South Africa economic outlook, November 2023

Struggles with a power, logistics, and growth crisis has impacted South Africa’s public purse. The economy’s medium-term outlook remains dim but vital reforms are gaining traction.

After the euphoria and celebrations of the Springbok Rugby team bringing home the Webb Ellis cup for the fourth time, South Africans were sobered by reality on Nov. 1, 2023, when finance minister Enoch Godongwana delivered the 2023 Medium Term Budget Policy Statement (MTBPS). As many expected, a domestic economy weakened by electricity and rail capacity constraints, coupled with the challenges of a slower and uncertain global environment, has delivered unfavorable news for South Africa’s public finances.

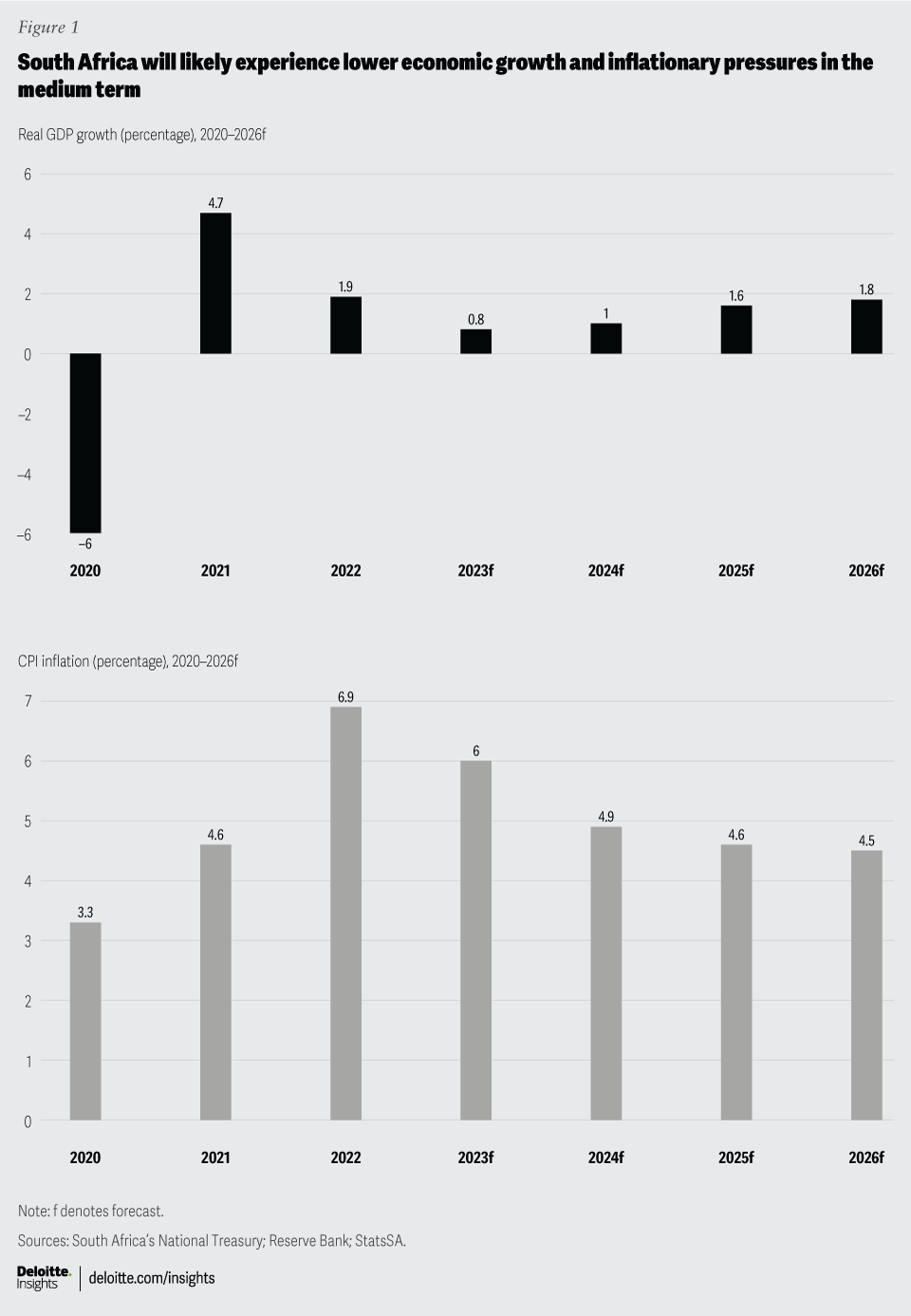

South Africa’s National Treasury revised down the country’s growth outlook from 0.9% for 2023 (as per its estimate in February 2023) to 0.8%.1 This figure remains slightly higher than the growth expectation of many analysts and commentators. Also, the growth outlook for the coming years has been revised downwards—from 1.5% in 2024 to 1%, and 1.8% in 2025 to 1.6%; and now it is expected to average only 1.4% over the 2024 to 2026 period.2 This does not compare well with the 4% projection for emerging and developing economies, and notably even falls below advanced economies’ growth outlook of 1.7% over the same three year period, as projected by the International Monetary Fund (IMF).3

This is driven in part by lower household expenditure. Households continue to struggle with finances in an environment of high interest rates, elevated inflation, particularly food and fuel inflation, the impacts of loadshedding on the cost of living, lower real disposable incomes, and higher household debt. While some measures of consumer confidence, including Deloitte‘s ConsumerSignals,4 show some signs of recovering confidence, the increased willingness of consumers to spend is not matched by households’ financial health and ability to spend.

Almost half of the consumers surveyed in Deloitte’s September 2023 Food Frugality Index said they were engaging in at least three “frugal behaviours” to make ends meet, making South Africa the country with the highest frugality among 14 countries surveyed by Deloitte. Consumers have been making trade-offs, such as opting for lower-cost meats or ingredients, and economizing by reducing food waste and focusing on only buying essentials due to their financial struggles and affordability concerns.5 Retail sales figures have fallen for nine consecutive months up to August 2023.6

{kind=link}

