Winning in middle-market banking has been saved

Winning in middle-market banking New strategies and new tools

18 February 2016

Although many middle-market customers seem satisfied with their current banking relationships, that’s no guarantee of success in the future. Here are three strategies that can help banks sharpen their competitive positioning and compete against new players.

Changing competitive dynamics

“I would say the competitiveness on the rates are pretty steady. We are not seeing an undue amount of pressure except in the middle-market C&I space.”

Richard Davis, chairman, president, and CEO, U.S. Bancorp1

“And the one that is most challenging, but still growing, is middle-market [lending]. Fiercely competitive; everybody is chasing the sector.”

Marianne Lake, chief financial officer, JPMorgan Chase & Co.2

These comments on the growing competition in US middle-market lending are not atypical. Banks, both large and small, have been aggressively targeting the middle-market segment and attempting to grow their wallet share for some time now. The good news is that some of these strategies appear to have succeeded—many middle-market customers seem satisfied with their current banking relationships. But this is no guarantee of success in the future. Banks need to realize there are two main forces that could diminish their position in this space:

These comments on the growing competition in US middle-market lending are not atypical. Banks, both large and small, have been aggressively targeting the middle-market segment and attempting to grow their wallet share for some time now. The good news is that some of these strategies appear to have succeeded—many middle-market customers seem satisfied with their current banking relationships. But this is no guarantee of success in the future. Banks need to realize there are two main forces that could diminish their position in this space:

- Banks are generally perceived to be competing mainly on price—there is limited product or service differentiation.

- Disruptive forces evident in consumer and small-business banking, such as marketplace lending and digital banking, are likely to reshape the competitive dynamics in the middle market as well.

In the news

Read the American Banker articleOur analysis suggests that middle-market banking is entering a new battle zone. To win in this new competitive landscape, institutions will not only have to sharpen their existing competitive positioning but also devise new strategies and tools to effectively compete against new players.

The importance of middle-market banking

The middle market continues to lead the US economy with very strong domestic confidence and revenue gains.—Thomas A. Stewart, executive director, National Center for the Middle Market

While Stewart’s statement refers to all middle-market companies with annual revenues between $10 million and $1 billion, it is just as applicable to firms at the lower end of the spectrum; that is, those with annual revenues between $10 million and $100 million. In our study, we focused on these smaller middle-market companies for two reasons: First, they are an attractive segment for financial services firms, and second, this is where we see the next wave of disruption happening as marketplace lenders and other fintech firms move into this space.

In recent years, this group, similar to its larger counterparts,4 has outperformed the US economy. For instance, average quarterly revenues for companies in this segment grew by 6.6 percent year-over-year (YoY) in the second quarter of 2015 (2Q15)5 compared to GDP growth of 2.7 percent6 (figure 1). In addition, employee headcount at these firms increased by 3.8 percent YoY,7 compared to the US economy’s 2.1 percent employment growth in 2Q15.8

More importantly, it is reasonable to expect this growth trajectory to continue. The middle-market segment we surveyed is quite diverse, spanning a variety of industries. Many are local private businesses, although more of them are exploring international expansion plans. As these firms grow, so will their financial needs. According to a Deloitte Growth Enterprise Services (DGES) survey conducted in June 2015, nearly half of the middle-market firms with $50 million and $100 million in annual revenues plan to increase capital expenditure in the near future; about a third expect additional financing; and more than half are likely to engage in an M&A transaction as an acquirer in the next 12 months (figure 2).9

The emerging needs of this diverse segment present a huge opportunity for banks, but to fully capitalize on this potential, banks will need to develop more impactful strategies through innovation and differentiation.

About the study

- Andrews Research conducted telephone interviews with 100 key executives at middle-market firms with annual revenues between $10 million and $100 million in September and October 2015. (For the purpose of this survey, “primary bank” was defined as the financial institution with which the respondent’s firm has the most important banking relationship.)

- Respondents were C-suite level executives—including CEOs and CFOs—responsible for selecting and interacting with banks.

