Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue XLII

31 October 2018

Economy

A silver lining in trade impasse

China's stock market has been plagued this year by economic deceleration, the US-China trade talk impasse and resultant jitters in emerging markets. The latter were caused by escalating trade tensions between the two largest economies in the world and investors' perception that more emerging markets could become fragile as US interest rates rise. Given China is the largest export market for many emerging economies (e.g., Brazil and South Africa), there is also fear of a potential contagion effect on China's external sector. All of the above have created the bear market that we see today. On the other hand, the good news is that the persistent sell-off in A-shares may trigger policy changes in China. But the challenge remains unmet, so market sentiment is unlikely to improve significantly unless an escalation of the trade conflict is averted.

Over the past few days, top Chinese leaders have been outspoken in their support of private enterprise. On 20 October, President Xi Jinping said that "to support private enterprise has been the consistent policy of the Government". Liu He, the deputy prime minister, has outlined comprehensive measures aimed at revitalizing the stock market and has reiterated Xi's pledge to help private enterprises through favorable taxes and better access to finance. In addition to these assurances from top leaders, Yi Gang, governor of the People's Bank of China, Guo Shuqing, governor of China Banking & Insurance Regulatory Commission, and Liu Shiyu, head of the China Securities & Regulatory Commission issued a joint statement on October 19, implicitly pledging further support such as liquidity injection or relaxed rules on equity unwinding.

The call for calm from regulators prompted a strong rally of the A-share market on 20 October, although it quickly fizzled out. On China's stock market, we are of the long-held view that systemic risk from a significant sell-off of A-shares is negligible for a very simple reason: the percentage of corporate financing from capital markets is very low even during a bull market (less than 5%). Conversely, in many emerging markets, especially those where domestic investment is largely financed by capital inflows, a major correction of equity valuations will immediately put downward pressure on exchange rates or upward pressure on interest rates. What has unfolded in Türkiye, Argentina and Brazil this year is a case in point.

In China, the economy can easily withstand volatilities of the A-share market. However, the flipside of such resilience is the fact that China's stock market and capital markets in general do not have the capacity to efficiently allocate resources. The only way to make the stock market a key mechanism for resource allocation or, in other words, "to have market forces play a critical role"—as was the resounding message from the 18th Party Congress in 2013—is to reduce political interference while promoting competition. It would be unthinkable for any country to establish a well- functioning stock market without meaningful participation from foreign investors. China is no exception. From this standpoint, more rapid liberalization of the financial sector is badly needed given the current subdued sentiment in evidence here.

The inherent volatility of China's A-share market has reinforced the prevailing mentality of retail investors who are always betting on favorable policies (e.g., buying from the `National Team’, the fund which was created by the Government to stabilize markets in the wake of crash in 2015, direct intervention or liquidity injection). However, this time such policies have not garnered support. If the National Team has managed to introduce a temporary floor for the market by large-sum buying, this cannot last forever. It will have to find a sustainable exit strategy in the end. Even in the short run, retail investors can't beat the National Team. Foreign competition will naturally reduce political interference as no policymakers would gain politically by bailing out foreigners. The good thing is, at least in several areas such as stock broking/trading, insurance and asset management, foreign institutional investors remain extremely keen to invest in China. Keeping this in mind, the silver lining to the ongoing trade war may well be that it brings about convergence between external pressures and China's domestic reform agenda.

Should investors be spooked by the continued economic slowdown? We think not. If policymakers want to reflate the economy, the easy way to do it is a huge dose of pump priming of the kind we saw 10 years ago. But this is precisely what China must avoid. For the "4 trillion RMB" stimulus has left a legacy of excess capacity and worsening asset quality that is tormenting the economy today. In short, although an over-expansionary fiscal policy will boost the GDP growth rate in the short term, its side effects can be enormous in a rising interest rate environment. Moreover, the crowding-out effect (discouraging private sector spending) of such a policy could make future reform more difficult and reinforce the concern about the "state sector marching on while the private sector is in retreat". Over-reliance on fiscal levers might also make future trade talks with the US and other major trading partners more complicated in the sense that a large investment in infrastructure will put the brakes on capacity reduction which in turn will invite more protectionism.

Figure: A less accommodating external environment

On the monetary policy front, China could face certain constraints other than widening interest rate differentials between it and the US (given all China can do is lower reserve requirement ratios for commercial banks). It is true that a weaker RMB could improve monetary conditions so long as inflation is under control. But China could only use the RMB exchange rate as a monetary lever with a similar effect to lowering interest rates to a certain extent and provided there is some genuine progress in the stalled trade talks with the US. The US, however, would like to focus on thornier issues such as subsidies to SOEs and market access—as the recent comment by US Treasury Secretary Steven Mnuchin that China isn't manipulating the RMB exchange rate seems to suggest.

