{kind=link}

{kind=link}

{kind=link}

Trouble ahead for the housing sector? has been saved

Cover art by: Sylvia Yoon Chang

During the pandemic, the US government took rather extraordinary steps to safeguard homeowners and renters. Among its many provisions, the March 2020 CARES Act expanded access to mortgage forbearance, allowing homeowners to defer payments without any credit score consequences. Further, beginning as early as March 2020, some states put eviction moratoriums in place with the CDC, following that with a national eviction moratorium in September 2020. Finally, an Emergency Rental Assistance Program was put into place in December 2020 and expanded in March 2021, with a total of US$46.55 billion appropriated for support.

However, some of this house sector support will expire soon. The enrollment window for the mortgage forbearance program is set to close at the end of this month.1 The national eviction moratorium was originally set to expire last December, but it was extended several times before the latest extension was vacated by the Supreme Court in August.2 However, some state and local moratoriums remain in place. The last major backstop, the funds allocated to the Emergency Rental Assistance Program, were allocated to the states, but they are only now beginning to disburse the funds.

Given the large number of tenants behind on their rent, there is little doubt that the end of eviction moratoriums will result in a spike in evictions in coming months. However, what is less appreciated is how rental evictions might cause mortgage delinquencies and foreclosures to also rise, compounding the rise in foreclosures from those who are not able to pick up their mortgage payments when forbearance ends. Without the backstop of the pandemic mortgage forbearance program, the resources of the Emergency Rental Assistance Program will become essential to providing stability to both renters and property owners.

Between March 2020 and June 2021, 9.3 million mortgage holders took advantage of the opportunity to skip some mortgage payments under the forbearance, with the peak occurring early in the pandemic in May 2020, when close to 2.5 million mortgages entered forbearance. However, just under 2 million mortgages, or only 21% of the total, remained in forbearance at the end of June 2021.3 Mortgage forbearance made a measurable impact on mortgage delinquency rates as mortgages that are granted forbearance are not recorded as delinquent. The forbearance program has therefore been instrumental in keeping number of foreclosures at record lows since its inception.4

While the forbearance option has reduced delinquencies and foreclosures and preserved credit ratings, the shift in the composition of those in forbearance may cause problems going forward as the pool has become more heavily weighted toward subprime borrowers, i.e., those with a credit score less than 620. As of June, subprime borrowers made up 39% of those in forbearance, substantially higher than their 18% share of the overall share of mortgages and up from their share of the forbearance pool a year ago, when they were 26% of the pool total.5 As noted in a Federal Reserve Bank of New York study, “Looking forward, those borrowers remaining in forbearance are the borrowers that will be most likely to struggle when these policies are lifted. Federally backed mortgages are eligible for up to eighteen months of forbearance, depending on when the initial forbearances started. With this limit in effect, many of the borrowers remaining in forbearance will face the limits of this leniency in the coming 3–4 months, when they must either resume payment or will be pressured to sell their homes to avoid delinquencies and consequent foreclosures.”6

Depending on how many of those still in forbearance status ultimately end up in foreclosure, the impact could be sizable. For example, if all the subprime mortgage holders currently in forbearance were to end up in foreclosure, that would be just under 780,000 foreclosures. Although certainly not anywhere near the levels of foreclosures seen during the global financial crisis, when the number topped 2.8 million in both 2009 and 2010, it could contribute to a sizeable rise over the 493,000 foreclosures that occurred in 2019.7