- Respondents were distributed uniformly across industries and revenue size.

Middle-market firms’ banking relationships

Before analyzing the potential in the middle-market segment, we first tried to understand their current relationships with banks and gauge their degree of engagement with and perceptions of the services offered by their primary banks. Following are the key findings from our survey:

Middle-market customers are loyal . . .

The middle-market firms we surveyed have long-lasting relationships with their primary banks. This is true across multiple product categories (figure 3). Their average tenure is nearly 17 years for deposits and transactional services, 15 years for credit, and 14 years for investment banking and other financial services.10 What is equally impressive is that these relationships with primary banks are highly sticky.

According to our survey, 82 percent of middle-market customers are unlikely to switch their primary bank in the next two to three years.

. . . and have positive perceptions of their primary bank

Not surprisingly, given their loyalty, middle-market respondents view their primary bank quite positively (figure 4). About eight in ten believe their primary bank is fair in its pricing and responds to queries promptly. And over three in four respondents agreed that their primary bank “fully understands their needs.” A similar proportion feel their primary bank is a trusted advisor for their company.

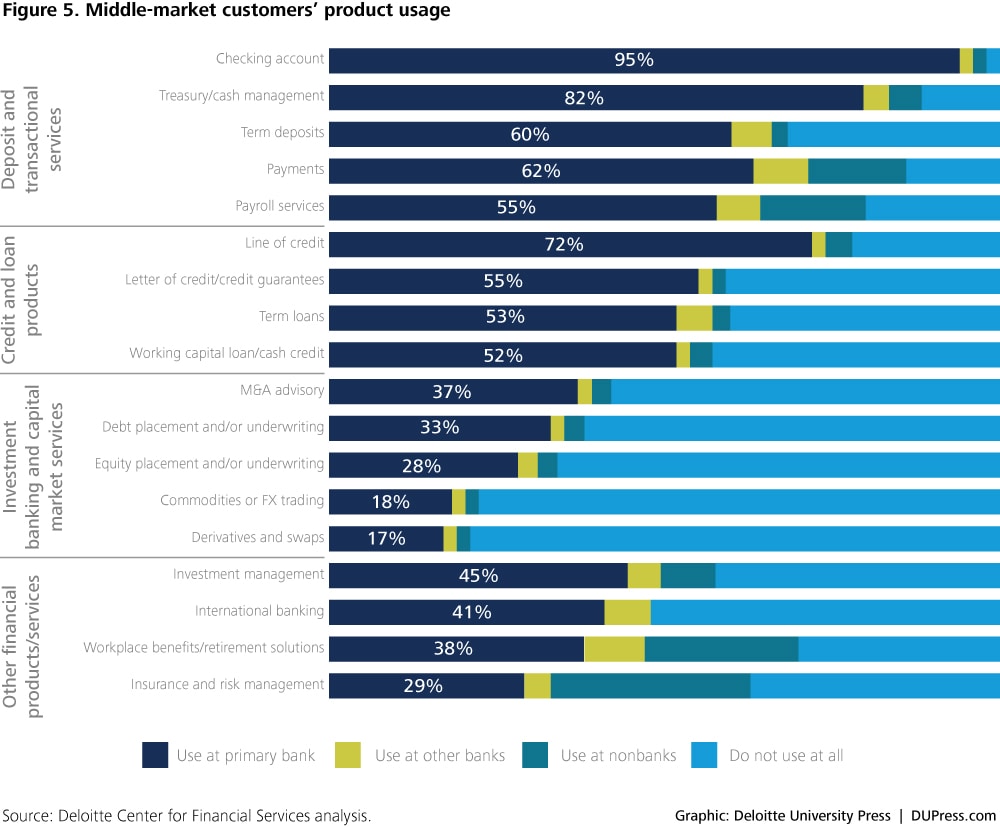

Middle-market firms use their primary banks mainly for traditional offerings . . .

