Brazil economic outlook, March 2025

The Brazilian economy was strong through 2024, with robust domestic demand driving growth. But looming challenges like persistent inflation and a weak real can hinder its momentum in 2025.

The Brazilian economy continued to outperform expectations in 2024: Real gross domestic product grew by 3.4% for the year, largely thanks to very strong domestic demand.1 Consumer spending and capital formation accelerated throughout much of the year, which more than made up for the slowdown in government spending and exports.

Despite the strong performance last year, the economy is now facing serious headwinds that are likely to create a substantial drag on GDP. Weak government finances are contributing to stronger inflation and higher interest rates, which challenge growth. There are already nascent signs of this occurring. Additional monetary tightening may be required to loosen the labor market and bring wage growth back down. On the upside, export growth is likely to improve this year, which will help cushion the anticipated slowdown of domestic demand.

Central bank intervention

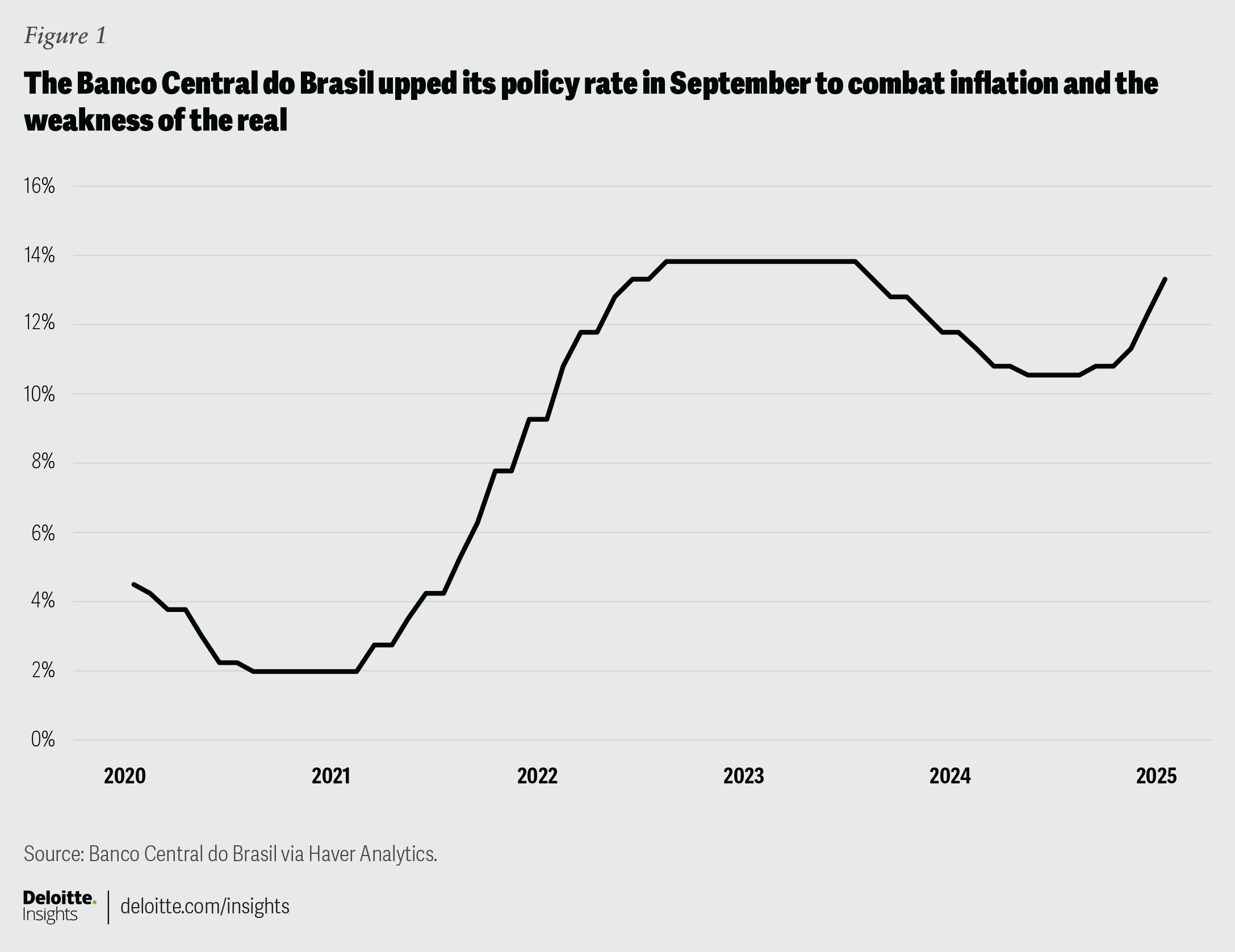

A combination of looser monetary and fiscal policy contributed to a stark depreciation of the real last year. The Banco Central do Brasil (BCB) cut rates through May 2024, while the Federal Reserve left its rates unchanged. This divergence in policy naturally led to some modest weakening of the real compared to the US dollar. However, in August, the real had depreciated by more than 12% from a year earlier, and headline inflation was nearing the top of the BCB’s target range.2 This prompted the central bank to raise rates by 25 basis points at its September meeting (figure 1).

