FATF Mutual Evaluation Report results released has been saved

Article

FATF Mutual Evaluation Report results released

Scores are positive, but the quest for more effectiveness remains

On August 24 2022, the Financial Action Task Force (FATF) released a report on its Mutual Evaluation of the Dutch AML framework. The report is significant, as over a decade has passed since the last FATF evaluation of The Netherlands. The overall scoring is positive, resulting in the question: how will this report impact the AML debate?

This blogpost provides an overview of FATF observations. As you will read below, the general rating of The Netherlands effectiveness and technical compliance levels is relatively positive. There are also some specific recommendations to address suboptimal outcomes against FATF’s standards. This means the Dutch AML framework has technically passed its exams, while the quest for more effectiveness in practice is not yet addressed.

Read our previous blog post to get an understanding of the Mutual Evaluation process itself and what role FATF plays within the global AML ecosystem.

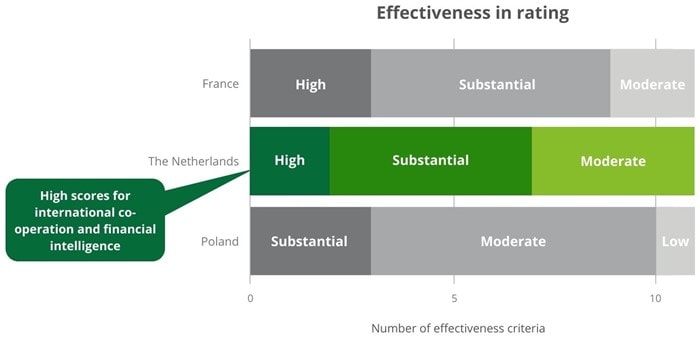

Scoring

Of the 11 effectiveness criteria that FATF applies, 2 criteria are scored as ‘high’ on effectiveness (on international co-operation and financial intelligence), 5 criteria are scored ‘substantial’ and 4 criteria are scored ‘moderate’. This also implies no criteria are scored by FATF as ‘low’ on effectiveness.

On the 40 FATF recommendations, The Netherlands is evaluated to be fully compliant to 10 recommendations and largely compliant to 28 recommendations. Only for 2 recommendations the score ‘partially compliant’ is provided, related to Correspondent Banking and New Technologies (Virtual Assets). For no recommendation The Netherlands is evaluated as non-compliant, though being non-compliant is in practice rare for a European country.

Overall, this is a relatively good outcome for The Netherlands. When compared to other countries that have recently been evaluated by FATF, these scores are for example marginally lower then France (especially on compliance to the recommendations), but better than Poland, and clearly better than Bulgaria, Croatia and South Africa. And as a historic reference: in 2011, The Netherlands was evaluated as only partially compliant with 22 of the then 49 recommendations.

Key observations

The full report gives a long list of observations supporting the scores. Observations that are highlighted in the evaluation report entail:

Financial intelligence, prosecution and confiscation

- The Netherlands is praised for a good understanding of its money laundering risks, as documented in the National Risk Assessment (NRA) on money laundering. It is also noted though, that for financial institutions the risk descriptions and assessments in the NRA are not granular enough.

- Co-ordination and co-operation in the AML chain at both policy and operational levels is named a key strength. It is recognized that multiple platforms for public-public and public-private cooperation are being leveraged and developed, and The Netherlands is identified as a leader in public-private partnership and information sharing to combat money laundering.

- Law enforcement is observed to have access to a broad range of financial intelligence. Where the effective usage of this information is being criticized in the report published by the Algemene Rekenkamer earlier this year, the FATF mutual evaluation acclaims the high quality products of the Financial Intelligence Unit (FIU) and its usage in law enforcement. The fact that there is a lack of ‘comprehensive statistics’ on the usage of such information is deemed a minor concern.

- On prosecution, FATF flags that the sentencing for money laundering is relatively indulgent in our country. Confiscation of criminal assets is recognized as policy priority, and confiscation results are said to be in line with the country’s risk profile. To the point of outcomes of law enforcement, it is also recognized that statistics are not very comprehensive.

Terrorist financing

- The Netherlands is judged to have a robust framework on Terrorist Financing (TF). However, it is noted that there are (almost) no convictions of non-profit organizations (NPO’s) in TF cases. Moreover, the fact that no formal supervision is executed on TF compliance by NPO’s is regarded a risk.

- When it comes to Sanctions, it is recognized that The Netherlands implements international sanctions without delay. However, it is also observed that sanction implementation by non-financial businesses is not supervised.

