Argentina economic outlook, November 2024

Argentina aims for economic stability through budget reforms, monetary supply control, and debt management: Despite signs of recovery, rainfall deficits and access to international credit remain critical hurdles

Fiscal adjustment framework: Achieving zero deficit

In recent years, Argentina has faced an economic and social crisis marked by high inflation, currency devaluation, declining real wages, and an increasing proportion of the population living below the poverty line. Beginning in December 2023, the administration under President Javier Milei initiated a stabilization program aimed at achieving fiscal balance and eliminating monetary issuance. As a result, after concluding 2023 with a fiscal deficit of 4.4% of gross domestic product, the national public sector recorded nine consecutive months of fiscal surplus—the first such occurrence since 2008.

This achievement was facilitated by a combination of reductions in budgetary allocations (for things including public works, economic subsidies for energy and transportation, and transfers to provinces) and below-inflation increases in other areas (such as public sector wages and pensions). Reducing government expenses was not easy, but the current administration pushed them through Congress.1 However, the social and political possibility of maintaining this anchor remains uncertain.2

Additionally, the temporary increase in the tax on foreign purchases (PAIS tax) in the first half of 2024 and the rise in income tax in the second half contributed to the achievement of budgetary balance. This rigorous fiscal adjustment along with a monetary contraction—unprecedented in Argentina’s history—has been a primary factor in the substantial decline in private consumption and domestic investment, resulting in a 2.6% decrease in GDP in the first quarter of the year, and a 1.7% decrease in the second quarter.

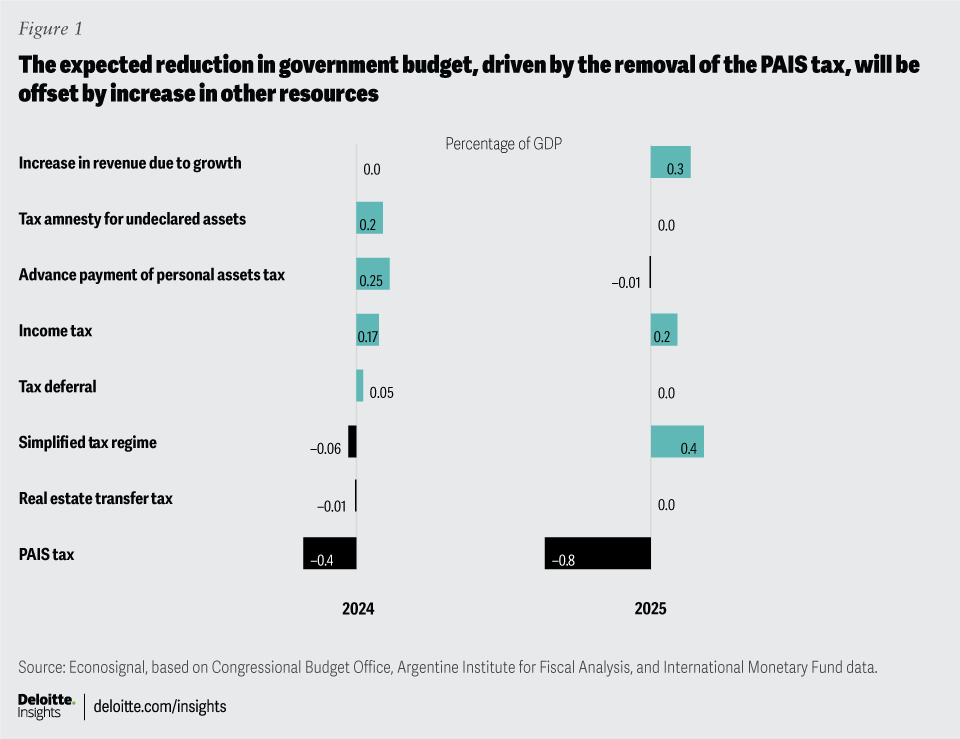

Maintaining a zero fiscal deficit poses a greater challenge for the government, especially with the removal of the PAIS tax at the end of 2024. This shift will result in a drop in revenue equivalent to 0.4% of GDP in 2024, which will be offset by higher income tax revenue, personal asset tax advances, and tax amnesty for undeclared assets (a tax must be paid when declared assets surpass US$100,000, and if certain conditions are not met).3 By 2025, the drop in revenue will be greater, but other resources will compensate for it, paving the way towards fiscal sustainability (figure 1). Concurrently, the Central Bank of Argentina (BCRA) will cease financing the treasury through monetary issuance, given debt is not expected to growth further.

