Perspectives

The Deloitte Research Monthly Outlook and Perspectives

Issue 91

China's economic and industry outlook for 2024

Published date: 2 July 2024

Economy

Recovery on track, but protectionism looms large

Following the release of Q1 economic data, this year's GDP growth target of 5% seems like a foregone conclusion. However, is this still the case considering mixed data of late, especially in May, and the external uncertainties caused by persistently high US interest rates, an overwhelmingly strong dollar, the fog of war in Europe, and tensions in the Middle East? Not to mention the looming threat of protectionism which has been present in both developed and emerging economies, and could receive an additional boost in post-election Europe where the far-right is gaining ground.

Let's take a closer look at the data for May. As anticipated, exports continue to boom. May exports increased at a brisk pace of 7.6% and 11.2% year-on-year in dollar and RMB terms, respectively. China's export machine has been supported by the recovery of regional trade. For instance, newly industrialized economies such as South Korea and Taiwan have witnessed a strong rebound in exports, particularly in electronic-related products, thanks to surging corporate demand for technological goods (China's exports to Korea and Taiwan increased by 3.6% and 25.5%, year-on-year in May, respectively). China's export competitiveness has also triggered a wave of tariffs from several countries. For example, Turkey surprisingly imposed a 40% tariff on Chinese vehicles starting from July 7, and Mexico has imposed temporary tariffs ranging from 5% to 50% on the import of 544 tariff items from countries with which it does not have trade agreements, including China. The key question now is whether the European Union's proposed tariffs against Chinese electric vehicles would provoke retaliatory actions from China, potentially leading to a mini trade war between China and its largest trading partner.

Additionally, as expected, weak housing data has persisted. Housing investment in January to May has fallen by 10.1% year-on-year, and new home sales in the same period have dropped by 27.9% year-on-year. The good news is that home prices have stabilized following an unprecedented housing relief package on May 17. Specifically, the initial down payment has been lowered to 15% (previously it was easily above 30%), and commercial banks will have more flexibility to reduce mortgage rates. On the demand side, first-tier cities have further eased restrictions, while most restrictions on purchases in the rest of the country were lifted earlier. Local governments have introduced various innovative methods to reduce housing inventories. However, we believe the government could have done more to stimulate the housing market, where consumers have invested a significant portion of their wealth. Stamp duties could have been reduced, and more importantly, there is room for the People's Bank of China (PBOC) to cut short-term interest rates. The PBOC's decision-making on interest rates is clearly being influenced by the Federal Reserve and the foreign exchange market. Meanwhile, the credit market has priced in one cut of the Fed Fund Rates (likely in Q4 of 2024), compared to four cuts at the beginning of 2024. The Fed's recent decision to leave interest rates unchanged in the most recent FOMC meeting has not deterred several major central banks from making their first rate cut in the post-Covid era (e.g., the European Central Bank, the Bank of England, and the Riksbank of Sweden). Such divergence in setting short-term interest rates has naturally reinforced the strength of the US dollar. In short, with both US dollar interest rates and the value of the dollar expected to continue on a trajectory of "higher and longer", central banks in Asia, including the PBOC, are expected to maintain their current monetary stance. Therefore, the PBOC's reluctance to cut interest rates is understandably unless the RMB exchange rate is allowed to fluctuate within a wider range. Despite a sluggish housing sector, signs of a tentative cyclical recovery are visible, as evidenced by a pick-up in retail sales (3.7% year-on-year in May compared to 2.3% year-on-year in April). This suggests that broader consumption recovery, similar to the one observed during the Dragon Boat Festival in June (where travel activities have surpassed pre-Covid levels), remains on track.

