Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 90

China's economic and industry outlook for 2024

Published date: 15 May 2024

Economy

Policy support to reignite animal spirits

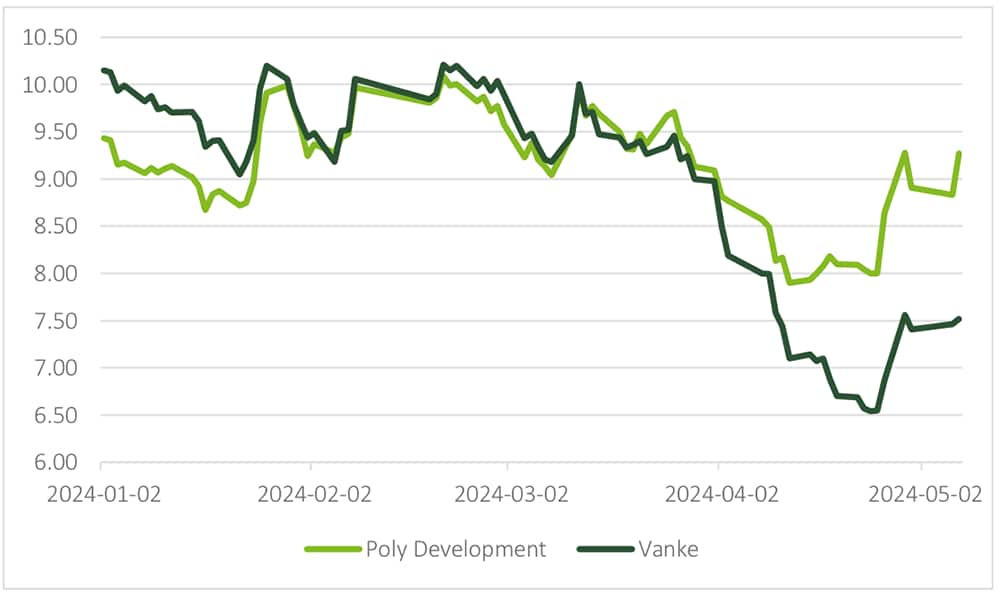

We are still of the view that a tentative cyclical recovery is underway in China, but the resilience of the economy can be marred by sluggish housing and construction data, with sales of commercial housing and property investment dropping by 27.6% yoy and 9.5% yoy respectively in Q1 of 2024. One could argue, of course, that some of these data are lagging indicators. The housing sector, which has gone through a consolidation period over the past few years on the back of stringent lending and administrative restrictions, is unlikely to turn on the dime. But encouragingly, policy support to the real estate sector has gathered momentum as of April this year. Specifically, meaningful policy support which ought to address both supply and demand is currently being rolled out. On the demand side, Nanjing (September 2023) and Chengdu (April 2024) have removed all restrictions on purchases by early May. Among first tier cities, Guangzhou continues to lead the campaign to ease restrictions, including by removing the limitation on purchasing homes over 120 square meters in January 2024. Meanwhile, in April Beijing announced it would allow consumers to purchase second and third units beyond the fifth ring road. In our view, it is only a matter of time until the remaining restrictions are inevitably phased out. On the supply side, the government has made it explicit that the guaranteed delivery of housing units will be ensured. Of course, the quid pro quo is that developers who are committed to completing these housing units would get adequate financing. The stock market clearly has taken note of all these measures by pushing up the share prices of developers. The Hang Seng index has posted its tenth consecutive sessions of a ferocious rally, the first time since 2018, despite a more challenging external environment on interest rates which could stay higher and longer given the Federal Reserve’s hawkish stance. Policymakers have also signalled that the reduction of inventories in the housing market is of paramount importance. In a similar vein to the white-goods market, most cities have rolled out programs allowing homeowners to replace old houses with new ones. The details remain vague, but the general idea is to minimize the risk of forfeiting downpayments for consumers who are inclined to fulfil their need for improved housing.

Figure: Share prices of developers have rebounded strongly

Source: Wind

Source: Wind

Meanwhile, according to Caixin, the central government is considering setting up a national real estate platform entity to acquire residential buildings which will be subsequently transformed into affordable housing. As expected, there are lingering concerns over local governments’ ability to pay for existing homes, but the rationale of such centralized schemes is to channel fiscal outlays to effectively purchase unsold homes. Given that the central government has ample capacity to take on more debt, there is little to be concerned about regarding the source of this funding. If consumer expectations could be revived, moral hazard is a small price to pay.