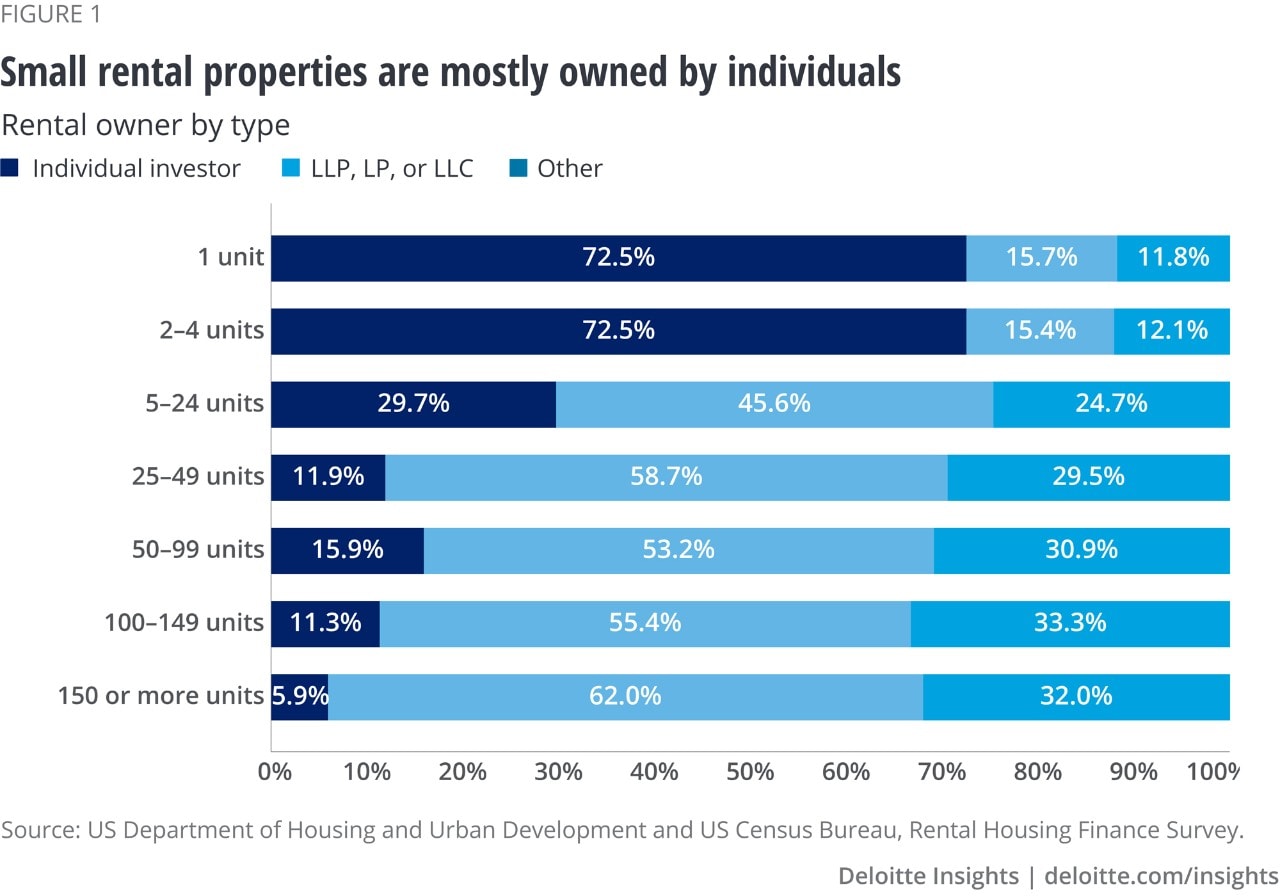

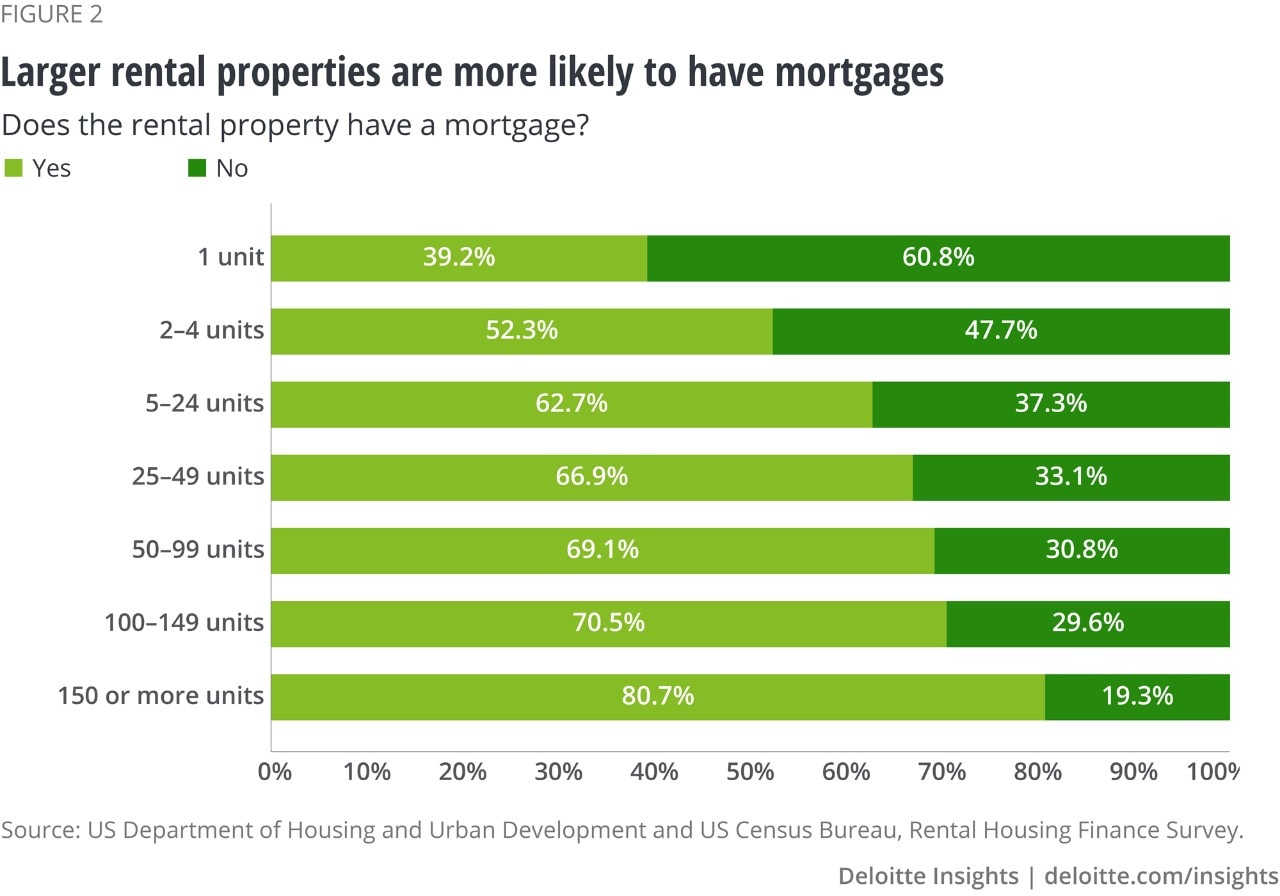

Another possible concern related to the end of pandemic mortgage forbearance is very much tied to the end of the other housing-related support, the eviction moratorium. In 2018 (the most recent ownership data available), individuals owned almost 20 million of the 48 million rental units in the United States, approximately 40%.8 As shown in figure 1, individual investors are concentrated in smaller properties, owning almost three-quarters of properties with less than five units. The loss of even a single tenant’s rent payment would likely stress these individual owners. And although a lower proportion of these smaller properties have mortgages (figure 2), individuals who own rental properties may have been using mortgage forbearance to cover either the rental property mortgage to the extent allowed9 or may have used the forbearance on their own home mortgages if they were unable to cover that payment due to the loss of income from rents.

With the forbearance program winding down and no quick fix to the problem of tenants in arrears on their rent payments, some individual rental property investors could soon be facing delinquency and foreclosure. The pain will not be limited to individual investors; other ownership types not eligible to participate in the forbearance program are also being stressed by the increase in tenants behind on their rent, although they are more highly leveraged. Federal money was provided through the Emergency Rental Assistance Program (US$25 billion in December 2020 and US$21.55 billion in March 2021) to help cover the costs of overdue rent and utility payments.10 As of August 30, US$6.54 billion, or 14%, of the total amount appropriated had been paid out.11