Tight control of monetary supply

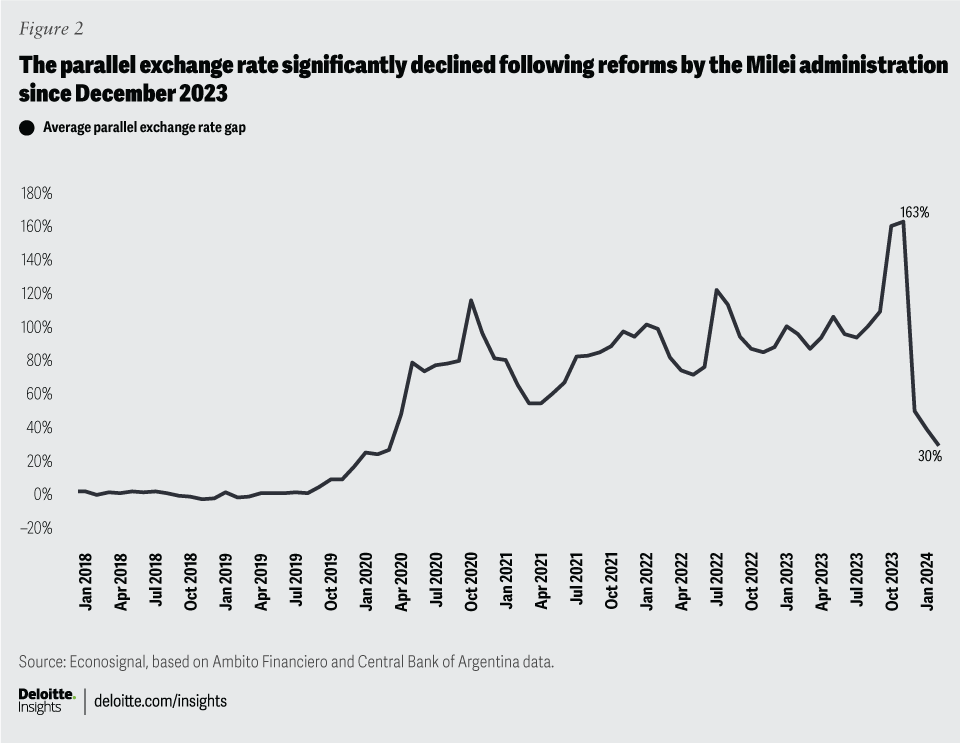

On the monetary front, Argentina’s government has announced the start of “phase two” of its economic plan, aiming to keep “broad money supply” stable. As inflation drops and economic activity picks up, the demand for pesos is expected to increase. By doing so, the government expects the parallel exchange rate to align with the official rate. Since late 2019, Argentina has imposed currency controls, creating a split in currency operations between an official market (where most foreign trade operations occur) and a parallel market (where the rest of the operations, mainly financial, take place). Before the change in government and the depreciation of the currency in December 2023, the parallel exchange rate was 930 pesos per US dollar, while the official rate was 360 pesos per dollar, marking an exchange rate gap of 158%.

By the end of September, the official rate was at 970 pesos per dollar, while the parallel dollar was quoted at 1,230 pesos per dollar, marking a significant reduction in the gap to 27%, mainly driven by the cut in the fiscal deficit, control of monetary aggregates, and government intervention in the parallel market (figure 2). This reduction in the gap brings the values closer, thereby increasing the potential for unification and liberalization of the exchange market. If not addressed, the primary issue with this scheme is that it discourages dollar inflows for investment, thus negatively impacting the country’s long-term growth.