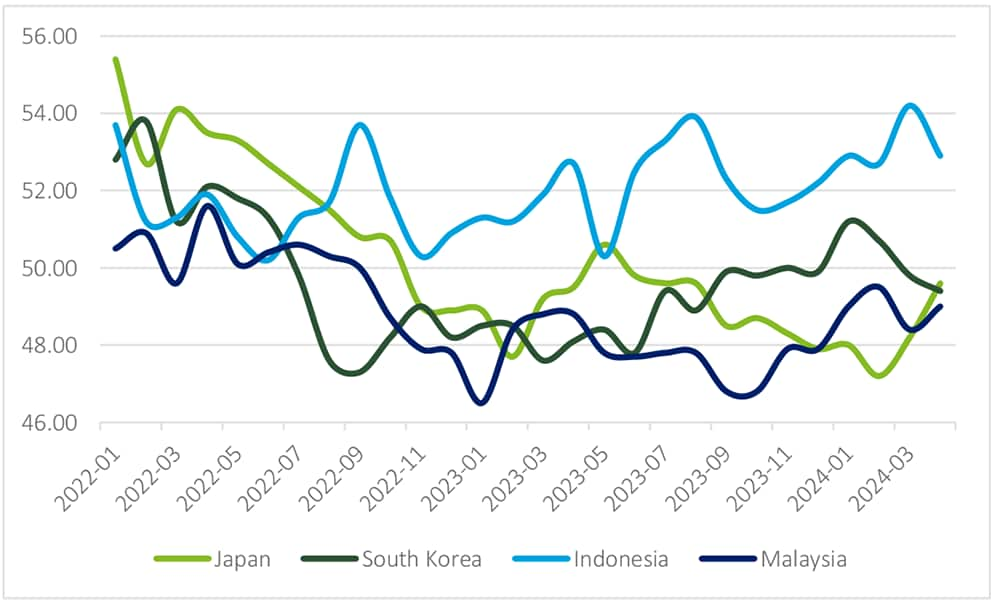

At this juncture, consumer confidence is still being hamstrung by the slow pace of recovery and a slumping property sector. The good news is that following exceedingly strong Q1 growth of 5.3%, the economy is on the mend. The 2024 growth target of “around 5%” is well in reach. PMI readings for April by the National Bureau of Statistics came in at a respectable 50.4, reinforcing the trend of a gradual recovery or at least stabilization. Travel data for the May holiday also eclipsed pre-Covid levels, with total spending by domestic tourists increasing by 13.5% compared to the same period in 2019. The PBOC would have cut interest rates if not due to drastically changed expectations on the USD interest rates. In fact, China’s central bank is not the only regional central bank whose easing is being delayed by the changing dynamics of both USD interest rates and the dollar’s overwhelming strength. The Bank Indonesia has maintained its benchmark rate unchanged in the wake of the Fed’s on-hold decision on the Federal Fund Rates in its latest FOMC meeting. On the USD interest rates, within three months, investors have completely changed their expectations from around four rate cuts by the Fed to “no change or at the most once in 2024” due to a much greater likelihood of a no landing scenario for the US economy. As a result, the Japanese Yen has been in free fall against the greenback, driven by carry-trade (interest rates are virtually zero in Japan) in the forex market. The Yen’s sharp fall is reminiscent of painful memories of emerging Asia in 1998 when the region was forced to devalue its currencies sharply on the sudden withdrawal of short-term capital inflows and worsened terms of trade. Such painful adjustment was further exacerbated by a persistent fall of the Yen until a joint G7 intervention in October 1998. However, Asia today is fundamentally different from what it was in 1998, and most regional economies are on a growth trajectory as evidenced by PMI data. The Yen’s once dominant role has been replaced by the renminbi which has held steady this year and even appreciated against most major currencies. More importantly, almost all regional economies have maintained a comfortable balance of payments and inflation is hardly a concern in Asia so long as crude oil prices are not seeing a significant spike.

Figure: Most Asian economies are on a growth trajectory, as evidenced by PMI readings

Source: Wind

Source: Wind

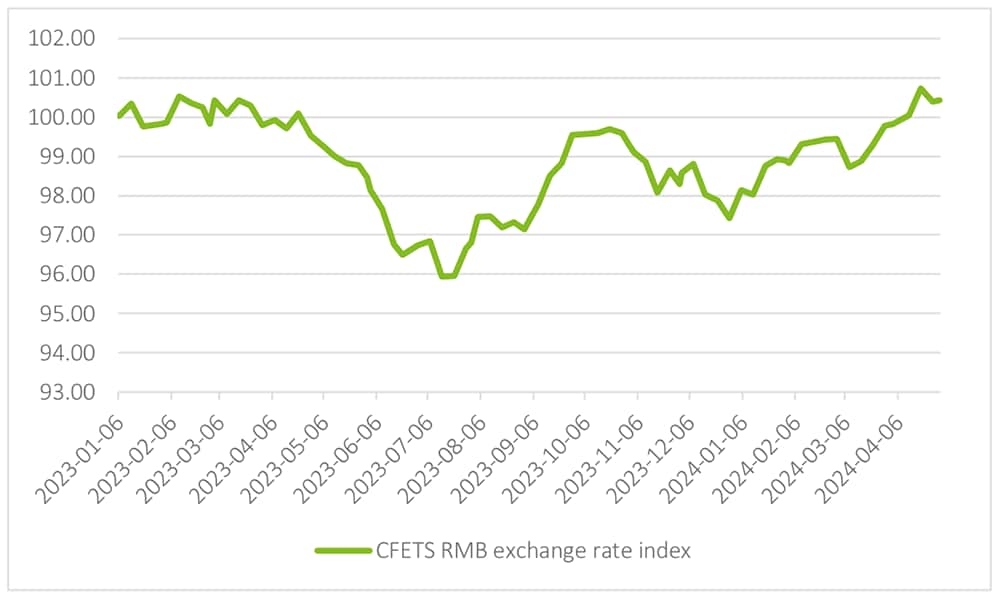

Against this backdrop, we believe China’s policymakers ought to step up its fiscal levers and continue to guide interest rates lower. So far, China’s external sector has not been adversely affected by the renminbi’s strength. The risk for China’s external sector is looming protectionism, not reduced competitiveness. At this year’s Beijing Auto Show during the May holiday, the biggest auto exhibition in the world, China’s EVs were a dazzling display in terms of sleek designs and smart features. As expected, the crowd was dominated by young, tech savvy consumers. China’s EVs will have to accelerate their exports given the contractions of the domestic market. Assuming the coveted North American market will become less open and more trade barriers will spring up regardless of the outcome of the US election, Chinese EV makers will need to penetrate further into the Global South and Europe. Potential tariffs by the EU will also be a test for China, but Chinese EV makers whose cost structure is so compelling could easily shrug off tariffs in the range of 15% to 20%. However, the EU has pledged not to de-industrialize and its auto sector is widely considered to be a strategic sector for several EU member states. The risk of a mini trade war therefore can’t be ruled out.

Figure: The renminbi has held up in the face of the dollar’s onslaught

Source: Wind

Source: Wind

TMT

Generative AI: endless possibilities for human resources

The enthusiasm for generative AI within enterprises has been high, and it is anticipated that generative AI will bring about a transformation in business models soon. For enterprises, the greatest value of generative AI lies in various benefits it brings, such as cost reduction, increased efficiency, and accelerated innovation. Deloitte's latest survey of enterprise executives found that generative AI has already penetrated several aspects of enterprise operation, such as IT, marketing, product development, and human resources. Most enterprises also recognize the importance of making AI talent management and training a top priority.

