Balancing payments: Why it’s harder than you might think to cut the trade deficit has been saved

Balancing payments: Why it’s harder than you might think to cut the trade deficit Behind the Numbers, February 2017

28 February 2017

Can you cut the trade deficit with taxes on foreign goods? A little accounting helps explain why economists think it’s not so easy.

Introduction

The United States buys more goods and services from foreign countries than it sells to other countries. That’s been true for many years—the last time the United States sold more goods and services abroad than it purchased was in the first quarter of 1976.1 In 2015 alone, the US trade deficit for goods and services—the difference between the value of imports and the value of exports—amounted to $500 billion. That may seem like a lot of money, but what does it really mean? And how does the United States manage to buy more than it sells year after year?

The optics of trade deficits may seem pretty clear. One country (for instance, the United States) buys more goods and services abroad than it sells to foreign countries. Some commentators claim that if buyers in the United States only turned to domestic suppliers, more people would be put to work in the country and everybody would be better off. So the trade deficit may look like a problem, but a problem with an easy solution.

But this is economics, so of course it is more complicated than that. To better understand the problem, however, we turn to accounting, rather than economics—not company cost accounting, but balance of payments (BOP) accounting. This is the system that government statisticians use to classify all international transactions. It’s a double-entry system, and that means that the balance of payments … well, balances. Which can make cutting the deficit on the trade account—a sub-account of the total balance of payments—challenging.

Recording international transactions

The BOP accounting system, like other systems, starts with two columns. A country records credits when it sells something and debits when it buys something. As mentioned earlier, it’s a double-entry system. Every entry in the debit column has a countervailing entry in the credit column.

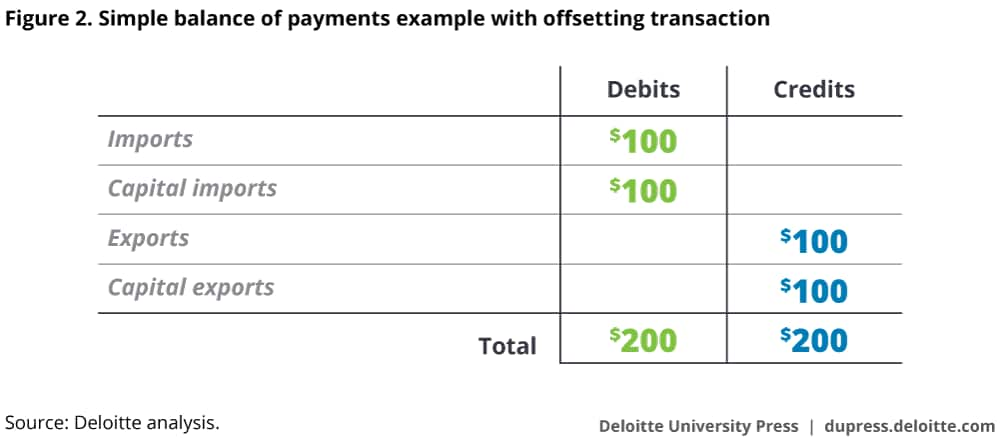

For example: A US retailer orders shirts worth $100 from a Chinese supplier. This is a US import, which is recorded as a debit on the BOP (figure 1). (And this is the BOP for the United States; there is a separate BOP for China, which shows a $100 credit from this transaction.)

Since it’s a double-entry system, there will be a corresponding credit entry recording the fact that the Chinese supplier now has an additional $100 in the bank. The US purchaser “sold” that cash to obtain the shirts, so it shows up as a credit for the United States. Because the United States “sold” an asset (money is an asset, just like bonds or stocks), it is considered an “export” of capital.

Of course, the Chinese supplier can’t pay its workers with dollars—it needs Chinese currency (renminbi). To exchange dollars for renminbi, it has to find somebody that wants the dollars to purchase something from the United States. Perhaps a Chinese airline needs dollars to buy parts from a US company to fix an airplane. The two transactions together look like this:

Now we have balanced trade, and nobody has “foreign” assets. And credits still equal debits—the balance of payments balances.