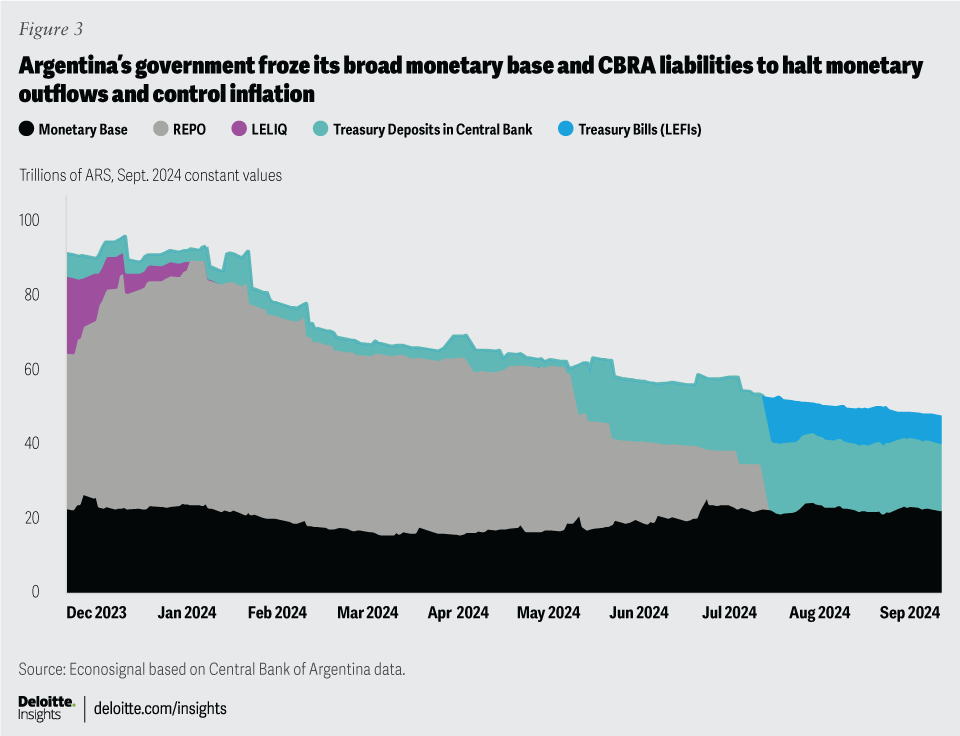

To reinforce the determination of the money supply, the government has committed to offsetting the amount of money issued from the purchase of foreign currency while maintaining a fiscal surplus. This means that the BCRA will have the capacity to intervene in financial markets to prevent the exchange rate from rising, with a capacity of US$1.8 billion—of which, US$480 million was used in July and August. Moreover, the government issued bills to absorb the remaining pesos from repurchase agreements and bills between commercial banks and the BCRA, ensuring that the interest from this debt will come from taxes and not from newly issued money. The counterpart of this operation has been an increase in treasury debt and peso deposits by the government in the central bank (figure 3).

In recent times, the decrease in the demand for money has brought the monetary-base-to-GDP ratio to historic lows—currently at 4% of GDP. As inflation stabilizes at lower values, it is expected that monetary demand could rise, reaching an equivalent of 7% of GDP. This would represent a demand of 20 trillion pesos, a value similar to the treasury’s deposits in the BCRA. In this scenario, that money could be released without affecting prices. This transactional demand has already been accompanied by an increase in credit demand. Since April, credit demand has increased by 10% per month, while deposits have increased by 2%. This implies that banks will have to reduce their loans to the public sector and begin lending more to the private sector.

