Digital transformation in financial services has been saved

Digital transformation in financial services The need to rewire organizational DNA

07 November 2016

Financial services firms continue to effectively leverage digital technologies to innovate and improve the customer experience. But our new study reveals that to become fully digital enterprises, many FSI firms may need to shift the focus inward and innovate the employee experience.

In the quest to achieve market leadership, financial services industry (FSI) firms continue to focus on becoming holistically digital, customer-facing enterprises. But are they there yet? The 2016 Digital Business Global Executive Study and Research Project (“the survey”), the fourth annual study conducted by MIT Sloan Management Review and Deloitte Digital on this topic, offers some revealing insights and their implications.

Learn more about the Deloitte Center for Financial Services

Tell us what your digital future looks like: Take the 2017 MIT Sloan Management Review and Deloitte Digital survey

The survey showed that overall, the financial services industry is on the cusp of a digital transformation right now. FSI firms are making significant investments to enhance customer experience and engagement through the development of new digital products and capabilities. The survey revealed that of the FSI firms with a digital strategy, 93 percent agree or strongly agree that the objective of their digital strategy is to improve customer experience and engagement.

Throughout the industry, there is widespread digital disruption. A full 90 percent of respondents agreed or strongly agreed that digital technologies are disrupting the industry to a great or moderate extent. Yet the study also showed that a majority of the financial institution employees surveyed do not believe their firms are ready for this disruption. Only 46 percent of FSI respondents agree or strongly agree that their firms are adequately preparing for digital disruption, marginally better than the 44 percent last year.1 So what’s holding FSI firms back from fully embracing the digital world and all that becoming digital entails?

To help answer this question as completely as possible, in addition to our research findings and analysis, we have also included industry-specific case studies, along with cross-industry case studies, of digital transformation in action. The cross-industry examples—GE, CBRE, Whirlpool, and Amazon—can be found in the Appendix.

What about the employee experience?

It appears that as a whole, the industry has not fully explored what it means to be digital, from the inside out. Many FSI firms, focused primarily on leveraging digital capabilities to become customer experience champions, have not devoted enough attention to the other side of the coin: the employee experience. For the purposes of this report, the term “employee experience” is defined as how employees feel about their organizations with regard to both opportunities for growth/skills development, and employees’ willingness to continue to work for their current firms. The following survey findings reveal that employee experience remains a blind spot in FSI firms’ digital efforts (see figure 1):

- A full 76 percent of the survey respondents consider it very important or extremely important to work for an organization that is digitally enabled or is a digital leader.

- Only 38 percent of FSI respondents agree or strongly agree that their organization offers employees the resources or skill-development opportunities they would need to thrive in a digital environment.

- Nearly half—41 percent of survey respondents—plan to stay at their current organizations for three or fewer years.

A blending of focus on customer experience and employee experience is key to better preparing FSI firms for a digital future. In a recent interview, Donna Morris, executive vice president of customer and employee experience at Adobe Systems, explained, “By combining employee and customer experiences, we are able to create rich customer experiences through high levels of employee engagement.”2

But how can FSI firms improve the employee experience? This can happen when an organization successfully aligns its culture—a system of values, beliefs, and behaviors that shapes “how work gets done”—with the business, operating, and customer models found in digital enterprises. This is largely because, in a dynamic digital environment, the legacy approaches involving a firm’s adaptability to change, work style, leadership style, decision making, or for that matter, risk appetite, may not be effective.

Research suggests that culture gets hard-wired over time and is difficult to change.3 According to Maile Carnegie, group executive, digital banking at ANZ Banking Group Limited, “[Culture is] the hardest thing to get right, but it's also got the highest leverage. The highest return on investment is getting that culture right.”4

So, which behaviors should FSI firms demonstrate and where should they start? It should be pointed out that while Deloitte has a very comprehensive and robust approach to organizational culture, this report will focus on a highly specific subset of culture—Digital DNA. Deloitte’s Digital DNA framework outlines the traits and characteristics of “being” digital, and what it takes for businesses to thrive in a digital world.

