Climate change and home insurance: US insurers have been hit hard by severe weather-related claims

A sunnier profitability forecast may be possible—if personal property insurers partner with stakeholders to build resiliency and address climate-related risks head-on.

Rising weather-related losses and inflation-impacted costs to restore damaged assets are impacting homeowner insurers’ profitability, exacerbating pressure on a segment already stressed from years of persistent high loss ratios. In 2022, 75% of the property and casualty sector’s insured losses, or US$74 billion, were related to the US homeowner segment.1

As the severity and frequency of losses caused by natural catastrophes continue to accelerate at an estimated average annual growth rate of 5% to 7%,2 US homeowners could face up to US$118 billion in losses by 2030 due to weather events.3

It doesn’t have to be that dire. Deloitte predicts that if insurers, in partnership with government agencies and policyholders, invest US$3.35 billion in residential dwelling resiliency measures, the two-thirds of US homes that are not currently built to code could be made resistant enough to reduce many weather-related claims losses. In fact, these actions could save insurers as much as US$37 billion by 2030 (see “About this prediction” for more on our methodology).

About this prediction

The Deloitte Center for Financial Services’ forecast bases weather-related insured losses on Swiss Re’s growth rate estimates.4 Our analysis also factors in research from the US Federal Emergency Management Agency (FEMA) and the National Institute of Building Sciences. Homes that meet FEMA’s hazard-resistant building codes or standards could see declines in average annual damages by up to 48%.5 According to FEMA, only 35% of the homes in the United States are built to code.6 The National Institute of Building Sciences’ cost-benefit multiplier of 1:11 suggests that every dollar invested in making homes resilient (to code) could generate savings of US$11.7

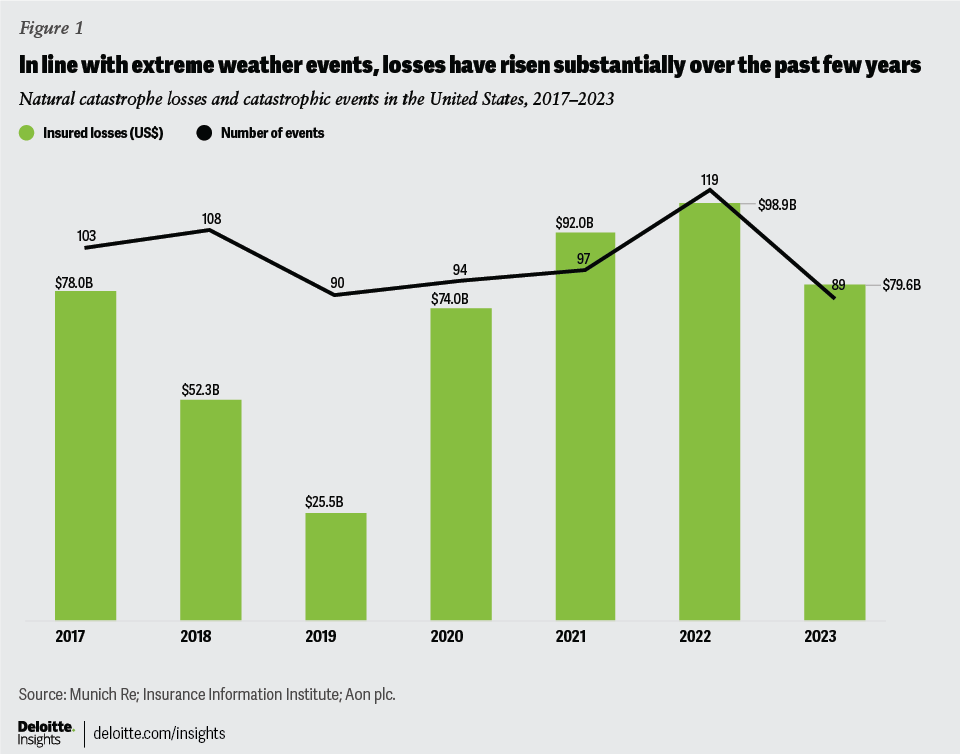

Rising costs and weather-related disasters jeopardize insurer profitability

The rising frequency and intensity of natural disasters are damaging more assets every year. The number of US catastrophic events increased by 32% between 2019 and 2022.8 Insured losses escalated from US$25 billion in 2019 to US$99 billion in 2022, accounting for 80% of global natural catastrophe losses (figure 1).9

Exacerbating this, between 2020 and 2023, replacement costs for property and casualty-related losses also rose by an average of 45% amid overall inflation growth of 15%.10 Climate change may be fueling disasters, but housing demands are further driving risk. Even in the face of rising climate-related risk, Americans continue to migrate to disaster-prone parts of the country, often building higher-value homes in these regions.11 For example, between 1990 and 2020, nearly 44 million homes were built in areas where wildfires are common, such as California and Colorado.12