Sectoral performance and economic recovery

In the second quarter of 2024, GDP fell by 1.7% compared with the previous quarter—an effect attributable to statistical drag. However, comparing with April, the economy appears to have stabilized in June. Positive data has already been observed in industries and construction, with a 1.7% monthly growth in July according to INDEC, the country’s National Institute of Statistics and Census. August presented mixed data, with negative figures for construction and slightly positive results for auto production and energy consumption. This economic rebound can be primarily attributed to wage recovery and credit revitalization—two crucial factors driving durable goods sales and construction.

Looking ahead to 2025, a significant source of risk is the lack of precipitation in Argentina. Despite expectations of a mild La Niña event, the National Meteorological Service forecasts below-average rainfall. This rainfall deficit could affect the country’s exports and, consequently, the trade-balance surplus. If this extreme event does not occur, the government could maintain the agreed-upon devaluation scheme and even reduce it, aiding efforts to decrease inflation. A descending inflation path is expected to continue through the end of 2025.

The lack of net international reserves means that abruptly lifting exchange controls would be complicated, so a gradual removal of currency controls is anticipated. To increase BCRA reserves and reduce short-term maturities, the government may enter negotiations with various institutions. This would provide the government with the flexibility to lift foreign exchange controls, and the capacity to intervene to prevent foreign exchange rates from overshooting.

Argentina’s 2025 debt amid tight short-term maturities

Argentina’s debt situation in 2025 is challenging. Public debt relative to GDP reached 110.5% in the second quarter of 2024,4 indicating very high debt levels. Key challenges include the sheer size of debts, economic volatility, and political uncertainty. However, there’s cautious optimism that the newly elected president’s policies, such as his “zero-deficit” budget and emphasis on debt repayments, might bring some stability. The long-term outlook depends on the successful implementation of these policies and the overall performance of Argentina’s economy.

