Article

MOF proposes tax reform that includes abolition of imputation system

Taiwan’s Ministry of Finance (MOF) announced a proposed tax reform package on 1 September 2017 that would overhaul the income tax system. The proposals include the following:

- Increase in the corporate income tax rate from 17% to 20%, accompanied by a reduction in the rate of the corporate surtax from 10% to 5%;

- Increase in the withholding tax on dividends from 20% to 21%;

- Abolition of the imputation system;

- Reduction of the highest tax bracket for individuals from 45% to 40%, as well as increases in deduction thresholds.

If approved, the measures are expected to apply for tax years beginning in 2018 (i.e. 1 January 2018).

Imputation system

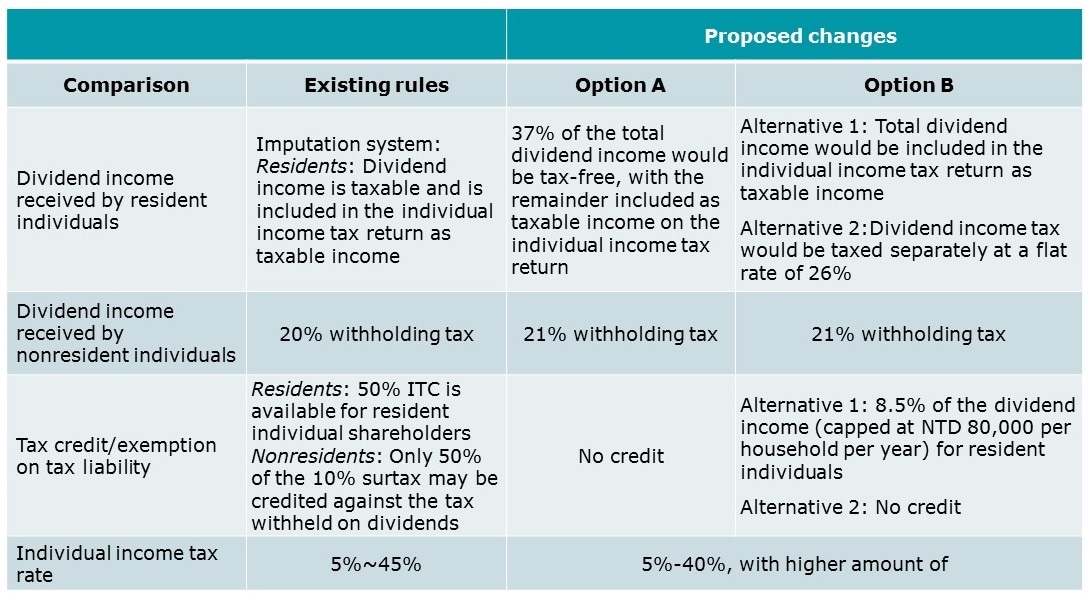

The imputation system has operated since 1998 to prevent the double taxation of corporate earnings. Under the imputation system, when a Taiwan company distributes after-tax profits as dividends to resident individual shareholders, the individual may use 50% of the corporate income tax paid by the company as a tax credit to offset his/her personal income tax liability. For Taiwan resident corporate shareholders, dividends received are not considered taxable income, but the imputed tax credit must be included in the balance of the recipient company’s shareholder imputation tax credit account (ICA) and imputed to the company for future dividend distributions (the ICA records the corporate income tax paid by the company, as well as the imputation tax credit). There is no mechanism for passing on the imputation tax credit to nonresident foreign individual or corporate shareholders, i.e. for foreign shareholders, tax is withheld at source on cash or share dividends distributed by a Taiwan resident company (currently, 20%, although the rate may be reduced under an applicable tax treaty).

In addition, a 10% surtax is imposed on a Taiwan company’s current year earnings to encourage the distribution of dividends and to narrow the gap between the corporate income tax rate (currently 17%) and the highest individual income tax rate (currently 45%). Resident individuals currently can credit 50% of the surtax against their personal income tax liability. However, nonresident shareholders may only use 50% of the 10% surtax paid by the company to offset the withholding tax (not the corporate income tax) levied on the dividends (subject to certain restrictions).

The imputation system has been subject to considerable criticism over the past two decades. The system is perceived to have increased the administrative burden on Taiwan companies, widened the differences between the tax burden on local and foreign investors, and given rise to controversies regarding the calculation of the ICA.

The MOF has proposed to eliminate the imputation system and replace it with one of two alternative systems. Under Option A, individual shareholders would enjoy a tax exemption on 37% of dividends they receive, with the remaining 63% taxed as personal income at the relevant rate. Option B includes two alternatives: (i) all dividend income would be taxed as personal income, but an exemption on the tax liability would be granted for 8.5% of the dividend income capped at NTD 80,000 annually; or (ii) all dividend income would be taxed at a flat rate of 26%.

A comparison of the existing rules and the proposals that would affect individual shareholders are follows:

For foreign companies doing business in Taiwan, the key changes would be the increase in the corporate income tax rate to 20% and the increase in the dividend withholding tax rate to 21%. Further, the ability of nonresidents to credit 50% of the 10% surtax paid by a Taiwan distributing company would be eliminated once the imputation system is abolished, for dividend distributions made on and after 1 January 2019 (a one-year transition period would apply for the ICA to be utilized for nonresidents).

The following table provides a high-level summary of the impact of the proposed changes for foreign companies with subsidiaries in Taiwan:

Comments

A one to two-month comment period will be open before the Executive Yuan finalizes the amendments to the relevant laws.

The proposal to abolish the imputation tax system follows extensive research and discussions, and aims to simplify the Taiwan income tax system, align the overall tax rates for local and foreign investors, and ease the tax burden on small and medium-sized local enterprises in Taiwan. However, the proposed changes will increase the overall income tax costs of doing business in Taiwan. In light of the potential changes, multinationals doing business in the country should seek tax advice to assess the implications and options available to mitigate the potential impact.