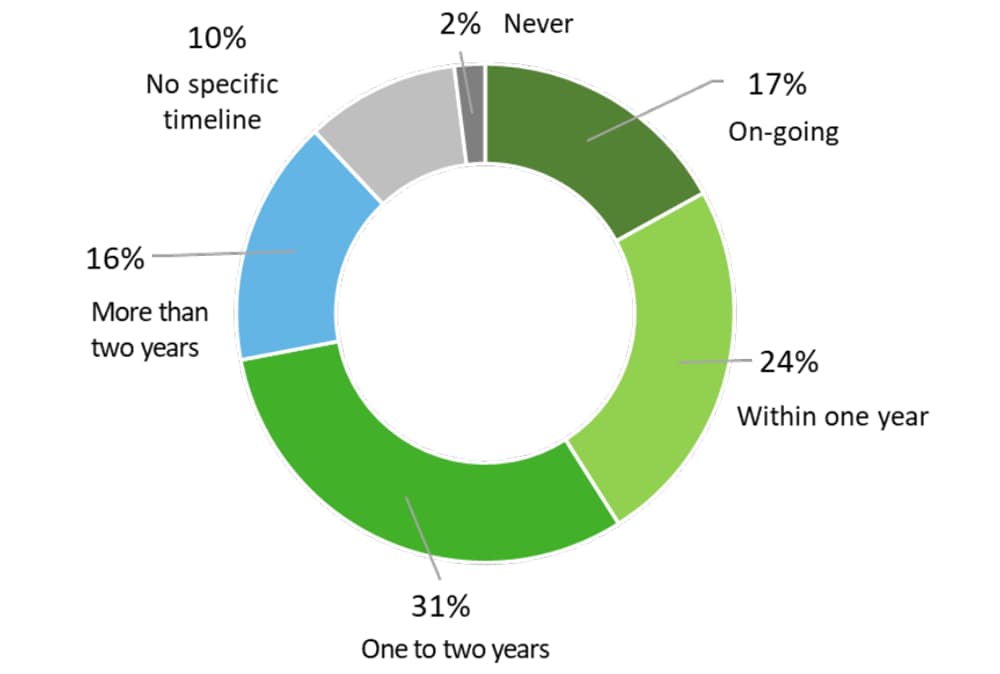

According to the survey, the vast majority (72%) of business leaders expect generative AI to drive changes in their talent strategies in the next two years (17% now; 24% within 1 year; 31% within 1-2 years). However, less than half (47%) of the respondents stated that they have educated their employees about the functionality, benefits, and value of generative AI. One of the biggest challenges in implementing generative AI is the lack of technical talent and skills. Therefore, effectively managing and training generative AI talent to adapt to constantly evolving technologies will become a top priority for enterprises.

Figure: How soon will Generative AI change your talent management strategy?

Source: Deloitte’s State of Generative AI in the Enterprise: Now decides next

Source: Deloitte’s State of Generative AI in the Enterprise: Now decides next

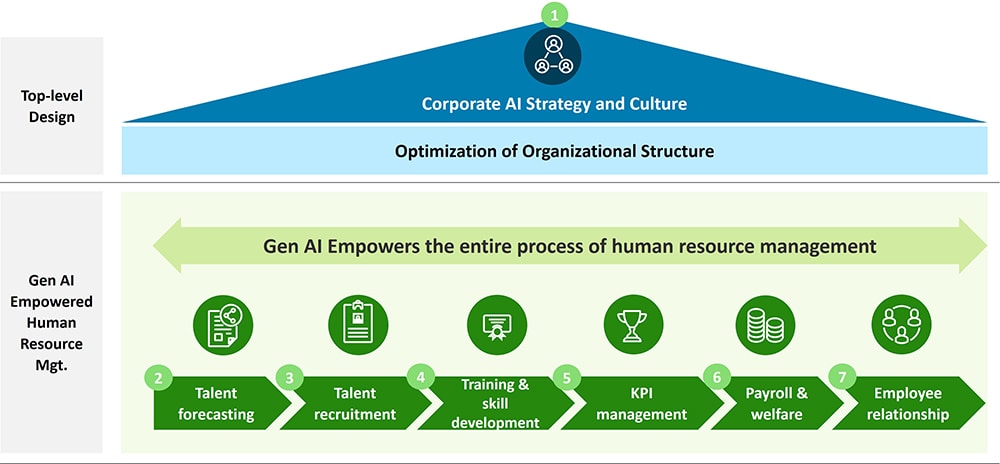

We think that generative AI’s greatest contribution could very well be in the human resources management process. Enterprises should seize the opportunities presented by generative AI to effectively enhance management efficiency, thereby increasing the competitiveness of the company.

Figure: Generative AI in a Human Resources Framework

Source: Deloitte Research

Source: Deloitte Research

From the strategy design stage onwards, companies should aim to create a culture that is suitable for the adoption of generative AI. This will involve a re-think of human resource management strategies, and organizational restructuring.

- Foster a culture suitable for the introduction of generative AI: Companies must reassure their employees that they are still central to operations and that AI is just another tool to facilitate their work. Upholding the principle of a "people-centric work culture” in an increasingly technology driven environment will ensure consistency between employees' work and the organization's mission and values.

- Prepare for the transformation of management objectives: HR managers need to understand not only employees' needs, motivations, and behaviors, but also the characteristics, capabilities, and limitations of generative AI in order to be able to effectively integrate and coordinate human-AI collaborative work within the organization.

- Transform recruitment strategies: Identifying, evaluating, and attracting the right kind of talent requires management to ‘look with new eyes’ in order to make accurate assessments of people's overall qualities and potential. They must develop a good understanding of the characteristics of the generative AI talent pool.

- Cultivate innovation and training tactics: New training strategies need to be introduced that focus on cultivating employees' technological capabilities and innovative thinking. Companies need to cultivate their employees' capacity to combine these new technologies with existing business to create new value.

- Reshape performance evaluation and incentive mechanisms: In addition to traditional performance indicators, performance evaluations should place more emphasis on employees' capacity for innovation and contribution in generative AI technology applications, as well as their long-term value creation for teams and enterprises.