Most respondents say their primary banking needs are in traditional product categories such as deposits, lending, and cash management (figure 5). Very few reported using capital market services such as M&A advisory, equity/debt underwriting, or derivatives and swaps.

. . . and mostly rely on primary banks to meet their overall financial needs

Eighty-six percent of respondents consider their primary bank as the “go-to” provider for all their financial needs. Also, of the ten banking products that a middle-market customer uses on average, seven are with their primary bank. Perhaps this is not surprising, given that the primary bank is the institution with which they have the most important banking relationship.

Middle-market firms appear to have more product relationships with regional/community banks, compared to large banks.

Regional/community banks command a higher wallet share among middle-market customers

According to our survey, middle-market firms appear to have more product relationships with regional/community banks, compared to large banks.11 Regional/community banks also enjoy more favorable perceptions and stronger relationships with their middle-market clients, compared to the larger institutions. For instance, 82 percent of respondents whose primary bank is a regional/ community bank consider them to be a trusted advisor, compared to 69 percent of respondents whose primary banking relationships are with large banks. Regional/community banks’ greater focus on commercial clients’ needs after the financial downturn12 while competing with large banks at the same price points (as our survey demonstrates) has likely paid off in the form of higher satisfaction among their middle-market clients.

Fragmented relationships and growth of nonbanks: A sign of things to come?

The fact that many middle-market customers are currently satisfied with their primary banks is certainly reassuring. However, as they grow and their financial needs become more sophisticated, how will this reliance on their primary bank change, and would they be open to new relationships? We analyzed these questions by asking middle-market customers about their willingness to extend their banking relationships to other institutions over the next two to three years.

We [will] probably go to another provider . . . [having] expertise in those areas [capital markets], not our existing banks.—Survey respondent

Nearly half of middle-market respondents—mostly those who already use both basic and sophisticated/specialized products at their primary bank—are likely to consolidate their relationships with a single institution. However, our survey reveals that nearly a third of middle-market customers at both regional/community and large banks are willing to establish relationships with other banks and nonbanks (figure 6). Analysis of this group of respondents highlights two distinct customer groups:

- Customers who already have a relationship with other banks and nonbanks for sophisticated banking needs

- Customers who currently have limited banking needs (that are largely met by their primary bank), but are open to working with other financial institutions as their financial needs become more specialized

Our survey suggests that a significant number of middle-market respondents value specialist firms for offerings such as investment banking and capital markets services.

But why are middle-market customers willing to look beyond their primary bank?

There are two possible reasons. First, our survey suggests that a significant number of middle-market respondents value specialist firms for offerings such as investment banking and capital markets services. Second, banks have been scaling back their presence in the riskier subgroup of the middle-market segment, in part prompted by federal regulators’ leveraged lending guidelines. This has opened a window of opportunity to nonbanks, including private equity firms, hedge funds, business development companies, and marketplace lenders.13

Middle-market firms also appear to be more open to working with nonbanks now. Admittedly, the numbers are small at this time, but 15 percent of our survey respondents consider nonbanks as serious competitors to traditional banks, and 12 percent are more open to working with a nonbank today than they were two years ago. Our survey suggests that middle-market customers are keen to work with nonbanks for payments and payroll products, likely for ease of use and rich user experience.

Refining middle-market banking strategies for the future

Based on our analysis of the customer and competitive dynamics in the middle-market segment, banks should refine their strategies in three areas (figure 7):

- Retool product portfolios to meet customers’ evolving needs

- Revamp customer strategies to deepen profitable relationships

- Reorient operating models to position for digital transformations

Retool product portfolios to meet customers’ evolving needs

For a number of years, banks have focused on expanding their product portfolios to gain a larger share of the middle-market segment’s wallet.14 Treasury, payables management, payroll processing, debt placement, and investment management are some of the many offerings in most banks’ middle-market product suite now. However, our research suggests that in the future, when middle-market firms’ needs become more complex and they are exposed to nonbanks, some of the gaps in traditional bank offerings are going to become more pronounced. To encourage customers to consolidate their financial needs with them even in the future, banks should start planning for customers’ evolving and more sophisticated financial needs.