In conclusion, economic deceleration is the natural consequence of de-leveraging and this is why investors really need not be too concerned. Based on Q3 data, GDP growth has come in at 6.5% despite an unusually weak result in fixed asset investment (cumulative growth in first three quarters is 5.4%, whereas Q3 alone saw growth of 4.6% YOY). This is largely due to the greater importance of the role of consumption in the economy. But, for the consumption story to be credible, the policy framework should be aimed at boosting consumers' income and wealth. Specifically, this means lower income taxes, import tariffs and a stock market reinvigorated with more foreign participation. Recent tax cuts to raise individual income threshold for households and deductions for education are welcome steps, though a bolder step is anticipated. The same argument goes for the stalled trade talks. If China can preempt a meaningful cut in tariffs and unveil a "big-bang" in financial sector liberalization, it will put the US in a corner if it continues to link non-trade issues to the trade talks.

Retail

A newcomer to the daily life services market

In October 2018, in a bid to take on its rival Meituan in the digital daily life services market, Alibaba announced that it would establish a new company essentially consisting of Ele.me and Koubei, its food delivery and food and lifestyle purchasing businesses. This expansion is believed to be yet another top strategic move by Alibaba, in the line of the New Retail strategy. Meituan, the leading company in this market, already listed itself on the stock market in September and, thanks to the potentially gigantic size of the market, its market capitalization exceeded HKD 400 billion in the first day of trading, eclipsing the market capitalization of companies such as JD and Xiaomi. Alibaba's strategic deployment and integration in this market will bring about new changes to the sector as a whole and in several sub-sectors, in which the two giants will set off a new round of competition.

Over the past several years, the digital daily life services market has experienced continuous and rapid growth. According to iResearch, the total market size of daily life services swelled to RMB18.4 trillion from RMB11 trillion with a CAGR of 13.7% between 2013 and 2017, while the digitalized daily services market grew at a much faster GAGR of 50% from RMB0.43 trillion to RMB2.7 trillion in the same period. The digitalized daily services market is project to grow 19.8% annually between 2017 and 2023 and is expected to reach RMB 8 trillion in 2023, about three times the present market size (as of 2017). Additionally, the penetration rate of digitalized services will increase to 24.2% in 2023.

Figure: The size of the digital daily life services market

Notes: services include food delivery, catering services, food retail, local transportation, online booking etc.

For now, Meituan remains the undoubted leader as its services cover almost every single sub-sector of digitalized daily life services. Although Alibaba’s coverage is not quite as extensive, the merging of Eleme and Koubei will allow it to integrate service resources across the entire spectrum and serve consumers better across the board. Therefore, competition between these two industry giants will escalate to a level where they will fight over the ecosystems of their business on top of the single-sector businesses they also compete in.

However, the fact Alibaba and Meituan have different strengths and weaknesses is what will make this competition not just interesting but also instructive.

- Meituan has a market share advantage in main sub-sectors like catering and food delivery. According to Trustdata, Meituan's transaction share registered 59% in the first half of 2018, larger than Eleme's 30% market share. Not content with resting on its laurels, Meituan's new "Food plus" strategy focuses on food-related services and the company will continue to invest more resources into these services. To carve out more market share from Meituan, Alibaba has poured a large funds into Eleme. The new company could be a sign of a new round of investment in this market, giving rise to fiercer competition between these two giants.

- Eleme and Koubei draw strength from Alibaba's ecosystem. The combined Eleme and Koubei will benefit greatly from Alibaba's bank of digital experience and consumer data, gaining insights into consumer preferences, diversified services, delivery capability, technologies and other resources Alibaba has garnered from other businesses. Although Meituan is continuously expanding its service offerings, its ecosystem is nonetheless weaker than Alibaba’s. Although Meituan has several major business operations like food delivery, booking and group purchase, its local transportation and retail services have still got some way to go. Alibaba, on the other hand, has already built an integrated ecosystem comprising new retail, finance, entertainment, sports and healthcare on the foundation of its main e-commerce businesses. If Hema, Hellobike and Figgy are all included in its daily life service matrix, Alibaba's capacity to influence this market will increase.

