Creating a viable hydrogen economy

A future of energy point of view

To stay in line with the 2015 Paris Agreement, the global energy system must shift from fossil fuels to renewables. This is already happening thanks to the plummeting cost worldwide of solar and wind energy. The energy system requires high levels of electrification to reap maximum benefits from renewable electricity’s low CO2 emissions and cost. However, not all end-uses can be electrified. This is where hydrogen comes in as a solution for decarbonization, provided that it stems from a zero or at least low-carbon source. There are, in fact, several hard-to-abate sectors that cannot be electrified: overall 50% will likely be electrified, and another 30% potentially electrified with great effort. Nevertheless, at least the remaining 20% (possibly as much as 50%) of current final energy consumption cannot be electrified, especially in industry and transport sectors (Figure 1). There is a lot of hype around hydrogen, and it will introduce new elements into the energy value chain that require further analysis to track the key trends and developments in its own value chain.

Hydrogen demand

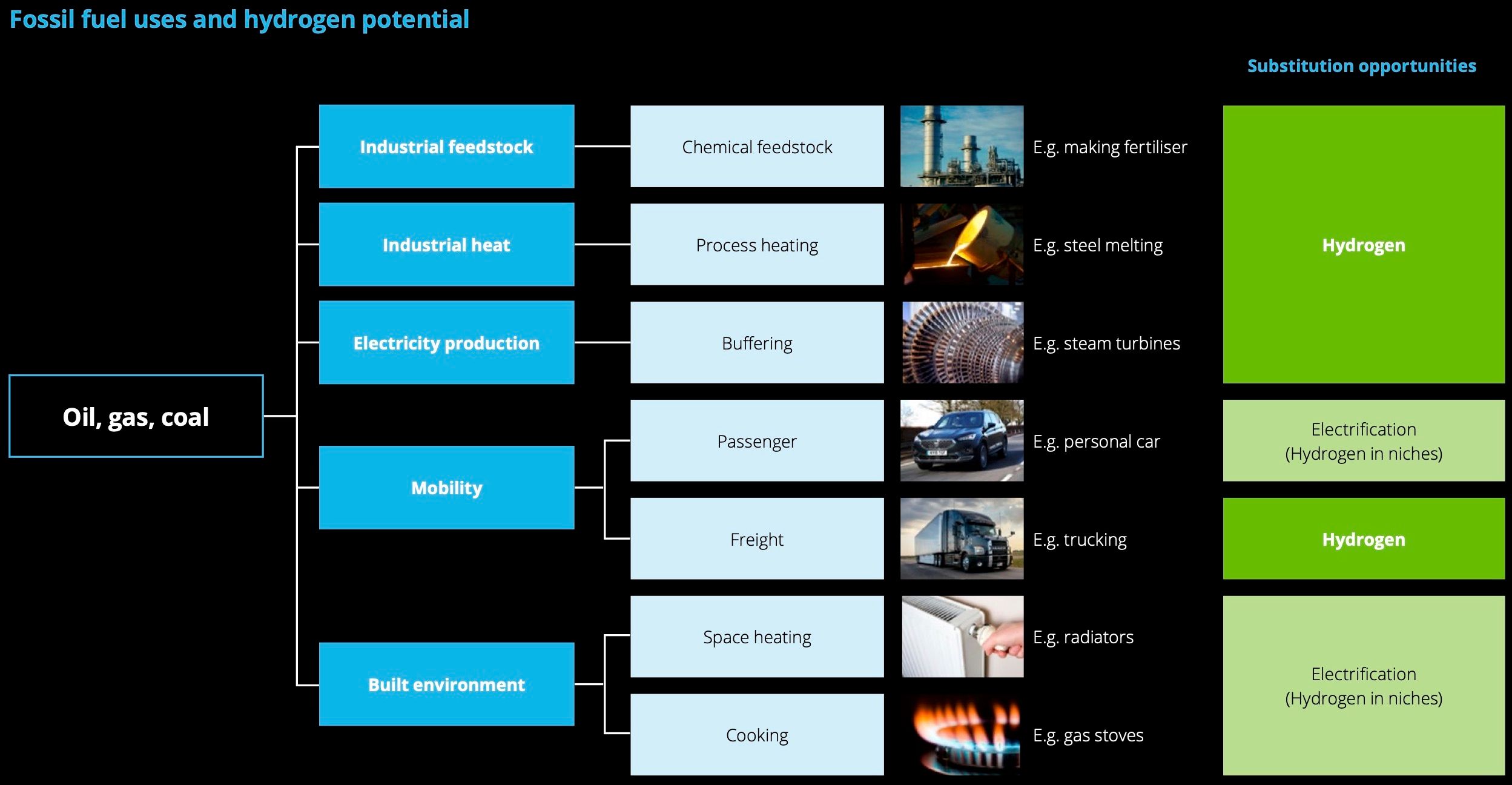

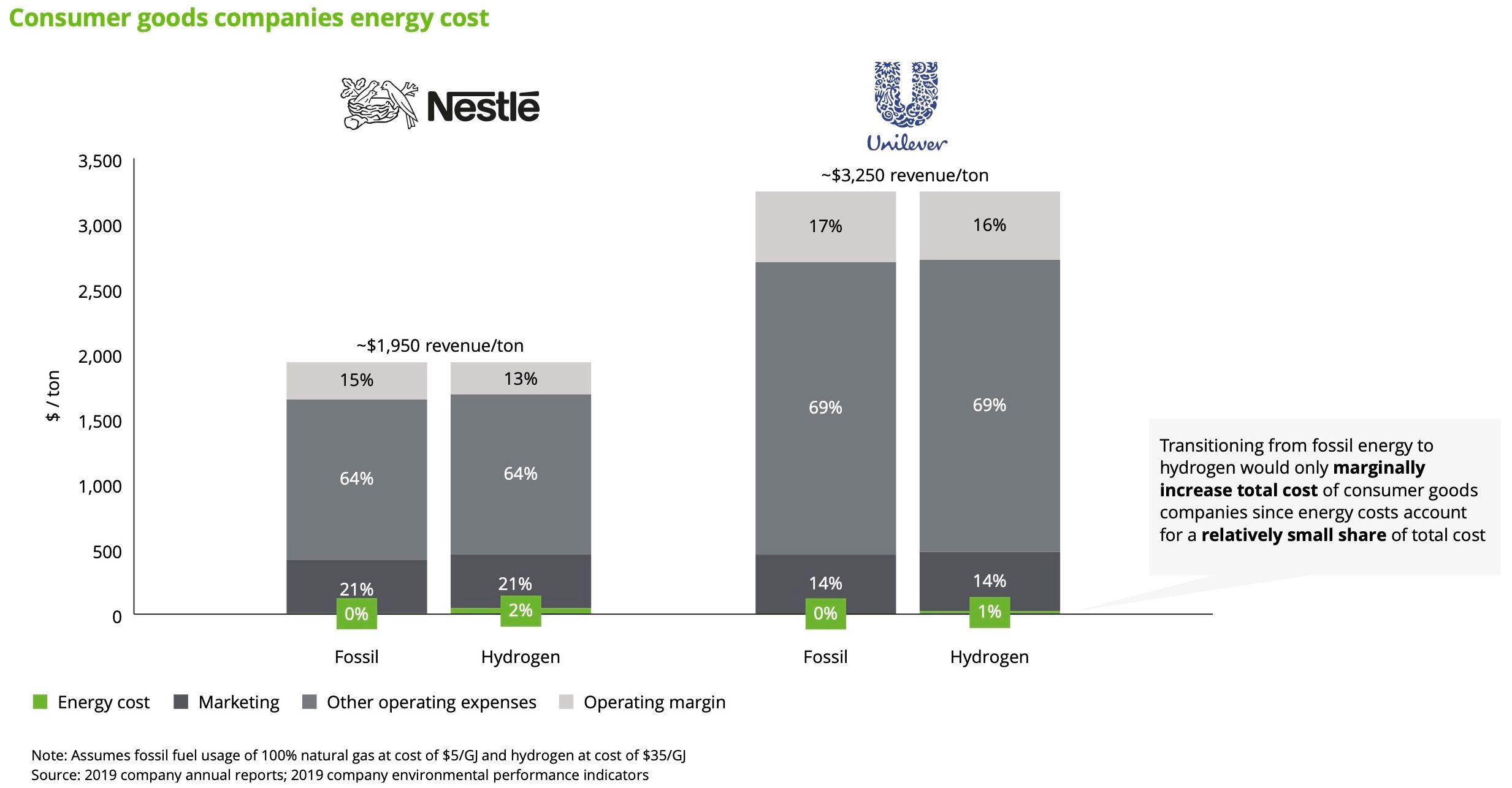

Hydrogen is well positioned to replace fossil fuels in industry, both as an energy source and feedstock. For feedstock appliances, it is even more competitive since it replaces converted hydrocarbons. But this replacement is slow because fossil-based hydrogen production assets (gray hydrogen) are already in place, while green hydrogen is not readily available yet and has higher marginal cost. Hydrogen is an energy source with the potential to replace fossil fuels in providing industrial heat. This is primarily due to the often relatively easy adaptation of burners and boilers to hydrogen combustion. Furthermore, from an economic point of view, energy cost often accounts for a very small part of total operating costs, thereby entailing very little extra cost for this end-use (Figure 2).

In the transport sector, hydrogen provides the opportunity to decarbonize high energy-density end-uses, such as buses, trucks, and specialized equipment. What’s more, hydrogen derivatives such as synthetic fuels like methanol and ammonia can decarbonize shipping and aviation while replacing the gray equivalents now in use. Although hydrogen use in the transport/mobility sector is a niche, in the long-term it and its derivatives have the potential to become the main fuel for hard-to-electrify transport segments.

Hydrogen can also help store renewable electricity. Once stored geologically (underground storage mainly in salt caverns similar to natural gas), hydrogen can provide long-term storage for variable renewables (mainly wind and solar) to deal with their inter-seasonal variability. In the built environment, moreover, hydrogen can be blended into the gas network for use in final consumption points, specifically homes. But overall, end-use electrification through heat pumps overall seems more commercially viable for homes.