Yet, South Africa’s headline inflation has moderated to 6.2% year over year (YoY) in the first quarter of 2023, from a peak of 7.63% YoY in Q3 2022.7 At the time of writing, the latest inflation print for September 2023 showed an increase to 5.4%, from 4.8% in August 2023, with the key contributors being food, housing and utilities, and transport, placing upward pressure on annual inflation.8

While upside risks to headline inflation exist (uptick in global oil prices’ impact on fuel prices, El Nino effect driving higher food prices, etc.), inflation expectations have recently declined. According to the Bureau of Economic Research (BER) that surveys business, labor, and analysts, the third quarter of 2023 reading of inflation expectations saw “the first drop in average 2023 expectations in two years”.9

Still, headline inflation is expected to come in at the upper end of the 3 to 6% of the inflation targeting band in 2023. But the South African Reserve Bank could keep rates high for longer, and even squeeze in another rate hike in November 2023. In its Monetary Policy Review released in October, headline inflation is expected to average 5.9% in 2023, and is likely to only near the midpoint of 4.5% of the inflation target range in 2025,10 given the above risks but also higher for longer rates in developed markets.

This is a concern not just for households but also businesses. Despite an uptick in business confidence in the third quarter of 2023–the first since the first quarter of 2022–business confidence remains low. Businesses are faced with a challenging local environment including high costs of doing business, high lending rates, loadshedding, freight and logistics constraints, policy uncertainty, among other things. In Deloitte’s pilot South Africa CFO Survey, released in June 2023, loadshedding, the poor domestic economic outlook, political and policy uncertainty, currency fluctuations as well as geopolitical risks were seen as the most pressing business risks for the year ahead.11

Tight lending conditions and high inflation have dampened or postponed investment and hiring decisions, with findings from leading CFOs surveyed showing that companies are more likely to make capital investments than hire more staff.12 Businesses have indeed increased their investments, largely driven by energy-related investments such as self-generation projects to deal with loadshedding. Private sector investment spending has driven up gross-fixed capital formation to 6% year-on-year in the first quarter of 2023.13 This, in turn, has boosted the construction sector, which has been underperforming for years, but helped drive growth in the first half of the year. While smaller in scale compared to private investment, public sector capital spending has also supported overall investment.14

