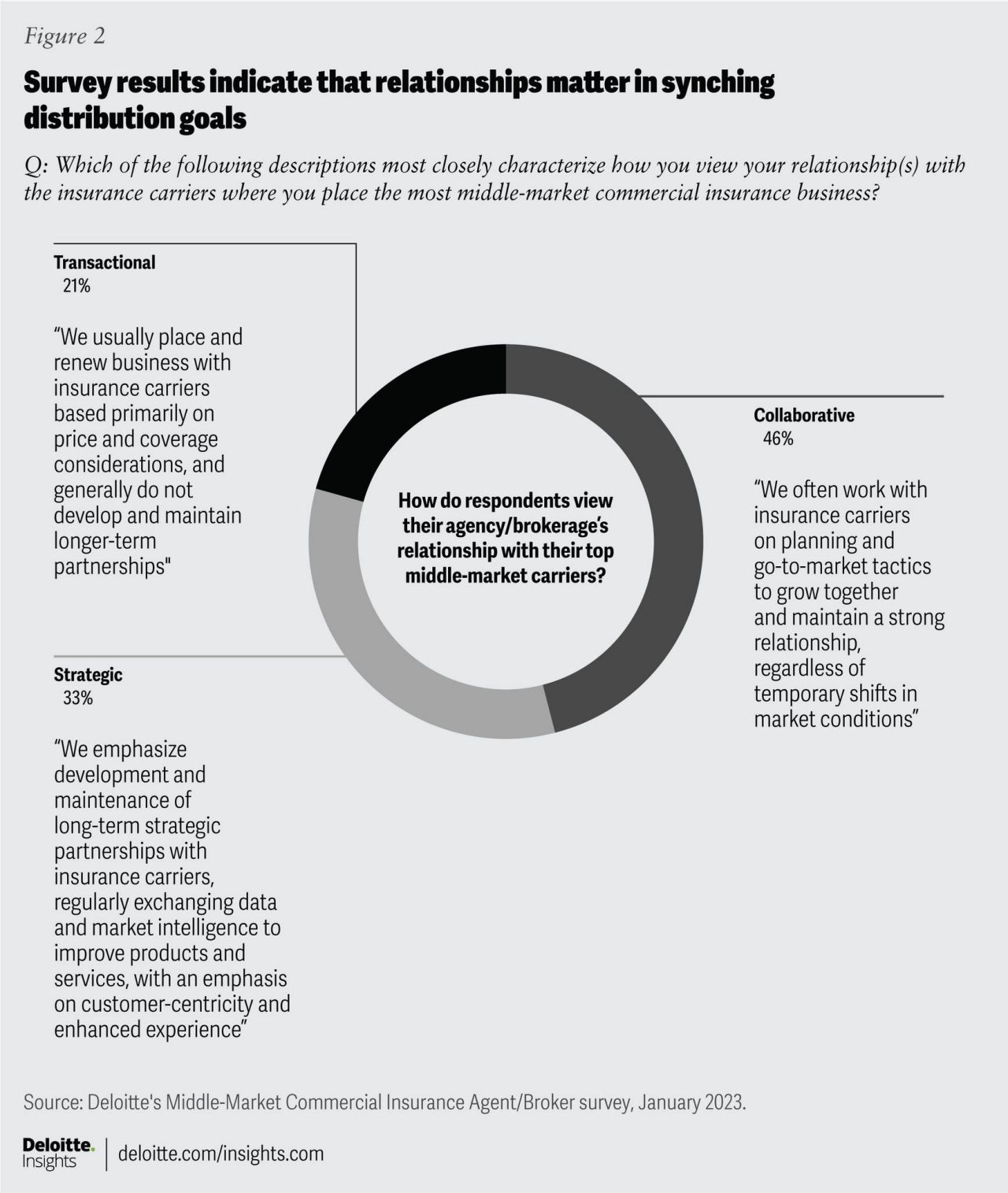

Reassess distribution makeup: Carriers should evaluate the current state of their distribution force, in terms of what percentage of production is generated from transactional ABs, versus collaborative and strategic. Does this mix align with their short- and long-term sales and market share goals in specific lines and geographic regions? If not, where might adjustments be made? For instance, carriers looking to lessen price-driven turnover should avoid having their distribution mix lopsided toward transactional distributors. Yet, transactional ABs may be far more valuable to newcomers seeking to buy their way into a particular market by underpricing the competition, at least in the short term. Rationalizing a carrier’s distribution portfolio can also yield savings on licensing and administrative expenses for low-producing transactional agencies.

Reset relationship mix: Once a preferred distribution-force ratio is determined, carriers should be looking to nurture relationships with the types of ABs with whom they wish to develop long-term partnerships. Carriers seeking to optimize their relationship mix should identify which transactional ABs might have the potential to become collaboratives, and which collaboratives could be upgraded to strategics.

Determine differentiation levers: Whether a carrier is trying to maintain or alter its producer mix, tailored approaches to establish and sustain longer-term partnerships may be called for, since each relationship type has its own set of preferences and priorities. Retention incentives could be raised, for example, to convince transactional ABs to keep more business in place. Greater data-sharing along with value-added risk management services could attract and retain more collaborative ABs. Providing leading ABs with a seat at the table to discuss product development and go-to-market plans could help impress strategic distributors.

Alter processes, while demonstrating commitment: To become more committed partners with their preferred ABs, carriers could consider altering how they deal with distributors in both day-to-day interactions and long-term planning. A logical starting place might be to appoint relationship managers for collaborative ABs, with concierge-level attention provided to current and potential strategic partners. If transactional ABs are the prime target of a carrier’s distribution strategy, more data-driven insights on leads and referrals for prospecting, cross-selling, and upselling could be a compelling value proposition.