To sum up, the integration of Eleme and Koubei will help Alibaba enhance its dream concept of the "3 kilometres" radius of ideal life. Meituan, at the same time and although it is market leader, is tasked with integrating its different businesses better and improving its synergy across businesses. Competition in the digital daily life services between Alibaba and Meituan will escalate as Alibaba puts more resources into this market.

Technology

Countdown to 5G

Imminent commercialization

The clock is ticking: the global telecommunication network is about to begin the process of transitioning from 4G to 5G. 5G promises to have a profound impact on our daily lives. Higher speed, lower latency, lower power consumption and a highly reliable network is expected to give rise to new business scenarios and create an "everything-connected" world that will generate billions of dollars of economic value. 5G will be adopted in emerging sectors such as autonomous driving, Internet of Things, connected-vehicles and the industrial internet. It is estimated that 5G will cover 40% of the global population by 2025, reaching 2.7 billion consumers. China is on track to become the world's biggest 5G market.

In the race to seize first mover advantage, trials to roll out 5G have been underway in 49 countries by 77 telecom operators. Judged by their working progress, commercialization has reached the countdown stage in the US, China, Japan and South Korea; for 5G development is not only about internet speed per se, but a competitiveness showdown among great powers in the intelligence era: AT&T will roll out the world's first 5G mobile network before the end of this year, whereas Verizon has already "brought online" a 5G broadband internet service this October, replacing FTTH (fiber to the home). Looking east, China plans to kick off the commercialization of its 5G network in the coming year.

Economic contribution

Large-scale deployment of 5G will soon benefit almost every industry. By 2035, 5G is expected to bring about USD 12 trillion worth of economic value. The manufacturing sector is likely to see the largest increase, given 5G business will stimulate spending on related equipment production.

Figure: 5G's economic contribution to key industries (billion USD)

Drones for aerial surveillance are one example. These may enable greater sales in the transportation sector, but for this, the transportation sector will have to buy additional drones from the manufacturing sector that utilize the hyper fast 5G network to communicate with each other. To tap the full potential of 5G, leading companies need to keep up with investment along the value chain; it is estimated that leading 5G countries will spend an average of more than USD 200 billion a year on research and capital expenditure. At the initial stage, fundamental research and network deployment will take up the lion's share of budgets. As technology matures, the focus of investment will shift to application development and service customization.

Disrupting industries

5G is the next disruptive technology that will transform almost all existing industries, particularly sectors such as transportation, energy, manufacturing, education, healthcare and retail. We think the adoption of 5G will get off the ground on the consumer side, than spill over to the business side. Smart city and intelligent life will be the first key application scenarios for consumers. These include advanced video capabilities (i.e. 4K, 8K, 3D video, 360-degree video sports broadcasts), AR and VR applications for gaming and immersive TV. As 5G enters the phase of business application, autonomous driving and remote control of heavy equipment will be the next developments to watch.

It should be noted that 5G cannot be taken as a stand-alone technology, but rather as an "amplifier" in a technological ecosystem that consists of AI, edge computing, AR/VR and cloud computing. For example, 5G is the foundation of autonomous driving, allowing low-latency connections between vehicles and any entity via V2X (Vehicle to Anything). However, autonomous driving still requires sensor networks, edge computing and AI to ensure total safety.

Shifting roles

5G will redefine the role played by telecom operators. In the 4G era, Chinese operators have spent over RMB 300 billion building base stations covering 99% of the population. But in many regions, demand for 4G is in fact low and hence lacks application scenarios for business, so operators have not been able to recoup their investment. Given a 5G base station costs 1.5 times more than a 4G base station, and that the overall investment expenditure of 5G coverage is four times larger than that for 4G, it is imperative for operators to thoroughly analyze the market for downstream application before investing (return on investment, business model and specific application scenarios, etc.). This comes down to re-conceptualizing the role played by operators: they will no longer act only as asset or connectivity providers, but need to work together with vertical enterprises to maximize the value of a particular application and deliver one-stop solutions for customers.

Education

Unicorns, present and future

On 16 September, the 2018 List of Unicorns: China’s Education Industry was released at the education industry summit in Beijing. A total of 50 educational companies active in China were selected, the top 20 enterprises of which are “qualified-unicorns” while the rest are “potential-unicorns”. A "qualified-unicorn” refers to an education company that has shown sustainable growth in revenue and technology innovation capabilities. Most of the "qualified unicorns" are generally preparing for stock market listings. A “potential-unicorn” refers to an education company showing high growth in emerging segments.

