Latin America economic outlook, September 2024

Countries in the region are adjusting budget deficits and discussing pension-fund reforms for long-term economic stability. However, some nations still face substantial challenges that may impede economic growth.

Daniel Zaga

Daniel Gonzalez Sesmas

Nicolás Barone González

Federico Di Yenno

Juan Ignacio Lacapmesure

Latin American economies, as they stand post pandemic

Since the COVID-19 pandemic, most Latin American countries have maintained a path of sustained fiscal adjustment. Among them, several groups can be identified: ones that have reached and maintained low budget deficits (such as Nicaragua or Honduras); ones that achieved fiscal deficit stability and returned to pre-pandemic economic levels (such as Chile or Guatemala); and ones that still need major economic and systemic reforms to achieve a healthy fiscal balance (such as Brazil or Argentina).

Economies that need appropriate adjustments expect lower levels of growth, a phenomenon that could affect the rest of the region. In this context, while the drop in interest rates offers opportunities, the threat of lower growth in China remains a concern for several Latin American economies dependent on trade with China. As far as fiscal balance is concerned, an emerging issue in multiple countries is the sustainability of pension funds and the need for reforms to ensure their long-term viability.

The Latin American economic landscape: Challenges and opportunities

Latin America is currently experiencing a challenging economic landscape, characterized by both external and internal hurdles. While the possibility of US interest-rate reductions offers hope for the region’s future, concerns arise from the slowdown in the Chinese economy, contributing to global uncertainty. Moreover, the region’s economies are grappling with significant structural challenges, such as budget deficits, pension systems in need of reform, and debt burdens: These internal obstacles, coupled with the necessity to reduce inflation and exchange-rate volatility, create a complex economic scenario for most of them.

Recent US economic factors—including unemployment and slow job growth—have fueled speculation that the Federal Reserve may need to act to prevent a deeper economic downturn. While inflation remains slightly above the Fed’s target, it’s moving in the right direction. But labor markets are showing signs of cooling, leading economists to revise forecasts, with many now expecting at least three rate cuts of 25 basis points each before the end of the year. For Latin America, a US rate cut could bring mixed consequences.

On the one hand, it could ease pressure on the region’s currencies and reduce the respective countries’ debt burden, potentially allowing these economies to lower their own interest rates and stimulate capital inflows through increased investment. On the other hand, the recurrence of interest-rate cuts could also signal a weakening of the US economy, negatively affecting global demand, including demand for Latin American exports.1

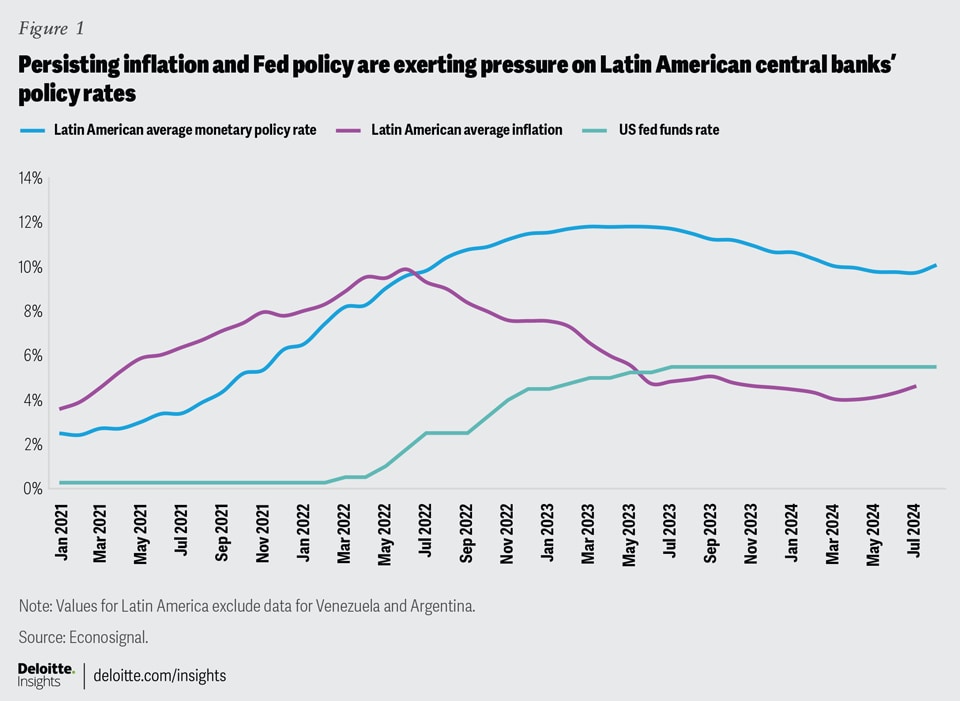

Most Latin American economies had been reducing interest rates following inflation declines. However, this trend has stalled in recent months. The narrowing interest-rate differential between these countries and the United States—coupled with exchange-rate volatility stemming from various economic turbulences in 2024 and preexisting domestic challenges—has led to a pause in further interest-rate reductions.

At the same time, inflation, while still stubbornly resistant to significant reduction, has been on the rise in some Latin American countries in recent months, increasing concerns about potential price instability and adding pressure on these countries’ central banks to reconsider their monetary policy stances (figure 1).

Meanwhile, China’s economic slowdown continues to pose a significant risk to Latin America, particularly for countries heavily reliant on exports to China (most South American countries). While China’s gross domestic product is projected to grow by 5% in 2024, this rate is expected to steadily decline in the coming years, reaching 3.6% by 2027. This deceleration could negatively affect Latin American economies dependent on Chinese demand for commodities,2 potentially reducing export revenues and hindering overall economic stability.

This escalating risk is evident in our report on risk assessments for Latin American countries, with commodity-dependent economies such as Chile, Ecuador, Peru, and Venezuela facing particularly challenging prospects. Furthermore, the potential for reduced Chinese investment in the region adds to economic uncertainty, potentially affecting infrastructure development and other crucial investments.

In addition to external pressures, Latin America faces its own set of deep-rooted structural challenges. Persistent budget deficits in some countries necessitate tough choices between spending cuts and potential tax increases. Unsustainable pension systems require reforms to ensure long-term viability. Moreover, high debt levels threaten fiscal stability and constrain policy options. These issues will be explored in greater depth later in this piece.

Fiscal adjustments to balance public finances

Fiscal outlook during and following the pandemic (2020 to 2023)

Latin America’s fiscal situation has undergone a complex evolution in the years following the pandemic. While significant progress has been made in consolidating public accounts, the region still faces major challenges that require urgent attention.

From March 2020 to December 2021, Latin American countries implemented expansive fiscal measures to mitigate the economic impact of isolation measures and quarantines, increasing average fiscal deficit in the region from 2.9% of GDP in 2019 to 6.3% of GDP in 2020 (excluding Brazil; for more details, please refer to the endnote here).3 This fiscal stimulus, which included increases in public spending and tax cuts, contributed to a strong expansion of the fiscal deficit. However, as the economies recovered and the health emergency began to be mitigated, the region’s governments initiated a process of fiscal adjustment, aiming to reduce deficits and stabilize public debt. As a result of these adjustments, the primary balances4 improved, thereby reducing the fiscal deficit of the region to 3.8% of GDP in 2022 (still higher than the 3.1% of GDP average seen from 2010 to 2019 in the region excluding Brazil). This means that governments were able to reduce their deficits in their current budgets, excluding debt service.