Expand product portfolios and target new market segments

Despite efforts to broaden their product suite, anecdotal evidence suggests that banks serving the middle-market have some gaps in their portfolios. To fill these gaps, banks may consider providing value-added services that complement their core offerings. Solutions targeting cash flow management, working capital finance, supply chain finance, and payments are likely to appeal to many middle-market customers. For example, U.S. Bancorp recently enhanced its payment offerings to include an app-based mobile payment tool for its aviation customers, which allows them to directly pay for fueling and services from their mobile devices.15

Banks can also pursue acquisitions to penetrate adjacent markets, target new customers, or expand their product portfolios. For example, through the acquisition of GE Capital’s Corporate Finance unit, Wells Fargo will be adding the former’s entire portfolio of secured loans and leases to middle-market clients in the United States and Canada.16 The acquisition will also help the bank expand its existing asset-based lending offerings and attract new clients.17

I don’t know what is going to change to cause pure middle-market lending-only relationships to be any more attractive, which is why we are focused so much on growing fee income in the cross-sell relationship.—Bill Demchak, chairman and CEO, PNC Financial Services

Similarly, meeting the needs of middle-market customers with international aspirations is another fertile area for banks, especially in trade finance, foreign exchange services, and international payments. Many respondents in our survey indicated that finding a single institution that can meet all their needs in international banking has been a challenge.

What will also become increasingly important for banks is their ability to customize products to meet their customers’ unique needs in an effort to ward off any potential threats from nonbanks. Ultimately, banks need to decide which product categories they would like to deepen their presence in and which products would be feasible to provide. But winning in the middle-market will require banks to provide the right product mix for their customers.

Focus cross-selling efforts around fee-based products

While banks have had great success in traditional lending and deposit products, the same is not true for some of the fee-based services such as investment banking, investment advisory, insurance, and retirement planning (figure 5). Our survey does indicate that many middle-market customers do not currently need these services. But it is also likely that lack of awareness about some of these offerings is another reason for this adoption pattern. If so, it would behoove banks to increase awareness of these services in anticipation of customers’ future needs.

To cross-sell fee-based products, banks could also consider providing incentives such as volume-based discounts, fee waivers, and lower processing fees to deepen relationships with their profitable customers. It is not clear to what extent these programs are in place in middle-market banking at this time. Banks also have the opportunity to cross-sell some of their retail products like personal wealth management to the executives of these firms. Services like retirement plans, estate planning, trust services, and investment advice are likely to appeal to these customers, as their primary bank also understands the professional environment in which these executives operate.19 For example, SunTrust’s private wealth management advisors offer solutions to meet business owners’ unique wealth management needs.20

It is also important to instill an efficient cross-selling culture and to train marketing executives and relationship managers (RMs) to proactively reach out to customers with creative solutions for their existing or emerging needs. This may be particularly challenging for fee-based businesses, where the marketing strategies and sales cycles are likely to be quite different from traditional lending products. Instilling a cross-selling culture in these circumstances will be easier said than done, but those institutions that are able to lead in this area could reap rich rewards.

Revamp customer strategies to deepen profitable relationships

Although banks have traditionally relied on better terms and rates to sell products, our survey suggests middle-market customers are also looking for a “customized solutions provider” rather than just a provider of generic products. While doing so, banks should try to balance service levels with customer profitability.

I am looking for a financial institution as a partner in business to help grow the business.—Survey respondent

You lose deals on price, but win on relationships.—Peter Cosgrove, regional president and senior director of commercial banking, First Niagara

Strengthen delivery of non-price value

Middle-market customers attach high importance to price—many say better rates and terms are the primary reason for their purchase decision across a range of product categories. However, they also indicate a strong preference for personalized and customized service (figure 8). For example, a middle-market business is likely to appreciate its RM’s advice on what type of credit would best suit a particular financing requirement,22 or how financing structures can be modified in a rising interest rate environment, or how treasury management operations can be automated to manage liquidity. A strong value proposition for this segment encompasses delivering compelling non-price value, especially in noncredit products.