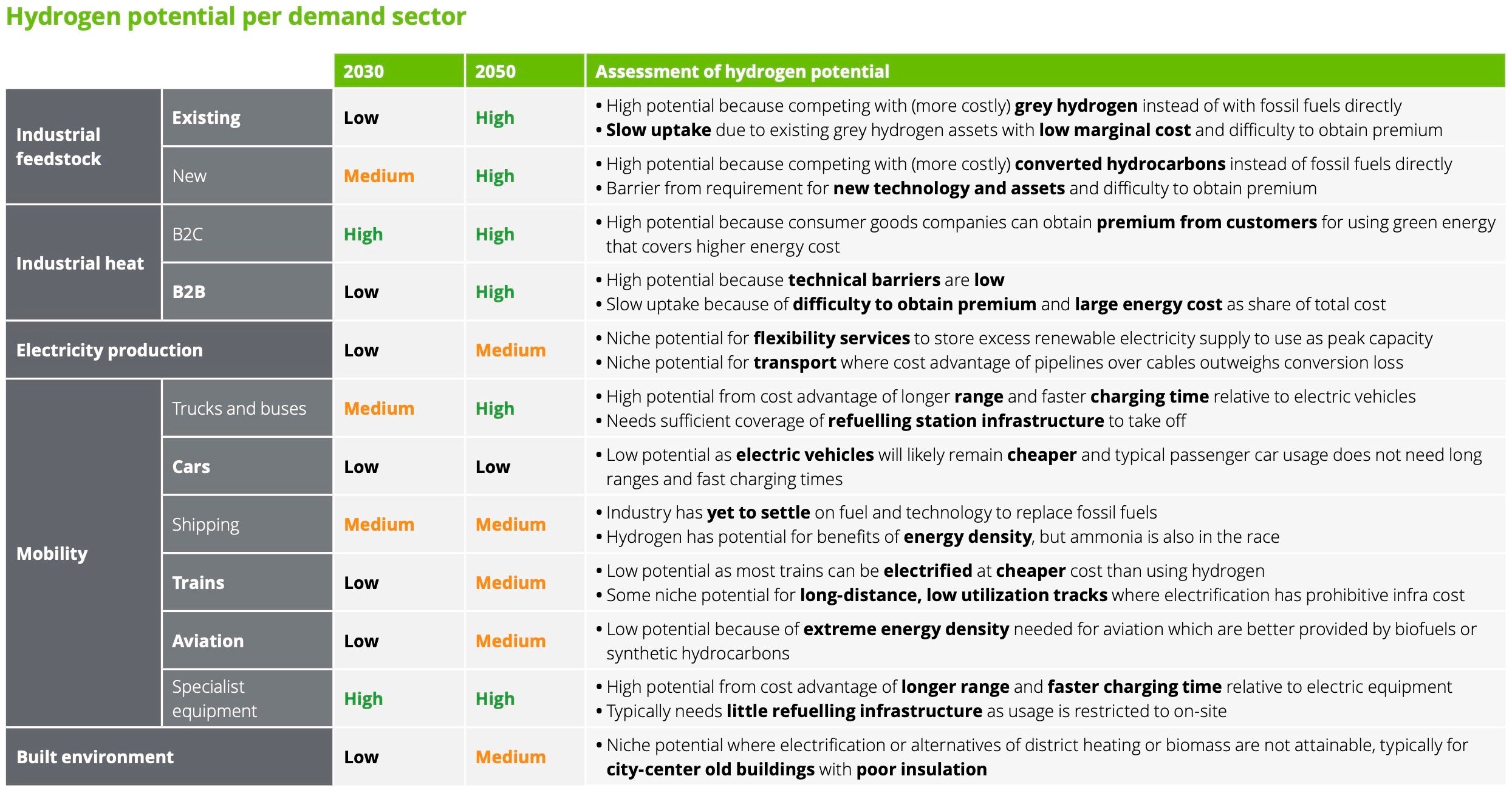

To conclude, the uptake of hydrogen will be driven by industrial heat and transport sectors in the short term, and will most likely extend to other hard-to-abate segments in these sectors (Figure 3). The direct replacement of gray hydrogen with green hydrogen in the production of ammonia and other industrial feedstocks also represents a medium-term opportunity for increasing the use and production of green hydrogen.