From a human resource management perspective, companies can leverage generative AI to empower the entire HR process.

- Talent planning and forecasting: Based on big data and machine learning algorithms, companies can use generative AI to predict future talent needs and obtain corresponding talent planning suggestions. Meanwhile, as long as they satisfy all the compliance requirements, companies can use web crawling technology to obtain various kinds of recruitment information of other companies on different channels. This will help them understand competitor companies' overall talent strategies. Using such metrics as talent deployment, talent type deployment, or talent city deployment layout they can adjust their own recruitment strategies.

- Talent selection and recruitment: Generative AI can be used to screen many resumes quickly and accurately, automatically matching candidates based on preset conditions to achieve intelligent resume screening and matching. It can also be used to evaluate candidates' responses and performance through voice recognition, emotion analysis and other technologies in an automated interview assessment process. In addition, companies can use intelligent robots and virtual assistants to provide candidates with fast, personalized application information and support.

- Employee training and development: Generative AI can also be used to customize training programs based on employees' needs, matching training content with precision to achieve personalized customization of training products. Meanwhile, integrating internal and external training resources will allow a company to generate targeted content and aggregate training products/content resources, as well as adopting VR/AR and other technologies to create immersive learning experiences for employees and enhance interactivity. Additionally, they can also use generative AI to track employees' learning progress and effectiveness in real time and provide instant feedback and suggestions.

- Performance management: This can be enhanced by combining generative AI's analysis of factors like corporate strategy, organizational goals, team goals with job requirements and individual capabilities to help managers set performance goals more scientifically for employees. Also, managers can use generative AI and employee history data, work performance and results, to provide more targeted performance coaching. This will help employees identify problems and adjust personal development directions in a timely manner, achieving rapid performance improvement and fast personal growth.

- Compensation and benefits management: Generative AI can also be used to conduct salary benchmarking tests by analyzing external market data and workforce data to gain insights into competitive remuneration, incentives, rewards, and other benefit plans. Also, using automated salary calculations to reduce manual input and calculation errors will enable quick and accurate salary, bonus, subsidies, and benefit calculations and save time.

- Employee relations management: Generative AI can be deployed for big data analysis and modelling of employees' work directions, learning habits, career planning, hobbies, daily habits, social interactions, consumption data, and the like, facilitating personal profile tagging and generating personalized employee care plans.

Life Science & Healthcare

AI drives innovation in the drug industry

The cross-industry integration of artificial intelligence (AI) and biopharmaceuticals continues to accelerate, increasing safety, accuracy and efficiency in the production chain. During this year's ‘Two Sessions’, innovative drugs were included in the list of ‘new high quality productive forces’ in the economy for the first time, and the drum beat for "full-chain support for innovative drug development" sounded ever louder. As a tool for innovation, AI is showing great application value from top to bottom of the value chain of innovative drugs, particularly in the improvement of R&D efficiency and in accelerating the capture of market opportunities. The integration of generative AI, we believe, will eventually improve the competitiveness of pharma companies across the board.

The R&D of AI Drug Development (AIDD) continues to gain momentum, with more local players joining the field

AI technology has been gradually integrated into all aspects of innovative drug R&D with high application value. It is bringing about significant efficiency improvements and innovation breakthroughs in drug R&D activities. The integration of AI technologies is also expected to address the issue of high investment, high risk and long R&D cycles and in traditional drug R&D. According to a Qibitai forecast, the size of China's AI pharmaceutical market, which in 2022 was estimated at around RMB 2.7 billion, is expected to hit RMB 204.0 billion by 2035, a gigantic growth potential. This breakneck growth will arise mainly from its wide range of application fields and application values. AI shows great potential in the following areas:

- Drug R&D: Accelerating the drug R&D process by properly handling and designing molecule structures, as well as predicting drug characteristics.

- Diagnostics: Identifying more granular images and gene mutations to improve disease screening and covering more disease areas.

- Clinical Trials: Assisting in clinical trial protocol design, patient enrolment, surveillance, pharmacovigilance, and so on.

- Supply Chain: Identifying and monitoring system issues in the drug manufacturing process, shortening batch cycle length, and enhancing drug safety and quality.

- Commercialization: Developing and accelerating promotion and marketing campaigns and improving promotion content accuracy.

From 2019 to 2023, the number of AIDD-related deals has increased steadily around the globe. The number of AIDD deals of overseas and local companies increased from 10 and 2 deals in 2019 to 39 and 21 deals respectively in 2023. As of November 2023, there are more than 90 AI innovative drug start-ups in China, among which Insilico Medicine and XtalPi, the two leaders in the sector, have submitted IPO applications. Most of the AI pharmaceutical companies are based in the economically developed provinces, especially in the Yangtze River Delta region.

Accelerated cross-industry integration enables the iterative upgrade of the innovative drug industry

