Trender

Retailtrender for 2024

Å skape muligheter i et år med usikkerhet

Vi gir deg tre hovedtrender for varehandelen for kalenderåret 2024.

Publisert: 9. februar 2024

Når vi ser tilbake på 2023, vil flertallet av handelsaktører over hele verden reflektere over et år preget av stigende inflasjonsrater, redusert forbrukertillit og høyere utgifter. Tross dette var det grunn til optimisme forårsaket av eksponentielle teknologiske fremskritt med blant annet generativ AI. 2024 vil by på nye muligheter og betydelig fremskritt innen teknologi som vil redusere kostnader, forbedre produktiviteten og kundeopplevelsen.

Imidlertid er det ikke bare fremskritt innen teknologi som gir grunn til optimisme i 2024. Med en global økonomi som viser tegn til bedring, begynner handelsaktørene å se etter nye muligheter for vekst og ekspansjon. I starten av året viste Deloittes Consumer Signals-analyse, som gir en indikasjon på følelsene til titusenvis av forbrukere over hele verden en nedgang i bekymring for inflasjon og en økning i kjøpsintensjon.

Trendene for 2024 vil ikke bare definere det kommende året, men også fremtiden til detaljhandelen.

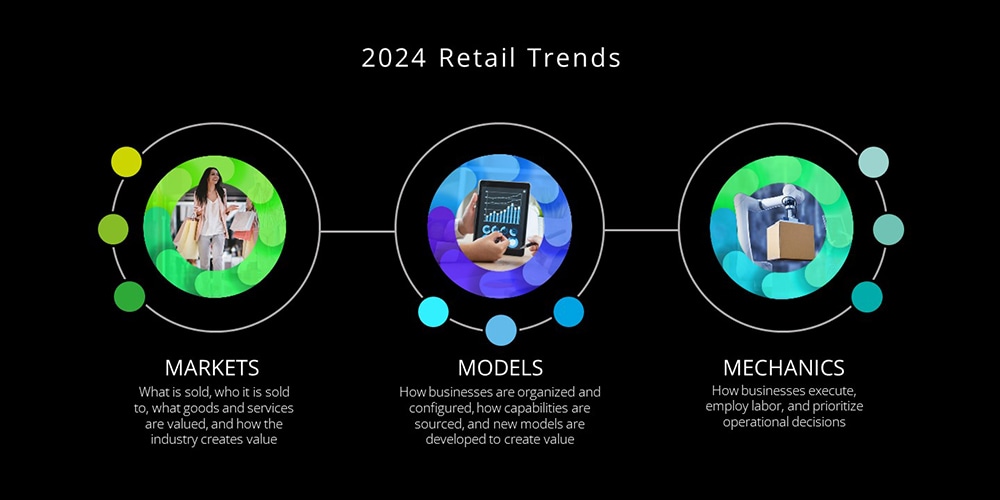

Det stadig endrende landskapet i detaljhandelen betyr at forhandlere står overfor økt kompleksitet i det kommende året. For å navigere gjennom denne kompleksiteten og agere på det som påvirker bransjen har vi i år valgt å definere trendene i tre kategorier: Markeder, modeller og mekanikk.

Les mer om hver enkelt kategori ved å trykke på lenken til høyre.

Spørsmål? Vi hører gjerne fra deg!