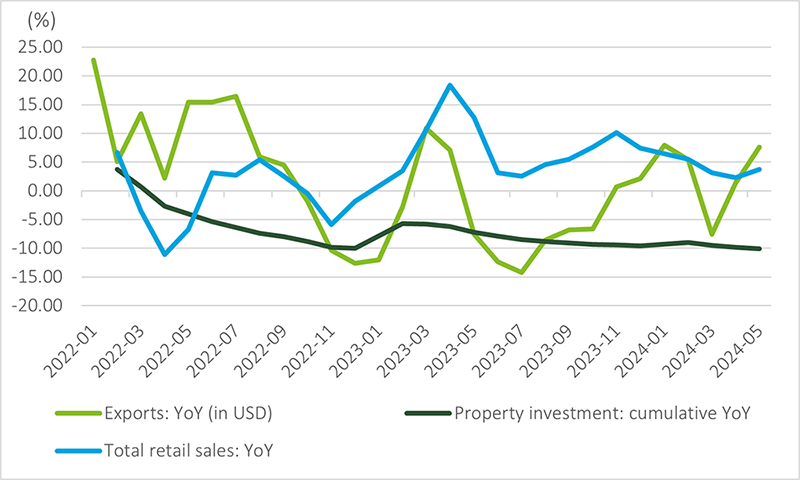

Chart: Sluggish housing investment partially offset by booming exports

Source: Wind

Source: Wind

All in all, the 2024 growth target of around 5% is indeed within reach, despite the mixed economic data in May. Additional stimulus may be necessary to offset potential external shocks which could impact policy decisions. Is Brussels' action of imposing tariffs against Chinese EVs considered an external shock? The answer is both yes and no. In this publication, we have consistently argued that the automotive and related sectors are considered strategic by several EU member states, unlike solar panels. In 2012, the influx of Chinese solar panels led to tariffs being imposed due to allegations of dumping. EVs have presented a complex issue precisely because they are crucial for the EU's energy transition. However, the cost disparity between Chinese EVs and those produced locally in Europe is simply too significant. Prior to the EU's announcement, we believed that tariffs ranging from 10-15% would have had little impact, while tariffs exceeding 30% would have signaled an escalation. According to the press release Electric vehicle value chains in China (europa.eu), there will be an average tariff of 21% imposed on Chinese EVs on top of existing import duties, effective from July 4. BYD, China's largest EV maker, will face a 17% tariff, while SAIC, the second largest, will be subject to a 38% tariff. Many questions have arisen due to the wide range of tariffs imposed on various EV makers. The EU has explained that the calculation of tariffs was based on the degree of subsidies from the Chinese government. This implies EU policymakers have not given state-owned companies such as SAIC the benefit of the doubt. Meanwhile, the share prices of Chinese EV makers, especially BYD, have rallied on the assumption that a major uncertainty has been removed and that such tariffs will not undermine their competitiveness. Investors may also have taken a positive view regarding the risk of further escalation should tit-for-tat measures be taken by the Chinese government. In fact, China's Ministry of Commerce (MOFCOM) launching an anti-dumping investigation against imported pork and byproducts (worth about $3 billion in 2023) reflects China's measured responses.

In conclusion, recent economic data does support the hypothesis of a tentative cyclical recovery, but further policy support for the housing sector remains crucial for the revival of both investment and consumption. The EU's tariffs will serve as another catalyst for Chinese companies to link their overseas expansion to job creation in local economies.

Financial Services

Adapting to the new normal

The year began on a good note with economic operations in Q1 of this year off to a good start. But by April important financial data had come in that indicated a slowdown. In response, statements began to emerge of squeezing the “excess water” out of and/or trimming the financial sector and showing a “positive attitude” towards industry. But why is financial activity weak at a time when the economy and domestic demand is gradually recovering? The answer lies in this: the financial system is not slowing down so much as it is undergoing a transformation. A qualitative shift has taken place in financial activity with money being targeted not at producing a higher quantity of goods but at the development of higher quality goods. The activity slowdown is a signal of structural adjustment in the financial sector, a 'pruning' one could call it, which will lead to an improved efficiency of capital use and high-quality development.

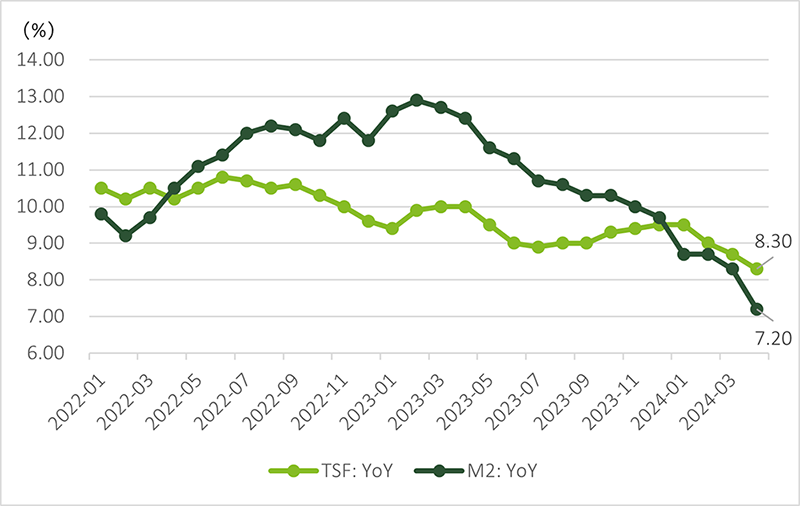

The growth of monetary aggregates is slowing down.