By October, headline inflation accelerated to 4.8% on a year-ago basis, which is firmly above the inflation target’s upper bound of 4.5%.3 The BCB raised rates by another 50 basis points in November. Around the same time, the finance minister announced a fiscal plan that included spending cuts to appease financial markets. Persistent government deficits had caused many investors to worry about the sustainability of government debt, which was adding to the weakness of the real. However, politicians diluted the fiscal plan.4 This less fiscally prudent policy led to a selloff of the real, which lost nearly 25% of its value by December on a year-ago basis.

The selloff caused the BCB to intervene in foreign exchange markets to provide support to the exchange rate.5 The BCB then raised rates more aggressively in December, this time by 100 basis points. It raised rates by another 100 basis points at its January meeting. Central bank intervention seems to have worked: The real steadily appreciated from 6.19 per dollar on Dec. 31, 2024, to 5.78 per dollar on Feb. 13, 2025.

Although the BCB stabilized the currency, government finances will likely remain a key challenge for the foreseeable future. On the surface, government finances have evolved, as planned, in the fiscal framework. The central government posted a primary deficit of just 0.1% of GDP in 2024, which was within the targeted range of plus or minus 0.25% of GDP.6 If that target had been missed, it would have forced the government to lower spending this year, as stipulated in the fiscal framework.

The problem is that the government was only able to hit its target due to one-off factors. For example, expenditures related to natural disasters like flooding and forest fires were excluded from the calculations.7 In addition, revenue was unusually high in 2024, thanks to strong economic growth and enhanced tax collection measures. Those drivers of revenue growth are unlikely to be repeated this year, as GDP growth is expected to slow while improved tax collections have little upside left.

Had those accommodations not been made, the primary deficit would have been much larger: Although it may make sense to exclude spending on natural disasters when calculating whether policymakers have adhered to the fiscal framework, those expenditures were still real payments that the government made. This means the central government continued to run a primary deficit last year, which is expected to be larger this year than it was in 2024. This suggests that the debt-to-GDP ratio will continue to rise, which could further spook financial markets and force additional central bank intervention.