Many financial institutions have failed to recognize that digital business is fundamentally different in many ways, and that simply doing the digital things described above will not suddenly make them digital. In other words, while many FSI firms have leveraged digital technologies to extend their product and delivery capabilities, they have not yet rewired their organizations’ business, operating, and customer models to actually being digital. We explore this purposeful reorientation of Digital DNA attributes in greater detail in the following sections.

Demystifying Digital DNA

Being digital is significantly different from the traditional way of doing things in FSI firms. As our survey suggests, FSI firms’ legacy cultural attributes include a protracted response to change, siloed work style, hierarchical organizational structure, and a cautious, regulation-determined risk appetite, among other behaviors (figure 2).

On the other hand, Digital DNA behaviors create the environment that enables firms to do business digitally. We have grouped Deloitte’s Digital DNA framework’s characteristics into five categories for purposes of our study: agility, collaboration, distributed organizational structure, bold risk appetite, and customer centricity.

As figure 2 shows, there may be some extent of commonality between the legacy DNA and Digital DNA attributes. Customer experience is a good example, where FSI firms have been doing digital and investing in new products and capabilities. That said, many FSI firms have the scope to improve real-time collection of customer data and provide more relevant on-demand experiences. Given the fact that FSI firms already recognize the importance of using digital technologies and are taking proactive steps to enhance customer experience, we have kept customer experience out of the purview of discussion in this report.

In contrast, there are some Digital DNA attributes that are potentially in conflict with the legacy way of doing things—for example, risk appetite. Here, it’s essential to strike a balance, which could allow firms to remain cautious when engaging in high-risk activities, but lend a freer hand and become more exploratory when handling less-risky ones. Banks opening up their APIs to allow technology firms to build applications for their customers could be viewed as one such exploratory move.5

Digital DNA attributes better prepare FSI firms for a digital disruption

So, if FSI companies recognize the importance of using digital technologies to enhance customer experience, how can they use the notion of Digital DNA to help them better prepare for digital disruption? For purposes of this report, we have delved deeper into attributes of Digital DNA that can help FSI firms improve the employee experience. We also assess the positive correlation between companies’ Digital DNA attribute strength and employees’ willingness to work in such companies for a longer tenure.

But what do these Digital DNA attributes entail? Let’s understand them in some detail.

Agility

Agility refers to a firm’s ability to move rapidly and flexibly in order to make adjustments in a continuously disruptive ecosystem. In fact, the constant disruption and innovation in digital businesses tend to result in new models of what the work is and how work gets done. Job descriptions, tasks, skills, and requirements also tend to be highly fluid. Indeed, traditional FSI firms may move slower as compared to a digital enterprise and the uneven velocity between the legacy and digital business is likely to create friction between the legacy and digital operating models. According to the survey, lack of organizational agility is one of the biggest barriers impeding firms from taking advantage of digital trends.

FSI firms should recognize and develop an approach to minimize the impact of the differences between the two operating models. As highlighted in figure 3, only 19 percent of respondents believe their organizations are nimble. Of these, 71 percent agree or strongly agree that their organization is adequately preparing for digital disruption, as compared to only 34 percent of those considering their firms to be slow/deliberative. Moreover, 68 percent of respondents who said their firms are nimble are willing to work at their organizations for more than three years, compared to 41 percent of respondents who perceived their firms to be slow.

To embed agility into organizations, FSI firm leaders should exhibit the following characteristics:

- Iterative: Update and improve based on rapid and ongoing feedback and analytics insights.

- Fail early, fail fast, learn faster: Allow customers to test pilots of products and services in their minimum viable state. This process enables companies to learn from failures and provide a better offering vs. having an intermittent failure impede progress.

- Fluidity: Enhance ease of movement of talent and resources from one situation or solution to the next and possibly back again, while shifting operating models and offering frequent updates and communications.

- Continuously innovating: Promote continuous innovation by questioning and acting on how or why things are done the way they are, and why they couldn't be done differently. This is important because the digital ecosystem is broad, boundaryless, and dynamic, and new ideas and their different applications are constantly (and at an increased speed) being developed.