Customers may also be keen to get banks’ advice on technology, especially fraud prevention and cybersecurity. As a case in point, middle-market respondents of DGES’s latest survey of technology trends highlighted information security as an issue that will have the biggest impact on their business over the next 12 months.23

Building a reputation for value-added services will require banks to further deepen industry expertise, fill leadership positions for niche expertise, and more importantly, retain RMs who have a reasonable level of understanding of the business dynamics in the local markets.24 Banks could also set up resource centers to help middle-market customers better understand the impact of macroeconomic and industry changes to their businesses. For example, benchmarking analysis and best practices could prove to be useful to customers who are struggling to decode the changing business landscape.

Drive customer profitability measures

Lending-based relationships have traditionally been the cornerstone of banks’ relationships with their middle-market customers. However, not all of these relationships are profitable, as stiff price competition and stringent capital and liquidity requirements further constrain a bank’s ability to make reasonable profits.25 As such, it is important that in addition to building customer relationships, banks equally focus on maximizing customer profitability. Segmenting customers based on their profitability rather than the perceived value will be important. For this, relevant customer profitability parameters, such as current product usage levels, cost-to-serve, potential future earnings, and risk parameters (such as probability of default) should be considered while pricing products or deciding on service levels for various customer groups. Further, a more efficient service delivery system can be established to provide low-value, standardized services to relatively less profitable customers.

Finally, to optimize sales efforts, banks could link RMs and product specialists’ performance incentives to customer profitability rather than basing them solely on sales volume.

Explore new ways to target customers

According to our survey, middle-market customers are highly satisfied with their primary banks and are even willing to recommend their banks to peers. Seventy-nine percent of middle-market customers surveyed are likely to recommend their primary bank for deposits and transactional services (figure 9). To benefit from such high customer advocacy levels, banks could consider rewarding successful referrals and client conversions with fee waivers or rate discounts, especially on low cost-to-serve or standardized products. Convincing these customers to become the bank’s brand ambassadors can augment banks’ own cross-sell and acquisition rates.

Similarly, customer outreach programs, either through networking events or social media platforms, could be an effective way of spreading awareness about various financial offerings while also engaging with customers and generating potential sales leads.26

Reorient operating models to position for digital transformations

The changing middle-market business dynamics and impact of disruptive forces will require banks to embrace new technologies and fix internal collaboration and infrastructure challenges to position themselves for the future.

We want to know their [primary bank’s] plans for the next 10 years and what they are going to do about their ways [business strategy and operating model].—Survey respondent

Embrace digital technology and alternate channels

To keep pace with evolving market dynamics, improve process efficiencies, and be quick to market, middle-market customers are increasingly investing in technology. Similarly, they expect their financial services providers to support them with banking platforms that will complement their transformation.27 A Greenwich Market Pulse survey highlighted that more than half of mid-sized companies expect a credit decision within a week, but about one-third of mid-sized companies that had recently applied for bank credit described the documentation process to obtain a loan to be “extremely/somewhat difficult.”28 Such inefficiencies and inferior customer experiences can lead to customers switching to other providers, especially to nimble and technologically advanced nonbanks.

Replicating digital advancements in the retail online and mobile channels for middle-market clients will likely enhance ease of use, provide greater access to near real-time information, and improve customer experience. For example, some regionals banks provide enhanced payment solutions to their commercial card customers through electronic accounts payable offerings. These products are designed to enable easier and faster payments to the commercial clients’ vendors via online platforms, significantly reducing the need for them to issue checks.