Monetary and financing growth continued to hit record lows in April. Specifically: 1) The growth rate of M1 and M2 in April was -1.4%, and 7.2% respectively. 2) Total Social Financing (TSF) recorded a negative single-month growth for the first time, and the stock of TSF increased by 8.3% year-on-year. The weak TSF was the result of a reduction in government bond issuance in April, at a time when household loan demand had also remained weak.

Money supply refers to the total volume of money held by the public at a particular point in time. This is the sum of the financial instruments that support the means of circulation and payment at any point in time. Narrow money (M1) is cash plus unit demand deposits, which is an indicator of the degree of liquidity of capital. Broad money (M2) is M1 plus fixed-term deposits and household deposits. M2 includes bank loans and sums borrowed through other channels. So, the deceleration of M2 growth in April in relation to its growth in the previous year is a more accurate reflection of the actual weakening of domestic demand in the economy.

Credit growth turns into a demand constraint.

In the past two years, M2 had been growing more slowly than the stock of TSF. This intuitively reflected the oversupply of money, a situation that continued until January this year when TSF growth, which had continued to grow slowly, exceeded the growth of M2. But this has happened within the envelop of a significant overall deceleration in the growth of both indicators.

With the sharp adjustment (by policymakers) of the real estate market, the debt-driven economic growth model of the past no longer holds sway. As a result, real estate and local financing platforms have undergone significant changes. Heavy industries that traditionally relied on credit have become saturated with excess capacity, so credit growth is now coming increasingly from the service sector as the development of the asset-light service industry accelerates. As a result, the demand for credit is having to be adjusted accordingly. A just-released PBOC report highlighted this, and urged financial institutions to adapt to the changing nature of credit growth which is increasingly being determined by demand, as opposed to supply, constraints. This signals that the volume of credit disbursed should now be considered a less important indicator of performance than the quality of credit, as reflected by its returns.

This year, the government set the goal of "matching the money supply and scale of social financing with the expected targets of economic growth and price levels". With the gradual restoration of aggregate demand and market confidence, TSF and price levels have shown a steady improvement. The government has welcomed the change of direction in the CPI, which has just gone from negative to positive, but cautioned that the rise should be modest so that it does not breach the target rate of "around 3%" for the whole year.

Figure: historical lows of both TSF and M2 growth

Data Source: People's Bank of China

Data Source: People's Bank of China

Deposits need to flow.

In the process of economic cycles, money is flowing through and amongst enterprise investment, household consumption, and fiscal revenue and expenditure. Growing uncertainty about the future makes people cut back on consumption to safeguard their savings.

There has therefore been a marked increase in the propensity to save, and a corresponding decline in the purchase of homes after the COVID pandemic. PBOC's Monetary Policy Implementation Report Q1 2024 estimated that of the total deposits of about RMB 296 trillion, residents, enterprises and governments accounted for 49%, 27% and 14%, respectively (the remaining 10 percent was accounted for by non-banking institutions and other local bodies). Compared with the data before the pandemic, household deposits were up 7.1 while the other two were down 4.2 and 3.3 percentage points, respectively.

This explains the preponderance of bank deposits in M2, which is a result of the large increase in the amount of capital that is lying dormant in the banks. Therefore, it is not the money stock that is in short supply but the decline in the efficiency of capital that is responsible for the slowdown of the economy. This has led to the adoption a multi-pronged strategy to improve the atmosphere for investment:

1) on the one hand, banks have been required not to engage in what is called "manual interest compensation" operations and to stay within the upper limit of deposit interest rates (thereby lowering the attractiveness of bank deposits by a given deadline); to reduce high-interest-paying liabilities, and to guide some deposit funds to transfer to off-balance sheet WMPs (wealth management products), monetary funds and other fields.