Collaboration

Collaboration in today’s work environments involves a mix of virtual and physical employee participation where teams cooperate for a common overarching cause. It’s gaining prominence as a key attribute as digital technologies are increasing customer and employee expectations. For instance, customers expect digital interactions to be both rich and consistent across every touchpoint they encounter, regardless of the channel, while employees expect a more engaged and fluid work environment. While these goals may seem straightforward, meeting these needs often requires multiple team members working together and communicating regularly. Collaboration is essential to aligning goals across technology, people, and processes and to delivering superior customer and employee experiences; therefore, leaders need to design work processes so that intentional collaboration takes place.

As highlighted in Figure 4, 33 percent of the FSI respondents believe their organizations are collaborative. Of these, 62 percent agree or strongly agree that their organizations are adequately preparing for digital disruption, nearly twice the percentage of respondents who consider their firms to have the opposite, or a siloed work style. Further, 64 percent of respondents from the more collaborative firms are willing to stay with their current companies for more than three years, compared to 41 percent of the respondents who perceive their firms to have siloed work cultures.

That said, we recognize some regulatory requirements would necessitate FSI firms to maintain silos in select functions or business lines. However, to embrace a collaborative approach in the broader fabric of organizations, FSI firm leaders should adapt the following elements:

- Morphing team structure: Intentionally design flexible team structures so that they can be formed, reshaped, or disbanded to adapt to changing and varying business needs.

- Democratizing information: In the past, information was usually available and accessible on a need basis. However, digital often increases availability and accessibility of information to various stakeholders such as customers, suppliers, competitors, and employees. As a result, FSI firms need to often provide more clarity about decision and access rights and information security, as these tend to get blurred in digital businesses.

Distributed organizational structure

FSI firms traditionally possess a position-based structure in which the most important decisions are vested with senior management. In this top-down hierarchy, very often there is little focus on nontraditional but new types of stakeholders, such as social media influencers and other residents of the digital ecosystem.

But as firms become more digital, an ongoing shift in decision rights often occurs. Valuable information is increasingly shared with a broader set of traditional and nontraditional stakeholders and new processes/work flows emerge. This can result in changes in power and influence, inside and outside the organization; as a result, there may be less need for layers of structure.

The survey suggests that only 16 percent of the FSI respondents believe their firms to have a distributed organizational structure (figure 5). Of these, 71 percent agree or strongly agree that their organizations are adequately preparing for digital disruption, compared to 32 percent of respondents who perceive their firms to have hierarchical structure. Moreover, 67 percent of respondents at firms with distributed structure are willing to work for their current firms for more than three years, while only 44 percent of respondents from firms with hierarchical structure plan to stay that long.

Bold risk appetite

FSI firms’ risk-taking ability is limited by regulations, especially in the post-2008 environment. And as such, it can be a tricky situation for firms as they build their digital businesses. However, given the increased competition from nimble fintech players and nonfinancial technology companies, FSI firms will likely need to make bold decisions to become digital leaders.

Moreover, with the increase in digital adoption and use of multiple devices, information access is democratized. This technology proliferation also raises concerns around new types of risks, such as cyberattacks and data privacy issues.

FSI firms will need to consider ways to be more flexible in managing their risk and security boundaries, likely by continually planning and monitoring activities, identifying large exposures, and focused action planning. They are also likely to benefit from increased collaboration across functional areas to address risks and security issues.

The survey analysis results in figure 6 highlight that 21 percent of the FSI respondents believe their firms have a bold/exploratory risk appetite. Of these, 71 percent agree or strongly agree that their firms are adequately preparing for digital disruption, more than twice the percentage of respondents who consider their firms have a cautious risk appetite. Further, 65 percent of respondents from the bolder companies are willing to work for their current firms for more than three years, compared to 42 percent of respondents who believe their firms have a cautious risk appetite.

Data-driven decision making

As FSI firms align their digital business to the Digital DNA attributes, it is important for companies to also consider a data-driven approach to decision making. This is because regulators’ expectations for transparency with regard to how decisions are made has compelled FSI firms to move away from instinctive decision making. The good news is that the increased use of technology is changing the quantity, quality, speed, and complexity of data available to various stakeholders. The plethora of data allows companies to make more informed decisions and may also change decision-making criteria. For instance, unlike in the past, FSI firms now have more granular information about customer preferences, behaviors, and feedback. Yet, the survey revealed that only 38 percent of the FSI survey respondents believe their firms have a data-driven decision-making approach.

