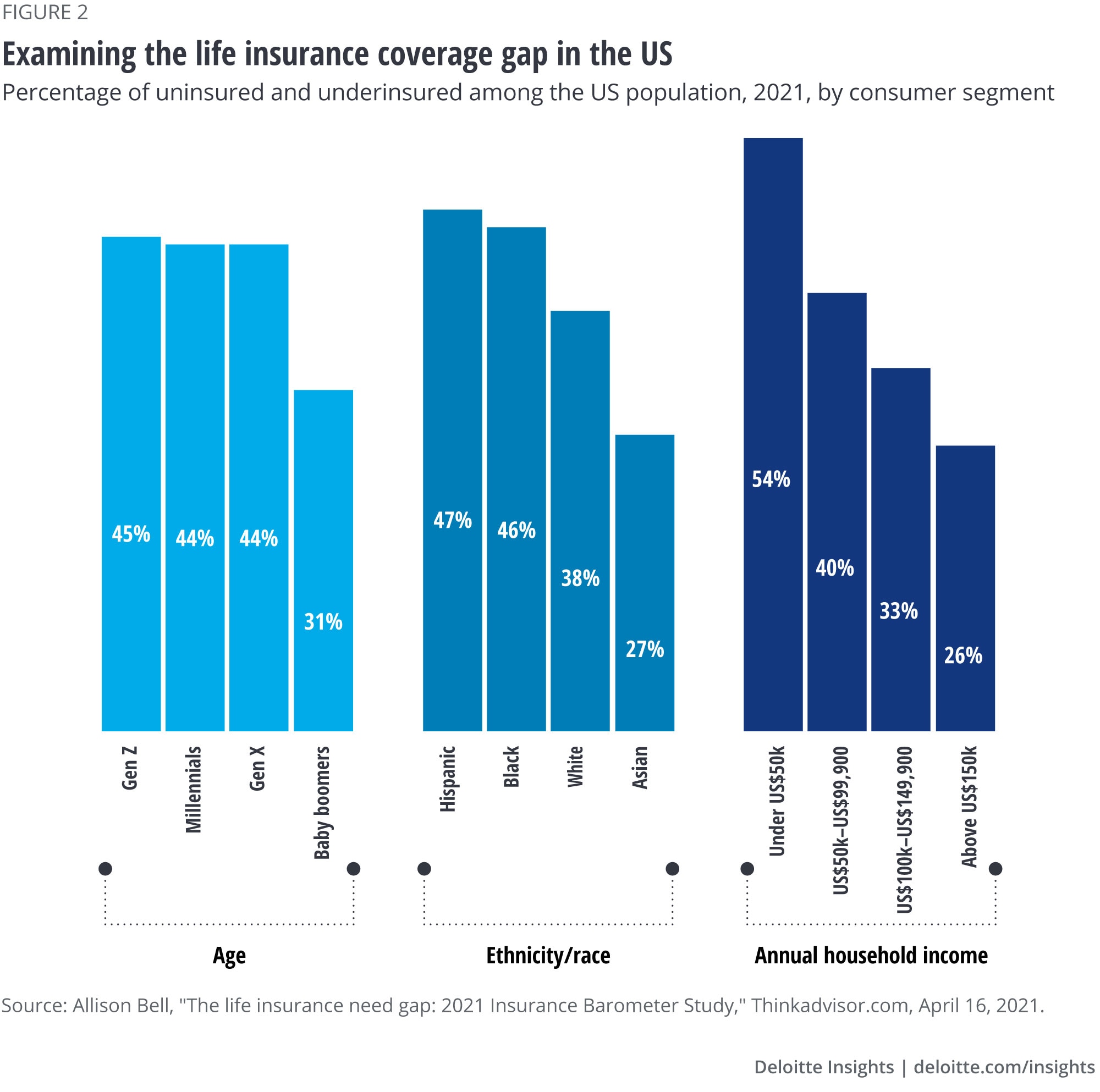

According to LIMRA’s 2021 Insurance Barometer Study, the largest percentage of coverage gaps appear in the youngest age group and lowest-income segment and decreases as age and income increase (figure 2).8 The study also reveals Latino/Hispanic and Black/African American consumers tend to be more uninsured or underinsured compared to white and Asian/Pacific Islander segments.9