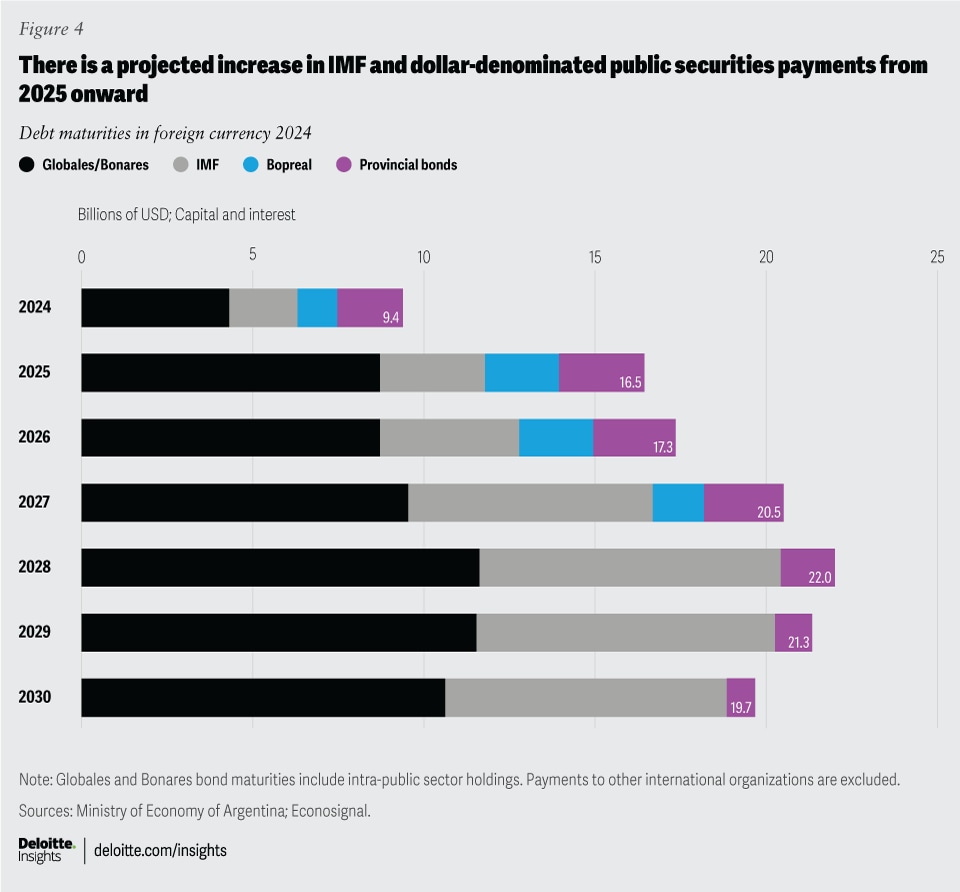

The government faces a challenging debt-maturity profile for 2025. The debt denominated in foreign currency—representing 56% of total debt5—presents greater difficulties for rollover than the debt in pesos due to country risk6 (around 1,000 basis points) and capital controls, making it difficult for the country to access international capital markets.

Among these debts, the one owed to the International Monetary Fund (IMF) stands out. The current agreement with the IMF was signed in early 2022, with the aim of refinancing maturities for the initial loan of US$44 billion, borrowed in 2018. Unlike the original loan, which consisted of a standby agreement, the current one is part of an extended facilities program—which, although on longer payment terms, includes the obligation to meet certain economic goals evaluated by the IMF in 10 quarterly reviews. If the IMF confirms compliance with these goals, it will release funds to pay the maturities of the original agreement.7

In November 2024, the IMF will conduct its last review of the agreement within the framework of the program, with a final disbursement of US$545 million. Starting in 2025, the country’s government will begin to make net payments to the IMF. However, it will have to pay US$3 billion in interest, since Argentina will not have any capital maturities remaining with the IMF.

Yet, the main challenge will lie in the maturities of sovereign bonds denominated in foreign currency (“globales” and “bonares”),8 which must be paid mainly in January and July 2025, amounting to approximately US$4.3 billion each. These payments represent 55% of the total foreign currency maturities in 2025, while these foreign currency–denominated bonds represent around 30% of the country’s total public debt.

In turn, the central bank will have to face maturities for approximately US$2 billion in BOPREAL, the bond issued by BCRA with the aim of regularizing debts of importers with suppliers abroad. For their part, the provinces will have to face debt payments in foreign currency for US$2.5 billion. Additionally, there are maturities with other international organizations for US$5.1 billion, which are more feasible for the government to pay with new lines of credit.

Given that access to credit in foreign currency is impossible, the availability of the BCRA’s net international reserves emerges as a relevant issue for the analysis. Despite the solid fiscal performance to date, Argentina has not been able to obtain the dollars necessary to rebuild the reserves at a level that ensures the payment of the obligations for the following year. After a strong accumulation of foreign currency in the first five months of 2024, purchases slowed down due to a higher volume of imports in the official market. It is expected that the central bank’s balance will be a seller’s one again in October. It will be essential to continue monitoring the evolution of net international reserves in view of government’s ability to face increasing debt maturities denominated in foreign currency.

Although the government has made gestures, such as the purchase of dollars from the BCRA with part of the deposits in pesos to ensure the payment of the January interest, there is still uncertainty about a path that allows future payments to be faced in a sustainable manner over time thanks to better macroeconomic conditions.

In this context, it is imperative for the Milei administration to obtain additional financing that will allow it to increase its net reserves and gain some leeway when facing increasingly large foreign currency–denominated maturities. In this context, the government is conducting negotiations, seeking to advance a new program with the IMF that would provide funds to rebuild the BCRA’s balance sheet.9 At the same time, to guarantee debt payments in 2025, the government is continuously negotiating a repo loan (repurchase agreement) with international banks, using government bonds or gold as collateral (figure 4).10

