Japan economic outlook, October 2024

Wage gains and a growing yen are driving households’ spending power and domestic demand, but persistent inflation is still a major challenge to Japan’s growth

Evidence of improvement is emerging in the Japanese economy: After a contraction in the first quarter, real gross domestic product rebounded by 0.7% in the second quarter of 2024, thanks to strong domestic demand.1 Consumer spending grew 0.9% from the previous quarter, while both residential and nonresidential private investments picked up. Year over year, consumer spending returned to growing ways, while exports contracted for the first time since 2020.2 Clearly, the driver of Japan’s economic growth is shifting from external to domestic demand. Although we expect domestic demand growth to continue, gains will likely be modest as elevated inflation limits the benefits of stronger wage growth.

Real GDP growth was a welcome development, but some of the gains in the second quarter went toward merely overcoming losses seen in the first quarter. The pent-up demand in the second quarter was warranted after automotive plants shut down unexpectedly in December, thus affecting the country’s economy in the first quarter 2024.3 Even with the gain in the second quarter, real GDP was still 0.9% lower than a year earlier. Consumer data released thus far for the third quarter have pointed toward modest growth. Real household spending was up just 0.1% from a year ago in July, which was the first positive reading since February 2023.4 Similarly, the real consumption activity index reached its highest level since February 2020, but was up just 0.2% from a year earlier.5

The improvement in the consumer outlook is mostly due to stronger wage growth. June 2024 marked the first time when nominal wages outpaced inflation since 2022. However, by August, real wages were flat compared with a year earlier.6 Part of the problem for workers is that much of their wage growth was driven by bonus pay, which typically falls off after the summer. Contractual wages, which exclude bonus payments, accelerated to 3% from a year earlier in August in nominal terms, which was the same as headline inflation.7 Nominal wage growth has accelerated, but the unemployment rate has trended higher this year.8 A tighter labor market is likely needed to sustain stronger wage growth.

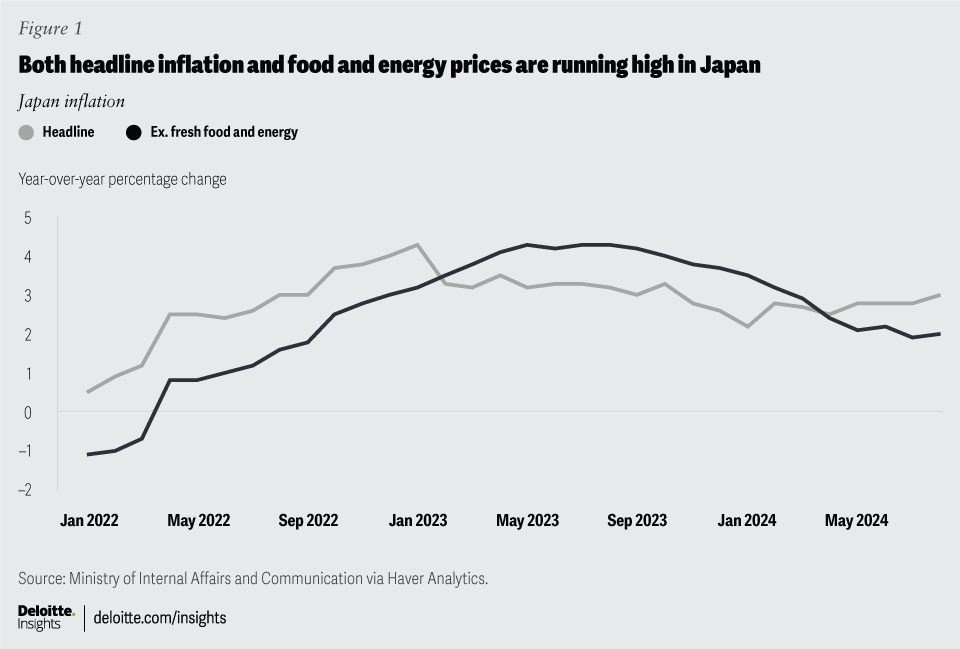

The other major challenge to stronger consumer spending is that inflation continues to run hot. Headline inflation was up 3% from a year earlier in August, an acceleration from 2.7% in July (figure 1).9 Costs of fresh food and energy have been particularly high, rising to 7.8% and 12%, respectively.10 After excluding these items, inflation was just 2% in August.11 Fortunately, some of the inflationary pressure on fresh food and energy is already subsiding, thanks to the appreciation of the yen.

{kind=link}

Expectations of stronger rate cuts in the United States and more rate hikes in Japan caused the yen to appreciate in August 2024. By the end of August, the yen had appreciated to 144.6 against the US dollar—the strongest it had been since the first week of the year.12 The yen continued to appreciate slightly in September: A stronger currency will lower the cost of imports, notably for food and energy. The import price index in August was up just 2.6% from a year ago, after rising by 10.8% in the previous month,13 signaling that imported inflation has responded quickly to the stronger yen.