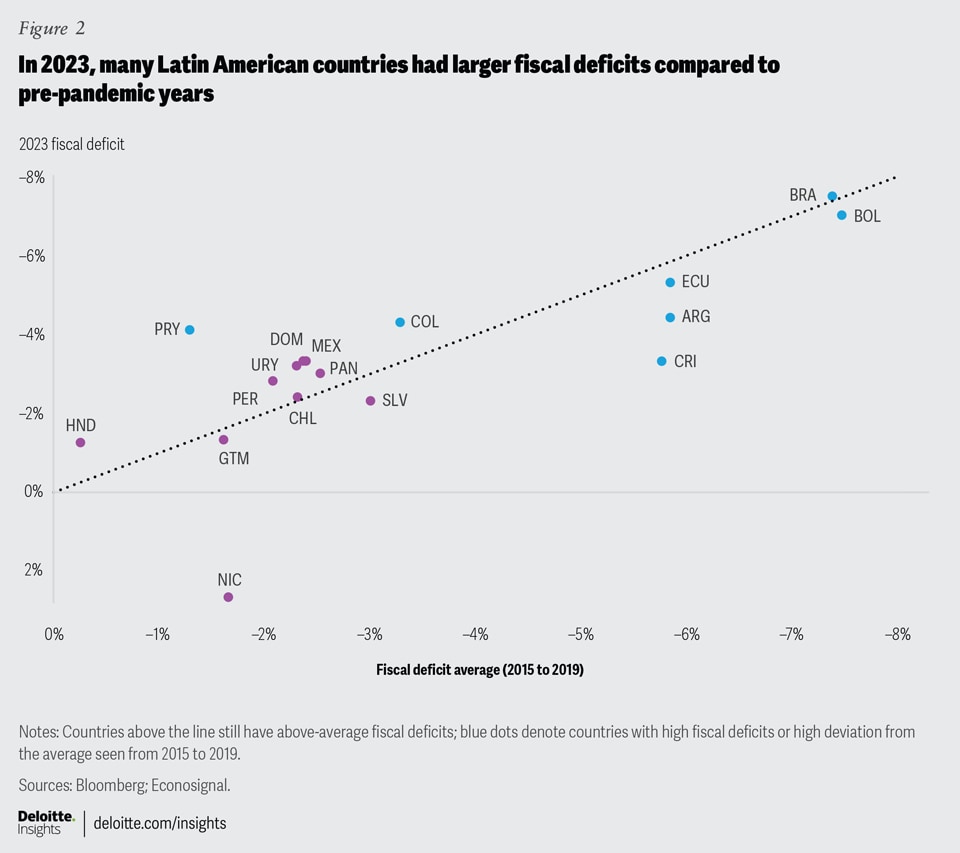

Despite the advances made, fiscal accounts in some countries experienced significant deterioration in 2023, reversing the trends observed in previous years (figure 2). The deficit of the region was the same as in 2022, that is, 3.8% of GDP (excluding Brazil).5 This situation is attributed to various adverse factors. First, the slowdown in economic activity and lower aggregate demand—which is driving the trend of continued low growth—have led to a loss of dynamism in tax revenues, ending two consecutive years of recovery in fiscal income. Notable declines include 3.3 percentage points of GDP reduction in revenues for Brazil and 2.6 percentage points for Chile and Ecuador. Second, primary public spending increased, interrupting a period of fiscal adjustments, with significant increases in Brazil, Colombia, Ecuador, Honduras, and El Salvador. Third, the tightening of global financial conditions, characterized by high local and international interest rates and lower capital flows to emerging markets, has increased debt-servicing and financing costs. Finally, the decline of 7% in overall commodity prices has negatively affected the revenues of commodity-exporting countries in Latin America.

If Brazil is accounted for, the average overall balance of the region deteriorated considerably—from 3.3% of GDP in 2022 to 5.1% of GDP in 2023—reflecting a substantial increase in debt service. Similarly, the average primary balance turned deficit again, from 0.5% of GDP in 2022 to 0.6% of GDP in 2023, indicating an imbalance between lower revenues and moderately higher public spending.

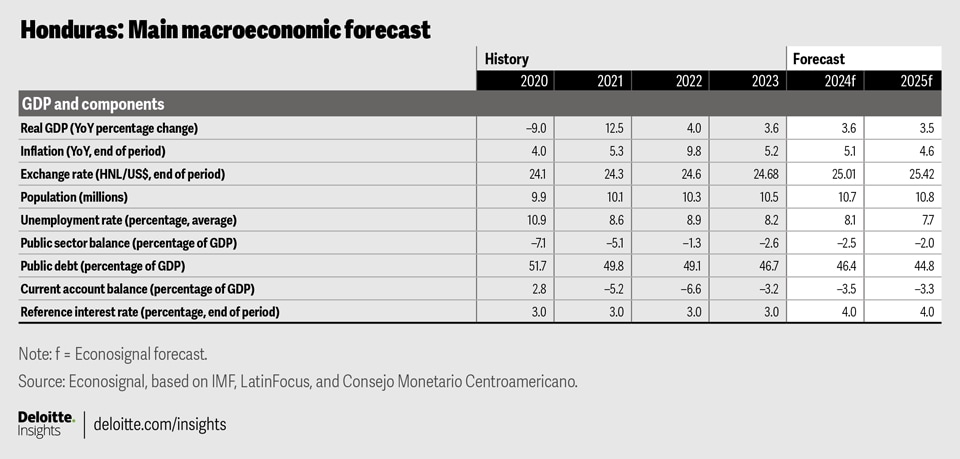

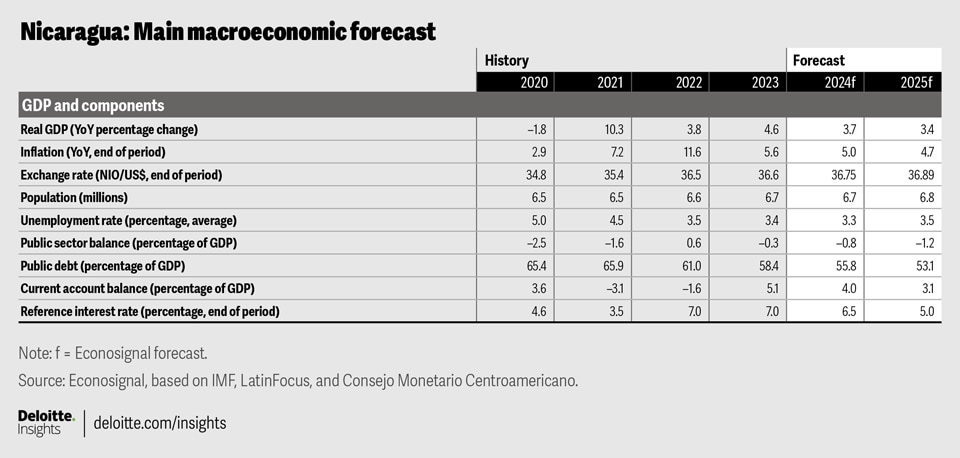

Among countries experiencing fiscal stability in recent years, Central American countries such as Guatemala, Honduras, and Nicaragua stand out. They have managed to return to sustainable levels of public accounts after the spending expansion and revenue reduction caused by the pandemic. Nicaragua, despite not having a fiscal rule, has achieved a general balance surplus for the second consecutive year and is likely to sustain this trend into 2025. With a fiscal rule, Honduras aimed to gradually reduce its deficit and return to a more sustainable level of 1% of GDP by 2023, which involved a gradual reduction of the deficit ceiling each year.

In 2022, countries like Mexico, Colombia, Peru, Ecuador, Uruguay, and Paraguay had managed to recover a fiscal balance similar to pre-pandemic levels. However, due to lower growth rates that reduced tax revenues and high international interest rates that increased the debt-interest burden, in 2023, their fiscal accounts experienced some deterioration, resulting in a fiscal deficit slightly above the levels seen from 2015 to 2019. In this group, the countries with the biggest deviations from previous deficits were Paraguay and Colombia.