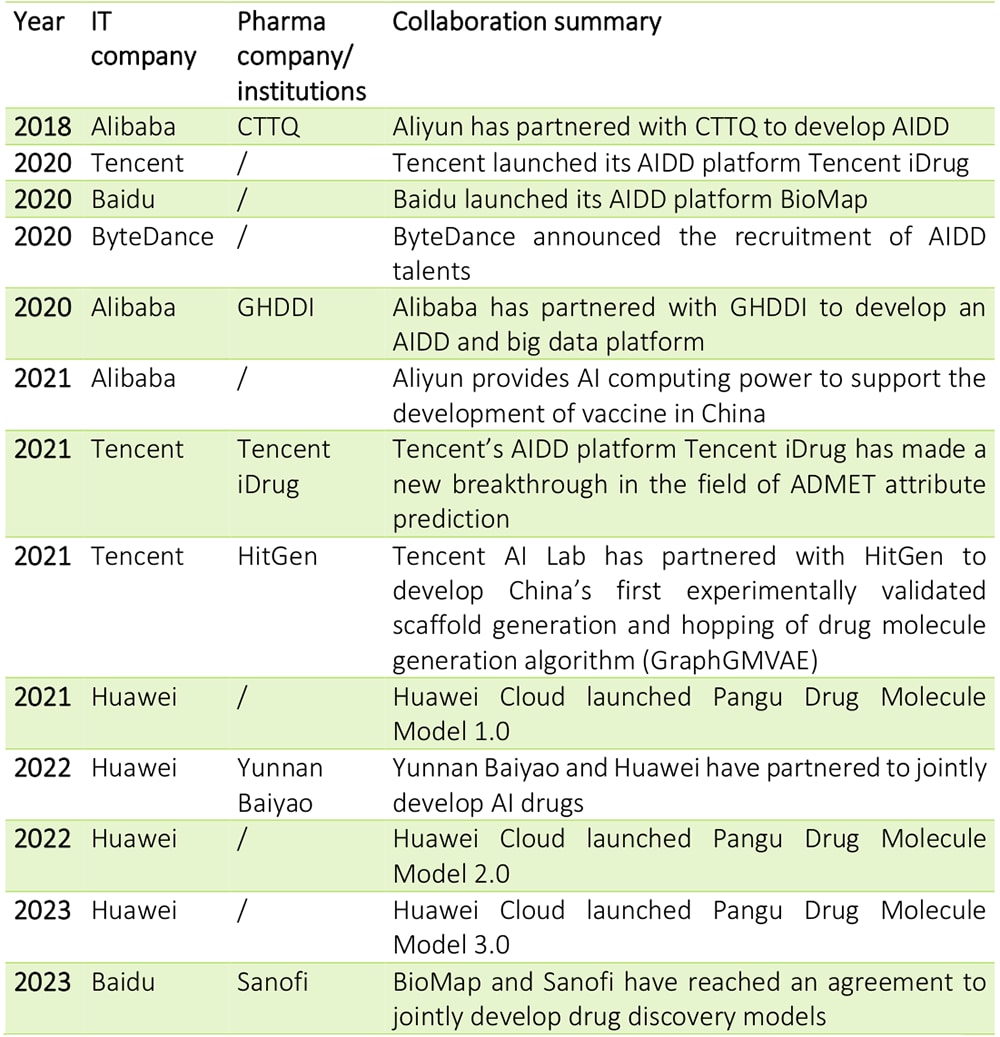

Several IT giants are accelerating deployment in the innovative drug industry. They have already reached a few strategic collaborations with innovative pharmaceutical companies (Table 1) to explore the possibility of “AI+ new drug R&D”. Compared with the US and Europe, the collaborations between Chinese large pharmaceutical companies and AI companies started late, indicating that Chinese pharmaceutical companies are still relatively conservative in the use of AI technology. As early as 2014, Google entered the AI pharmaceutical field through the acquisition of DeepMind. Nvidia and IBM also entered the AI pharmaceutical field in 2018. In China, on the other hand, the collaboration between AI companies and pharmaceutical companies only started since 2018.

Table: The deployment of Chinese IT companies in the AIDD field in recent years

Source: Public info, Deloitte Research

Source: Public info, Deloitte Research

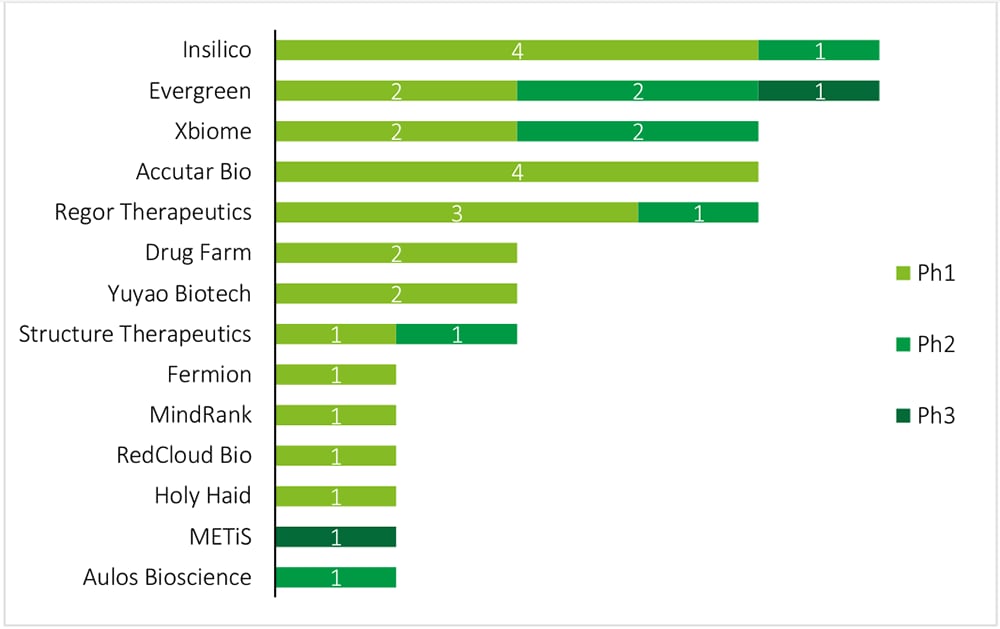

Although they were late starters, Chinese AI pharmaceuticals have developed rapidly. According to public data, 14 of the 93 Chinese AI pharmaceutical companies in 2023 have successfully advanced their pipelines to the clinical stage (refer to the figure below), including many self-developed products. The R&D capability of China’s AI pharmaceutical companies has improved significantly, among which Insilico Medicine and Evergreen have the largest clinical product pipelines in China (as of January 2024).

Figure: Pipeline AI drugs approved for clinical trials in China, by clinical study stage

Source: Yaozhi, Deloitte Research

Source: Yaozhi, Deloitte Research

AI technology is accelerating the transformation of the innovative drug industry, ushering in a new era for the development of novel drugs

All in all, even though China’s AIDD industry started later than its overseas counterparts, it is moving fast to catch up, leveraging the advanced digital technology available domestically. AIDD has ushered in a new innovative drug R&D model which has brought about significant changes to the innovative drug industry and has huge market potential. AIDD is expected to become the next industry growth driver.