Hydrogen supply

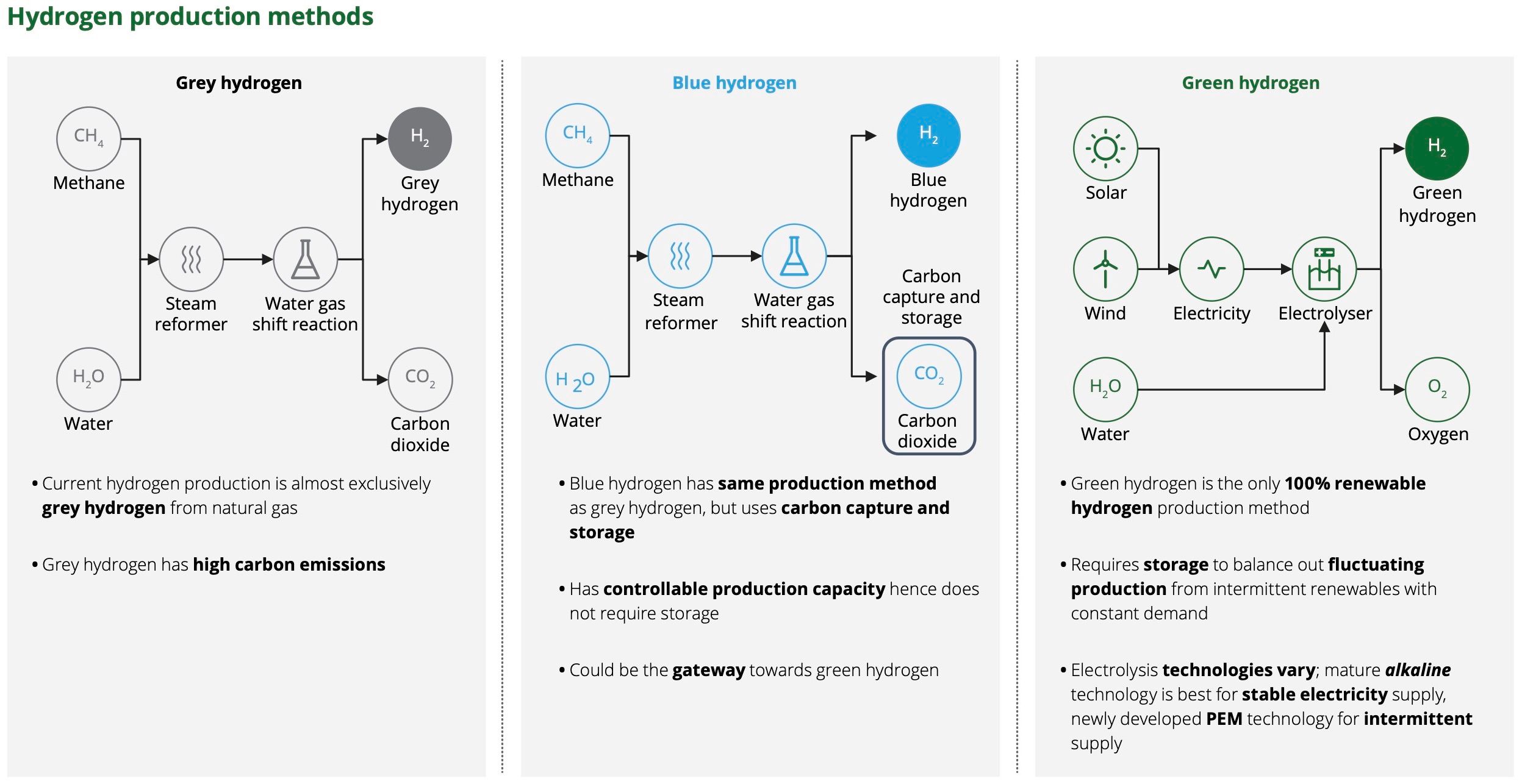

Gray hydrogen is produced from steam reforming of natural gas, and leaves a substantial carbon footprint. If the resulting carbon dioxide is captured and stored all along the supply chain, this hydrogen becomes low carbon (with residual CO2 emissions), and is commonly referred to as blue hydrogen. Hydrogen can also be produced via water electrolysis using electricity; if this electricity is renewable, the resulting hydrogen is called green hydrogen (Figure 4).