Brazil, Argentina, and Bolivia are experiencing high fiscal deficits in recent years. Brazil, unlike Bolivia, for example, has a relatively moderate primary deficit, but the high interest burden drove its overall balance to 7.8% of GDP in 2023. On the other hand, 2023 was a year of significant economic challenges for Argentina. High inflation, fiscal deficits, and currency depreciation persisted, impacting growth and stability. These persistent fiscal deficits can lead to economic crises and increased unemployment in the long term, as has happened repeatedly throughout history. This is why, in 2024, these countries plan to reduce this burden, some with more success than others, not without consequences on their economic activity.

Ongoing fiscal adjustments on larger fiscal deficits (2024)

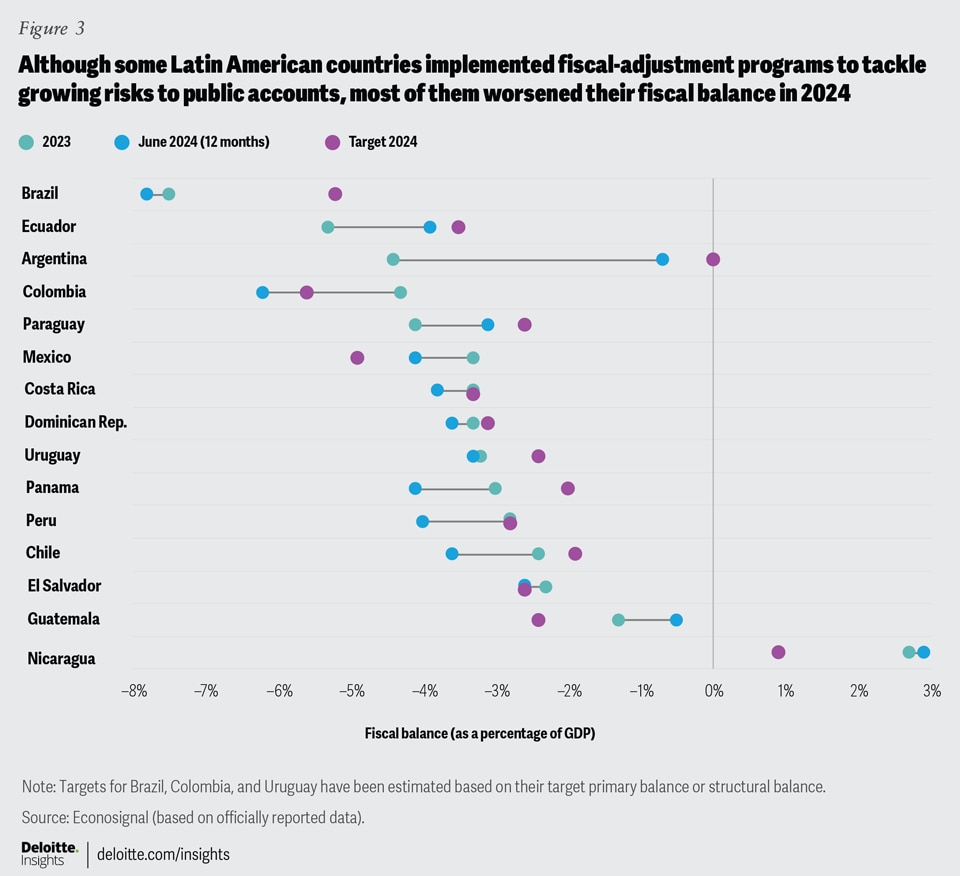

The deficit trend in Latin America has been toward further deterioration of fiscal accounts in the first half of 2024, continuing down the trajectory of 2023. Only five countries have managed to reduce their fiscal deficit. For most of the others, it has deteriorated further (figure 3).

Argentina has experienced an economic and social crisis in recent years, characterized by high inflation, currency devaluation, a decline in the real wages, and an increasing portion of the population living below the poverty line. However, starting in December 2023, after years of chronic fiscal deficit, the government led by Javier Milei began a stabilization program focused on achieving fiscal balance and zero monetary issuance. Thus, after ending 2023 with a deficit of 4.4% of GDP, in June 2024, the national public sector recorded six consecutive months of fiscal surplus for the first time since 2008, and the central bank of Argentina stopped assisting the treasury through monetary issuance.

In this way, the country accumulated a primary surplus equivalent to 1.1% of GDP in the first half of the year, exceeding the International Monetary Fund (IMF) program target of 0.7% of GDP. This result was achieved through a combination of cuts in budget items (public works, economic subsidies for energy and transportation, and transfers to provinces) and below-inflation increases in others (public sector wages and pensions).

Additionally, the increase in tax on purchases abroad in the first half of the year and the rise in income tax in the second half are contributing toward achieving budget balance. This strong fiscal adjustment, unprecedented in Argentina’s history, has been one of the main causes of the sharp decline in private consumption and domestic investment, which led to a 2.6% decrease in GDP in the first quarter of the year and an estimated 1.7% in the second quarter.

In 2022, Ecuador had managed to strongly stabilize and mitigate the fiscal deficit resulting from the pandemic, but in 2023, a series of factors hindered fiscal consolidation and increased risk in a dollarized economy where the order of public accounts is crucial for the country’s financial health. High international interest rates significantly increased the payment of Ecuadorian public debt, while the decline in oil prices and production, political instability, and the economic and security crisis forced the government to increase public spending, resulting in a sharp increase in the fiscal deficit in 2023 and delays in payments.

Ecuador has no formal fiscal rule in place, but the government has set itself the goal of reducing the deficit and growing revenue. And they are succeeding, demonstrating a commitment to fiscal discipline and financial sustainability even without a specific legal framework in place. The Noboa administration has implemented a reduction in its gasoline subsidy from the second quarter of this year and a series of tax reforms in 2024, such as the 3-percentage-point increase in value-added tax, which rose from 12% to 15% since April, and the reestablishment of tax on currency outflows at 5%, among others. Consequently, Ecuador’s tax revenue in the first half of 2024 grew by 7%, compared to the same period the previous year, which has helped ease the fiscal burden, generate resources to cover the country’s economic needs, and prevent an even greater fiscal crisis.

In Paraguay, the fiscal deficit increased to 4.1% of GDP in 2023, partly due to extraordinary payments related to the recognition of pending claims with construction companies and pharmaceutical suppliers accumulated during the pandemic. Thus, considering the growing risk to the sustainability of public accounts, the government decided to initiate a fiscal consolidation process with the aim of sharply reducing the deficit to 1.5% of GDP by 2026. In the first half of the year, it managed to improve the health of its public accounts thanks to lower capital expenditures. Additional revenues from the Itaipú hydroelectric plant, solid economic activity growth, and the elimination of the extraordinary expenses of 2023 strengthened revenue collection and facilitated consolidation without a significant effect on the real economy. However, beyond the favorable prospects for Paraguay’s fiscal sustainability, the reform of the fiscal fund and the public sector pension system represents one of the main challenges for the country’s public finances.

In the first half of the year, both Guatemala and Nicaragua improved their fiscal positions, compared to the strong results achieved in 2023. Although Guatemala maintained a low level of expenditure in the initial months due to the continuation of the 2023 budget, a supplementary budget representing approximately 1.7% of GDP was recently approved by its Congress. This supplementary budget, aimed at improving infrastructure and social development, does not pose a risk to the fiscal sustainability of the economy in the near term. Meanwhile, Nicaragua continues to demonstrate a strong fiscal position driven by substantial revenue increases from economic activity growth and tax reforms implemented between 2019 and 2022, coupled with strict expenditure control and lower costs of fuel subsidies.

Beyond these five cases of fiscal consolidation in the first half of 2024, the vast majority of countries in the region experienced a significant deterioration in public finances, in a context in which, although the cycle of interest-rate reductions has begun, domestic and external financing costs remain high.