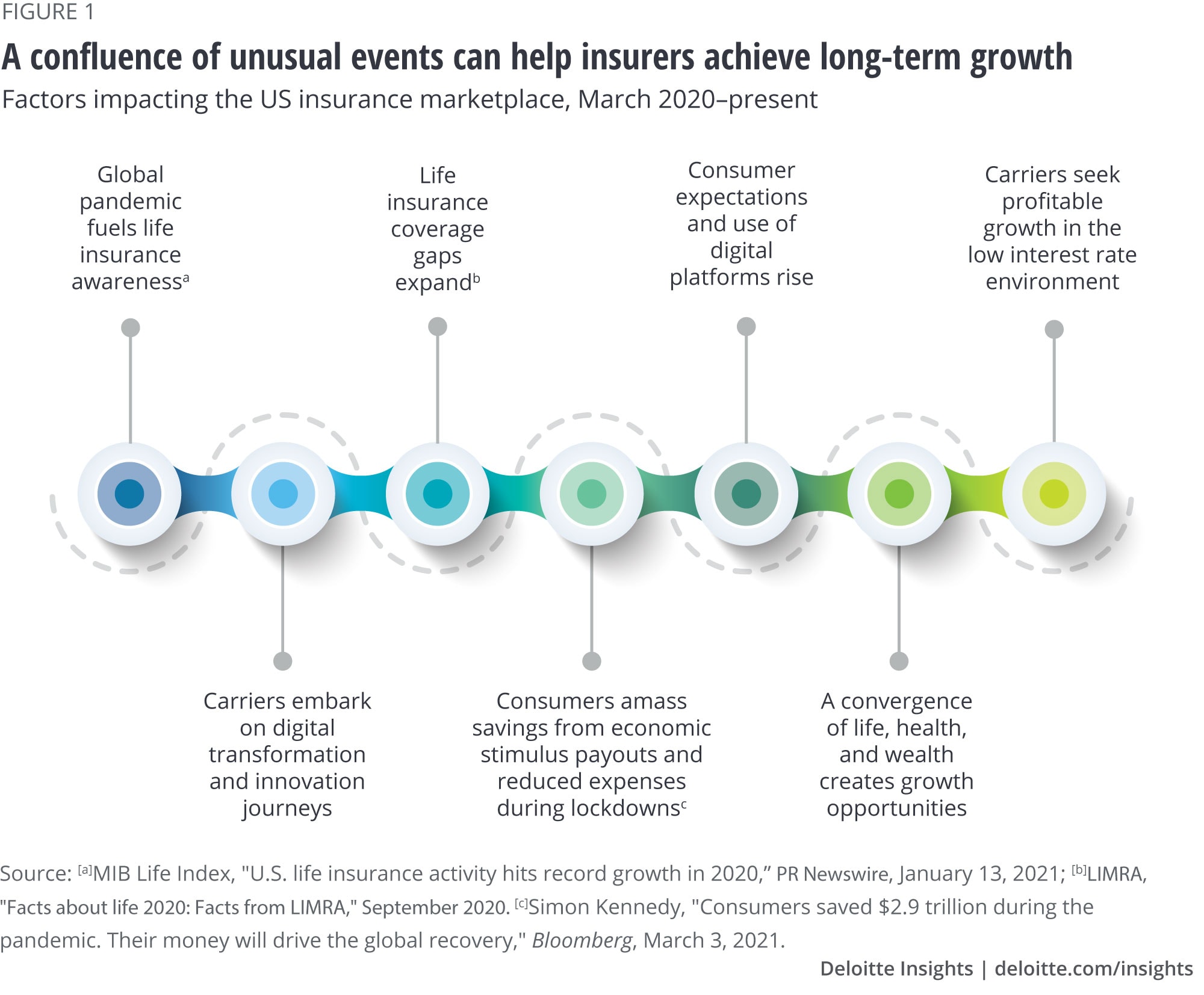

Capitalizing on pandemic-fueled savings and awareness could help fill gaps

Our survey revealed that across all ages, income levels, and races/ethnicities, the top deterrents for respondents to buying additional or new life insurance were perceived cost of coverage and other financial priorities. But, despite the rise in unemployment during the period, the pandemic-driven surge in savings among the US population10 could make consumers more open to buying coverage now than they were prior to the pandemic—at least in the short term.

Still, some consumer segments are less financially literate than others. They may first need to be educated on the value of life insurance coverage before considering a purchase.

For example, nearly twice as many respondents in the youngest age segment (21- to 30-year-olds) revealed they were unfamiliar with the value of mortality products compared to older respondents. Not surprisingly, the lowest-income groups knew less about these products than higher earners did.