Meanwhile, another fundamental aspect of Argentina’s negotiations regarding the management of foreign currency debt is the swap with China. In June 2024, the monetary authorities of Argentina and China agreed to renew the entire activated portion of the swap equivalent to US$5 billion for a period of 12 months. From that moment on, the BCRA will gradually reduce the activated amount of the swap over the following 12 months, ending the agreement in mid-2026.11 The extension of the activated tranche of the currency swap allowed the BCRA to continue reducing risks and improve the terms of its foreign currency obligations profile. In this sense, it is essential for government to maintain commercial, institutional, and financial relations with China, not only to improve the payment conditions of the swap, but also to reactivate the flow of investments to Argentina in hydroelectric dams, mining, and hydrocarbons. Thus, President Javier Milei confirmed that he will travel to China in January 2025 for a joint summit between China and the Community of Latin American and Caribbean States.12 As time progresses in the maturity profiles, an increasing volume of payments to the IMF is observed, mainly from 2027 when large amortization payments begin, and of public securities denominated in dollars. For this reason, access to international credit markets as soon as possible is of utmost importance, for which it is essential to release restrictions in the exchange market and reduce country risk.

Setting the strategic path to economic stability and growth

Government’s successful implementation of strategies to stabilize the monetary base, manage debt, and control the exchange rate will be crucial in achieving economic recovery and sustainable growth. The reduction of government expenses, though challenging, has been carried out despite hurdles, but its sustainability remains uncertain. This is the main anchor of the program—if done carefully, this will enable the administration to continue reducing inflation and monetary issuance.

The decrease in inflation and the foreign exchange anchor is starting to take effect in the economy, despite the cut in government expenses. This economic rebound is driven by wage recovery and credit revitalization, boosting durable goods sales and construction. However, risks such as below-average rainfall could impact exports, the trade balance, and the sustainability of the economic plan.

A gradual removal of currency controls is anticipated due to low net international reserves, with the government likely negotiating with institutions to increase BCRA reserves and manage short-term maturities. Although maintaining fiscal discipline will be challenging, the results of lower inflation and the economic rebound could make this path easier in the long term. The necessary rolling over of debt will require significant effort from the current administration. While the future of the country appears promising across various sectors such as agricultural output, oil and gas, and software, it is imperative that the country effectively manage the short term and establish credibility. This will enable the reordering of the budget and facilitate sustainable growth in the long term.

As we enter 2025, a significant risk emerges: a lack of rainfall in Argentina. Although a mild La Niña event is expected, the National Meteorological Service forecasts below-average precipitation.13 This rainfall deficit could impact the country’s exports and, consequently, its trade balance surplus. If this extreme event does not occur, the government could maintain the agreed-upon devaluation scheme and may even reduce it, thus aiding efforts to decrease inflation. Regarding the pace of this so-called “crawling peg exchange rate,” a downward trajectory is expected to continue until the end of 2025.

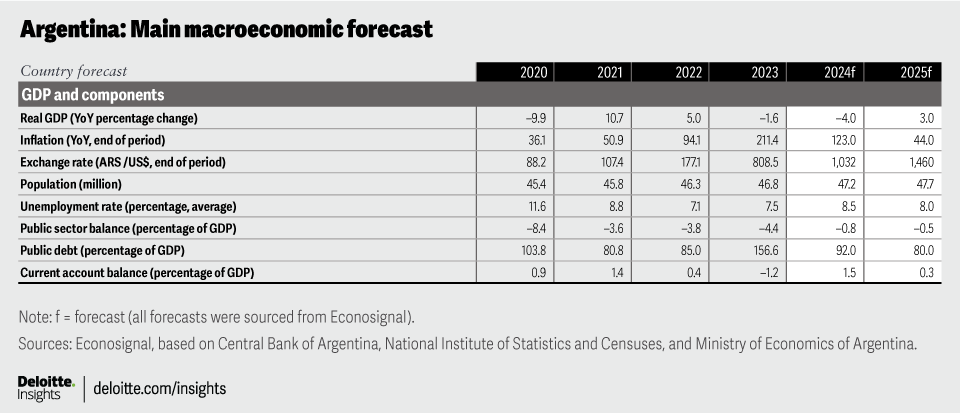

Appendix

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}