In a move toward fiscal responsibility and sustainable growth, the Brazilian government introduced a new fiscal framework in 2023. This framework initially aimed for zero primary deficit in 2024 (which excludes interest payments, with a tolerance band of 0.25% of GDP, either plus or minus) and a primary surplus of 0.5% of GDP in 2025, gradually increasing to 1% by 2026.6 Additionally, a significant value-added tax reform has been approved, along with a series of new taxes that will be implemented from 2026 in a gradual process that will conclude in 2033, with the goal of streamlining the tax system and boosting economic efficiency in the long run. However, expenditure control and relatively high public debt have sparked ongoing discussions on fiscal sustainability.7 Most market participants expect that the deficit could largely exceed the target band of the year-end primary fiscal result (–0.25% of GDP to 0.25% of GDP) despite the freeze in government spending in June of 2024.8

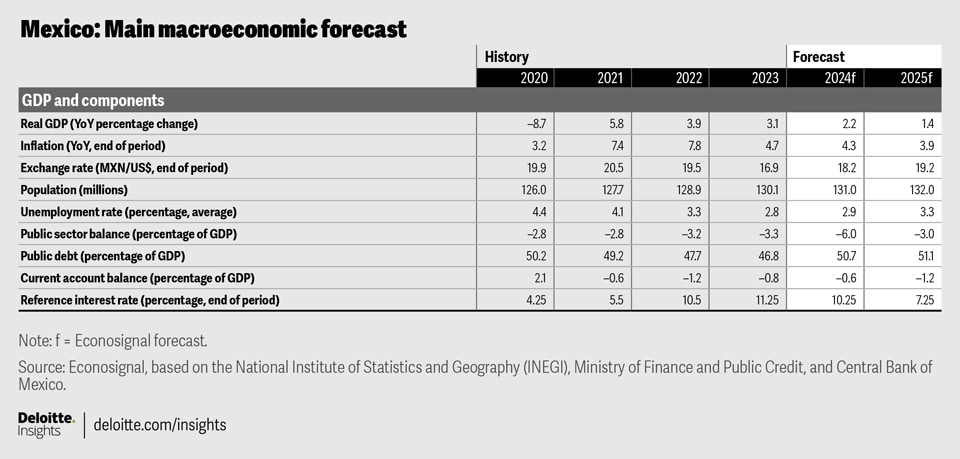

In Mexico, public spending grew significantly, by 12.2% in real annual terms, in the first half of the year due to elections—this surge was driven by higher expenditures on subsidies and transfers, social programs, and infrastructure projects. Consequently, between January and June 2024, public sector financial requirements amounted to 821.1 billion pesos, representing a growth of 51.2% compared to the same period in 2023.

Given the high fiscal deficit this year, the incoming administration led by Claudia Sheinbaum has decided to initiate a fiscal-consolidation process to achieve a maximum fiscal deficit of 3.5% of GDP by 2025. However, uncertainty remains as to whether this target can be reached without comprehensive fiscal reform, or if improvements in processes and digitalization for greater fiscal revenue collection, along with the completion of infrastructure projects, will suffice.

In Uruguay, within the framework of the Urgent Consideration Law, in 2020, the executive branch proposed a tool known as the fiscal rule, aimed at controlling the growth of public spending adjusted for the economic cycle and the fiscal sustainability of Uruguay, constituting a significant change for fiscal institutionalism. This rule is based on three pillars: a structural fiscal balance target, a cap on the growth of real primary expenditure, and net indebtedness. After four consecutive years of compliance since its implementation, its adherence is at risk in 2024 within the context of an election year.

Across Latin America, the interplay between fiscal deficits and public debt is a central theme in understanding the region’s economic challenges. As countries strive to balance fiscal discipline with economic growth, the impact of these efforts on public debt becomes increasingly evident. Effective management of fiscal deficits is crucial in preventing further debt accumulation and ensuring long-term economic stability. As we delve deeper into the issue of rising debt in the region, it becomes clear that comprehensive fiscal strategies are essential to address these challenges and promote sustainable economic growth.

Post–COVID-19 debt levels

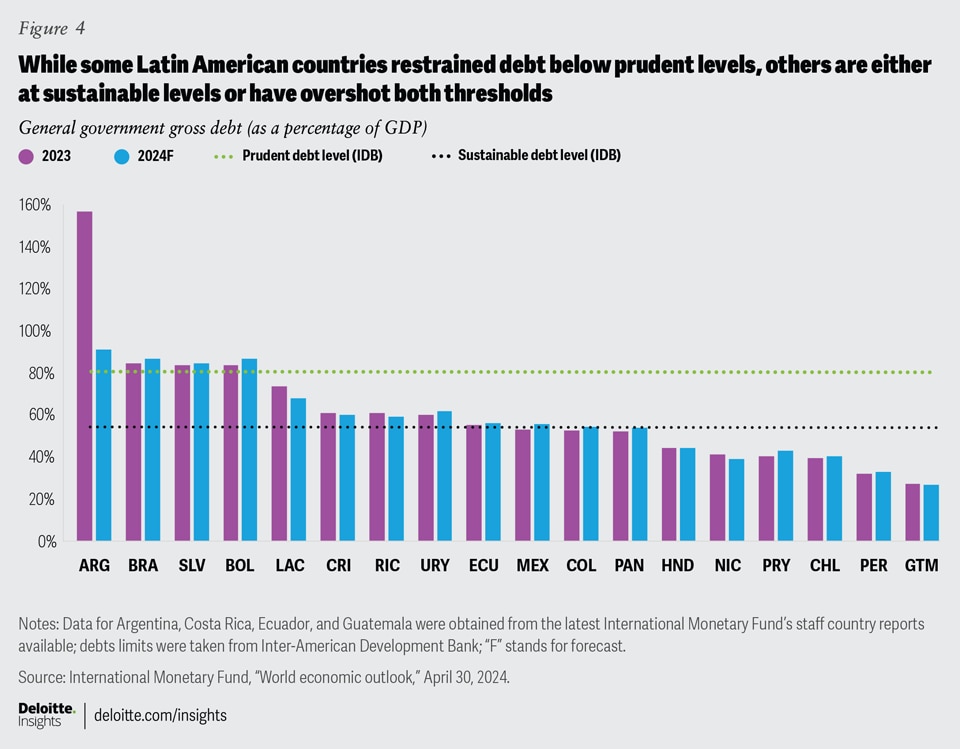

The increase in the public debt-to-GDP ratio recorded in 2020 reflected the great financing needs of Latin American economies to cope with the high costs of the pandemic. Since the peak of 76.1% of GDP seen in 2020, the trajectory of gross public debt in Latin America and the Caribbean has progressively improved, reaching 68% of GDP in 2022. However, in 2023, the downward trend had been interrupted, representing 73.7% of the region’s GDP.

This change in trajectory is primarily explained by the abrupt increase in the public debt-to-GDP ratio in Argentina: General government gross debt reached 156.7% of GDP at the end of 2023, driven by the valuation adjustment derived from a sharp increase in the exchange rate in December that affected the stock of dollar-denominated bonds and an inflationary adjustment, impacting average public debt in Latin America (figure 4).

In this sense, excluding Argentina, the average public debt of the region went from 65.9% of GDP in 2022 to 64.8% in 2023, continuing the post-pandemic downward trend.