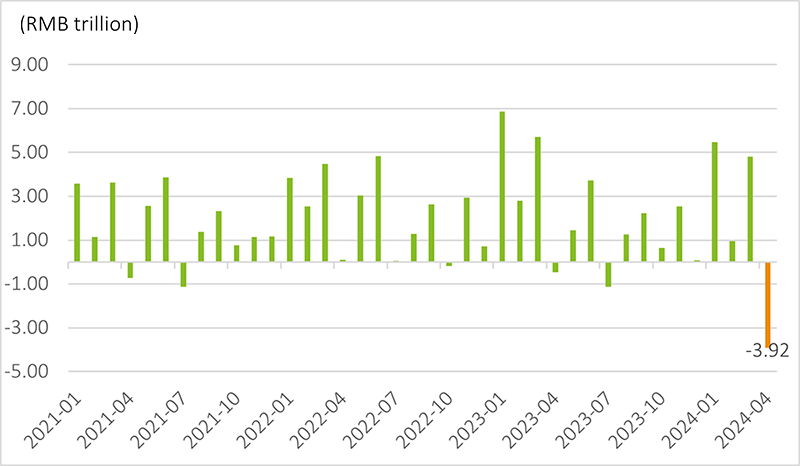

2) In Q1 of this year, the accounting method for measuring value added by the financial industry (VAFI) was adjusted, to reflect performance in contrast to promise. Bank Regulators were asked to use the growth of net income, (including net fees and commissions and the like) and not the growth rate of deposits and loans to evaluate their performance and their contribution to the GDP. The new method will not only discourage giving high risk loans to improve performance figures, but also compel the banking sector to focus on improving the efficiency of the use of funds. These directives have already led to a sharp decrease in deposits of RMB 3.92 trillion in a single month in April, the sharpest decrease in history since the collection of such statistics. This is an unambiguous indicator of the regulators' determination to reduce the dormant capital pool and to enhance the efficiency of capital turnover.

Figure: single-month negative deposit growth (historic low)

Source: PBOC

Source: PBOC

The benign substitution effect of direct financing

Credit is only one channel in the TSF toolbox. Proper financial support for the real economy requires a balance between direct and indirect financing. The vigorous development of high-tech innovative enterprises requires a financing method that understands the inherent nature of the business - high risks but high yields, heavy knowledge content and light collateral assets. Direct financing such as raising equity capital is one good method.

With the weakening of the correlation between credit loans and economic growth, enterprises must rely more on active direct financing, corresponding to the huge bond and stock market. The new "Nine Guidelines" will promote better capital allocation. It will also guide financial institutions to a better understanding of the changed nature of the economy.

Energy

Sailing towards a greener future with sustainable marine fuels

The shipping industry accelerates the pace of decarbonization

As a pillar of the global economy, the shipping industry accounts for over 80% of the world's trade volume, but also emits around 3% of global greenhouse gas emissions (GHG). Over the past decade, the industry's emissions have risen 20% . To accelerate the decarbonization process of global maritime transport, the International Maritime Organization (IMO) revised its GHG emissions reduction strategy in July 2023, pledging to reach net zero by or around 2050. In Europe, the shipping industry was included in the EU's Emissions Trading System (ETS) from 1 January 2024, which means shipping companies must purchase emission allowances for specific ships entering or leaving EU/EEA ports. This has made it even more necessary for the shipping industry to cut emissions.

One way to do this would be to use sustainable fuels. Promising sustainable marine fuels include green methanol, green ammonia and biodiesels. These fuels, which can be produced from synthesized hydrogen and captured CO2 or from biomass such as waste oils, fats, and agricultural residues, can help cut ship emissions to nearly zero or net zero. According to the IMO's emission reduction strategy, clean fuels and decarbonization technologies should account for at least 5% of total energy consumption in international shipping by 2030, and the industry should strive to reach 10%.

Leading shipping companies accelerate the transition to sustainable fuels

Leading shipping companies have already started taking action. The Danish shipping giant Maersk has set an ambitious target to achieve net zero by 2040, the adoption of green fuels playing a key role in its decarbonization strategy. The company has invested billions of dollars to build a green fleet of about twenty methanol-powered vessels. To secure a green fuel supply for its fleet, Maersk developed a variety of commercial partnerships. At the end of 2023, it signed the world's first large-scale green methanol offtake agreement with the Chinese clean energy company, Goldwind, for an annual volume of 500KT. Production is expected to begin in 2026.

There has also been an acceleration in the development of Ammonia-fueled ships. The Japanese shipping company NYK recently announced plans to convert an LNG fueled tugboat to ammonia. Overall, we are seeing an increase in the demand for ammonia capable vessels in recent years.