Among the unicorns, Hujiang and New Oriental Online have submitted listing applications to the Hong Kong stock exchange, and ITCAST and GAOSI Education are in the pre-IPO stage. LAIX was officially listed on the New York Stock Exchange on 28 September, 2018.

Figure: 2018 China Education Industry Qualified (or Potential) Unicorns List

Enterprise Project |

Financing round |

Enterprise Project |

Financing round |

ITCAST |

Pre IPO |

Small station Education |

C round |

DaDa |

C round |

New Oriental Online |

Pre IPO |

Gaosi Education |

Pre IPO |

Xuebajun |

C round |

Hujiang |

Pre IPO |

Xueleyun |

D round |

iTutorGroup |

C round |

Yiqi Education Technology |

E round |

Kaochong |

D round |

LAIX |

Pre IPO |

Qingqingjiajiao |

D round |

Langfudao |

E round |

| Songshu AI zhishiying Education | A round |

Zhangmen 1to1 |

D round |

VIPKID |

D+ round |

Homework bang |

D round |

NetEase youdao |

strategic investment |

Homework Box |

C round |

Afanti |

B round |

Lejiaolexue |

A round |

Zuomeng young children programming |

B round |

Meishubao 1to1 |

B3 round |

Baby English |

B round |

Magic Ears |

A round |

Beierkejiao |

B round |

Muhuachengzhi |

B+ round |

Bianchengmao |

B+ round |

Nandinggeer |

B round |

Chengzhangbao |

B+ round |

Quxueche |

C round |

Duiawang |

B+ round |

VIP peilian |

B round |

E xueyun |

A round |

Schoolpal online |

C2 round |

Haiduxueyuan |

A round |

Yangcongjiaoxue |

C round |

Huohuasiwei |

B+ round |

Yizhaoyizxi |

B round |

Jike Big Data |

B round |

YoKID |

A+ round |

Kaishujianggushi |

B+ round |

Yulewan |

C round |

Koala reading |

B round |

Zhangtong Family |

C2 round |

Keai learning |

C round |

Smart study Education |

B+ round |

Langbowang |

B round |

Haifeng Education |

C+ round |

Source: Black Horse, released on September 16 2018, compiled by Deloitte

Note: The top 20 are qualified unicorns, and the last 30 are potential unicorns.