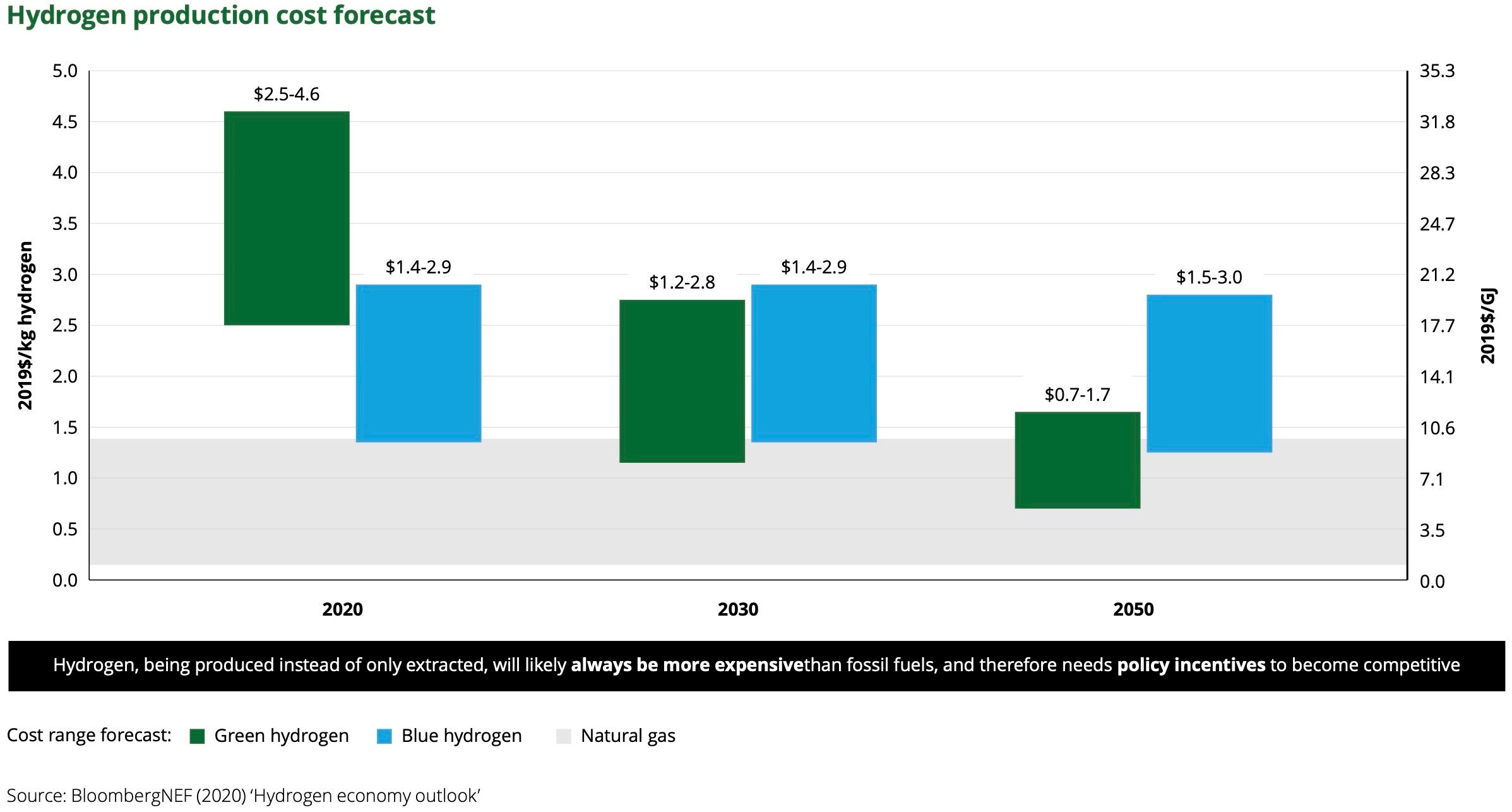

Both blue and green hydrogen are more expensive than the gray hydrogen that dominates hydrogen production. But in the long term, green hydrogen can become cost-competitive thanks to falling renewable electricity prices and electrolyzer cost. Moreover, additional carbon taxes or increased cost of carbon emissions through certificates would raise the cost of gray hydrogen. Blue hydrogen is a relatively mature technology that, in the short-term, is cheaper than green hydrogen and can kickstart clean hydrogen supply. In the long term, however, green hydrogen is set to be the cheapest (Figure 5), especially from locations with exceptionally renewable resources.

While hydrogen converted from electricity has very low efficiency (between 25% and 50% for electricity via fuel cells and between 60% and 80% via combustion for heating), it has advantages over electrification in terms of total cost and full decarbonization for some applications. First, it allows for decarbonization of end-uses where electrification has physical limits. Second, hydrogen pipeline transport is from eight to 15 times cheaper than electricity transport via cables. Finally, hydrogen allows for energy storage, and thereby full variable renewable electricity integration.