According to the Inter-American Development Bank (IDB),9 there are varying levels of sustainable debt for different countries. Countries that are heavily reliant on commodities experience greater volatility in their economic activity and exports, thereby constraining their attempts to maintain lower levels of sustainable debt. Conversely, nations with a more diversified economic structure are better-positioned to manage a higher level of debt relative to their GDP.10 The IDB has established a maximum average sustainable debt level for Latin America and the Caribbean at 80.5% of GDP, while recommending maintaining a prudent debt level between 55% and 44% of GDP.11 Several countries in the region, such as Argentina, Bolivia, Brazil, and El Salvador, currently stand above this sustainable debt limit. There are almost no prospects of their debt burdens to be decreased enough to reverse this trend. This implies that these countries may have little fiscal space to maneuver and urgently need to implement further fiscal reforms to ensure long-term economic stability and growth. On the other hand, the robust performance of countries such as Guatemala, Peru, Chile, Paraguay, Nicaragua, and Honduras—which have managed to sustain public debt well below prudent levels, thanks to solid and sustained fiscal policies over time—stands out.

It is imperative for countries with high public debt to promote fiscal consolidation to prevent public debt from becoming a drag on economic growth. According to the IDB, elevated levels of public debt can limit access to financial markets, redirect public expenditure toward less productive sectors, increase domestic interest rates, and curtail private investment, all of which could collectively decelerate economic growth. Specifically, according to IDB studies, “debt peaks” can have a considerable negative impact: Each year following a debt peak results in an additional decline in economic growth by 1.5 percentage points.12

As we turn our focus to the pension systems in Latin America, the dilemma around fiscal deficits becomes even more pronounced. Pension systems’ financial sustainability is intrinsically linked to the broader fiscal health of a country. Elevated public debt and persistent fiscal deficits can undermine the ability to fund pension obligations, leading to potential shortfalls and increased pressure on public finances. Addressing the deficits in pension systems thus requires a holistic approach that considers the overall fiscal strategy, aiming to ensure long-term economic stability and social security for the aging population.

Latin American pension systems

The ongoing demographic shift toward an aging population in Latin America poses significant challenges to the fiscal sustainability of social protection systems. The increasing demand for health care, pensions, and care services will strain public finances. Additionally, high levels of informal employment not only limit access to quality jobs and social protection but also reduce tax revenues, further exacerbating fiscal pressures.

According to the Economic Commission for Latin America and the Caribbean,13 pension systems have low coverage, with less than half of the working-age population contributing, underscoring the difficulty in ensuring adequate retirement incomes for a growing elderly population. This demographic transition, coupled with the informality of the labor market, necessitates comprehensive reforms to ensure the long-term viability of social protection systems and promote inclusive economic growth.

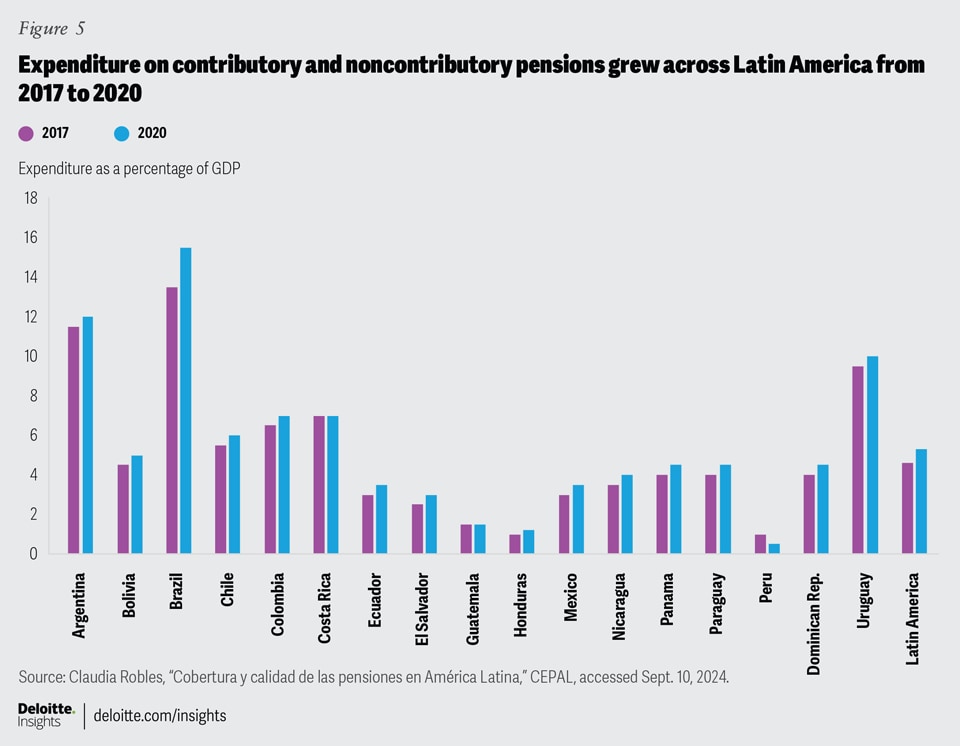

Furthermore, the rapid aging of Latin American and Caribbean populations is driving the expansion of noncontributory pension systems, placing additional pressures on fiscal budgets (figure 5).14 The number of people 65 years and older has increased dramatically, from 5% of the total population in 1990 to almost 9.8% in 2023, and this trend is expected to continue. For example, Latin America and the Caribbean will age to the same levels as Europe but in half the time, increasing the pressure on preexisting pension systems.

In 2023, while the population that is 65 years and older as a percentage of the total population in Latin America reached 9.8%, in Europe, it was 20.4%. By 2053, the number for Latin America is projected to reach 20.6%, while in Europe, it will be almost 30%. In 30 years, Latin American populations will age faster compared to Europe in the past. An estimated average pension expenditure of 5.3% of GDP in 2020 is expected to rise to 6.3% of GDP in 2030 and 8.4% by around 2064. The demographic effect is estimated to increase pension spending by an average of 60%. This will occur along with new challenges related to the demographic transition, such as people in situations of dependency and with the need for long-term care.

According to the Economic Commission for Latin America and the Caribbean, the countries experiencing the highest pressure from pension systems include Argentina, with a pressure of 11% of GDP, followed by Brazil and Uruguay. Costa Rica follows with 7.3% of GDP. These countries, characterized by high levels of expenditures and extensive coverage of individuals within their pension systems, are expected to experience a faster aging of their populations, making the situation riskier in terms of fiscal impacts.

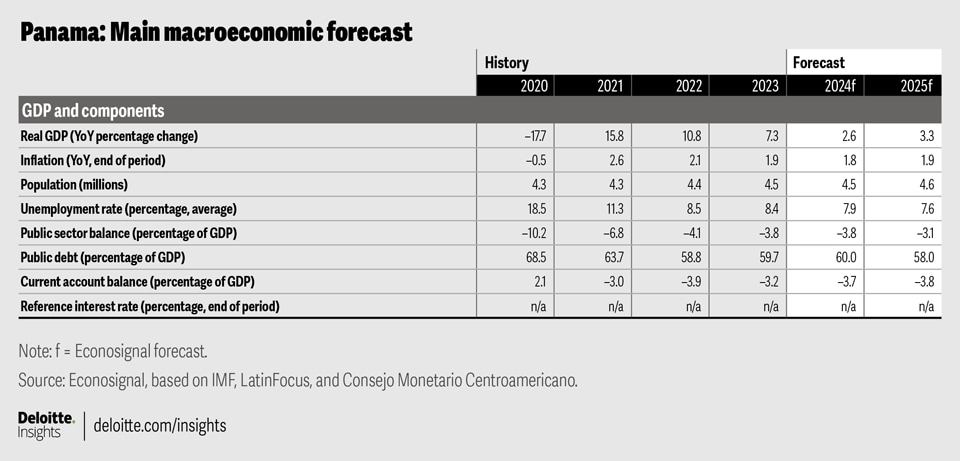

Next, there is a middle group comprising Colombia, Ecuador, and Bolivia, with pension expenditures around 4% of GDP and a mixed aging population. Finally, Mexico, Chile, Panama, and El Salvador, with expenditures at approximately 3% of GDP, face less risk due to lower GDP and moderate population growth, except for Chile, which is experiencing a high rate of aging. The rest of the region can be considered to have low risk, taking into account the lower impact of pension systems and their slower aging processes. In response to mounting pressures on pension systems due to aging populations and the expansion of noncontributory benefits, several countries are actively debating or undergoing pension reforms: Colombia, Peru, Paraguay, and Uruguay are leading examples.