Consider the example of Toyota Financial Services (TFS), a global organization that provides retail and dealer financing to automotive dealers and their customers. The company has used analytics to enhance risk and customer segmentation decisions. In 2009, already challenged by a drop in demand due to lower automobile sales, TFS experienced a surge in payment delinquencies: A record 100,000 customer accounts entered delinquency, while 60-day delinquencies rose by 25 percent.6 Company leaders realized they needed to abandon a one-size-fits all approach to reduce these delinquencies and adopted a multi-year, analytics-based approach to help solve this costly problem.

Using analytics software along with other technologies, TFS segmented customers into high-risk and low-risk categories, which improved their collection approach. Low-risk customers were treated with a lighter touch, while high-risk ones were followed up more frequently after their accounts entered delinquency. To make the process more efficient and collaborative, both the analytics team and the implementation team were co-located.

As a result of this initiative, TFS grew its portfolio of loans by 9 percent using existing staff resources and more than 50,000 customers benefited because the new process enabled them to keep their cars by avoiding loan defaults.7 The company is now planning to utilize a similar analytics-driven approach to improve its loan origination process.

Current strength of Digital DNA attributes among FSI firms

While it may seem attractive in terms of reasonable goal-setting, the vast majority of FSI firms should not expect a complete turnaround of their digital transformation efforts by perfecting a single Digital DNA attribute. Rather, we have found that most firms can reap significant rewards by incrementally embracing multiple attributes.

To lend credence to this hypothesis, we analyzed the strength of FSI respondents’ Digital DNA as a combination of the four cultural attributes discussed earlier (figure 7). The exercise yielded three distinct cluster profiles: the evolving adopters, the enthusiastic progressives, and the experiential drivers. (For methodology, see sidebar, “How digital is your organization?”)

How digital is your organization?

We performed a profiling exercise to understand the differences in the strength of FSI firms’ Digital DNA. A cluster analysis was used to arrive at three mutually exclusive clusters based on the strength of the four Digital DNA attributes: 1) agility, 2) work style, 3) organizational structure, and 4) risk appetite.

Who are the evolving adopters?

The evolving adopters’ cohort comprises survey respondents from organizations that have embraced few Digital DNA attributes. Their firms appear to have leveraged digital technologies to extend capabilities, but often operate in a siloed manner. Comprising 37 percent of the survey’s sample, these respondents rate their firms’ culture to be largely slow/deliberative, siloed, hierarchical, and cautious. These firms appear to have just set out on a digital and cultural transformation journey (see figure 8 and “Real-world spotlight” on ANZ).

Who are the enthusiastic progressives?

The second category, the enthusiastic progressives, represented 38 percent of the FSI sample respondents. This cohort works at firms that likely are more advanced than those of the evolving adopters in all the four Digital DNA attributes (see figure 9 and “Real-world spotlight” on the AXA Group).

Who are the experiential drivers?

The experiential drivers’ cohort work at organizations that are becoming digital—their firms have adopted many Digital DNA attributes by using digital technologies in a more synchronized manner than have many of their peers. Comprising 25 percent of the survey sample, they also far surpass many peer companies on cultural attributes, such as agility, collaborative work culture, bold risk appetite, and distributed structure (see figure 10 and “Real-world spotlight” on BBVA).

That said, the journey of cultural transformation does not end here for the experiential drivers. They have yet to mature to being digital firms, a stage in which digital is woven into the fabric of the entire organization.

Where do you start the rewiring?

“We are a technology company,” said Marianne Lake, CFO, JPMorgan Chase, during the company’s Investor Day this past February.8 Echoing Lake’s comments, FSI firms will continue to invest in digital, with the dual goals of delighting customers and keeping pace with competition. To emerge as holistically digital enterprises, though, companies need to focus on their cultures and work on enhancing both the customer and the employee experience. To get started, FSI firms should evaluate the status of their digital transformation journey; with this knowledge, they can begin to devise a plan to transform their cultures.