Commitment can also be demonstrated by providing greater clarity to ABs on a carrier’s sales goals, target markets, and risk appetite—a point that ranked high among nearly all those surveyed regardless of their relationship segment. This resonated with one carrier-distribution leader we interviewed, who said the lack of such clarity has resulted in “tremendous submission inefficiency,” with thousands of coverage applications rejected out of hand because they were not among the carrier’s preferred targets. “Our cost of acquisition is too high, and one way to lower it is being better at communicating what kinds of business we actually want to write and at what price range,” this interviewee noted.

Establish ongoing feedback loop: Finally, carriers could establish ongoing communication both internally (to make sure leaders of various business lines and operational functions are aware and on board with evolving distribution strategies) and externally (to get regular input from ABs and make them part of the decision-making process, emphasizing collaboration and partnership). Along those lines, carriers could consider establishing a distribution council, with key ABs and carrier leaders as members. Such feedback could help flag areas of concern—such as a problematic product or go-to-market initiative that should be tweaked or dropped.

While appointing relationship managers could help facilitate greater communication and quicken response time to any issues raised, strategic and higher-level collaborative ABs should have access to a wider range of carrier contacts. Munich Re, for instance, looks to offer a “holistic” broker-centric experience by connecting ABs with a broad range of individuals at the carrier involved with insurance and risk management services, or those with specialized product and industry expertise, rather than perpetuating a siloed approach with AB contact limited to assigned underwriters.11

The ultimate barometer of success for a carrier’s AB strategy should be influenced by return on investment. Not every insurer has access to investment funding to enable and cultivate the relationships targeted in their strategy. Carriers should take a pragmatic approach in understanding which types of relationships are worthy of limited investment budgets and set their strategy, enablement, and data-sharing agendas accordingly.

