Driving healthy employment growth: A look at occupations in health care has been saved

Driving healthy employment growth: A look at occupations in health care Behind the Numbers, March 2017

24 March 2017

Patricia Buckley

Patricia Buckley

Accounting for a large and growing share of employment and GDP, the occupational composition of health care industries seems to have changed relatively little since 2000.

Introduction

The health care services sector is a major driver of employment growth in the United States. Between 2000 and 2016, overall private sector employment grew by 9.8 percent, while health care employment grew by 42.0 percent. This caused health care services’ share of total private sector employment to rise from 9.8 percent in 2000 to 12.6 percent in 2016.1 Expenditures on health care likewise have risen faster than other type of spending, resulting in health care accounting for 17.8 percent of GDP in 2015 (latest data), up from 13.3 percent in 2000.2 The types of businesses making up the health care sector are fairly diverse, from enterprises, hospitals, home health care services, and medical and diagnostic laboratories to community care facilities for the elderly. Reflecting the breadth of purpose, the occupational makeup of each of these types of businesses are quite distinct. This report explores the occupational makeup of the five industries that account for three-quarters of health care employment and finds that even with the major changes in health care policy that have occurred since the start of the century, the occupational makeup of individual industries has remained fairly constant.

Of the 4.6 million health care jobs created between 2000 and 2016, 1.1 million were in hospitals, 728,800 in home health care services, 726,600 were in physicians’ offices, 431,100 were in outpatient care centers, and 130,500 were in nursing care facilities (figure 1). Together these five accounted for 74 percent of health care employment in 2016, a slight decrease from the 77 percent they accounted for in 2000. On a proportional basis, the fastest rates of increase were in the two smallest categories, home health care services (115.1 percent increase) and outpatient care centers (101.4 percent increase). Looking at the increases in employment pre- and post-Affordable Care Act (ACA), each of these health care services grew more slowly on an annual basis during the post-ACA period (2010–2016) than in the period prior to the ACA (2000–2009), except for outpatient care centers.3

As shown in figure 2, as of 2015, outpatient care centers and hospitals had the highest proportion of specialized, highly skilled workers such as registered nurses, physicians, therapists, and technicians (65 percent and 68 percent, respectively). Physicians’ offices also had a high proportion of highly specialized workers (50 percent), but they also had a large segment of office workers (32 percent). Home health care services and nursing care facilities had a much lower proportion of the highly specialized workers and a much higher proportion of the lower-skilled aide occupations.4 For detailed visualizations of the occupational distributions of these industry groups, see the appendix.

Changes over time

Office of physicians

Between 2000 and 2015, the ordering of the top five most prevalent occupations remained identical and there were only minor changes in the ordering of the second five. Medical doctors comprise only 17.8 percent of those working in a physician’s office, down from 19.9 percent in 2000 (table 1). There were also decreases in the proportion of secretaries and administrative assistants and office supervisors. Occupations experiencing proportional increases were medical assistants, billing and posting clerks, and medical and health services managers. In 2000, nurse practitioners and nurse midwives were included with registered nurses and when these two categories were combined with registered nurses in 2015, their combined proportion was 9.2 percent, slightly below the 2000 proportion.

Hospitals

Between 2000 and 2015, the occupational skill level at hospitals rose somewhat, with the proportion of the registered nurses group, physicians and surgeons, and two categories of technicians increasing. Among those occupations losing share in this industry were health aides and secretaries and administrative assistants.