These dynamics contributed to deterioration in the US property and casualty industry combined ratio, from 98.8% in 2020 to 102.7% in 2022. And at 103.8%, the expected ratio for 2023 is even worse, reflecting an alarming trend in underwriting loss.13

Insurers near-term efforts to lower losses are mostly stopgaps

The gap between what constitutes viable insurance pricing and what some state regulators permit is also widening.14 Several insurers are reacting to this untenable situation by either reducing or entirely pulling coverage from areas prone to weather-related disasters, decreasing the overall availability of insurance coverage.15

Since having fewer insurance options could have negative impacts on homeowners, regulators in some US states are beginning to work with insurers to find ways to factor in increased hazard risks in property insurance pricing.16 Home insurance premiums rose by 11% on average last year.17 In high-risk states like Florida, premiums jumped as much as 35%,18 making affordability a challenge for an increasing number of homeowners. Reinsurance rates are also likely to remain elevated because reinsurers’ retained earnings have been insufficient to bear their cost of capital, let alone build stronger balance sheets to cater to an increasing risk landscape.19

Proactive steps insurers can take to boost resiliency and stem losses

Property and casualty insurers can’t change the weather—or the likelihood of more extreme weather events in the United States. But they can explore alternative strategies like loss prevention and mitigation to help maintain market viability in regions prone to extreme weather. Here are some approaches insurers can consider:

1. Elevating awareness for policyholders on risk prevention and mitigation. New homes built with advanced construction techniques and materials, like engineered timber, impact-resistant glass windows, reinforced doors, and enhanced roof coverings, are more resilient to damage from severe weather compared to most existing homes. For example, the average annual costs from wind damage are about 84% lower for a home built in 2022 to code compared to a 1990s-era home.20 However, adhering to the Federal Emergency Management Agency’s hazard-resistant building codes for existing structures could also reduce losses significantly. The agency suggests that average annual damages from storms could decline by 48% for homes that meet the specified criteria (to code).21

Still, many homeowners are struggling to understand how to fully protect themselves. In a recent survey of 2000 US homeowners, 63% of respondents were confused about what coverage they needed and how much to purchase, leaving them at risk of being underinsured.22 In fact, 84% of respondents wanted carriers to educate them on weather-related risks and how to prevent or mitigate losses.23 This suggests an opportunity for insurers not only to help empower homeowners to make more informed decisions, but to take action to build or adapt their homes to become more resilient.

2. Upgrading to code may seem cost-prohibitive to many homeowners, so insurers could promote incentives to balance out short-term investments. Currently, only 35% of residences nationally are built to code,24 creating an opportunity for insurers to help homeowners in the remaining 65% shore up their dwellings to meet current standards. For example, insurers can consider offering policy premium discounts to incentivize homeowners to upgrade to hazard-resistant structural improvements. Insurers could also inform homeowners about state-sponsored incentives for upgrading to code and offer guidance on how to best take advantage of these programs.

In several states, such as Florida, insurance companies offer discounts for policyholders that fortify their homes against hurricane winds by securing roofs and shutters and reinforcing garage doors.25 The state also offers sales tax exemptions for impact-resistant windows, doors, and garage doors.26 National Flood Insurance Program policyholders can lower their premiums by raising their properties up, moving equipment off the bottom floor, and providing flood openings to allow floodwaters to flow from the interior to the exterior.27 California offers incentives such as discounts on insurance or tax credits to homeowners who make their homes more resistant to fires, wind, rain, and hail.28

3. Deploying new technologies can help insurers anticipate risks with more precision. Location is one of the most important risk factors when it comes to a natural catastrophe, and many communities continue to reside in hazard-prone regions.29 But improvements to satellite imaging can help insurers map out high-risk areas at a more granular level and identify and offer guidance on safe areas to build or rebuild. One Insurtech company uses artificial intelligence to score climate risks and property vulnerability and help identify risk-prone areas. Deploying these types of measures can help facilitate prudent underwriting and loss mitigation.

4. Partnering to build back better. Insurers can align with and encourage the use of vendors and suppliers that procure and undertake repairs to drive more resilient build-back-better approaches. These can include measures like using sustainable and durable building materials and designs during repairs.

Guiding and incentivizing the 65% of consumers whose homes are currently not up to code to shore up their dwellings could reduce average annual losses by as much as 48%, or US$37 billion.30 The National Institute of Building Sciences’ cost benefit multiplier of 1:11 suggests that every dollar invested in bringing homes up to code will generate savings of US$11.31 Deloitte predicts that if insurers, in partnership with government entities and policyholders, invest US$3.35 billion in residential dwelling resiliency measures, homeowners could see a reduction in weather-related claims losses by up to 31%, or US$37 billion, by 2030.32 This could help boost profitability and drive toward a more stable industry combined ratio, which can be a win for insurers and consumers alike.

{kind=link}