{kind=link}

{kind=link}

{kind=link}

{kind=link}

Globalization is here to stay has been saved

We thank Jim Kilpatrick and Bill Marquard for their contributions to this paper.

Cover image by: Pooja

After numerous shocks to the system, including a pandemic, a trade war between the world’s two largest countries, and rising geopolitical tensions, numerous analysts have suggested that globalization is in decline. That decline is expected to reverse the benefits of globalization that lifted millions out of poverty and to usher in a period of higher inflation and lower productivity growth. However, there is strong evidence to suggest that such a scenario will not come to pass.

Since globalization can be defined as the “growing interdependence of the world’s economies, cultures, and populations, brought about by cross-border trade in goods and services, technology, and flows of investment, people, and information,”1 deglobalization would be the unwinding of that interdependence. For the purposes of this article, we focus exclusively on the international trade in goods to show that:

Nonetheless, these findings are by no means a call to “inaction.” Rather, we conclude by proposing a number of important steps companies can take to mitigate the risks of future changes to globalization.

A narrative has emerged that asserts globalization peaked around the time of the global financial crisis of 2008. This assertion is used to claim that future deglobalization would merely be an extension or acceleration of the current trend.2 The problem is that the first assertion is not factual, which makes the second more tenuous.

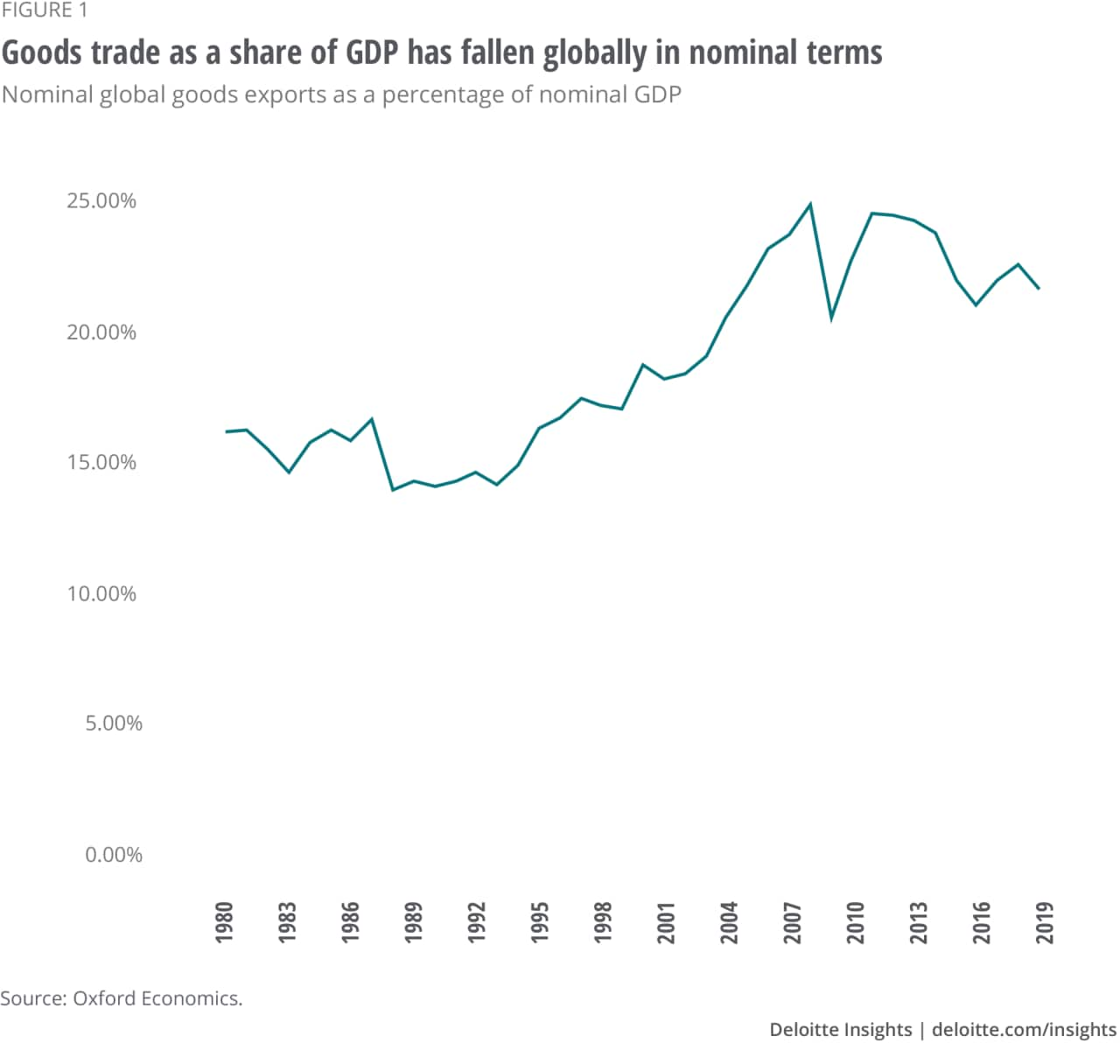

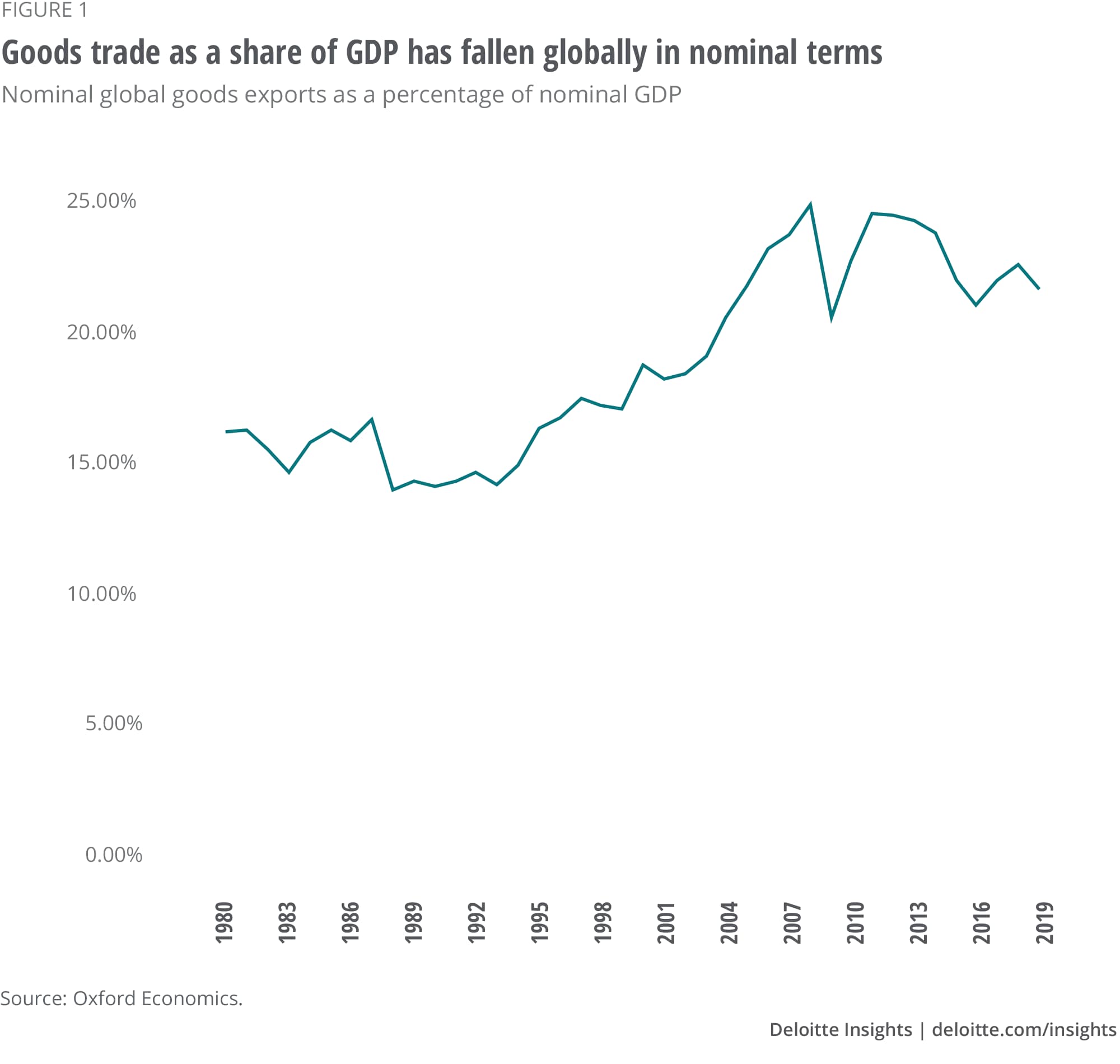

The claim that deglobalization has already begun is often based on the statistic that goods trade as a share of GDP has fallen globally in nominal terms3 (figure 1). Although that seems like compelling evidence of deglobalization, it misses a key understanding of what underpins those numbers. The commodity super-cycle—the dramatic rise and subsequent fall of commodity prices in the early 2000s—is what drove most,4 if not all, of the decline in goods trade as a share of GDP. Commodities play a much larger role in international trade than they do in overall GDP. Therefore, when commodity prices surge, the average price of traded goods rises faster than the average price of all goods and services produced (i.e., GDP) and vice versa.