Similarly, 18% of Blacks/African Americans surveyed said they were not familiar with the purpose of life insurance compared to approximately 12% of whites, Latinos/Hispanics, and Asian/Pacific Islanders. Moreover, a higher proportion of surveyed Black/African American and Latino/Hispanic insurance owners (36%) revealed they are unfamiliar with different life insurance options, compared to 27% of whites and Asian/Pacific Islander respondents.

Our survey shows interest in purchasing life insurance over the next 12 months was highest for Black/African American and Latino/Hispanic respondents. This could be because both were hit hardest in terms of death rates11 and unemployment12 (resulting in loss of employer-sponsored coverage) during the pandemic.

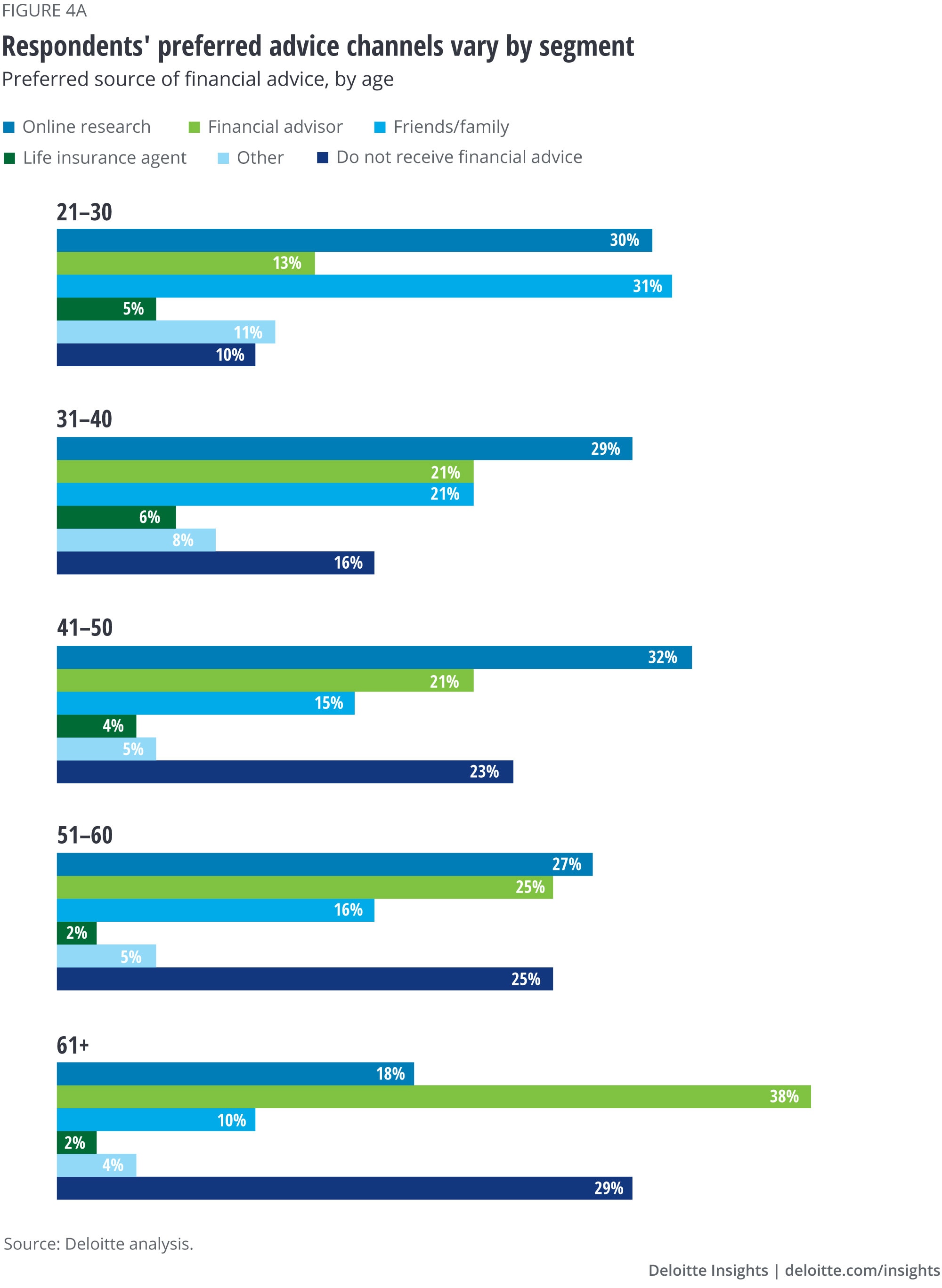

Interest in purchasing coverage also appears to be highest among younger consumers (under age 50): More than half of respondents between 31 and 40 years old said they plan to buy a life insurance product in the next year. Indeed, the surge in application activity throughout the pandemic was highest among respondents younger than 44 (7.9%) and decreased as age increased.13

Given the financial literacy disparities among segments, insurers have an opportunity to build on the increase in awareness of the need for coverage.14 They can explore new ways to educate underserved populations by focusing on demographics that are least likely to understand the value of mortality coverage.