Automotive

Flying cars are taking off with the rise of the "low altitude economy"

As one of the revolutionary technologies reshaping future transportation, flying cars are experiencing a momentous shift, moving from 0 to1 in terms of feasibility and actualization. In March 2024, the Chinese government for the first time included "low-altitude economy" in its Government Work Report, elevating it to a national strategic level. Local governments are actively following suit, with 26 provinces and cities drafting provisions for the development of the low-altitude economy in their government work reports.

The low-altitude economy encompasses unmanned aerial vehicles, helicopters, and flying cars. Broadly speaking, flying cars can be classified into electric vertical takeoff and landing (eVTOL) aircraft and “flying cars” (it has two-part design that allows the aircraft to seamlessly switch between land and aerial modes). Compared to traditional helicopters, flying cars have certain advantages such as lower noise, environmental friendliness (eVTOLs emit 77% less CO2 than fossil fuel powered helicopters), and higher cost-effectiveness. In comparison to road transport, flying cars offer higher speeds, faster point-to-point passenger transportation services. Flying cars can also significantly improve traffic efficiency and reduce road congestion to a certain extent.

The combined forces of industry, technology, capital, and policy are driving the rapid development of flying cars in China.

- Industry: Flying cars, as a cross-industry product of aviation and automotives, are attracting active participation from aviation manufacturers and automakers. Currently, there are over 300 eVTOL companies worldwide, mainly comprising civil aviation companies, automakers, and startups. Global carmakers such as Toyota, Hyundai, Daimler and Chinese domestic counterparts such as Xiaopeng, Geely, and GAC, have all joined the "flying car" race. The entry of carmakers takes the form of in-house R&D, equity investment/acquisition, and strategic cooperation. Geely acquired the US flying car company Terrafugia in 2017, and later invested with Daimler in the German company Volocopter and established "Volocopter China" in 2020. Xiaopeng acquired the startup Huitian Aerospace in 2020 before forming "Xpeng Huitian. For automakers, eVTOL shares some similarities with the NEV industry chain as they both need a powertrain system - batteries, motors, and power controls, as well as intelligent devices like millimetre-wave radars. Automakers can leverage their expertise in the R&D and manufacturing of the electric vehicles and autonomous driving systems to accelerate the development of flying cars. Furthermore, flying cars have pushed battery manufacturers to focus on developing aviation-grade high-energy density batteries. In April 2023, CATL released its solid-state battery with a single-cell energy density of up to 500Wh/kg, collaborating on the development of civilian electric manned aircraft projects and executing aviation-level standards and tests.

- Technology: In this area, we are already seeing a progression from feasibility verification to flight testing and aircraft certification. The development of eVTOL can be divided into four stages: conceptual design, scaled prototype testing, full-scale prototype testing, and prototype flight testing. According to the Vertical Flight Society, one fourth of eVTOL projects globally are currently in the flight-testing stage. Leading flying car companies such as Joby, Volocopter, Lilium, Vertical, EHang, and Volocopter China have all unveiled full-scale prototypes and conducted their maiden flight tests in 2023. Since 2024, eVTOL manufacturers around the world have been accelerating their certification processes in an effort to become the first in the world to obtain airworthiness approval from aviation authorities.

- Policy: eVTOL occupies a unique niche in the aviation industry, distinct from both helicopters and civil aviation aircrafts. This means that existing policies and regulations will be not suitable to meet the development of these emerging aircrafts. However, regulations surrounding the low-altitude economy are taking shape. Civil aviation regulatory bodies around the world primarily focus on airworthiness approvals and low-altitude airspace management. However, different countries have different regulatory regimes and varying degrees of regulatory rigor. Europe is the frontrunner in laying the legal groundwork for the development of eVTOLs as the European Aviation Safety Agency issued in 2019 the Airworthiness Certification Framework for Novel VTOL Types. This framework provides guidelines for manufacturers and sets the highest safety standards for manned eVTOLs, equivalent to those of civil aviation passenger planes. The US Federal Aviation Administration (FAA) tends to set safety standards equivalent to those for helicopters in terms of airworthiness certification. China has not yet established industry standards for eVTOL, although the Civil Aviation Administration of China (CAAC) has issued guidelines focused on special operational approval risk assessment systems and "special conditions" for eVTOLs. In October 2023, the CAAC issued the world's first Type Certificate for an eVTOL project.

- Capital: The eVTOL industry attracted $4.5 billion in investment from 2010 to 2020. In 2021, the investment amount and the number of investments in this field reached a record high, primarily due to Joby, Archer, Lilium, and Vertical Aerospace going public through special purpose acquisition companies (SPACs), raising $2.8 billion in total. The low-altitude economy has become an emerging hotspot in the capital market. Private eVTOL companies continue to raise funds through venture capital, and strategic investments. In the secondary market also, the low-altitude economy has become a popular sector. In the first quarter of this year, the flying car (eVTOL) sector rose by 30%, outperforming other popular themes on the Shanghai Stock Exchange.

Can flying cars become mainstream?

Taking to the skies is just the first step. For flying cars to become a safer, more affordable, and more efficient mode of transportation, manufacturers need to overcome multiple hurdles, including commercialization, technology, and regulation.

- Key technological challenges: Despite the technological advancements in eVTOL, there are still some critical challenges that need to be overcome. These include battery range and lifespan, situational awareness and advanced detection, and collision avoidance system design. For example, electric aircraft require power batteries with higher energy density, longer life cycles and increased safety when compared to electric cars. Currently, the energy produced by power batteries is insufficient to meet the demands of long-distance commuting, and the charging speed does not support high-frequency ride-sharing services. Additionally, as eVTOL evolves towards automation, it needs to perceive its surroundings in real time at the same level of accuracy as autonomous vehicles. This requires them to have deep learning neural networks to identify objects, utilize maps for navigation, and plot the best flight path in the air. Furthermore, advanced detection and collision avoidance systems are necessary for eVTOLs, enabling them to see farther and accurately detect and measure objects over longer distances. There are enhanced detection and collision avoidance technologies such as microwave or millimeter-wave technology but these will have to be developed further. Furthermore, they must make real-time decisions in unsafe operating environments and ensure safe flights in adverse weather conditions.