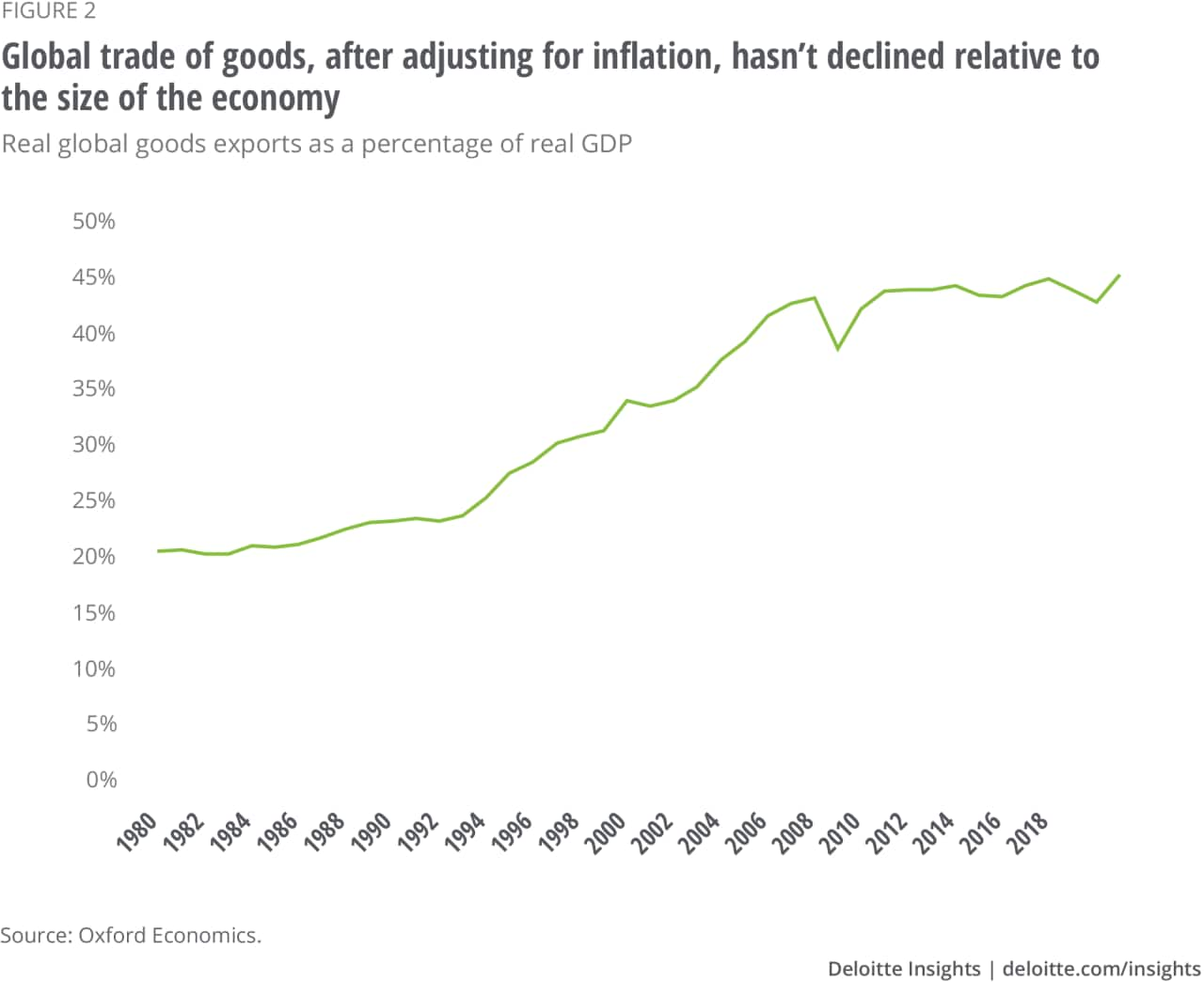

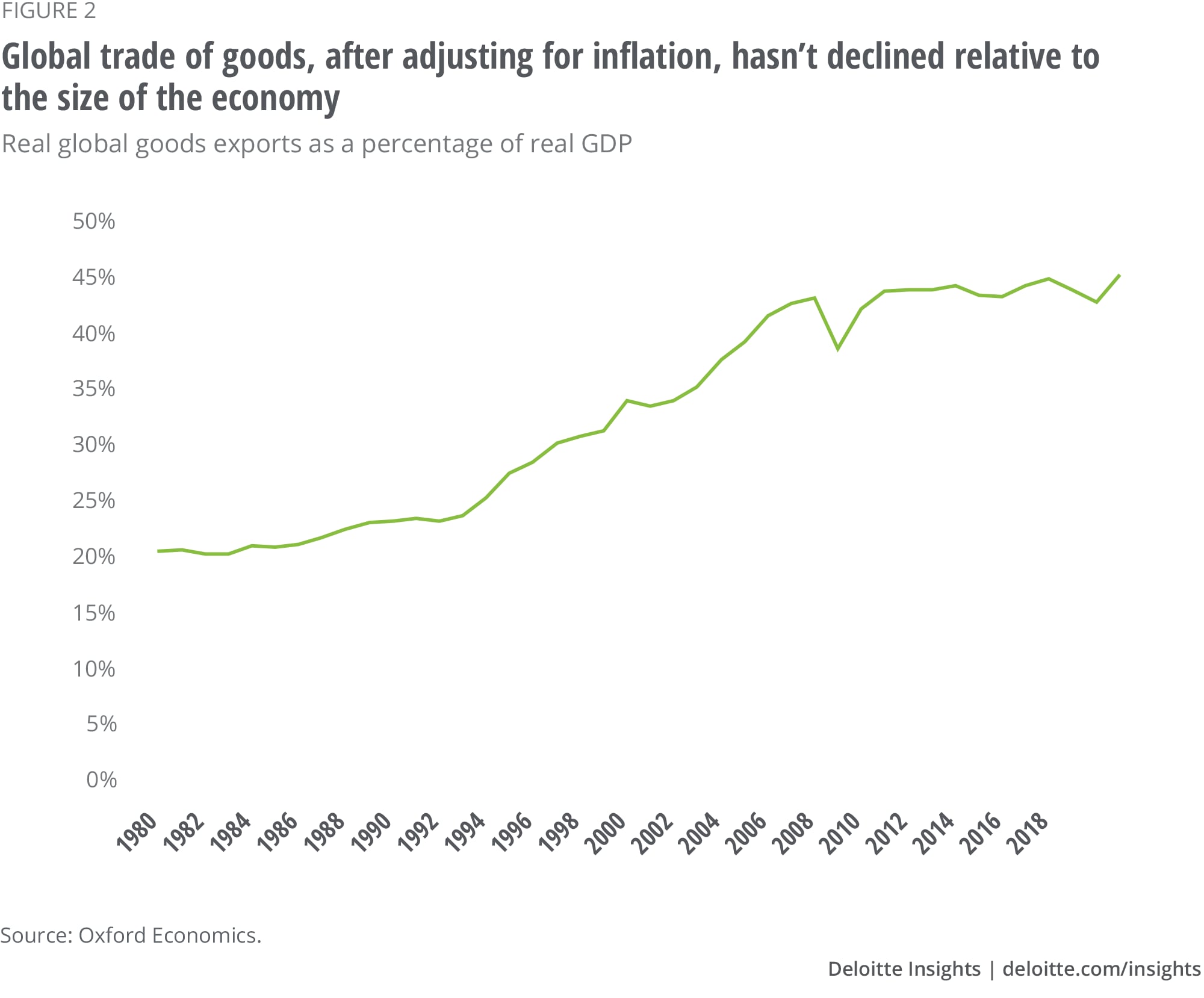

After adjusting for inflation, the picture looks quite different. Real goods trade as a share of real GDP has not declined (figure 2). However, it may have stopped rising around the time of the global financial crisis. Using different measures of inflation than the ones presented can yield slightly different results, but the overall conclusion is the same: There is little evidence to suggest that international trade of goods is in decline relative to the size of the economy.

Part of the reason is that a large share of global trade is immovable: Roughly 20% of international trade is in animals, vegetables, minerals, and fuels.5 Unless natural resource endowments suddenly change, it will be difficult to source these from domestic or even third-party sources. Producing goods near the source of their raw materials to minimize transportation costs would prevent more trade from relocating. Other parts of the supply chain are highly capital-intensive and require huge sums of investment, which would be difficult to abandon even under the direst of circumstances.

Even though deglobalization has not yet begun, shocks to trade could ultimately lead to such a trend. Looking at two recent shocks to global supply chains can help us better understand whether we are on the precipice of deglobalization. The first shock is the US-China trade war where substantial tariffs were raised on both sides. Looking at the US import side of the conflict, which is much larger in value terms, shows that the trade war shock did not result in deglobalization. Although the share of US imports from China declined by 3.8 percentage points since the start of the trade war,6 that production did not come back to the United States. Indeed, real US imports as a share of real US GDP continued to climb since the US-China trade war began,7 suggesting that the United States became less self-sufficient. A more detailed analysis from the Peterson Institute for International Economics shows how the drop in US imports from China were mostly replaced by imports from other countries.8