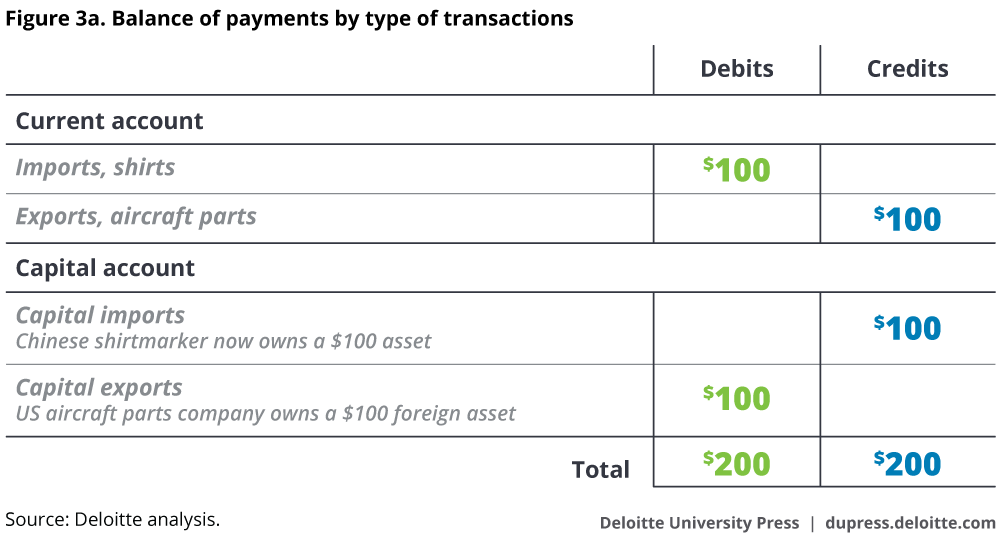

The current and capital accounts

Let’s now try classifying the transactions. Specifically, let’s classify transactions that involve financial balances from those that do not. Why? Transactions that do not involve financial balances are one-time actions. The shirts (or aircraft parts) ship and that’s the end of it. Financial balances, on the other hand, are “promises to pay.” A dollar represents the ability to buy, at some future time, a dollar’s worth of goods and services. This is an increase in the wealth—the capital—of the residents of the country that obtained the asset.

If a transaction results in no change in capital wealth in the country, the transaction is called “current.”2 And if the transaction does result in a change in wealth, it is a “capital” transaction. Below, the Chinese sale of shirts and the US sale of aircraft parts are each recorded twice, as the double-entry system requires. On the current account, the value of goods shipped is recorded, and on the capital account, the value of the payments received is recorded.

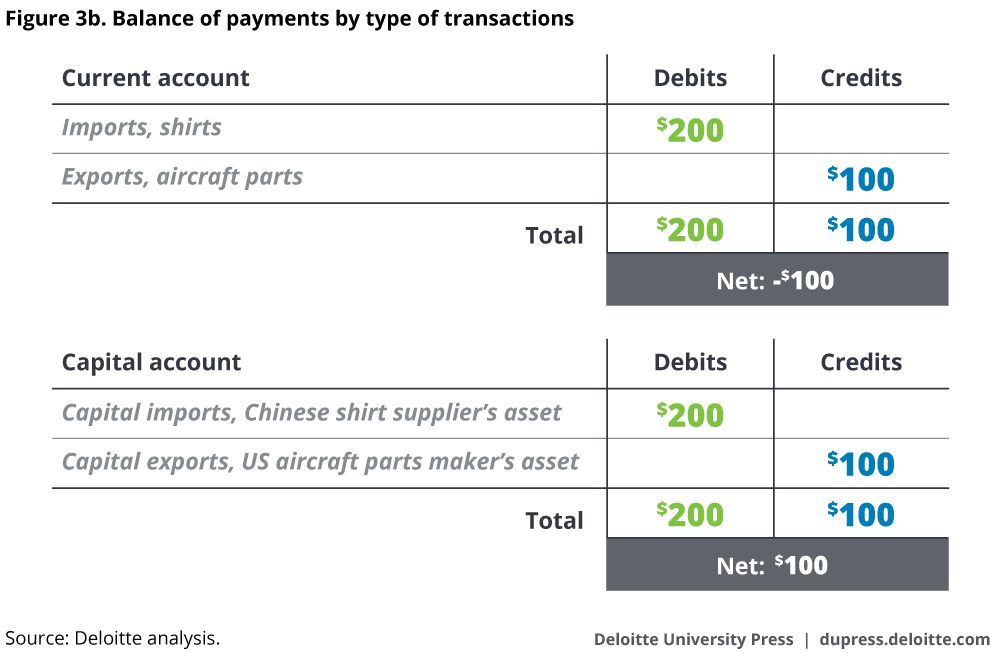

Now, suppose that US purchases of shirts are twice the value of Chinese purchases of aircraft parts. The different classifications, or accounts, are no longer balanced. There is a net negative on the current account, and a net positive on the capital account.