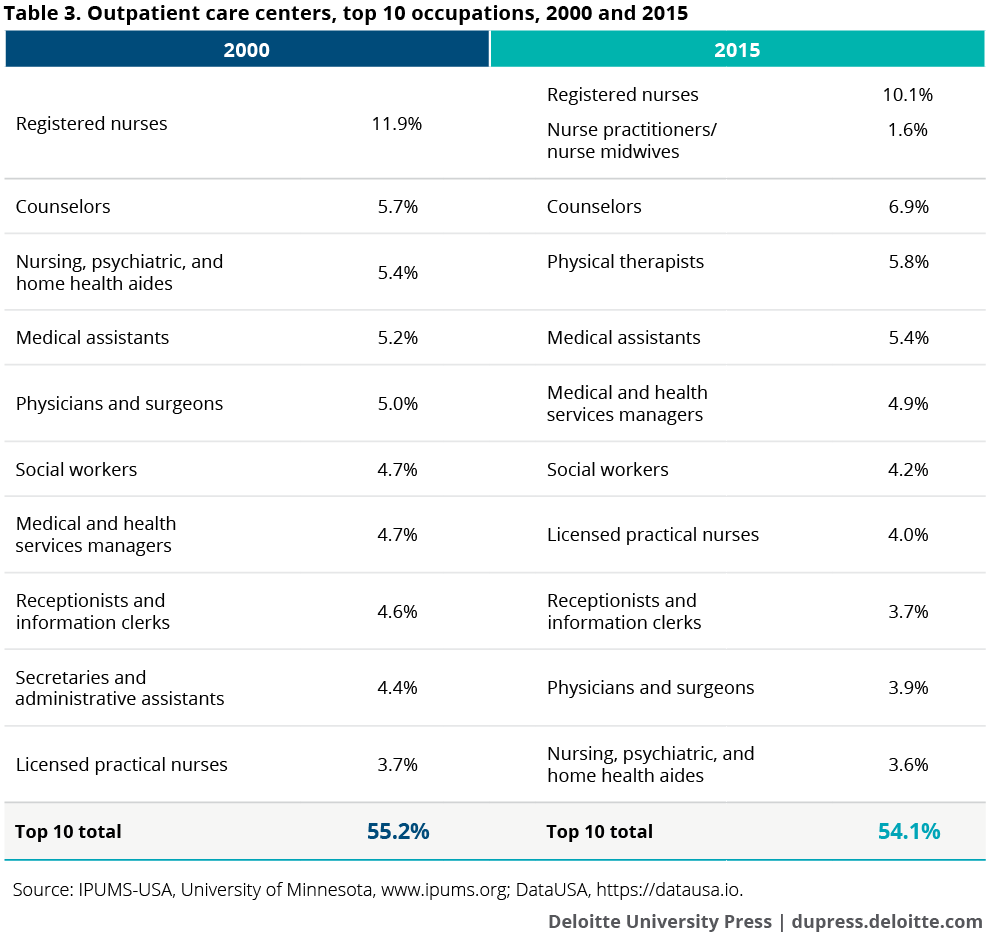

Outpatient care centers

Between 2000 and 2015, one of the larger changes was in the proportion of physical therapists in outpatient centers—in 2000 this occupation ranked eleventh at 3.3 percent (not shown) and by 2015, this group was the third most prevalent, comprising 5.8 percent of jobs. This perhaps reflects the aging Baby Boomer generation requiring more repair procedures such as knee and hip replacements. Other changes between the two periods include an increase in the proportion of counselors and a decrease in the combined registered nurse/nurse practitioner/nurse midwife group, health aides, physicians and surgeons, social workers, and receptionists. Secretaries and administrative assistants dropped off of the top 10 list in 2015, falling to eleventh place.

Home health care services

This industry has experienced the most change between 2000 and 2015 as it doubled in overall employment size. The proportion of personal care aides more than doubled (10.4 percent to 25.4 percent), while the proportion of health care aides, registered nurses, and maids and housekeepers fell. Licensed practical nurses are the only highly skilled category to increase in relative size in this industry.

Skilled nursing facilities

The slow-growing skilled nursing facilities industry is the only one examined here with employment growth below the national average. Although the occupations in this industry are concentrated in lower-skilled jobs, the biggest change between 2000 and 2015 was an increase in the proportion of both categories of nurses. The proportion of health aides and medical aides declined.

Given the aging of the population, employment in the health care sector should continue to experience a healthy rate of growth. Indeed the Bureau of Labor Statistics projects that health care occupations is expected to add more jobs over the next 10 years than any other group of occupations.5 As we think through the “workforce of the future,” it’s possible that health services employment could lead the way. However, given the lack of change in the occupational structures of the largest health care industries over the last 15 years, most of the changes to the overall occupational structure of the health care sector in the future will likely come from the differential growth rates of the individual industries rather than changes inside those industries.

Appendix

The visualizations below are based on data extracted from DataUSA (https://datausa.io). For additional information on these and other occupations, industries, or locations, please visit DataUSA.

To view the details for each group, place the pointer over individual blocks.

© 2021. See Terms of Use for more information.