of the organization would be successfully transitioned across multiple iterations of top leadership.

Bold change is rarely a one-off event, but rather a series of smaller decisions that will aggregate into real long-term change. Even the indisputable multibillion-dollar deal that could inevitably redefine the trajectory of an organization is not limited to the transaction alone; rather, it can serve as a jumping-off point to a massive change management journey. While the transaction itself may act as the catalyst for change, leaders will likely need to anchor decision-making to a strong vision to give these initiatives a chance to stand the test of time.

Reducing the friction points of bold change

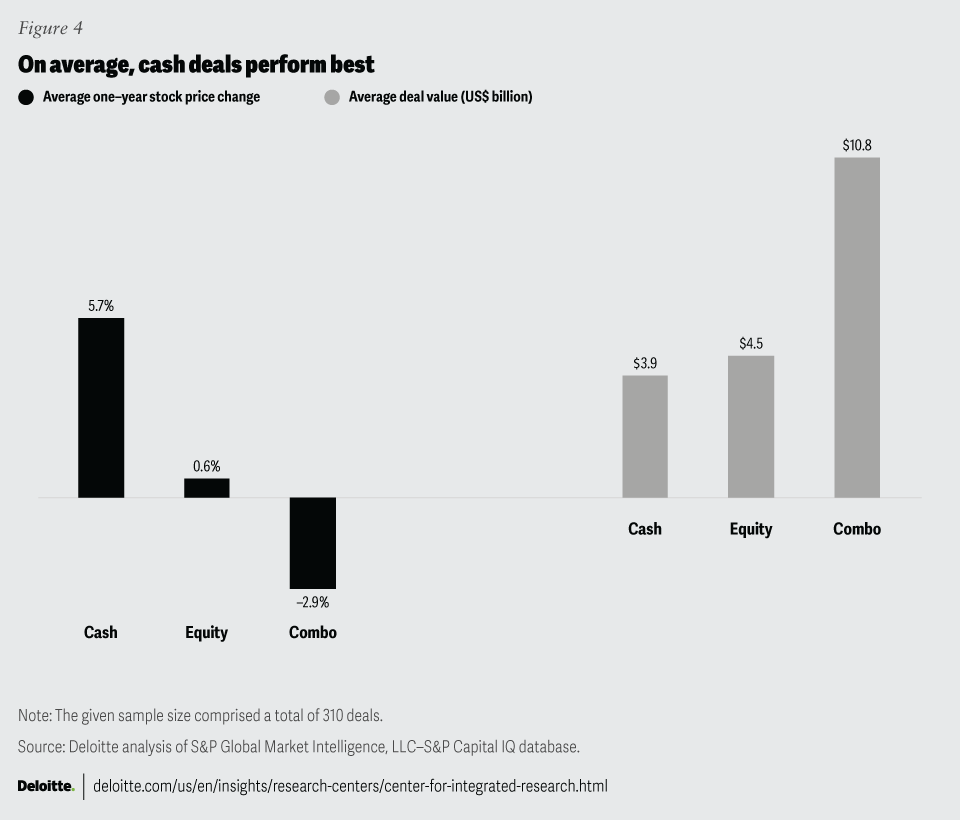

All-cash deals routinely and significantly tend to outperform all-stock and combination deals (mixed cash and stocks).13 This trend holds true for those bold transactions as well (figure 4). While cash deals average 5.7% growth over one year, equity deals average 0.6% and combination deals often see value erosion at –2.9%.

Of course, it’s unlikely companies can—or should—easily pivot to all-cash deals. However, the potential reasons that all-cash deals perform better on average may provide useful signals to those looking to enact substantial change on behalf of their organization. The lesson: In highly complex environments, like an M&A transaction or a massive change initiative, finding opportunities to remove points of friction and simplify the process can be powerful change catalysts.

Traditionally, all-cash transactions tend to be more straightforward and faster to execute than deals that involve equity, as they often present fewer regulatory and legal hurdles. In terms of control, they enable the buyer to retain full ownership without potentially conflicting with existing shareholders’ interests.14

For large-scale initiatives like these, funding with cash can create a more streamlined path to initiating and executing the change process since fewer new stakeholders potentially have a strong say in the future direction of the company. And as funding bold change often goes beyond a single transaction, reducing any friction points to implementation—and future funding requests—can create more autonomy for executing the longer-term vision.15

Paving a sustainable path to change

Given the long-term nature of change, it can be difficult to create a sustainable path to success. As we’ve seen through our M&A analysis, deals that seemingly falter in the shorter term may prove successful over the long run. With this in mind, consider the following ideas to help ensure your change journey is set up for sustainable success:

- Change initiatives can double as a tool for succession planning. Even the best leaders won’t be at an organization forever. However, the long-term nature of these initiatives can create an extended opportunity to develop future leaders for succession. Gaining the buy-in today from the next generation of leaders can increase the likelihood of a congruent vision for the future.

- Identify—and reinforce—your cultural strengths. Shared culture may be thought of as a signal of shared values—but it’s also a signal of shared strengths. Use the strengths that define your culture to help guide your bold change initiatives. Bold initiatives can act as a platform to amplify and extend what the organization does best.

Methodology

Using Capital IQ, we analyzed a series of M&A transactions to better understand if the “bold transactions” lead to notably different results, both in comparison to one another and relative to other general market transactions.

Sample background

We limited our sample through the following criteria.

- Deals between January 2015 and March 2023 were analyzed.

- The sample was limited to publicly traded companies (from global exchanges).

- Buyer’s annual revenue at the time of deal announcement was at least US$100 million (average annual revenue is US$11 billion).

- The deal size must total a minimum of US$10 million (the average deal size is US$2.4 billion).

- All deals must equal at least 3% of total market share for the buyer.

- Private equity deals were excluded from the analysis.

The above criteria generated a broader sample of 3,044 transactions. To hone our analysis further to identify the exceptional transactions we labeled “bold,” we classified three bold transaction types: adjacent market deals, cross-industry deals, and large relative market cap deals. Further, to ensure these three bold transaction types are truly unique, the buyer could not have made a similar purchase following any of the above criteria within two years of the deal analyzed, and they must have acquired at least a 90% stake in the target company. This resulted in 321 transactions fitting the bold criteria.

Success metrics

While measuring success can vary depending on goals and objectives, we limited our analysis to stock price changes both one and three years after deal announcement.16 Doing so provides a lens into market perceptions of company decisions and performance in both the medium and long term.

{kind=link}

{kind=link}

{kind=link}

{kind=link}