Hydrogen distribution

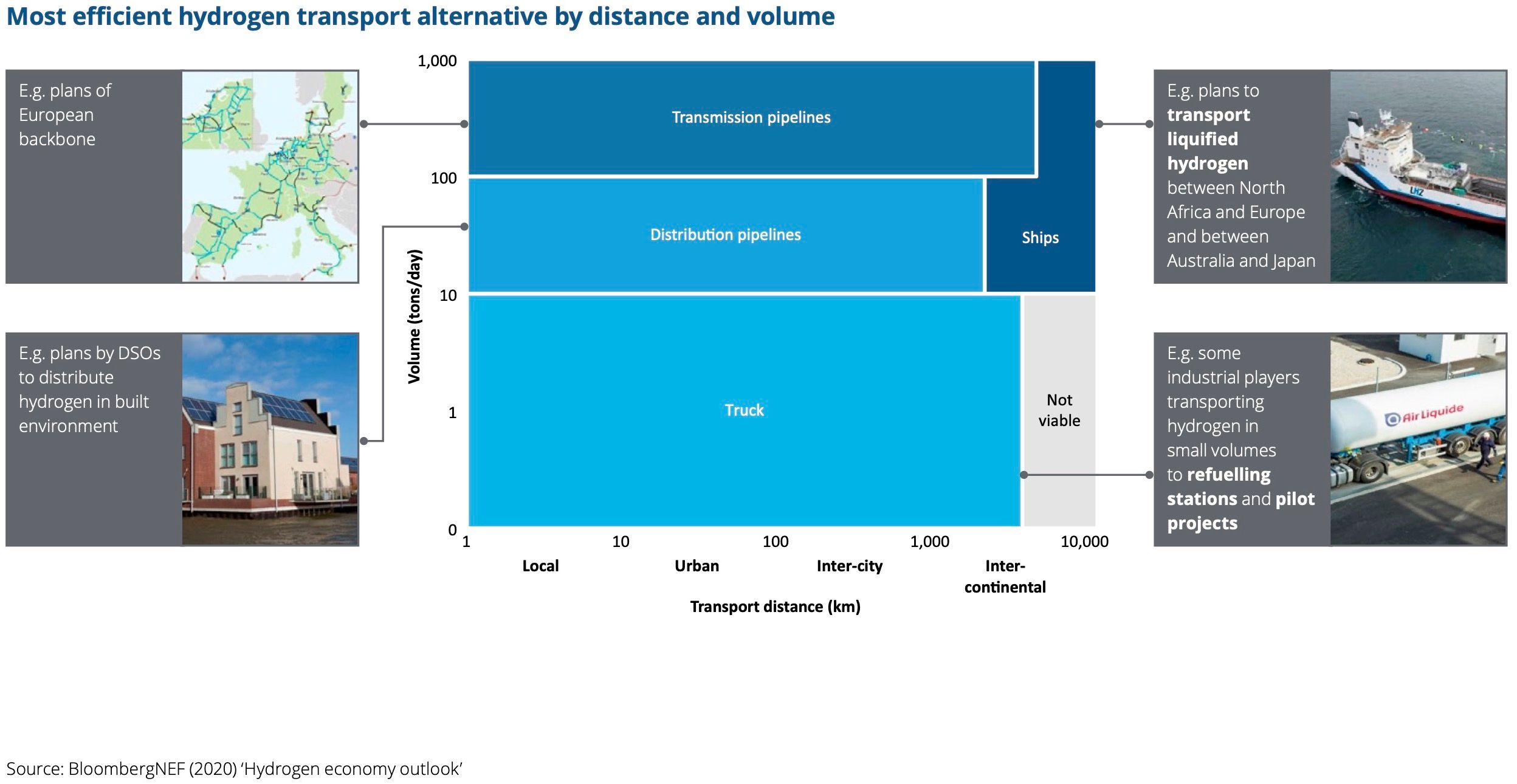

Like fossil fuel, hydrogen can be transported via pipelines, trucks and ships (Figure 6). Hydrogen transport is costlier than fossil fuel transport due to its physical properties. Hydrogen has lower energy density per volume (m3) than fossil fuel, and lower density means less energy transported in the same truck, ship, or pipeline. But hydrogen has higher energy density per mass (kg), which means the transported weight will be less. What is more, the higher flow velocity of hydrogen (3x faster than natural gas) partially offsets its lower energy density when evaluating pipeline transport, which boasts an even greater cost advantage over transport via truck.

A pipeline infrastructure is feasible for connecting large-scale hydrogen storage at close-to-sea locations, whereas it connects supply and demand at onshore locations. Hydrogen distribution via trucks will initially remain relevant because a dedicated hydrogen network will not be as widespread as the current natural gas network. Import (especially via pipelines and in the future via ships) will be essential as hydrogen demand likely exceeds European domestic hydrogen production and the cost advantage of some locations in the southern hemisphere.

Policy perspective

The uptake of a hydrogen economy and its value chain largely depends on the active involvement of policymakers in ramping up production, distribution, import, and demand-side support.

To begin with, decreasing the cost of clean hydrogen production depends largely on the development of hydrogen ecosystems. National and continent-wide hydrogen policy goals are taking shape and preparing the ground. These mechanisms vary across countries; for instance, Japan uses a demand-pull method, while China is more active on the technology-push side. There are wider policy goals in the European Union, where scale-up, investment, demand creation, and infrastructure development are all targeted policies (cf. EU hydrogen strategy).

Aligned with investment policies, governments should stimulate the hydrogen market via different instruments such as blending obligation, innovation budgets, market instruments, etc., although blending has become less of a priority now that the demand for hydrogen has become more certain.

Company perspective