Further appreciation of Japan’s currency will largely depend on policymaker decisions in both Japan and the United States. The Bank of Japan kept rates steady at its September meeting but has signaled a willingness to eventually raise rates to 1%, up from “around 0.25%.”14 The new leader of Japan’s ruling party, Shigeru Ishiba, is seen as an inflation hawk and supportive of additional interest rate increases. As a result, Japanese equity markets fell when trading resumed following his win.15 However, he is expected to maintain the Bank of Japan’s independence, which would prevent him from intervening in monetary policy. Plus, he has since stated that interest rates are not yet ready to rise further.16

At the same time, the US Federal Reserve cut rates by 50 basis points in September and signaled another 150 basis points of cuts by the end of 2025.17 A more dovish stance from the Bank of Japan or a more hawkish one from the Fed could cause the yen to depreciate again. A significant expansion of the US fiscal deficit following the election could cause the Fed to take a more hawkish stance than currently expected. Despite such risks, we expect the yen to gradually appreciate against the US dollar, which will support our view of a modest acceleration in consumer spending.

A stronger yen is also expected to help the government achieve its spending goals, especially for defense. The country’s defense ministry requested 8.54 trillion yen (or US$57 billion) for fiscal year 2025, which is up 10.6% from the budget submitted for the previous fiscal year.18 Japan is aiming to increase defense spending to 2% of GDP, now that it has adopted a new national security strategy that is no longer exclusively focused on self-defense.19 Because Japan will need to import defense-related goods from other countries, such as the United States, a stronger yen should make such expenditures more affordable. Japan’s defense spending will also need to be increasingly geared toward such equipment as an aging population limits growth of military personnel.

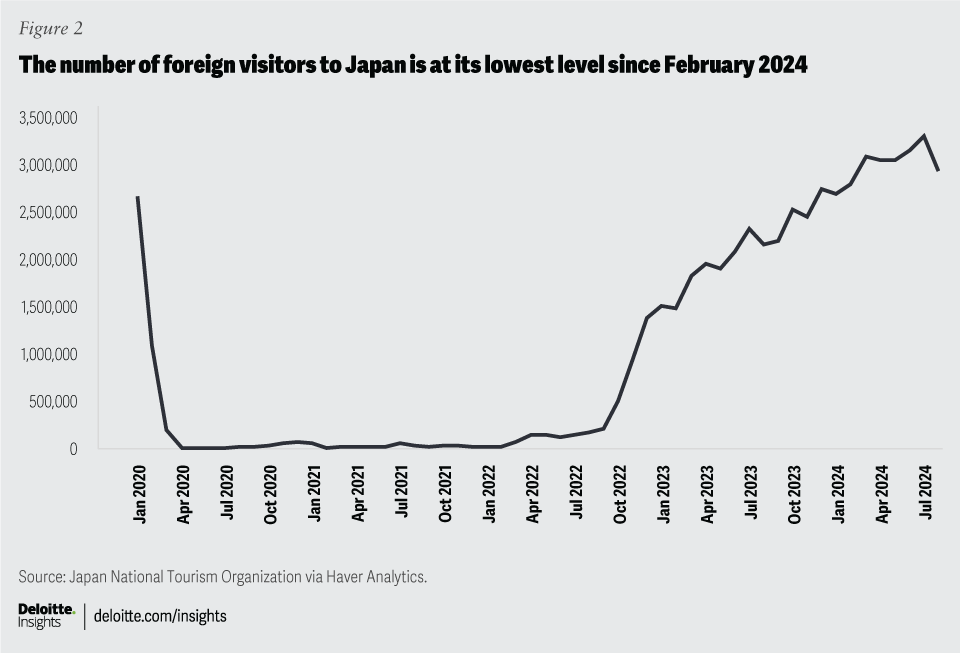

While a stronger yen is supporting consumer spending and domestic demand more generally, it is weighing on external demand. In August, the number of foreign visitors to Japan fell to its lowest level since February 2024 (figure 2).20 Foreign visitors are a large source of services exports for Japan. Similarly, goods exports fell to their lowest level since March.21 Some of the weakness was due to ongoing challenges in the auto sector. After auto production mostly recovered from shutdowns during the spring, a larger swathe of automakers and vehicles were revealed to have had testing irregularities.22 Auto production slumped again in June and July and has yet to return to the level of output seen in December 2023. As a result, motor vehicle exports declined by double-digit rates to China, the European Union, and the United States.23

{kind=link}

Motor-vehicle exports will likely recover some once production can resume. Other exports, such as semiconductor machinery, are likely to remain relatively strong as well. Japan produces goods that are critical to the semiconductor supply chain. With countries trying to expand their own semiconductor manufacturing operations, equipment from Japan has been in high demand. Notably, semiconductor machinery exports were up 55.2% from a year earlier in August. Still, a stronger yen will make most goods less competitive internationally, which will restrain export growth going forward.

Japan’s engine of economic growth is already switching from exports to consumer spending. A rapid rise in wages has finally given households the purchasing power they need to spend more. A stronger yen should also help alleviate some inflationary pressures, which will further bolster consumer spending. However, inflation is likely to remain elevated in the near term, which will keep the pace of spending relatively modest. A more hawkish monetary policy stance in the United States as well as a reversal of wage gains are risks that could further hinder Japan’s nascent recovery.