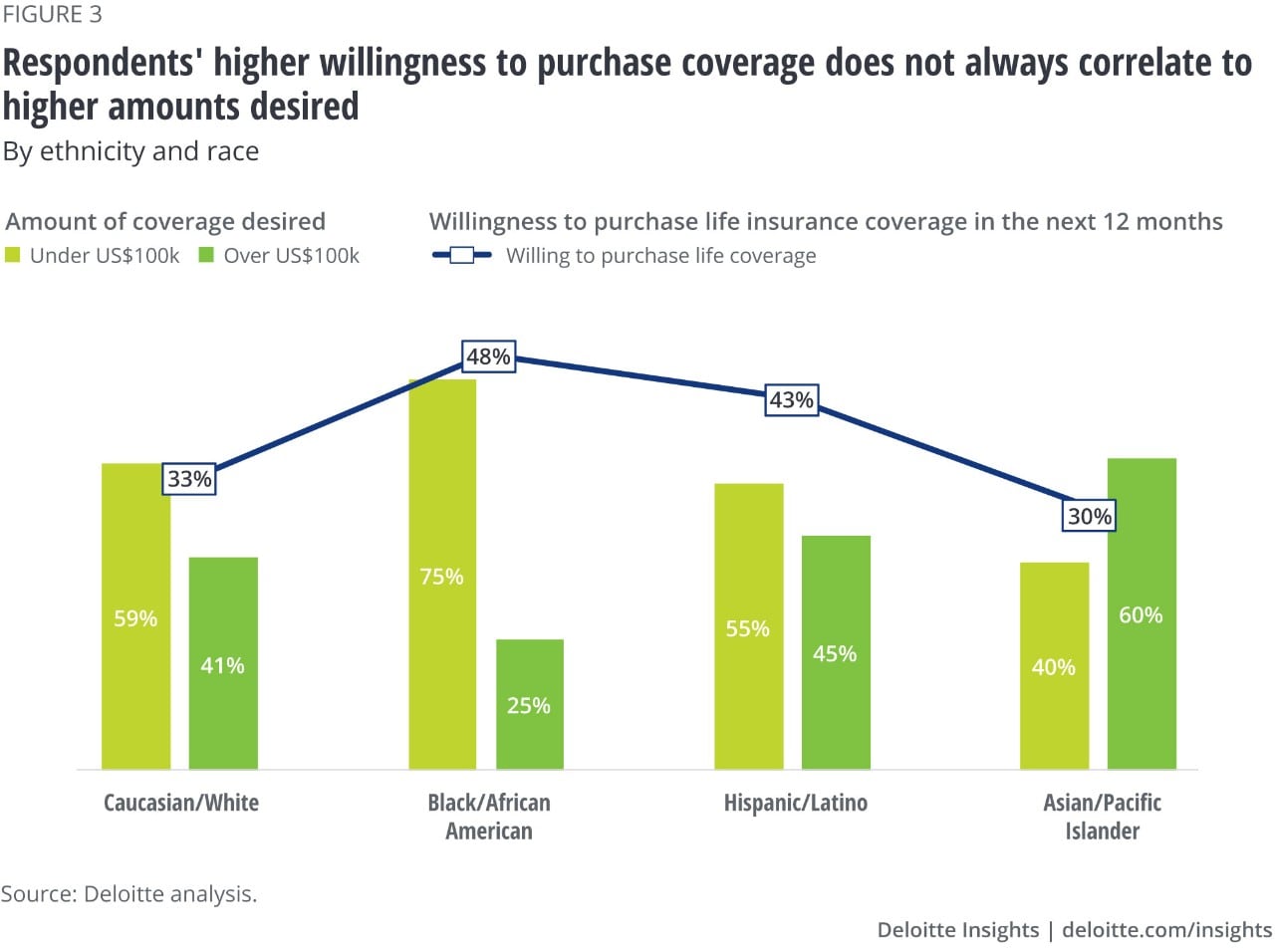

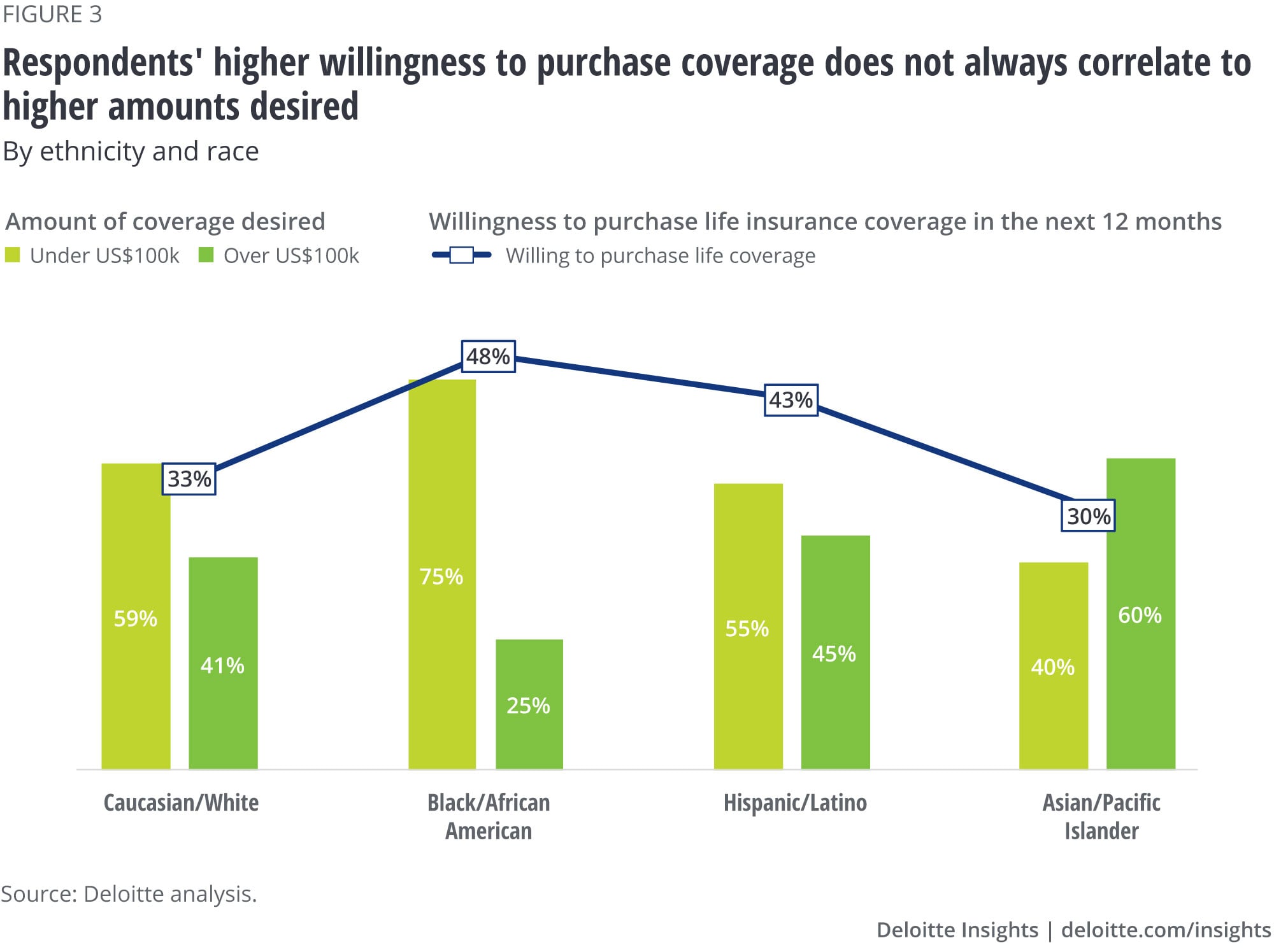

Higher interest does not always yield higher coverage

Our survey revealed the relationship between some segments’ willingness to buy and the coverage amounts they wanted were not necessarily correlated (figure 3).

For example, although Black/African American respondents showed the most interest in purchasing a life insurance product in the next 12 months, the coverage amounts they wished to buy were lowest compared to all other races/ethnicities. Studies show that despite being more likely to have life insurance, Black/African American people are far more underinsured than whites.15 Conversely, fewer Asian/Pacific Islander respondents said they wanted to purchase a life insurance product in the next year, and that they would like to attain higher levels of coverage than other ethnic groups indicated.

For consumer segments that wanted more life insurance but may understand it less, targeted initiatives exposing disparities between coverage levels and financial need could help fix this disconnect.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}