Preventive measures and supervision

- Financial institutions are said to have a generally strong understanding of money laundering risks and customer due diligence (CDD) obligations, but less so on terrorist financing risks. The settlements with ING and ABN Amro are said to have a prioritizing effect on AML efforts, in the banking sector and beyond. However, it is also claimed that there is a tendency within financial institutions to classify customers as low risk without adequate justification.

- The understanding by non-financial institutions on their obligations and risks is perceived lower. For instance, the fact that actors such as lawyers and real estate companies file a relatively low number of Unusual Transaction Reports (UTR’s) to the FIU is an indication to this. Moreover, the supervision on CDD obligations for non-financial institutions is generally weaker and subject to a lack of resources.

- The financial crime supervision systems of DNB and AFM are identified as strong by FATF, signalling there is a good understanding of money laundering risks and strong supervisory activities with a robust set of tools (including data analytics). However, the duration of AML/CFT failings by financial institutions in the past lead to the suggestion of FATF that previous actions may not have been sufficiently proportionate or dissuasive.

Transparency

- It is noted that, despite various separate initiatives, there is no coherent overview of money laundering risks associated with the legal forms in The Netherlands. It is noted that various trust legal forms that are possible in other countries, are not allowed in The Netherlands but that foreign trusts are being recognized.

- There is a general challenge in the financial sector to determine beneficial ownership (BO). The fact that the new UBO register is only partially populated, and that verification of records is mainly being relied upon by gatekeepers is seen as a risk.

- The struggle of Dutch government to fight ‘illegal trust offices’ evading supervision is also being mentioned as a problem, while FATF concludes that the authorities do not currently allocate appropriate levels of resources to address these risks.

International cooperation

- The Netherlands is recognized by FATF as a fast responder to international cooperation requests. This is supported by factual evidence and recognized in the international community. International co-operation is well organized and centralized, both on operational and strategic level.

Priority actions

FATF sees 8 priority actions for The Netherlands. These actions should for instance address the topics of lower awareness of money laundering obligations and supervision at non-financial institutions, the backlog in recording of beneficial ownership in the UBO registry, and more firm and dissuasive sentencing of money laundering offenses.

Noteworthy for financial institutions is that FATF encourages supervisors to continue to make use of their formal powers (such as fines), and rely less on informal supervisory measures (like letters and warnings). At the same time, it urges the supervision to be more risk based and to address unlicensed activities (such as underground banking and illegal trust services).

FATF’s impact

FATF evaluation results represent a significant milestone for a country and its financial system. Strong results signal a safe and robust financial system, positively impacting the country’s overall position in the global financial system and the perception of other countries of it as being low risk. These outcomes are key for the positioning of The Netherlands in politics and business.

A final key impact of the FATF evaluation is that the Dutch government will take the opinions and recommendations into account during the (further) development of policies and legislation against money laundering. Likewise, perceptions of other relevant stakeholders are being influenced by FATF opinions. As such, the report is a key contributor to the debate on the future AML framework.

A next step in the AML debate

As we have noted in our earlier blogpost on NextGenAML, the public debate on the Dutch Anti Money Laundering approach has taken off in 2022. The FATF evaluation report is a next step in a chain of events and reports. From an execution point of view, there are many advocates for fundamental change (including us), claiming the current efforts against money laundering are not effective enough. However, as we have seen in FATF’s evaluation outcomes, perceptions at a policy making level might be much more optimistic. Compared to international bureaucratic standards, the performance of the Dutch AML framework is rather good.

These different perceptions at execution and policy level could co-exist, but we will need to connect the two. Being happy on paper but frustrated in practice does not make us successful in the fight against financial crime. AML professionals will need to explain even more and better where the current system stalls and how it should be enhanced for more effectiveness. And policy makers and supervisors will need to look beyond the established legal framework and technical compliance, and continue to listen to ideas on reform to more effectiveness.

The AML debate continues

This autumn, the debate on AML reform will accelerate further, including an update on the National Plan against Money Laundering by the Ministers of Finance and Justice. In September and October this year, Deloitte will be knowledge partner during the Leaders in Finance AML events in Brussels and The Netherlands, where the search for AML effectiveness will be a central theme. The results of an AML survey, conducted by Deloitte and Leaders in Finance, will also be published, outlining the opinion of leading stakeholders in the AML chain in this ongoing debate.

Want to know more?

The full Mutual Evaluation report for the Netherlands can be read here.