The proposed changes to Colombia’s pension system may increase pressures on the system as opposed to reducing them. The introduction of a split system in the contributory pillar, where contributions up to 2.3 times the minimum wage go to the public system and the rest to private funds, aims to create a more equitable structure. However, this may create additional pressure on fiscal accounts in the long term. Additionally, a solidarity pillar provides noncontributory assistance for vulnerable elderly individuals, while a semi-contributory pillar combines savings with state subsidies for those in informal employment. This aims to increase equality in the system by increasing coverage and reducing poverty among the elderly, but also increases state subsidies, thereby jeopardizing the sustainability of public finances.

In Peru, a pension reform is under debate in Congress, currently. It proposes a multi-pillar system with noncontributory, semi-contributory, contributory, and voluntary components. The most controversial aspect is the introduction of a consumption-based pension, allowing everyone, regardless of affiliation with pension fund administrators or Pension Standardization Office administrators, to voluntarily contribute 1% of their purchases toward their pension. Additionally, the reform suggests raising the minimum pension from 500 to 600 soles.

Championed by President Lacalle Pou, Uruguay’s new pension reform took effect in 2023: This increased the retirement age to 65 and allowed retirees to continue working, aiming to modernize and ensure the system’s financial sustainability. However, it faces opposition from the left-wing coalition and trade unions who criticize it for reducing benefits and forcing people to work longer. They are pushing for a public consultation in the next presidential elections to potentially enshrine in the constitution a minimum retirement age of 60, align the minimum pension with the minimum wage, eliminate private pension-fund administrators, and establish pension adjustments based on public sector wage variations.

The cost of this initiative could increase pension spending by 2% of GDP by 2030 and 6% by 2050: The increased expense would also increase fiscal pressure, which is already high in Uruguay, given that currently half of pension spending is financed by taxes and the union initiative does not foresee changes in contribution rates.

In Paraguay, according to the World Bank,15 the pension system is characterized by low coverage, excessive fragmentation, and various institutional problems. These include actuarial deficits, regulatory deficiencies, a lack of standardized investment rules, and inequities, mainly within the Caja Fiscal (which manages the system for public sector employees). The overall system still has a low number of contributors, reaching only 23.4% by 2022.

On the other hand, the noncontributory system has allowed a significant part of the population to access a pension, but this is still low, reaching 14.8% of the population over 65 years old. In terms of budgetary impact, the main problem arises when considering the deficit of the Caja Fiscal. There are estimates that the growing deficit of this fund would reach 1.16% of GDP by 2030 and 2.4% by 2050, which implies that certain modifications may need to be made.

As we turn our focus to the pension systems in the region, the dilemma of fiscal deficits becomes even more pronounced. Pension spending is on the rise due to increasing pressure from low coverage, insufficient benefits, and accelerated aging. Aging will generate fiscal pressure and significant challenges for social security. The number of elderly people and their life expectancy are increasing. An estimated average pension expenditure of 5.3% of GDP in 2020 is expected to rise to 8.4% by around 2064. The demographic effect is estimated to increase pension spending by an average of 60%. The financial sustainability of pension systems is intrinsically linked to the broader fiscal health of a country. Elevated public debt and persistent fiscal deficits can undermine the ability to fund pension obligations, leading to potential shortfalls and increased pressure on public finances. Addressing the deficits in pension systems thus requires a holistic approach that considers the overall fiscal strategy, aiming to ensure long-term economic stability and social security for the aging population.

Looking ahead: The continuing challenges of an aging population and fiscal deficits

Most Latin American countries have demonstrated success in reducing fiscal deficits and sustaining the viability of public accounts. For example, Uruguay and Chile have 90% and 85% of their population above 65 years old covered by contributory or noncontributory pension systems, while poverty remains below 3% in this sector.16 At the same time, they have maintained low levels of fiscal deficit and debt while preserving good macroeconomic variables, low country risk, and high growth in recent years. These variables are further detailed in our risk assessments for Latin American countries. However, a significant challenge for Latin America is the constrained fiscal space within its primary economies, coupled with the repercussions that budgetary adjustments may induce.

For example, in Brazil and Argentina, 93% and 85% of their population above 65 years old are covered by contributory or noncontributory pension systems, while poverty remains below 7% and 3%, respectively. The problem arises from their high fiscal deficit, which now puts the countries’ macroeconomic stability at risk. The same problem is seen in smaller economies like Bolivia. In addition to issues related to fiscal deficits, these nations grapple with elevated levels of debt, necessitating a thorough consideration of potential ramifications, as evidenced in historical precedents. While interest-rate reductions in major economies may facilitate the management of substantial existing debts, the deceleration in China’s economic growth poses a threat to export performance and overall economic growth in these countries.

In contrast, several countries like Nicaragua or Guatemala have achieved significant outcomes in maintaining debt sustainability and moderate fiscal deficits but still need improvements in the coverage of pension systems and poverty mitigation among populations 65 years or older. This fiscal prudence has contributed to the substantial growth experienced in recent years and supports optimistic future projections—countries can make further improvements using this framework. Countries that have maintained fiscal sustainability through rational calculation and strategic planning of their budgets are able to create a stable investment environment, uphold high credit quality, and consequently achieve a better quality of life for all inhabitants.

The aging population in Latin America brings to the forefront critical issues such as pension regime reforms, which are beginning to generate extensive debate. The central concern is to implement these reforms without adversely affecting macroeconomic variables, thereby preserving the fiscal sustainability that has been meticulously safeguarded in recent years. This sustainability has been instrumental in enabling and continuing to facilitate substantial economic growth in many of these countries.