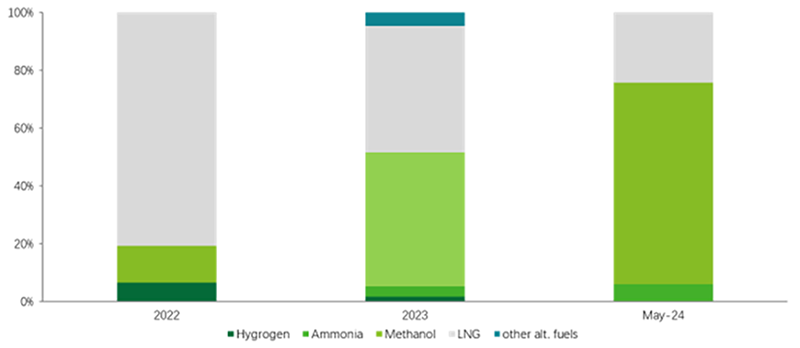

Figure: Alternative fuel mix in new shipbuilding contracting

Source: DNV, Deloitte research

Source: DNV, Deloitte research

The surge in demand for sustainable marine fuels sees supply struggling to keep pace

With the rise in orders for green ships, demand for sustainable marine fuels has increased, attracting many companies into the sustainable marine fuels market. As the world's largest producer of methanol and ammonia, China produces a substantial portion of global sustainable fuels. With steady cost improvement and strong policy support, the market share of Chinese companies is likely to increase rapidly. Currently in China announced capacity for green methanol has exceeded 9 million tons per year, and for green ammonia, capacity has exceeded 4 million tons per year.

But even so, there is still a huge lag in the supply of sustainable fuels. DNV estimates that to achieve the net zero target set by the IMO, an annual supply of 250 Mtoe (million tons of oil equivalent) of sustainable fuels is must be in place by 2050. And fierce competition for sustainable fuels from other "hard-to-abate" sectors cannot be overlooked.

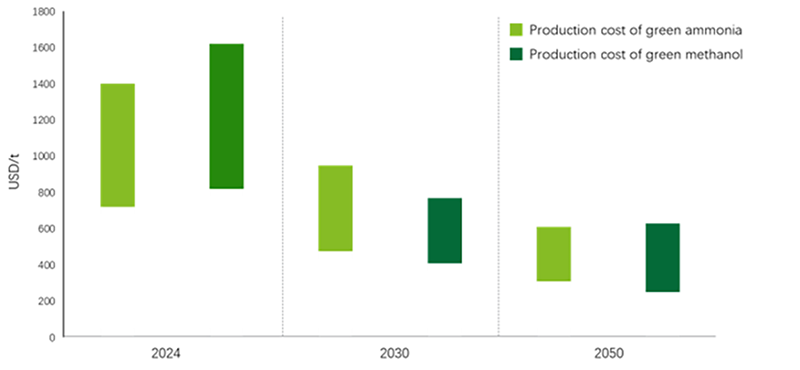

The scaling up of sustainable fuel production faces multiple challenges. First, the cost of producing sustainable fuels is much higher than that of traditional fuels, while clear cost-sharing mechanisms between shipping companies, cargo owners and end-consumers have not been put in place. Hence, investor confidence in the market's ability to bear these costs is low.

Figure: Cost trend of sustainable fuels

Source: Irena, Deloitte research

Source: Irena, Deloitte research

Second, there is still no clear frontrunner among the different green fuel types. Green methanol technology is mature and can be used readily for vessels. However, green methanol can only reduce carbon dioxide emissions by 60-95%. Ammonia, on the other hand, doesn't emit any CO2 when combusted. However, it is less combustible than methanol and other traditional fuels and requires specialized engine adjustments for effective use. Therefore, investors are still undecided about which technology to support.

Another barrier is the lack of a unified international certification mechanism. For example, there is currently no single global definition and certification system for green methanol. And the ISCC certification, which is widely recognized, has withdrawn certificates and excluded system users several times. End buyers also have strict requirements for renewable carbon sources and technology paths. Fuel producers must not only meet the requirements of international certification standards, but also align with the needs of end buyers.

Additionally, the large scale investment required to upgrade fleets and strengthen infrastructure can also limit the commercial viability of green fuel projects.

Collaboration is needed across the value chain to unlock the future of sustainable marine fuels

Sustainable marine fuels play a vital role in the shipping industry's journey towards decarbonization. However, as an emerging technology, it still requires the whole-hearted support of shipping companies, fuel suppliers, cargo owners, port operators and other shipping stakeholders, not to mention the regulators and investors, for full scale commercialization and large-scale application to be possible. Here is what we recommend:

Regulators:

- Regulators could send powerful market signals by issuing mandatory directives and incentives for the production and purchase of sustainable fuels.