The second shock is the Fukushima disaster. When Japan was struck by an earthquake in 2011 and the powerful tsunami that followed, supply chains in and out of Japan broke down. Economists from the World Bank analyzed this event to show how trade changed as a result. They found little evidence that reshoring occurred, and for some manufacturing goods, internationalization actually intensified.9

The World Bank also found that companies with limited exposure to Japan did not adjust their supply chains, while companies with larger exposures typically moved some of their production to a third country. This finding fits neatly with economic models of supply chains, which show that the cost of keeping production in a high-risk country rises with the value of what is produced. For example, a company buying insurance to mitigate natural-disaster risk would see their insurance premiums rise with the value of the goods being insured. Therefore, companies with small exposures to a particular risk find that the sizable upfront costs of switching the supply chain, which can include building a new factory and establishing new relationships, outweighs the benefits of moving to a new country, even when such a move includes a reduction in insurance premiums.

Although previous shocks have not resulted in the reshoring of supply chains, some analysts10 have hypothesized that they should result in nearshoring. The rationale is that risks of disruption rise with the length of the supply chain. However, there is little evidence that this has occurred after previous trade shocks. In the World Bank study of international trade after the Fukushima disaster, the suppliers that were rerouted typically remained far from the importing country. For some goods, especially computer components, the supply chain lengthened. The one exception was finished autos, which because of their high transportation costs typically moved to a closer country.11