One of the top performing sectors has been agriculture, with a year-on-year expansion of 8.2% in H1, on the back of good rainfall.15 The sector is poised for further growth, it still needs to address risks related to climate, logistics, and broader market access. Relatively good performance has also come from sectors such as tourism and finance.16

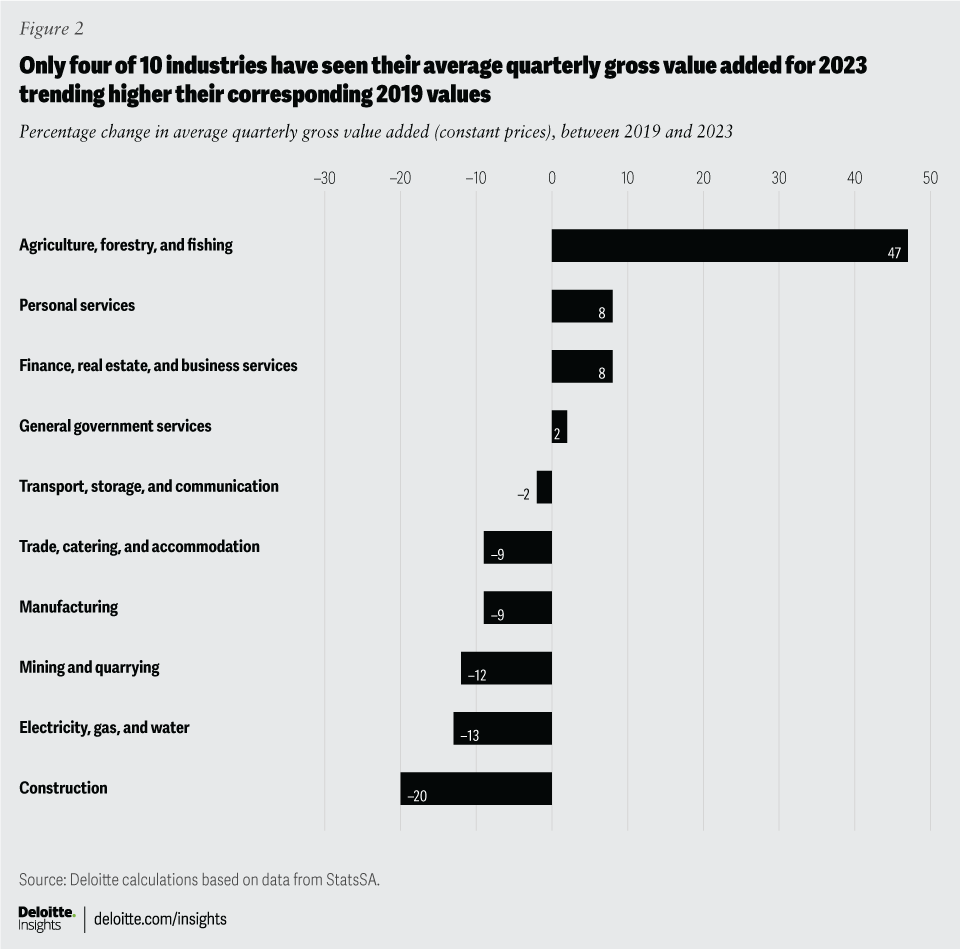

Manufacturing and mining have faced more challenging circumstances, due to ongoing electricity shortages, weaker freight and logistics capacity, and–in the case of mining–lower commodity prices. Manufacturing and mining are among the six industries (the others are electricity, construction, trade, and transport) that are still trending below their 2019 levels of gross value added (GVA), largely due to the noted supply-side constraints within network industries (figure 2).17

{kind=link}

A slower local economy (and sector-specific woes such as in mining) have given rise to lower than anticipated tax receipts, specifically lower corporate income tax collections. A sizable shortfall of R56.8 billion in tax revenue collection in this fiscal year (2023/24), and a further R121.4 billion over the next two fiscal years is expected, in comparison to the 2023 Budget.18 Tax revenue overruns seen in previous years from mining companies are unlikely due to lower commodity prices given slower growth in China.