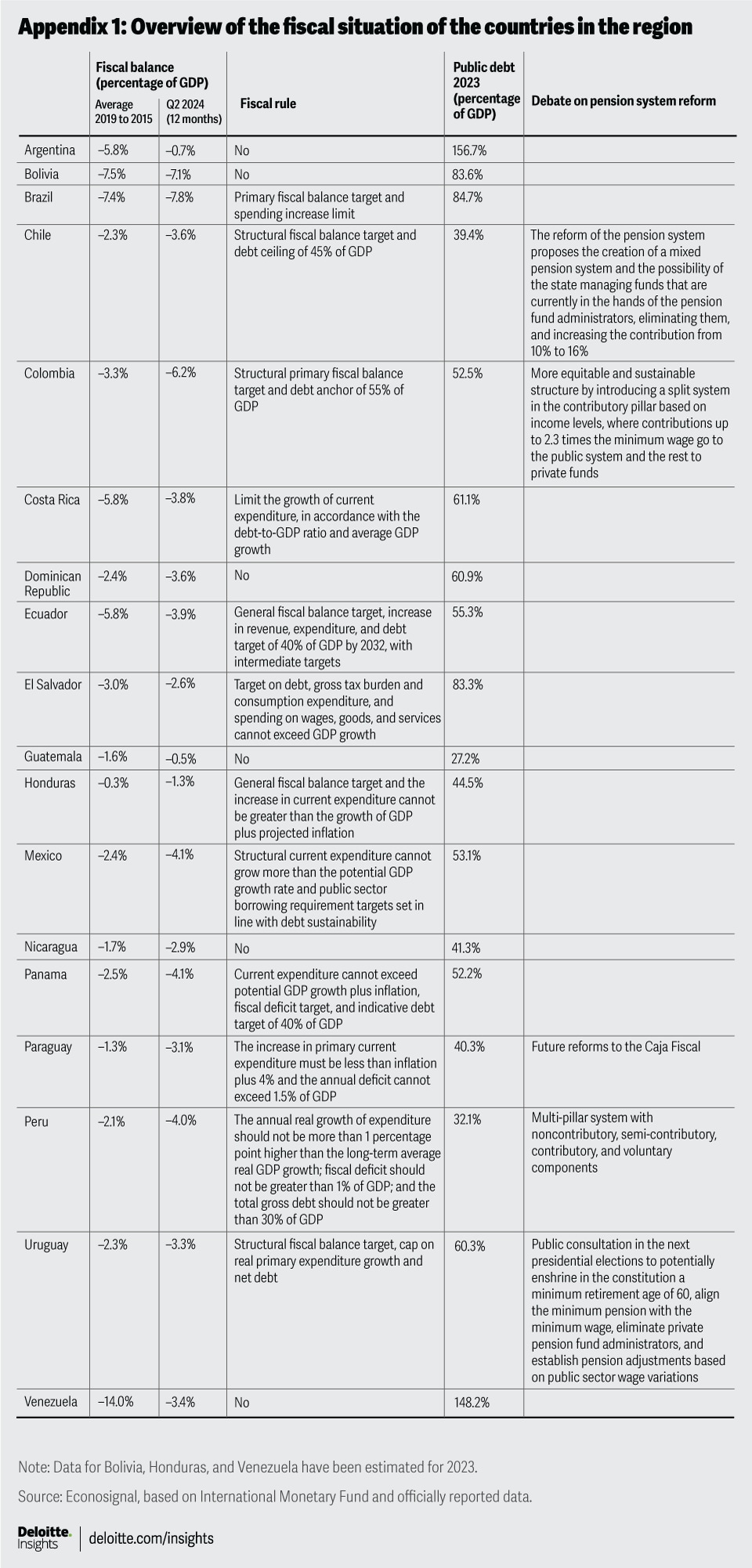

Appendix 1: Overview of the fiscal situation of the countries in the region

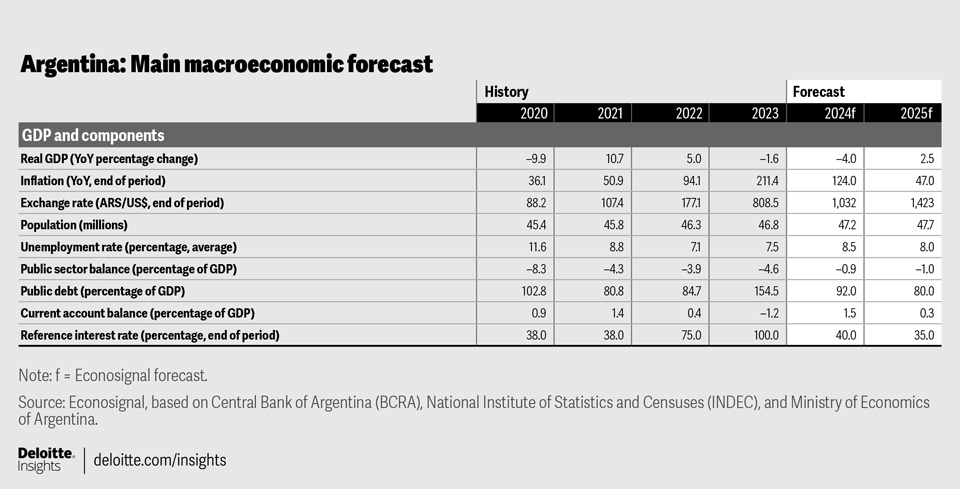

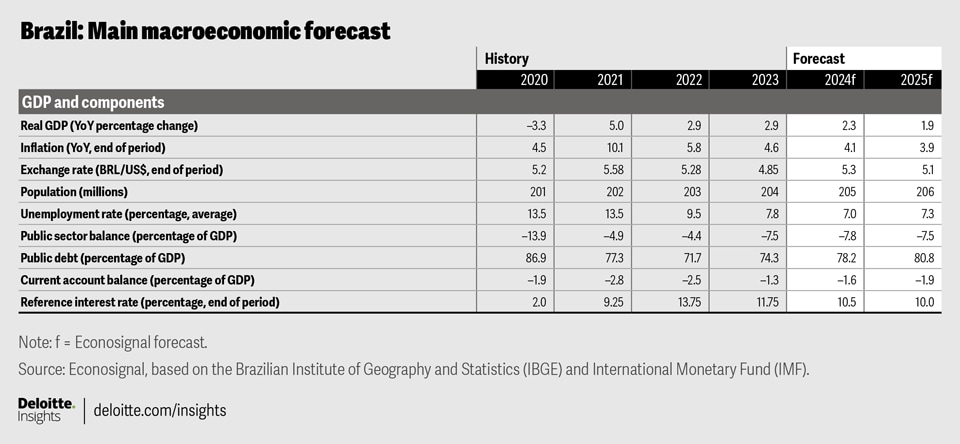

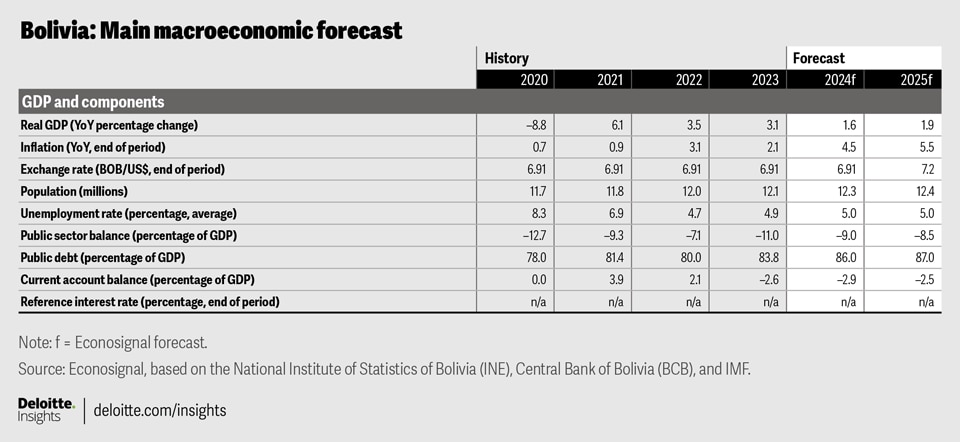

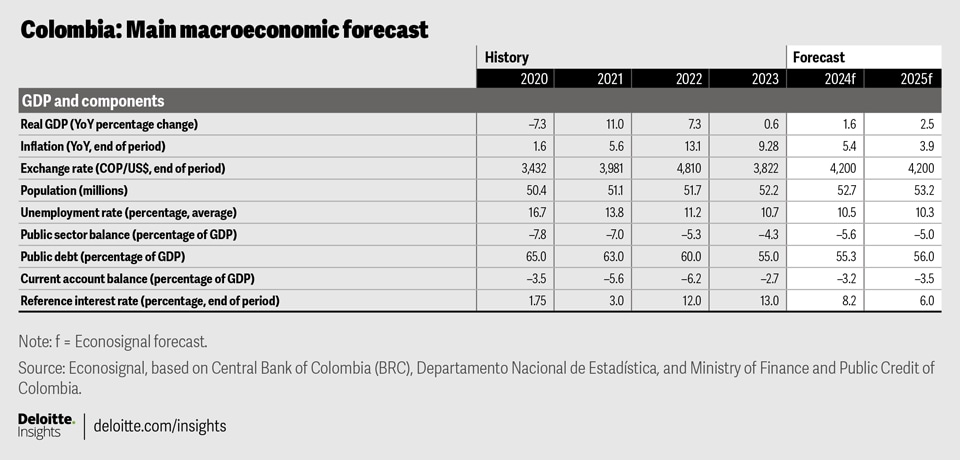