In this process, it’s important for FSI leaders to avoid the temptation to try to change everything at once. Organizations should identify and rewire the Digital DNA attributes at an acceptable pace vs. instituting a complete overhaul. FSI firms may initially choose to focus on certain aspects of the Digital DNA depending on current organizational constructs and their ability to meld the new cultural attributes with the legacy operating models. Once companies have successfully adopted incremental changes, and more and more Digital DNA attributes get woven into the fabric of their organizations, leaders can consider increasing the pace of the rewiring. But one of the common mistakes firms make is that they treat legacy and digital as two different models, which often fosters resistance. Instead, leaders should focus on adopting key digital processes that flow back into the legacy business.

Here are some steps that FSI firm leaders can consider as they rewire their cultures:

1. Navigate the ‘unevenness’ between legacy and digital operations

One of the biggest challenges in cultural rewiring is bridging the gap between legacy and digital operations, as the former often sub-optimizes or neutralizes valuable investments in the latter. This happens because there are significant differences in operating models, speed of business, agility, fluidity, and customer involvement. FSI firms should begin by completing a detailed review of key workflow patterns and interactions.

2. Lay down the roadmap for rewiring the culture

Next, FSI firms should select workflows and develop processes that can lead to seamless operations across the legacy and digital businesses. Here, it is often best to first focus on a few processes that are likely to make a difference, identifying and linking the critical processes between legacy and digital work. Employees should be given appropriate training and continuous learning opportunities to equip them with the requisite knowledge and skills to transition from the legacy working style to the digital ones.

3. Foster greater collaboration between different operations and approaches

Finally, as companies evaluate workflows, they need to collaborate intentionally. This is important because typically, the coexistence of these two different models can slow down operations and can lead to questioning of decision-making processes, which is often exacerbated by ineffective communication. To overcome this challenge, FSI leaders should design a change management plan that ensures that employees learn to transition between old and new ways as seamlessly as possible. Leaders should take the time to clearly communicate issues surrounding responsibility, accountability, and decision making. Throughout the rewiring process there will be disruption, but FSI firms should focus on minimizing that disruption to their legacy operations.

In summary, as Bob Contri, global financial services industry (GFSI) leader, Deloitte Touche and Tohmatsu Limited, recently stated at Deloitte’s annual Global Financial Services Industry conference, “The buzz in the room is on technology, not only about how it will change our day-to-day business, but how will it affect our talent. It’s an aspect that we have not really touched on yet. We all need to consider how we can utilize these new technologies to steer our people, and therefore our organizations, to lead us to real transformation.”

Appendix

Case studies on rewiring Digital DNA attributes

About the research

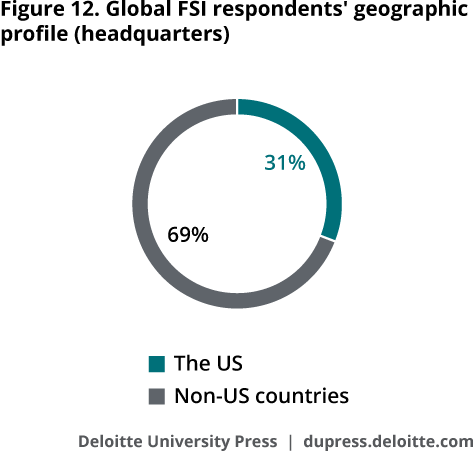

This report leverages data from the 2016 Digital Business Global Executive Study and Research Project, conducted by MIT Sloan Management Review and Deloitte Digital. To understand the challenges and opportunities associated with the use of social and digital business, MIT Sloan Management Review, in collaboration with Deloitte Digital, conducted its fifth annual survey of more than 3,700 business executives, managers, and analysts from organizations around the world. Completed in the fall of 2015, the survey captured insights from individuals in 131 countries and 27 industries, including organizations of various sizes. Nearly two-thirds of the respondents were from outside of the United States (see figures 12 and 13). The sample was drawn from a number of sources, including MIT Sloan Management Review readers, Deloitte Dbriefs webcast subscribers, and other interested parties. In addition to the survey results, business executives from a number of industries, as well as technology vendors, were interviewed to understand the practical issues facing organizations today. Their insights contributed to a richer understanding of the data.

For purposes of this report, we analyzed the 436 FSI respondents from the banking (42 percent), asset management/private equity (22 percent), construction and real estate (19 percent), and insurance (17 percent) sectors.

© 2021. See Terms of Use for more information.