In response to the noted shortfall–pre-MTBPS National Treasury already issued cost containment guidelines to government departments–the Minister also announced a downward revision in spending, by R21 billion. A further R133 billion in spending cuts has been tabled for the next two fiscal years.19 Adjustments have been made to prioritize the social wage, spending on health and education, as well as social protection (e.g., extending the COVID-19 Social Relief of Distress grant).20

Overall, public finances have weakened. An increase in the budget deficit to 4.9% of GDP is now projected, up from 4% estimated in February 2023. This means that gross debt is expected to rise from R4.8 trillion in 2023/24 to R5.2 trillion in 2024/25, exceeding R6 trillion in 2025/26 when gross debt is expected to stabilize at a high of 77.7% of GDP. This compares unfavourably to the Budget 2023, which projected stability at 73.6% that year.21 With rising financing needs being met through debt financing, this also sees debt-service costs increase: debt-service costs, as a share of revenue, are expected to increase from about 18% to 22.1% in 2026/27 and are the second fastest growing expenditure item over the medium-term period to 2026/27, after learning and culture.22

As National Treasury looks to stabilize the public purse, key action items to unlock much needed growth and in turn address many social and development woes the country faces were tabled by the minister. For one, Treasury has maintained a position of pursuing fiscal policy that is in support of stabilizing debt and fast-rising debt-service costs. The latter are quickly crowding out other spending areas, including social spending. At the same time, taking on new debt has become much more expensive. While this will not directly improve the growth outlook, it can unlock targeted social spending and public investment, maintain macroeconomic stability by lowering fiscal and economic risks, and build investor confidence.

A second action point tabled by Treasury is a focus on improving the efficiency of spending public resources. This includes reviewing the structure and size of the state, in line with President Cyril Ramaphosa’s State of the Nation Address commitment. Among other things, it looks to address executive remuneration, and importantly redundancy and overlapping mandates of state portfolios by rationalizing departments and programs over the next three years. This requires reviewing state capacity and capabilities, while eliminating corruption and wasteful expenditure.

As a third key action item, and one of the most significant focus areas in the medium term, will be unlocking investment in infrastructure to stimulate economic growth. Developing countries that have allocated about 30% of their GDP to infrastructure development have also been among the fastest growing economies.23 South Africa’s National Development Plan, published in 2012, had aims to achieve gross fixed capital formation (GFCF) spending of 30% of GDP by 2030, with public sector investment being a third of that.24 But South Africa’s investment in infrastructure has averaged about half of this 30% target since 2012, with underinvestment in sectors such as energy, transport, and water having led to a state of emergency in the case of electricity and logistics. The MTBPS emphasizes the commitment of the government to enhance infrastructure delivery, through upping both quantity and quality thereof. This includes crowding in more private sector financing for larger projects, through creating coinvesting mechanisms and implementing recommendations as per the public-private partnership framework (PPP) review. This will also involve the establishment of an agency to support finance and implementation of infrastructure.

Last, and most importantly, is the Treasury’s commitment to continued progress on structural economic reforms, specifically where these are most urgent, namely, in the electricity and logistics sectors. The economic costs of failure and inefficiency in these sectors have mounted over the past year, in part due to the lack of investment in deteriorating infrastructure, but in part also due to mismanagement, corruption, and even theft. Rolling blackouts last year are estimated to have cost the country between R400 billion and R600 billion; and 14 years of systemic power failures are estimated to have cost the country over R3 trillion.25 Rail underperformance is estimated to have cost the country about 5% of GDP in 2022.26 Port inefficiencies add further costs and delays, and South Africa’s ports rank as the poorest performers globally in this regard. Reforms in the electricity sector (including lower restrictions on self-generation, and reforms to encourage private investment) are expected to add over 11GW of renewable sources to help curb the power crisis in the medium term. Record levels of loadshedding in 2023 are expected to give way to an improved electricity system together with sizable private investment that will curb power cuts. And the scale of the crisis in the logistics sector warrants industrywide reforms.

The good news is that the crises in both sectors have prompted long overdue, holistic reforms that will be critical to get the economy back on course toward sustained, inclusive, and long-term growth. The bad news is numerous risks to a more favorable economic outlook still exist and addressing these in isolation will not suffice.