- Regulators should accelerate the establishment of fuel certification standards and create a proper trading system that allows shipping companies to buy fuel certificates without being tied to physical supply, and then to transfer the environmental credits to corporate customers.

Stakeholders in the industry ecosystem:

- Shipping companies, fuel suppliers, shipyards and other stakeholders need to improve economy, safety and cleanliness. Greater cooperation will promote technological innovation and help them achieve this. More pilot projects need to be carried out to provide suitable scenarios for technology verification and iteration.

- Stakeholders also need to expand sustainable fuel capacity as well as strengthen the infrastructure that will be required to cope with future demand.

- Stakeholders could jointly explore innovative business models for sustainable fuels and drive transparent cost sharing across the value chain for projects in fuel production.

Investors:

- Investors and financial institutions need to accelerate the speed and scale of investment in sustainable fuels, as well as explore purpose based financing instruments to mobilize capital.

G&PS

To boost the market or to control liquidity risk?

On May 17, China's central bank announced that it would establish a 300-billion-yuan (about USD42.25 billion) re-lending facility. The facility will support a buyout program through which local governments will be encouraged to leverage local State-owned enterprises to buy reasonably priced commercial housing that have completed construction. The idea is to turn these objects into government-subsidized housing, thereby reducing the number of commercial housing projects which are struggling with sales. The facility will be established by 21 national banks, including the China Development Bank, policy banks, State-owned commercial banks, Postal Savings Bank of China and joint-stock commercial banks, with one-year term at an interest rate of1.75%. The new mechanism is anticipated to generate banking loans by local commercial banks totalling RMB500 billion. The interest rate of the loans granted to the local State-owned enterprises by the commercial banks will be capped at 3%.

State-owned enterprises help with "destocking"

Currently, the national amount of unsold completed housing amounts to 22.5 months worth of transactions, exceeding the previous peak of a similar cycle (2015-2016). According to the Founder Securities Research Institute, as of April 24, national "completed but unsold" commercial housing for sale was measured at 390 million square meters, somewhat lower than the 460 million square meters of the 2015-2016 cycle. However, due to the slow pace of transactions, the destocking of these 390 million square meters will take 22.5 months, considering the average monthly sales of 16.7 million square meters during the last 12 months, which would be even longer than the peak of the previous 2015-2016 cycle (20.2 months).

Since the local State-owned enterprises will mainly conduct the acquisition of the unsold completed commercial housing but are not meant to hold hidden government debt or act as government financing platforms, they will be obliged to meet bank credit requirements and quickly sell or lease these houses after acquiring them. This means that the destocking is financially supported by the central government but implemented by local governments. The central government will require these local governments to resolutely ensure that all risks are under control. The re-lending facility may only be used for completed but unsold housing, not for housing currently under construction, nor existing housing held by residents. To sum up, the facility is designed to address risks rather than to boost the real estate market.

Figure: unsold completed housing stock-to-sales ratios exceed those of the last cycle peak (monthly)

Source: Wind, Founder Securities Research Institute

Source: Wind, Founder Securities Research Institute

"Destocking" requires more market-oriented measures

Anaemic real estate sales over the last two years are at the root of the heavy glut of unsold completed housing. Based on the nationwide cumulative average sales price of RMB 9,600 yuan per square meter of commercial housing in the first four months this year, even if the 300-billion-yuan re-lending facility is successfully launched and will generate banking loans worth RMB 500 billion, the funds are merely enough to absorb 50 million square meters of real estate, which represents only about 12.8 % of the total unsold and completed housing.

The remaining 87.2% will need to be sold to other market players -- residents or companies. So far, most cities have reduced their local interest rates for contracting new mortgages while still maintaining high interest rates for the existing ones. If interest rates for existing mortgages are not reduced in a timely manner, residents and/or companies will prefer to pay back early their current mortgages, in order to reduce their interest payments.

Aims to mitigate the liquidity risk of real estate enterprises

The new measure will help real estate companies with cash collection and allow them to reinvest into other projects under construction, therefore mitigating the risks to the real estate market. Another important measure to help relieve the pressure on corporate funds is the " Real Estate Financing Coordination Mechanism" set up by the Ministry of Housing and Urban-Rural Development and the National Administration of Financial Regulation. It requires local governments to establish a "White List", meaning solid real estate projects. Commercial banks will provide financing support for these projects and set up separate accounts to ensure that the funds are used to guarantee the construction and delivery of the housing. Currently, 297 cities have established such real estate financing coordination mechanisms. As of May 16, commercial banks have provided loans totalling RMB 935 billion for the White List projects.