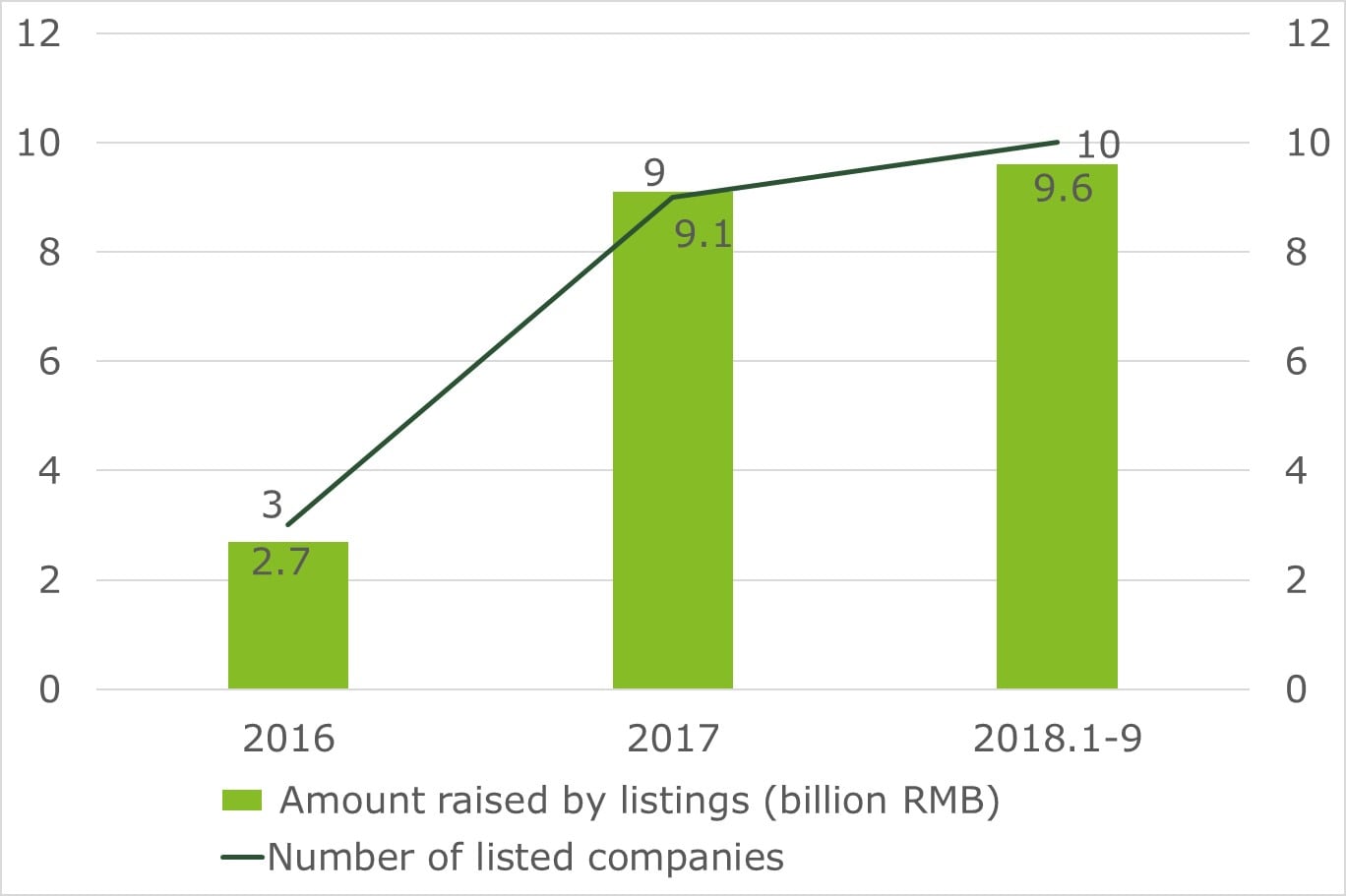

In 2018, Chinese educational companies seeking listings on the Hong Kong and US stock exchanges has become a trend. As of September 2018, 10 educational companies have been listed on overseas stock exchanges, raising a combined RMB 9.6 billion, far exceeding the amount raised by Chinese educational companies on overseas exchanges in 2017. Among them, six companies are listed in Hong Kong and four in the US. The domestic Chinese A-share market is also wooing educational companies to list as more details of regulations on private educational enterprises and process issues are gradually being clarified.

Figure: listed companies in the education industry and the amount raised (01/2016-09/2018)

Development trends in the education industry

Policy support

The government released a series of policies on the education industry recently. The Ministry of Justice published the Circular Seeking public comments on the Implementing Regulations of the Law on the Promotion of Private Education (Revised Draft) and (Draft for Review) in April and August respectively. The State Council then issued a document to regulate the K12 private tutoring industry. It also issued a directive to regulate the use of education funds. The principles and direction of educational supervision which were revealed in all the policies are to: 1) regulate and promote orderly growth of the industry; 2) provide fair access for all income groups; and 3) encourage private investment. It is obvious that the basic principles of state support for private education remain unchanged. Thus, the outlook for development of the privately invested education industry remains optimistic.

IPOs are expected

Companies on the unicorn list will very likely seek market listings. Deloitte expects that by 2020, the overall size of the private education market will reach RMB 3.36 trillion yuan. However, at present, the largest listed educational enterprise has not topped RMB 20 billion yuan in annual income. New Oriental, the largest private educational enterprise, made USD 2.444 billion in revenue in fiscal year 2018, up 36% year-on-year. Best Future, the second largest, had an annual income of USD 1.715 billion in fiscal year 2018, up 64% year-on-year. The potential of the Chinese education market is still huge, so it is only natural that a listing boom of educational enterprises will come.

Segmentation prospects

Most of the educational enterprises on the unicorn list focus on K12 tutoring and English language training. Among the 50 companies on the list, 27 operate in these two segments, which represent 54% of companies on the unicorn list. At the same time, a total of 10 companies focusing on quality [sriding1] [clrao2] education were selected as potential unicorns, accounting for 20% of the unicorn list.

From the perspective of the overall market for private education, numerous opportunities will emerge in the next two to three years. Given the importance attached to getting good grades in school, K12 after-school tutoring has big potential. The rise of STEAM education has attracted more attention from potential investors. In the number of new investments in the first half of 2018, STEAM education, vocational education and early education took the top three spots. The use of artificial intelligence will bring interesting changes in education as AI can help the scientific and technological development of the education industry and create new education models. International schools both in and outside China will continue to be in high demand. Many factors, such as the strong demand for overseas study, education consumption upgrading and fierce competition for further studies will ensure this market segment keeps growing.