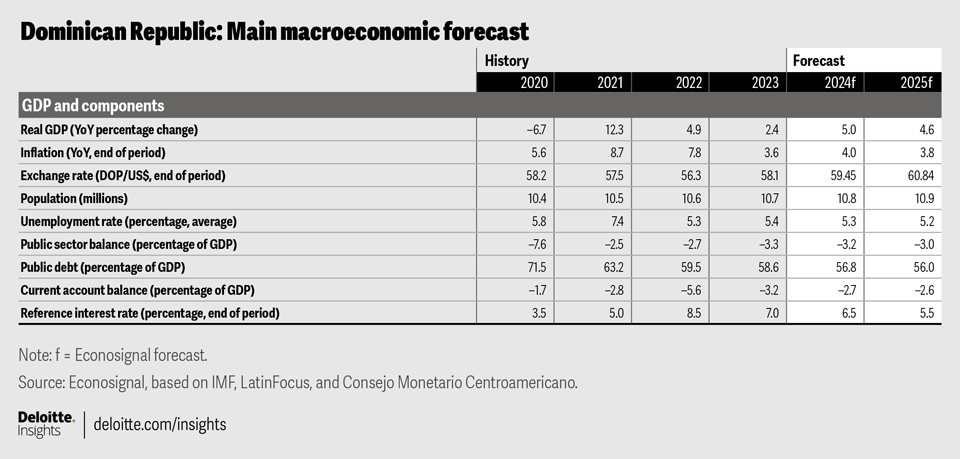

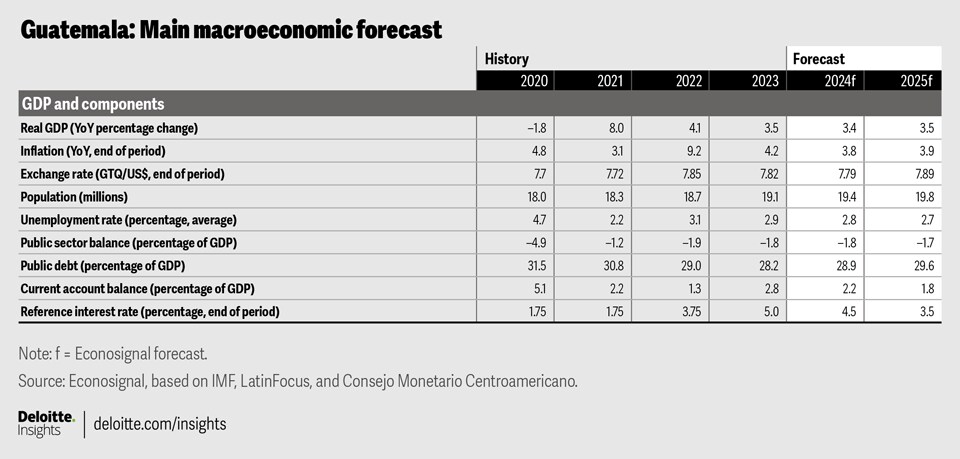

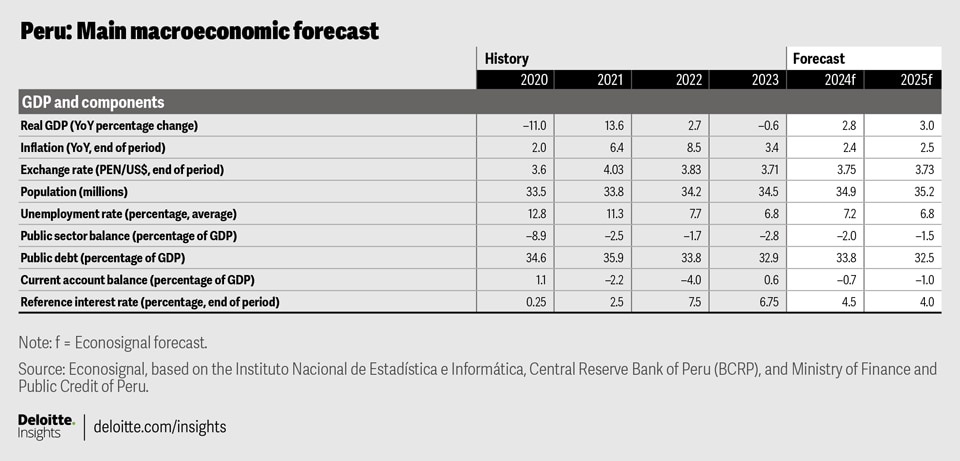

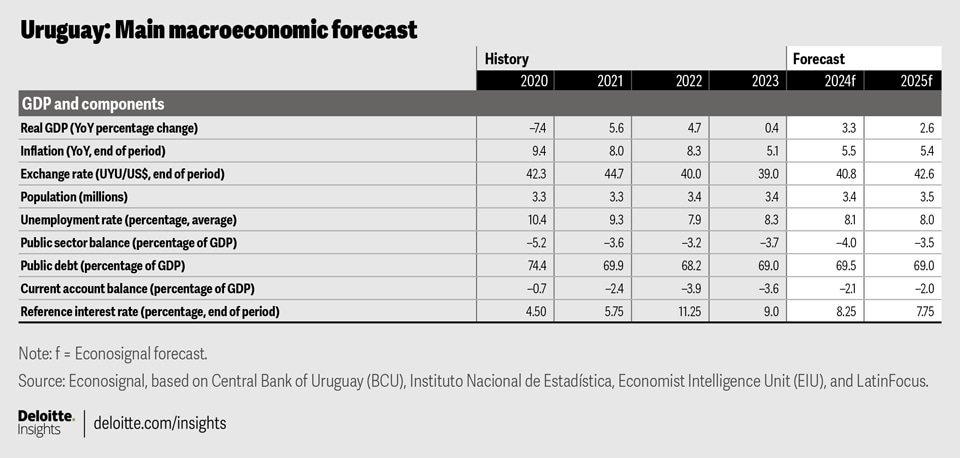

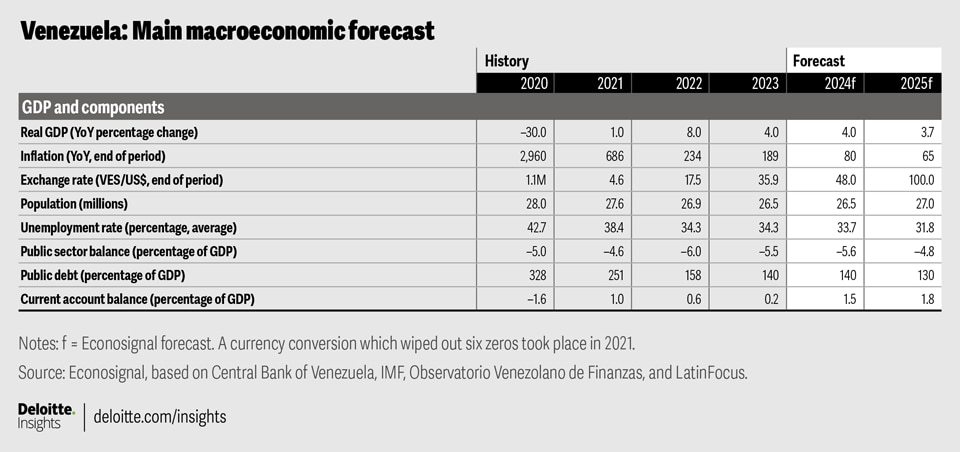

Appendix 2: Country forecasts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}