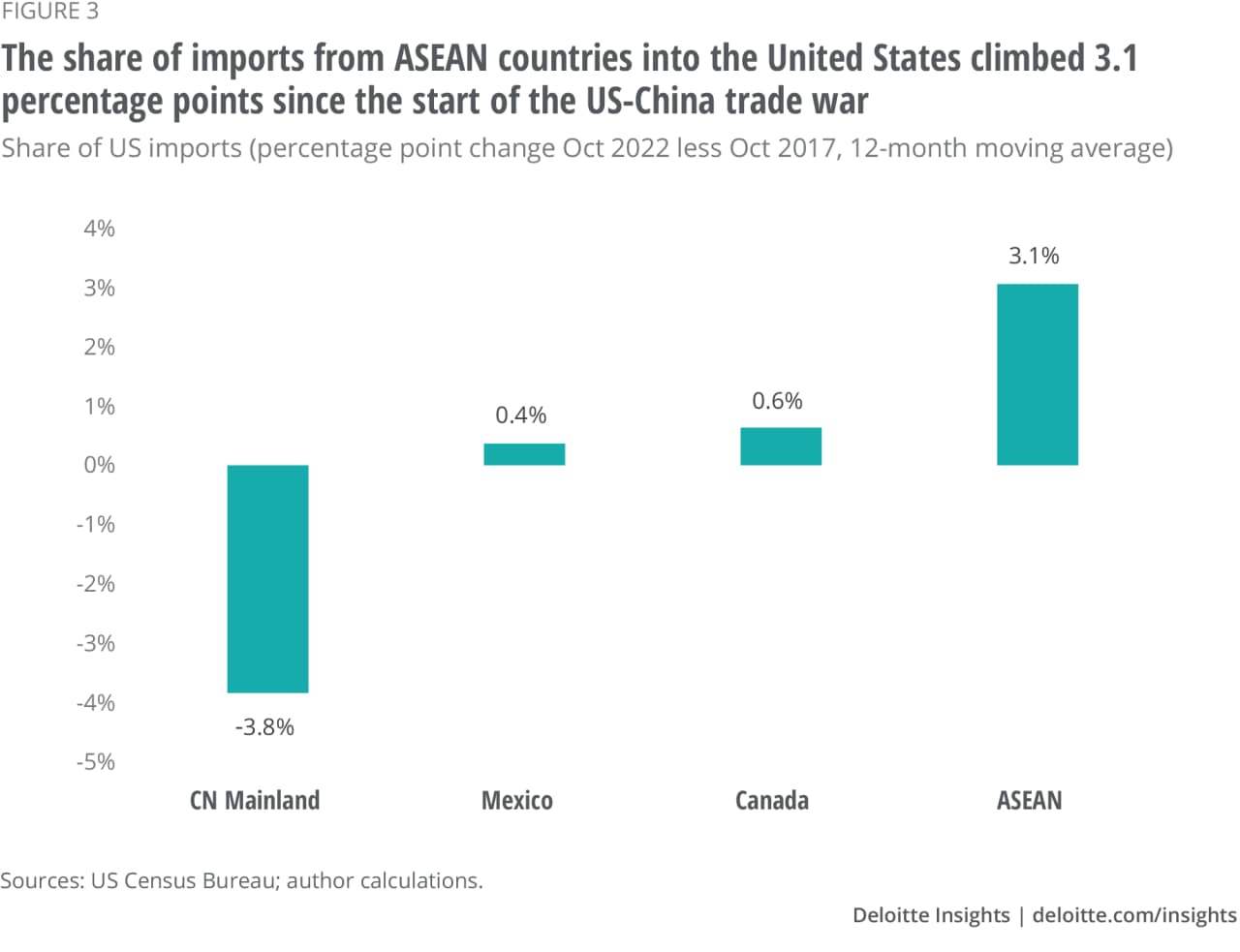

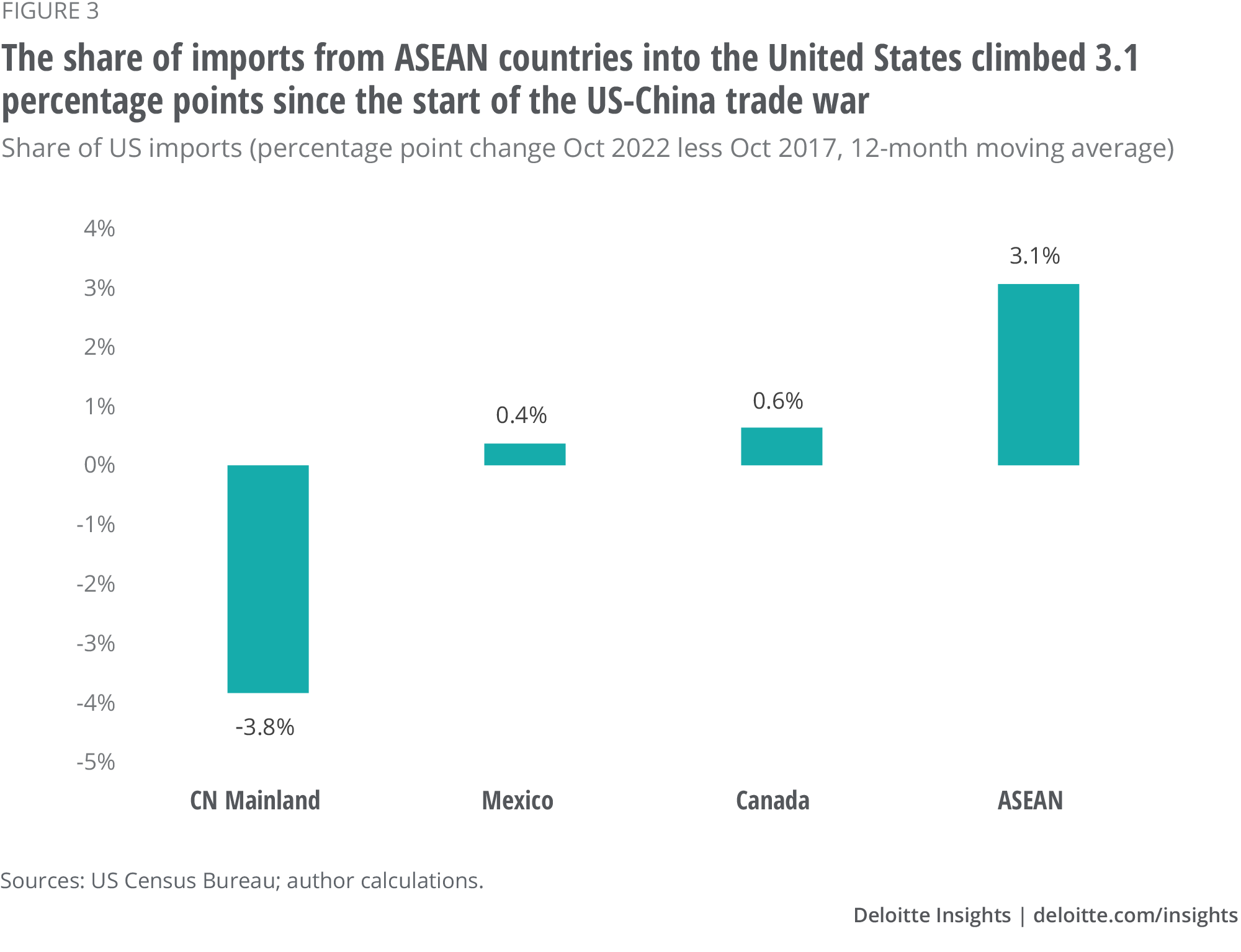

A similar finding occurs when examining the US-China trade war. While the share of imports from China fell after the trade war began, the share of imports coming from Mexico and Canada grew only modestly. Instead, the share of imports coming from ASEAN countries climbed 3.1 percentage points, which accounts for nearly 80% of the share lost by China12 (figure 3). Plus, nearshoring of supply chains does not necessarily reduce the risk of disruption. Russia’s invasion of Ukraine highlights the risks of Western European importers sourcing solely from Eastern Europe. Climate change and natural disasters will also affect large parts of the world, suggesting that concentrating production in one geography, even if close to final consumers, remains a risky proposition.

Historical evidence from the Fukushima disaster and the US-China trade war suggests that deglobalization has not begun and is not triggered by large disruptions to trade. However, that does not mean globalization will evolve the same way it did in the past. And how globalization ultimately evolves will determine the implications for the macroeconomic environment.

Proponents of deglobalization have said that the world will face higher inflation13 and lower productivity growth as a result. Their narrative suggests that the high cost of moving supply chains comes at the expense of deploying capital to more productive investment. Plus, a country’s comparative advantages will likely be overshadowed by its exposure to risks. This could raise inflation, lift interest rates, crowd out investment, and lower productivity growth. However, there are reasons to be optimistic that future changes to supply chains will not result in such a scenario.

The evolution of supply chains from here will depend on the risks at hand, the relative costs of mitigating those risks, and government policy. Given that risks in the current environment, which include climate change, geopolitical tensions, and a pandemic, affect numerous geographies simultaneously, adding redundancy to the supply chain is likely the best way to minimize those risks. However, redundancy will only be added incrementally given the sizable upfront costs associated with changing suppliers. Instead of scrapping production in a higher-risk area and losing out on the substantial investment that it required, additional production will likely be added in a lower-risk area as more capacity is needed.