The balance of payments still balances—net debits plus net credits equals zero. But the Chinese supplier winds up with an extra $100 in assets, money that can be invested in other dollar assets or used in the future to buy US dollar goods and services.

Sidebar: The balance of payments deficit

Some readers may recall hearing the phrase “balance of payments deficit” (or “surplus”). But if the payments accounts must balance—as is the case, since it is a double-entry system—how could there possibly be a deficit or surplus? The answer lies in some history and a bit more detail about the BOP.

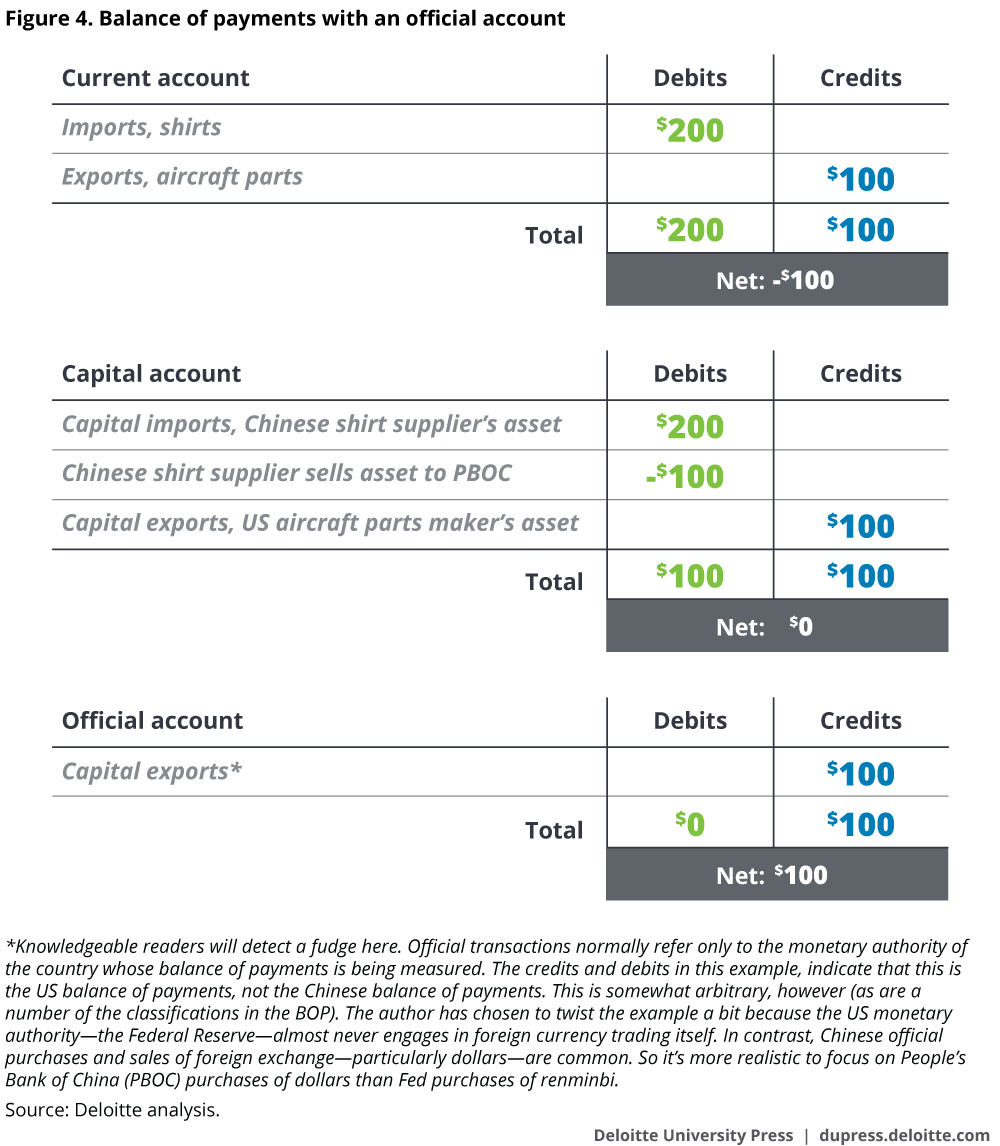

There is in fact a third account in the balance of payments—the “official” account. The official account records international transactions of the central bank. Suppose, in our example, the Chinese shirt supplier didn’t want the extra $100 in the final example. The supplier might sell the dollars to the People’s Bank of China (PBOC) for the renminbi necessary to pay employees. Figure 4 shows the full balance of payments with this transaction.