- Economics presents another challenge for eVTOLs: eVTOLs offer significant time efficiency advantages over ground transport but as long as passenger loads are low, they will be far more expensive. Currently, eVTOLs have achieved a cruising speed of around 200 kilometers per hour, far exceeding the average ground transportation speed of approximately 40 kilometers per hour. This makes eVTOLs commercially viable in scenarios such as passenger transportation (e.g., scenic tours, intercity air travel, airport shuttles, and air taxis), cargo transportation (e.g., cargo transport and short-haul delivery), and public utilities (e.g., medical and firefighting rescue operations). However, for eVTOLs to compete with existing urban public transportation systems, they must improve their economic viability. Over time, lower prices per seat may generate more demand, leading to high passenger load rates, as consumers are willing to pay for faster transportation. This is expected to be one of the major factors driving the commercial application of urban aerial transport.

In addition, the large-scale commercialization of eVTOLs also faces challenges in air traffic management, such as coexistence of these aircrafts in airspace with existing commercial and civilian airplanes, helicopters, and drones. Public acceptance can also be a hurdle, as consumer’s have a low opinion of eVTOLs' safety, convenience, and pricing.

Nevertheless, as many orders have been placed by air operators for passenger and cargo transport (as of the end of 2022, operators have ordered approximately 7,000 eVTOLs), pilot projects are expected to surge in 2024 to further demonstrate the feasibility of commercialization. The acceleration of global regulations will push the eVTOL industry from speculation to the eve of mass commercial production.

Logistics

Overseas warehouse development: differentiation and digital intelligence

Overseas warehouses will become the preferred fulfilment model for cross-border e-commerce companies

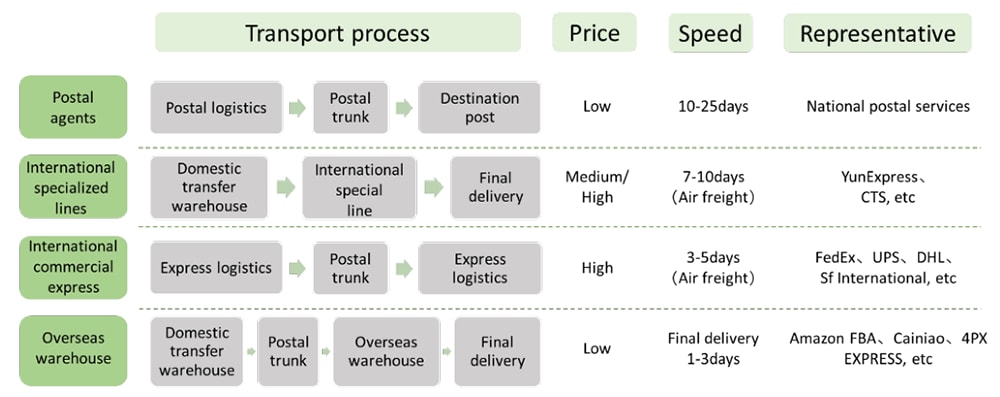

Cross-border e-commerce has become an important factor in China's foreign trade growth. According to data from the General Administration of Customs, cross-border e-commerce (import and export) amounted to RMB 2.38 trillion in 2023, marking a year-on-year growth of 15.53%. The logistics market has grown in tandem, an important support for the burgeoning cross-border trade. It was estimated at about RMB 756.3 billion in 2023, an increase of 11% year-on-year. At this stage, cross-border logistics can be divided into four categories: direct mail mode through postal agents, international commercial express mode, specialised international lines mode, and overseas warehouse mode (see the figure below). Amongst them, benefiting from the scale effect and geographical location, overseas warehouses have the clear advantages in terms of cost and speed. It is anticipated that the warehouse mode will become the preferred mode of transport for cross-border e-commerce in the future.

Figure: Comparison of cross-border logistics types

Source: Publicly available information, Deloitte research

Source: Publicly available information, Deloitte research

Overseas warehouse market sees overall stable development and particularly strong growth in Southeast Asia

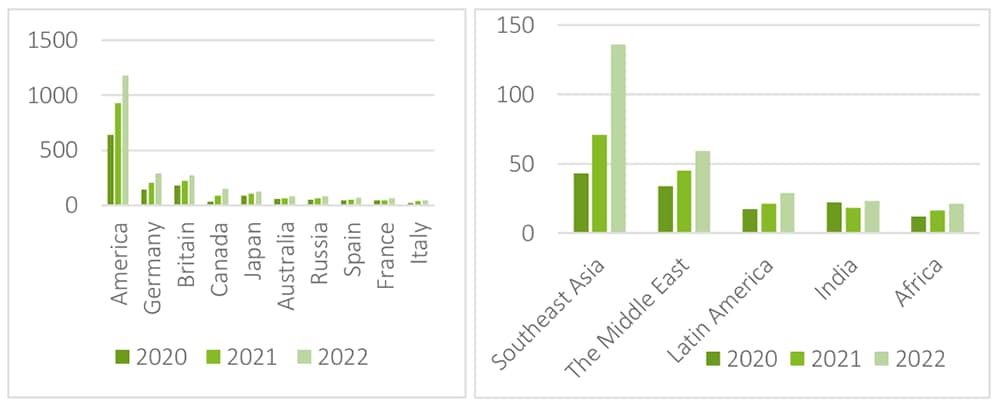

China's overseas warehouse market is booming. According to data from the Ministry of Commerce, as of January 2024, the number of overseas warehouses built by Chinese enterprises had exceeded 2,400, with an area of more than 25 million square metres. Moreover, overall growth has remained stable. From the perspective of cross-border e-commerce export destination countries/regions, the United States and Europe account for a high proportion, while emerging markets such as Southeast Asia, the Middle East and Africa are in a phase of rapid development too, with strong potential for further growth. Data from the 2023 Overseas Warehouse Blue Book shows that the number of overseas warehouses in major countries and regions increased by 30.17 percent year-on-year in 2022. In emerging markets such as Southeast Asia, the Middle East and Latin America, the number of overseas warehouses totalled 268 by the end of 2022, up 57 percent year-on-year. This is mainly thanks to the Regional Comprehensive Economic Partnership Agreement (RCEP) which went into effect on January 1, 2022, tax cuts and other preferential treatments further reduced the cost of going overseas for cross-border e-commerce sellers. This, coupled with the further increase in market demand, indicated that there is plenty of opportunities for growth for overseas warehouses.