A generational shift in the workforce at these commercial clients would further strengthen the case for such advancements.29Executives are increasingly preferring mobile apps or tablet-based tools, which offer mobility and convenience.30

Overcome internal infrastructure and collaboration challenges

Providing a seamless customer experience across various lines of business and functions is not an easy task for many banks.31 Gaps in infrastructure and operating models are typically the biggest roadblocks in this context, as many banks struggle with legacy and siloed infrastructure. This advice is of course relevant to other areas in banking as well, but leveraging innovative plug-and-play technologies could help banks overcome some of these challenges. For example, Deloitte’s BankApp for Origination and Onboarding leverages the Salesforce platform to streamline the business processes for originating new accounts and onboarding customers.32

Siloed business units and infrastructure also impede banks’ ability to obtain a holistic view and assess customers and their emerging needs. Here, data analytics can play a huge role in providing a better customer experience. Investing in better analytical tools could enable banks to estimate product/customer profitability parameters and develop a better understanding of customers’ product usage trends and patterns. Such investment could also help banks coordinate efforts to target their customers with appropriate offers and service levels to improve overall customer profitability and experience.

The way forward in middle-market banking: Partnerships could be key

The stakes are high: The middle-market business has historically been an important source of loan growth for banks, and perhaps now is an even more important source of relationship-building and cross-selling opportunities. Ensuring that they retain their dominance in the core lending and deposit front is a strategic imperative, as is expanding into newer territories of other fee-based products. The strength of their local army of middle-market business advisors—RMs—is one of the most critical weapons in banks’ arsenals. They can play a crucial role in multiple areas, including understanding middle-market customers’ banking needs, developing relationships, and delivering industry expertise and customized solutions.

I don’t know why financial institutions would take over for the other providers that are specialized.—Survey respondent

Banks should be ready to go on the offensive. Our analysis of banks’ actions in the middle-market space in the past 12 months has indeed revealed that there have been considerable efforts among banks to beef up their presence in this space through various strategic initiatives and leadership appointments (figure 10).

But do banks have to fight this battle alone?

Banks could explore collaboration opportunities with other market participants. Depending on the type of offerings, customer groups being served, expected profitability, and risks involved, sometimes collaborating with other players could be a faster and more efficient approach to meeting customers’ emerging needs. For example, Regions Financial acquired a middle-market M&A firm in October 2015 to strengthen its advisory capabilities and boost fee income.33 Similarly, to overcome the constraints set by the leveraged lending guidelines and capital requirements, banks are seeking partnerships with business development companies to facilitate junior debt (second lien loans) for middle-market customers.34 Banks could also collaborate with nonbanks to embrace newer data sources, algorithms, and advanced analytics used by marketplace lenders, for example, to strengthen underwriting practices.35

Future prospects of winning in the middle market will depend on how well banks position themselves before the disruptive forces and new players like marketplace lenders gain prominence. Acquisition, collaboration, and organic growth are all important tools, which, if used wisely and in a cost-efficient manner, can help banks maintain their competitive edge. Banks are currently in a position of strength, and by efficiently reorienting themselves to cater to customers’ evolving needs, they can potentially continue to dominate the battle for middle-market customers.

About the Deloitte Center for Financial Services

The Deloitte Center for Financial Services (DCFS) is a source of up-to-the-minute insights on the most important issues facing senior-level decision makers within banks, capital markets firms, mutual fund companies, private equity firms, hedge funds, insurance carriers, and real estate organizations. We offer an integrated view of financial services issues, delivered through a mix of research, industry events and roundtables, and provocative thought leadership—all tailored to specific organizational roles and functions.

Deloitte provides a variety of services relevant to middle-market banking:

Our Strategy and Operations practice works with senior executives to help them solve their toughest and most complex problems.

Our analytics and information management teams can provide support in transforming customer data into actionable information.

Deloitte Digital offers creative and digital capabilities that can cater to middle-market customers’ digital preferences.

Our technology strategy and architecture and systems integration specialists can help banks develop strategies and implement systems that build business value and overcome complex systems integration challenges while serving middle-market firms.

Deloitte Advisory helps banks avert unwarranted cyber, strategic, or operational risks.