In addition, the relatively large upfront costs of adding redundancy can be offset by lower variable costs such as those related to labor, tax, and the regulatory environment. This is particularly true for labor-intensive manufacturing in countries such as China that have seen a relatively recent rise in labor costs.14 This helps to explain why the production that moved out of China during the US-China trade war mostly went to low-cost southeast Asia rather than the more costly United States. The incremental nature of supply chain changes and the offsetting variable costs can help limit the inflationary impact supply chain changes will cause.

Even relatively large changes in supply chains may not have an inflationary effect. For example, China’s share of US furniture imports fell to 36% from 57% after the US-China trade war began.15 This sizable disruption did not seem to create price pressures for furniture. US import prices of furniture and related products from ASEAN countries, where most of the furniture production moved, grew by just 1.1% between January 2018 and January 2020,16 which is not a significant source of inflation.

The fact that supply chain changes have minimal triggers for inflation can also limit downsides to productivity growth. Without higher inflation from supply chain changes, central banks will be hesitant to raise rates, thereby preventing a crowding out of investment. Although substantial upfront costs used to move supply chains could limit investment in more productive uses and drag productivity as a result, efficiency gains can be made during this process. For example, switching to a new factory with the latest technological advancements should raise productivity.

From a country perspective, when labor-intensive production is moved from a middle-income country to a low-income country, productivity growth may improve in both locations. The middle-income country can focus on higher-productivity economic activities in line with their development stage, while the low-income country gets a chance to develop its manufacturing capability, increasing productivity growth there as well. Such a shift raises living standards in both places.