Figure: Number of overseas warehouses in major exporting countries for cross-border e-commerce vs. number of overseas warehouses in emerging markets

Source: Ministry of Commerce, Cross-Border Eye Insight's Overseas Warehousing Blue Book 2023

Source: Ministry of Commerce, Cross-Border Eye Insight's Overseas Warehousing Blue Book 2023

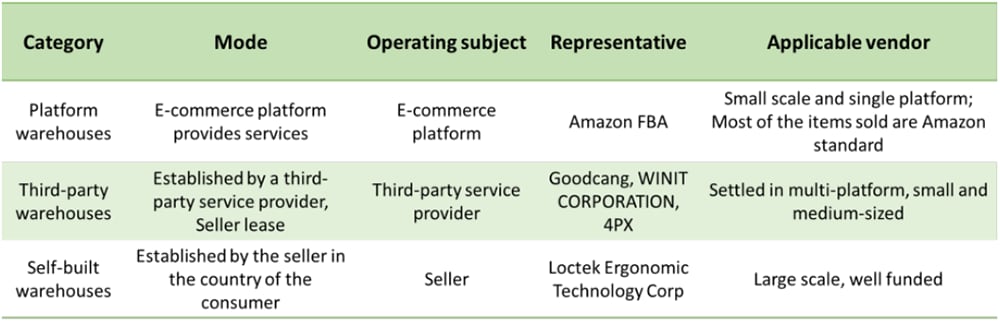

From the point of view of warehouse operation, overseas warehouses can be divided into three categories: platform warehouses, three-party warehouses, and self-built warehouses (see Figure 3). The platform warehouse is represented by Amazon FBA, which can provide high-quality and efficient support services, but the storage and distribution costs for non-standard-size pieces are high, and it does not support other e-commerce platforms; the third-party warehouse, as the name suggests, is provided by a third-party service provider, namely Goodcang, WINIT and 4PX, which have high comprehensive barriers. Sellers can get cross-border logistics one-stop service at relatively low cost, but their degree of control is low. The self-built warehouse givers sellers much more control but as it is established by sellers at their own expense (Loctek Ergonomic Technology Corp is a case in point), but the construction and operation costs are high, suitable only for sellers with large volumes and sufficient capital. In the Southeast Asian market, platform warehouses and three-party warehouses are actively battling for the Southeast Asian market, such as Shopee and Lazada. Other Southeast Asian e-commerce platforms are also accelerating the deployment of overseas warehouses.

Figure: Comparison of overseas warehouse types

Source: public information, Deloitte research

Source: public information, Deloitte research

Overseas warehouse development still needs to enhance differentiation and smart features

Overseas warehouses, as the core hub of cross-border e-commerce serving the international market, face two major developmental challenges.

Challenge 1: Shortage of high-quality services and lack of specialised and integrated facilities.

Since 2020, overseas warehouses have entered the stage of crude high-speed expansion with rapid increases of scale. However, follow-up service still fails to meet the needs of merchants, mainly because 1.) sellers have gradually shifted their focus to featured services, and there is more differentiation now in the storage and transport conditions for commodities of different natures; 2) most of the overseas warehouses are still confined to the function of warehousing, and awareness of integrated services is sorely lacking.

Solution: Service Differentiation. Overseas warehouse customers are of various types with different needs, and the storage and transport conditions differ for different categories of commodities. By considering the unique characteristics of commodities and customer types, optimization in warehouse design, inventory management, and returns management can provide customized professional services for specific vertical categories. This approach could serve as a breakthrough method for overseas warehouses. Take the case of Cainiao. Cainiao forged a global partnership with Lin's Home to provide comprehensive, end-to-end solutions for overseas warehouses specializing in bulky goods, including first-mile delivery, overseas warehousing, and final delivery. In the case of furniture, the Cainiao big data team has increased the loading rate of ocean freight containers by 15% with the help of simulated loading algorithms and customised equipment, greatly improving the operational efficiency of warehouses for bulky commodities.

When it comes to further integration, enterprises should pay close attention to the upgrading of customer demand and build a reliable and resilient end-to-end supply chain. They should provide customers with integrated supply chain solutions ranging from international trunk transport, overseas customs clearance and warehousing to final delivery. JD Logistics are a good example of this. JD has built a global supply chain network which includes an overseas warehouse network, international forwarding hubs, and local transport and distribution networks in overseas countries as well as a transnational trunk line transport network. In this way they are able to provide customers with end-to-end full-chain services and comprehensively improve the operational efficiency of their overseas logistics.

Challenge 2: Overseas warehouses are in dire need of upgrading their digital capabilities to improve capacity utilisation and turnover.

Compared with ordinary warehouses, running overseas warehouse services are a far more difficult and complex matter with information challenges and high running costs. Hence cost reduction and efficiency are the core requirements of overseas warehouses. With high labour costs in overseas markets (especially in Europe and the United States), automated operations can enhance the use of storage capacity and save labour costs. Also, as customers pay more for overseas warehousing, they have higher expectations and more requirements for the performance of overseas warehouses. As competition has intensified after the epidemic, overseas warehouses urgently need to assist and replace manual work with digital intelligence so as to achieve higher order processing speed and accuracy.

Solution: Warehouse Intelligence. Digital technology can significantly improve the operation and management of overseas warehouses through ameliorating the usage rate of storage capacity and the accuracy rate of orders. It can also provide users with real-time information on the status of their orders as well as on the progress of returns and exchanges through the real-time mastery of inventory data. The overseas warehouse of Goodcang is a case in point. After digitizing their operations their order correctness rate increased to 99.5 per cent, the inventory correctness rate to 99.7 per cent, and the storage capacity utilisation rate increased by 15 per cent.