The net is still zero. But now the People’s Bank of China owns the dollars, and these are now called “foreign exchange reserves.”

Now for a little history. After World War II, there was almost no market for global financial assets. So there were effectively no capital account transactions in the sense of purchase and sale of assets in different currencies by the private sector. Almost all international transactions were paid for in dollars, and economic actors outside the United States could only get those dollars from selling goods and services to the United States or by purchasing the dollars from their local central bank’s foreign exchange reserves. And exchange rates were fixed, meaning that the central banks were committed to buying and selling dollars at a fixed price.

A country with an import surplus therefore needed to find dollars to pay for the surplus. That need was often called a “balance of payment deficit,” which on reflection is a self-contradictory term. What it meant was that the central bank was paying out the dollars necessary for transactions from its reserves. If the central bank ran short of dollars, there was a “balance of payments crisis” (often solved by devaluing the country’s currency).

The dollar is still the most accepted global medium of exchange. But now dollars are not hard to obtain if necessary—particularly since many global investors hold a stock of dollar assets for investment purposes. And few central banks are committed to buying and selling dollars at fixed exchange rates. Thus, the rather odd term “balance of payments deficit” may no longer be meaningful.

How investors drive international competitiveness

Up to this point, our actors have mainly been interested in their business producing things such as shirts and aircraft parts. But suppose we start with a Chinese investor who wants to invest in dollar assets. Where can the Chinese investor get dollars? Only by selling something (such as shirts) to the United States. So global demand for a country’s assets—for investment in a country—can only be supplied if the country buys more from foreigners than it sells to them.

There are a variety of reasons why people around the world might want to hold US dollars. Some of these include:

- Dollars are the global currency, so an Indian company purchasing a German machine tool is likely to pay the German company in dollars. And just as US residents hold dollars in their wallet or checking accounts, foreign companies that engage in international trade need to keep dollar balances to make payments when necessary.

- Short-term investors may see advantages in holding assets such as Treasury bills, bonds, or even stocks because of higher returns in the United States or because they expect the US dollar to appreciate.

- Longer-term investors such as corporations may wish to locate operations in the United States to take advantage of US talent, or of the large, unified US market, or natural resources in the country.

So there a variety of people involved in the decisions that end up being recorded in the balance of payments. And there is a key mechanism behind the balance of payments that ensures that the aggregate behavior of all these actors results in balance.

The exchange rate and the capital account

Modern international economic analysis of the balance of payments sees the capital account—not the current account—as the key to understanding international transactions. Global investors usually want to hold a variety of assets from around the world. On a given day, the supply of those assets is effectively fixed—the number of dollar bonds, stocks, and so on is set. Demand, then, determines the international price of dollar assets—the dollar exchange rate.

And what happens if demand is strong? The dollar exchange rate is bid up, and US exporters of goods become uncompetitive. The US current account deficit increases—which means that the capital account surplus (the supply of dollar assets to the rest of the world) grows. And the global demand for more dollars is satisfied.

And if demand is weak? The dollar exchange rate falls, US exporters become more competitive, and the supply of dollar assets shrinks.

That leaves those who wish to reduce the US current account deficit in a bit of a pickle, because taxing imports of goods and services to make them less competitive than US products is unlikely to actually reduce the deficit. Why? As long as dollar assets remain popular globally, the dollar exchange rate will likely simply rise to compensate for the higher price of foreign goods and the supply of dollar assets to foreigners will likely remain at the previous level—as will the offsetting current account deficit.

So how to reduce the attractiveness of a country’s assets? A simple way to do it could be to cut interest rates. Assets that pay less are less attractive. Foreign investors will probably want to buy fewer dollar assets, the dollar will fall, and US goods and services will become more competitive. But it doesn’t have to be just lower interest rates. Anything that makes global investors want to park their money elsewhere could have a similar impact. If the risk of investing in a country rises, investors will likely sell assets in the country’s currency, its currency will depreciate, and the country’s goods and services will become more competitive.

Yet it hardly seems wise to adopt policies such as increasing risk for investors, or higher taxes on capital or more regulation, (all of which could make dollar assets less attractive and reduce the dollar exchange rate) just to keep out foreign investors and raise the current account balance. Indeed, nobody in the United States is recommending such an approach. This means that—despite changes in tax regimes or trade treaties—the US current account will likely continue to show the deficit necessary to allow foreigners to accumulate dollar assets.

© 2021. See Terms of Use for more information.