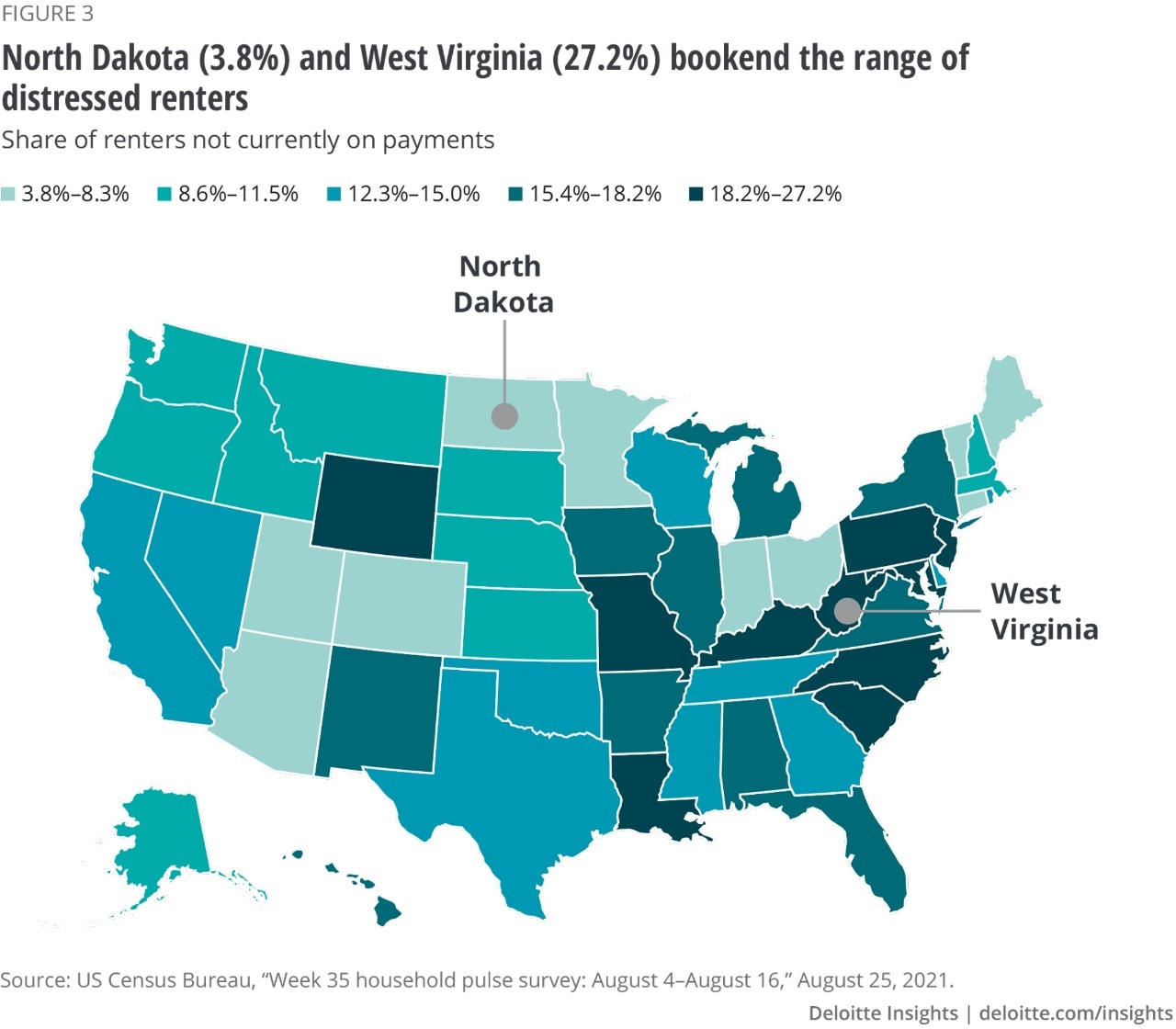

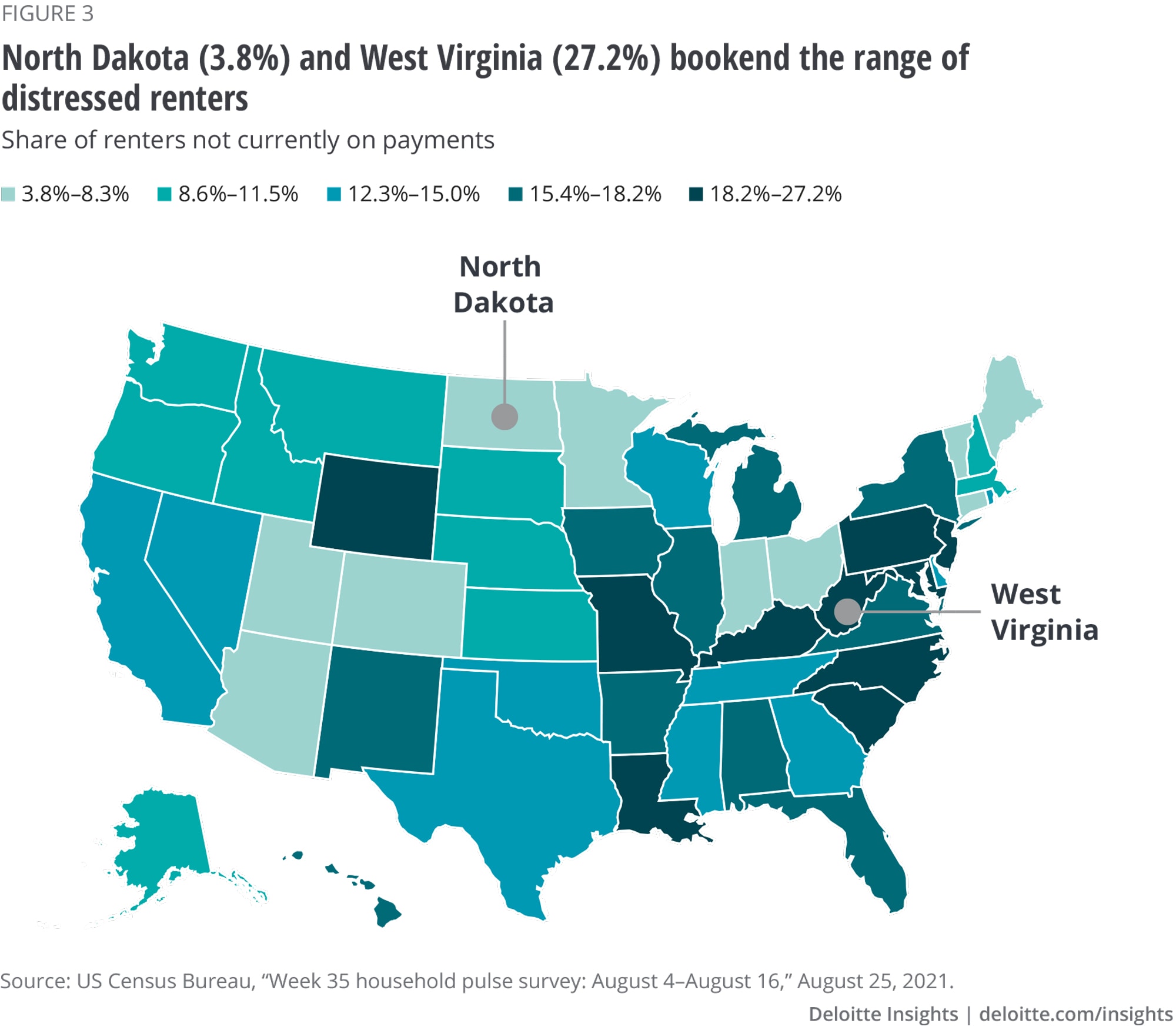

As of mid-August, 6.3% of rental households (3.5 million) reported that they are very or somewhat likely to be evicted in the next two months. But whether or not renters are concerned about the possibility of eviction—some may still be hopeful that eviction moratoriums will be extended at the state, if not national, level—twice as many (at 14.6% or just over 8 million households) are not current with their payments. There are substantial differences in rental stress across the country where the proportion of renters behind on rental payments range from under 6% in North Dakota, Maine, Indiana, and Utah to more than 25% in Louisiana, North Carolina, and West Virginia (figure 3).12

The issue of evictions is more than simply a property rights concern. As research from the Urban Institute points out, an eviction can impact all aspects of life, as families lose belongings and perhaps even jobs as they struggle to find new housing—a search made more difficult because of having been evicted. Trauma, particularly for children, is often an outcome.13 Given the high geographic concentration of tenants behind in their rents in certain states, it is likely that if a wave of evictions follow the end of the moratoriums, entire communities may suffer a series of adverse economic consequences. For instance, delinquencies and foreclosures may rise among the rental property owners who may be unable to find new tenants that can be relied upon to stay current on their rental payments. With such a large number of renters behind on payments and already worried about eviction, the impact on local housing markets, especially when combined with the likely increase in foreclosures due to the end of forbearance, could be substantial. And the impact would not be limited to housing if a substantial number of properties entered foreclosure—the loss of wealth would quickly translate into lower spending and employment and therefore lower rates of overall economic growth.

Supreme Court of the United States, “No. 21A23: Alabama Association of Realtors et al. v.

Department of Health and Human Services et al.,” August 26, 2021.

View in ArticleCover art by: Sylvia Yoon Chang