Consumer strength fading

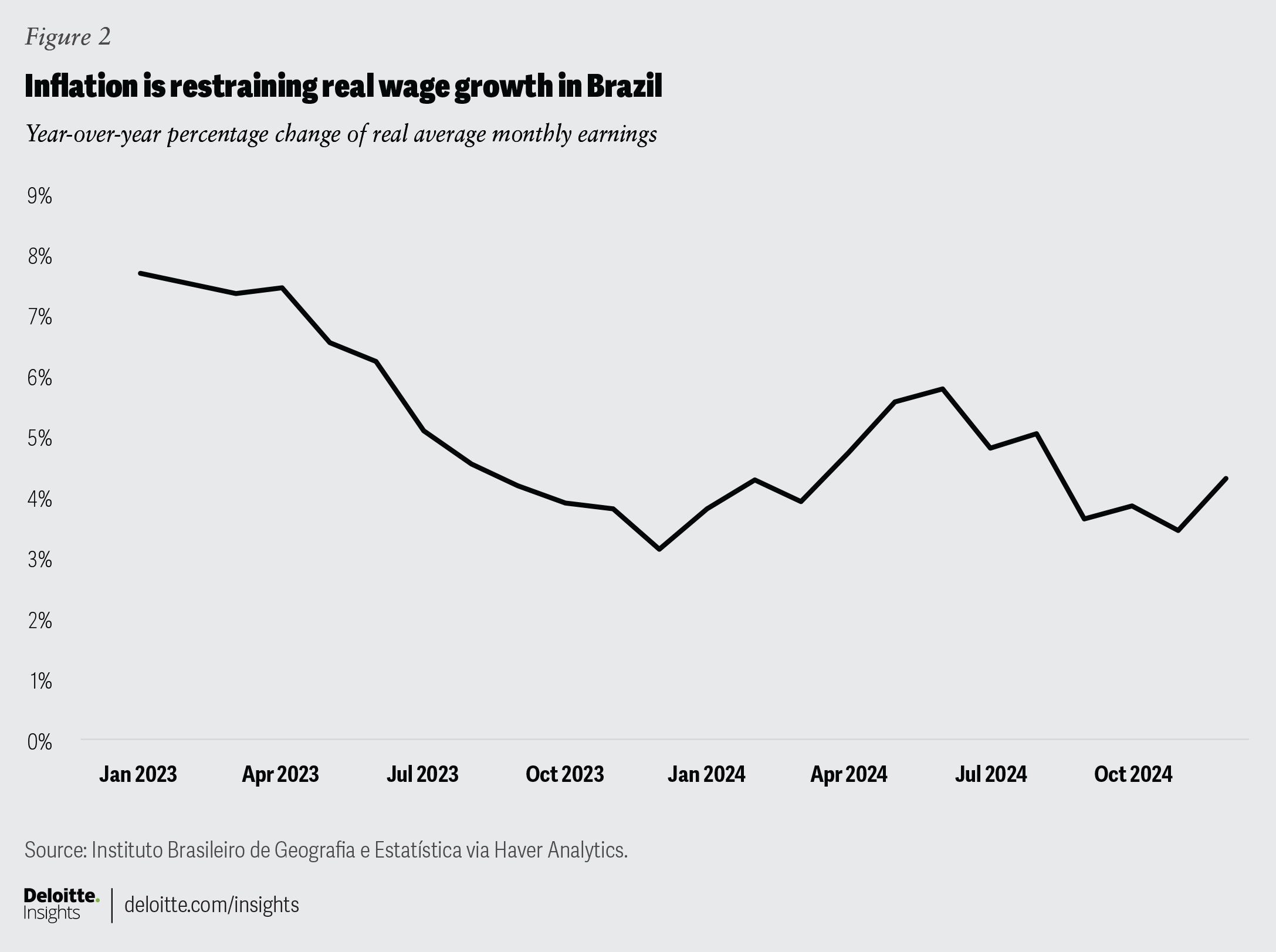

A tight labor market has allowed consumer spending to support economic growth. Although the unemployment rate ticked up to 6.5% in December 2024, it had never been below 6.7% since data began in 2012.8 Employment growth remains strong, rising 2.8% from a year earlier in December. Such tightness in the labor market has contributed to strong wage growth. Despite elevated inflation, real monthly earnings were still up 4.2% from a year earlier in December.9

Rapid employment and wage growth would normally portend ongoing strength in consumer spending. However, rising inflation is expected to weaken spending this year. As inflation accelerated in the second half of last year, real wage growth moderated by about 1.5 percentage points (figure 2). This suggests that real consumer spending this year will likely be weaker than it was last year.

The rise in inflation has caused a rise in interest rates that further threatens consumer spending. Indeed, the volume of retail sales already slowed dramatically in the last two months of 2024.10 Real retail sales were up just 1.6% from a year earlier in December—a clear deceleration from the 6.1% growth seen in October. The spending slowdown was most apparent for motor vehicles and construction materials, both of which are likely more susceptible to changes in interest rates. The number of vehicle registrations has fallen for three consecutive months.11

The slowdown in consumer spending is not limited to durable goods, however. Spending on nondurables such as pharmaceuticals and personal care products has also waned.12 The weakening of the real and the higher interest rates that accompanied it coincided with a plunge in consumer confidence. One measure of consumer confidence fell to its lowest level since August 2022 in February.13

Trade may bring opportunities

The external sector weighed on GDP growth last year. Goods exports fell 0.8% in 2024, compared to the previous year.14 Most of the weakness was due to an 11% decline in agricultural exports. Mining and manufacturing exports were both up a little more than 2.5% over the same period.15

Although export growth continued to weaken in January, there are several reasons to expect it will turn around this year. The first reason is that Brazil is likely to avoid trade barriers erected in the United States. The United States has threatened tariffs on more countries this year but is primarily focused on countries with which it runs a deficit. Fortunately, it runs a surplus with Brazil, which will likely prevent the United States from erecting such barriers against Brazil, at least in the near term. Assuming such an outcome, Brazilian exports may become more favorable to US importers, as the cost of importing goods from other countries becomes more expensive. A weaker currency will also help on the cost front.

The second reason to be optimistic about Brazil’s exports this year is due to the macroeconomic stability now seen in Argentina. The exchange rate between the two countries finally stabilized in 2024.16 This helped push exports to Argentina up 57.9% from a year earlier in January.17 Exports to Argentina were worth just US$13.8 billion in 2024, but with such fast growth rates, it could quickly become a key driver of export growth for Brazil.

The third reason to be optimistic about international trade is that a trade deal between the European Union and several Latin American countries, including Brazil, is moving forward.18 Assuming the deal is ratified, it will lower trade barriers for Brazilian exports to the sizable EU market. Indeed, Brazilian goods worth just shy of US$50 billion were exported to the European Union in 2023.19

A boost in exports is unlikely to be enough to offset the expected slowdown of domestic demand. The rapid rise in interest rates has already slowed the pace of consumer spending and dented consumer confidence. Additional rate hikes are not off the table despite stabilization in the foreign exchange market. Inflation continues to run above the BCB’s target range, which raises the probability of additional rate hikes and slower domestic demand. Overall, Brazil’s economy is expected to post positive growth this year, but it will be at a considerably slower rate.

{kind=link}

{kind=link}