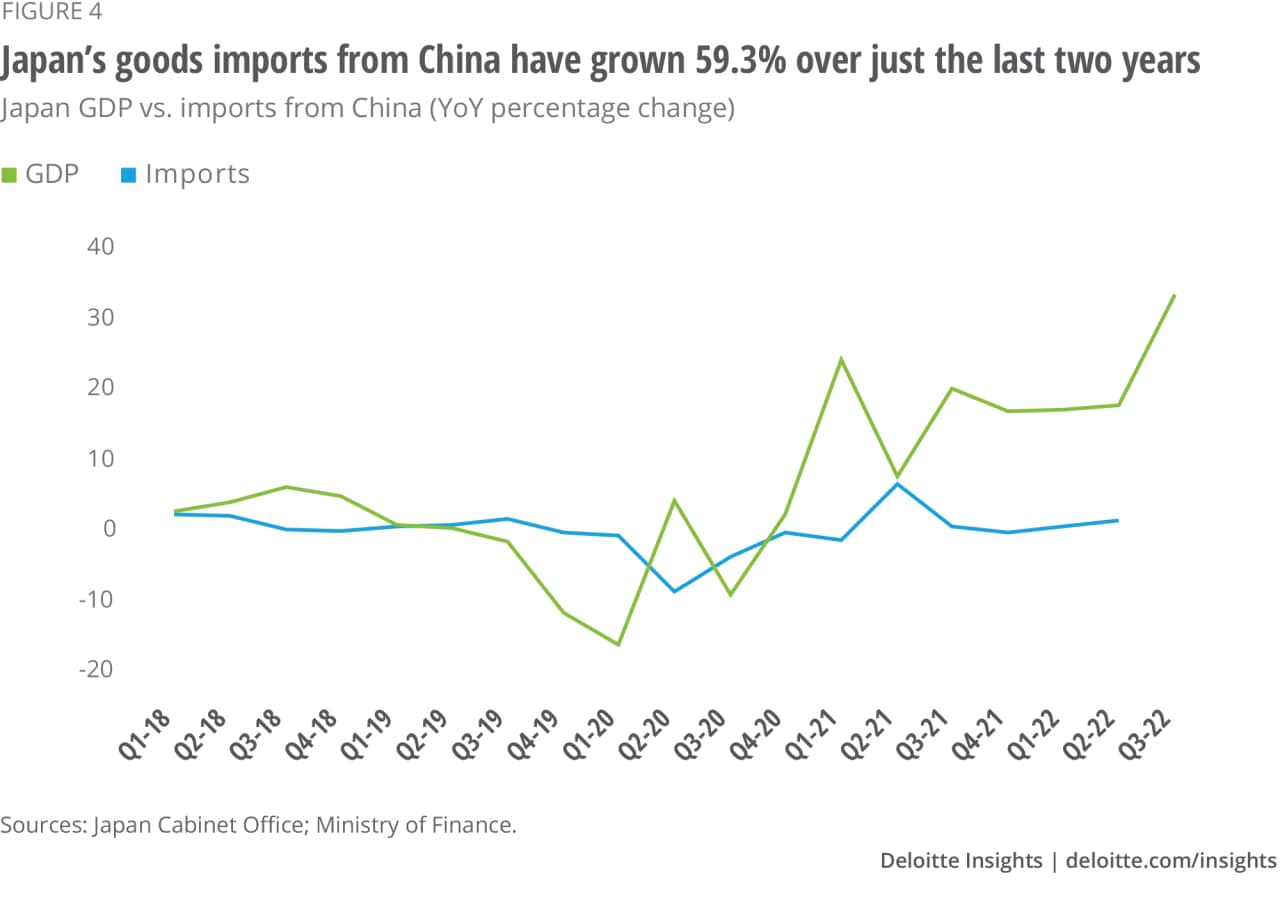

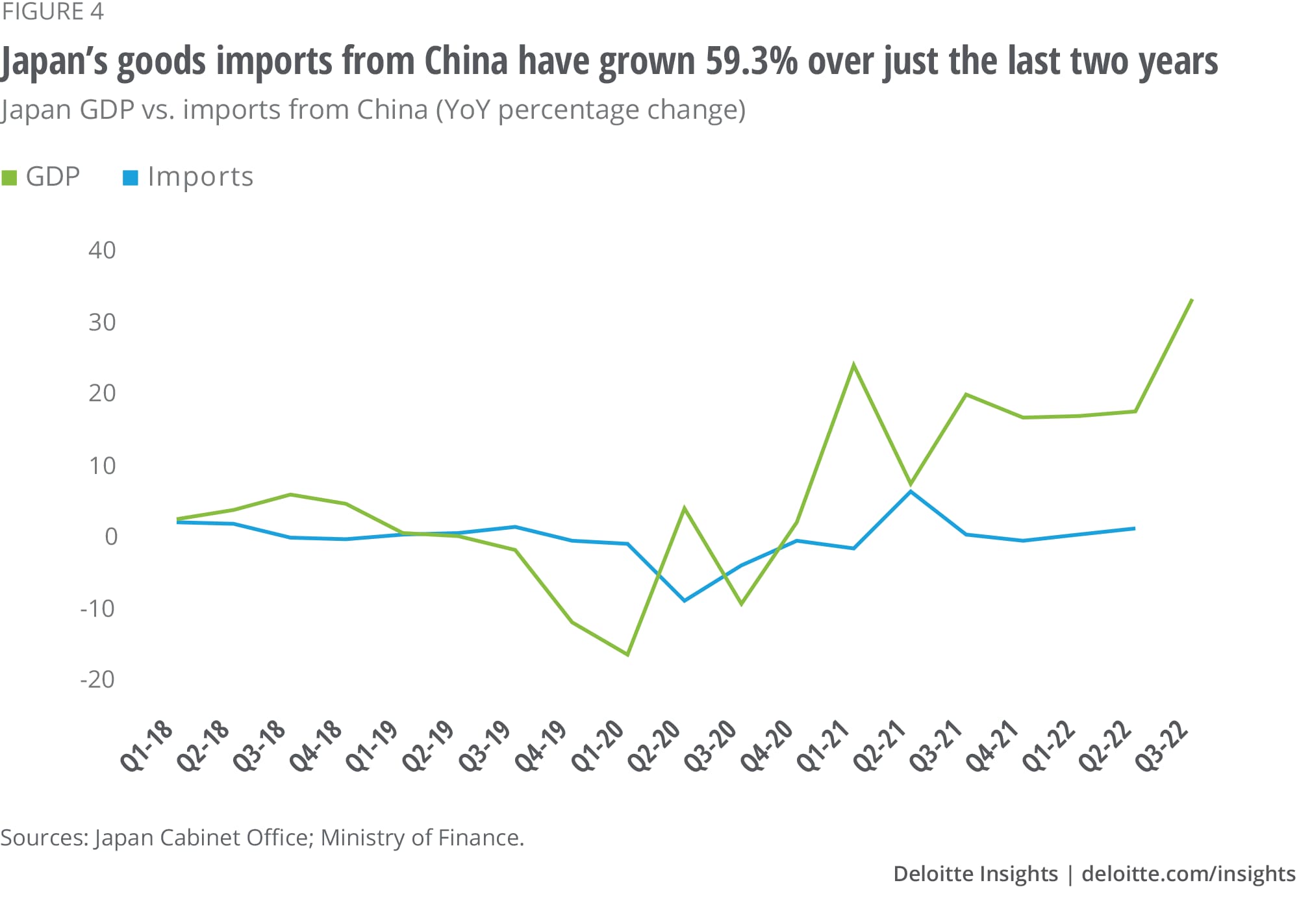

Government policies have the potential to alter the future of globalization. Already, numerous countries have offered incentives to add resilience to their supply chains, many of which encourage reshoring production. For example, Japan provided subsidies to reshore or nearshore production of critical goods away from China in the wake of the pandemic.17 Although these policies were taken up and may affect some specific sourcing, they remain too small to affect broader supply chains beyond the margins. After all, Japan’s goods imports from China have grown 44.1% over the last three years, which suggests the policy did not reduce trade flows from China (figure 4).18 Plus, such subsidies can be expensive, making it an unattractive policy tool for non-critical goods.

Other policies could have a larger effect than subsidies and incentives. Export controls from the United States that have extraterritorial reach, such as the foreign direct product rule, could materially affect supply chain organization. Such policies primarily affect goods that could be used for military purposes abroad, but they could theoretically be expanded to cover a much broader set of goods. The affected goods will likely see some “friend-shoring” where supply chains run primarily through allied countries. However, these policies can have a sizable negative effect on domestic businesses,19 which makes the expansion of such rules difficult to implement in democracies.

Historical evidence and cost-benefit analyses suggest that deglobalization is not upon us. International trade will continue, though it is likely to change and face ongoing risks. Remaining cautious when making changes to the supply chain is crucial:

Reducing supply chain risk does not necessarily need to come with huge upfront costs:

Once there is some physical redundancy in the supply chain, using it effectively is imperative:

Peterson Institute for International Economics (PIIE), What is globalization?, October 29, 2018.

View in ArticleDouglas A. Irwin, “The pandemic adds momentum to the deglobalization trend,” PIIE, April 23, 2020.

View in ArticleIbid.

View in ArticleRichard Baldwin, “The peak globalization myth: Part 2—Why the goods trade ratio declined,” VoxEU, September 1, 2022.

View in ArticleWorld Integrated Trade Solution, “Product imports, by country and region in US$ thousand 2019,” accessed December 2, 2022.

View in ArticleAuthor calculations using US Census Bureau data.

View in ArticleAuthor calculations using Oxford Economics data.

View in ArticleChad P. Brown, “Four years into the trade war, are the US and China decoupling?,” PIIE, October 20, 2022.

View in ArticleCaroline Freund et al., Natural disasters and the reshaping of global value chains, World Bank Group, June 2021.

View in ArticlePaolo Barbieri et al., “What can we learn about reshoring after COVID-19,” Operations Management Research 13 (2020): pp. 131–136.

View in ArticleIbid.

View in ArticleAuthor calculations using Census Bureau data.

View in ArticleDambisa Moyo, “Why deglobalization makes US inflation worse,” Project Syndicate, October 7, 2022.

View in ArticleSophia Yan, “‘Made in China’ isn’t so cheap anymore, and that could spell headache for Beijing,” CNBC, February 27, 2017.

View in ArticleChad P. Brown, “Four years into the trade war, are the US and China decoupling?"

View in ArticleAuthor calculations using US Bureau of Labor Statistics data.

View in ArticleShino Watanabe, “Japan’s initiatives to secure supply chains and its key challenges,” Italian Institute for International Political Studies, March 17, 2022.

View in ArticleAuthor calculations using Japan Ministry of Finance data.

View in ArticleReuters, “LAM research warns of up to $2.5 bln revenue hit from U.S. curbs on China exports,” Financial Post, October 19, 2022.

View in ArticleWe thank Jim Kilpatrick and Bill Marquard for their contributions to this paper.

Cover image by: Pooja