Hydrogen as a feedstock has gained significant attention from industry, notably via pilot projects for steel manufacturing and chemicals production. Decarbonized hydrogen production is also taking off via industrial partnerships and public-private cooperation (e.g., NortH2 and Zero Carbon Humber projects). In such a dynamic environment, companies can look to the following best practices.

On the supply side there is collaboration through consortia, specifically the world's largest energy companies driving the development of the hydrogen market. They will ramp up pressure on government to enable a hydrogen market that scales and matures like other global commodity markets for fossil fuels.

Uncertainties with regard to the first steps are driving the hydrogen economy towards a vicious cycle, very similar to the technology and infrastructure developments that required breakthroughs to piggyback off other technologies or systematic R&D investments (such as internet, renewable development, etc.). The key challenges in summary: policy and technology uncertainty, regulations and standards, cost effectiveness, and complexity of the ecosystem. To overcome these challenges, industry needs to (1) make strategic bets, (2) build an ecosystem, (3) keep learning and (4) proactively engage with policymakers.

On the demand side, the world's big brands can become game changers as they look for renewable alternatives to non-electrifiable energy use, driven by their green ambitions. This is likely to trigger the hydrogen equivalent of a PPA market, such as it emerged in the electricity market.

The development of a hydrogen market is associated with many opportunities in different sectors. The handling of hydrogen molecules fits right in with the core capabilities of the oil, gas and chemicals sector. This sector has experience with large-scale asset development projects, can use hydrogen to decarbonize refining operations by replacing gray hydrogen with green, and can decarbonize chemical production by using clean hydrogen as feedstock and energy source for heating. For the power & utilities sector, clean hydrogen provides arbitrage opportunities in electricity generation, increased flexibility in electricity systems, and new business opportunities. In other industrial sectors such as mining and metals and industrial products and construction, it can provide the opportunity to decarbonize operations and develop new business opportunities.

Contact

Bernhard Lorentz

Managing Partner Deloitte Sustainability & Climate GmbH

Global Consulting Sustainability & Climate Strategy Leader