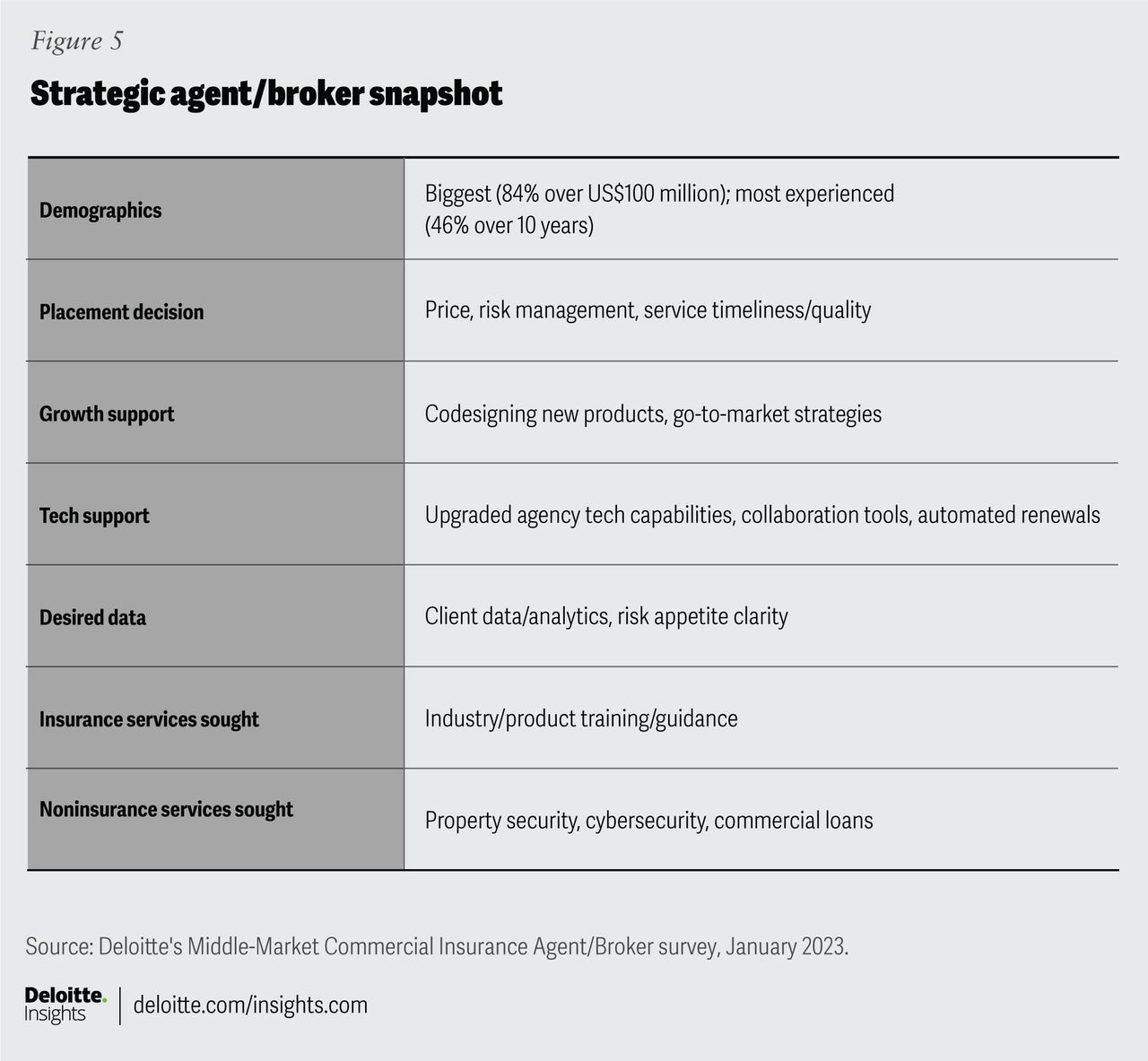

Depending on a carrier’s strategy, many may consider a balanced approach to near-term and long-term planning by cultivating long-standing relationships with strategic ABs that can yield significant distribution production over the course of many years, while attracting and optimizing the production results they can achieve from transactional ABs in markets where their product lines are competitive.

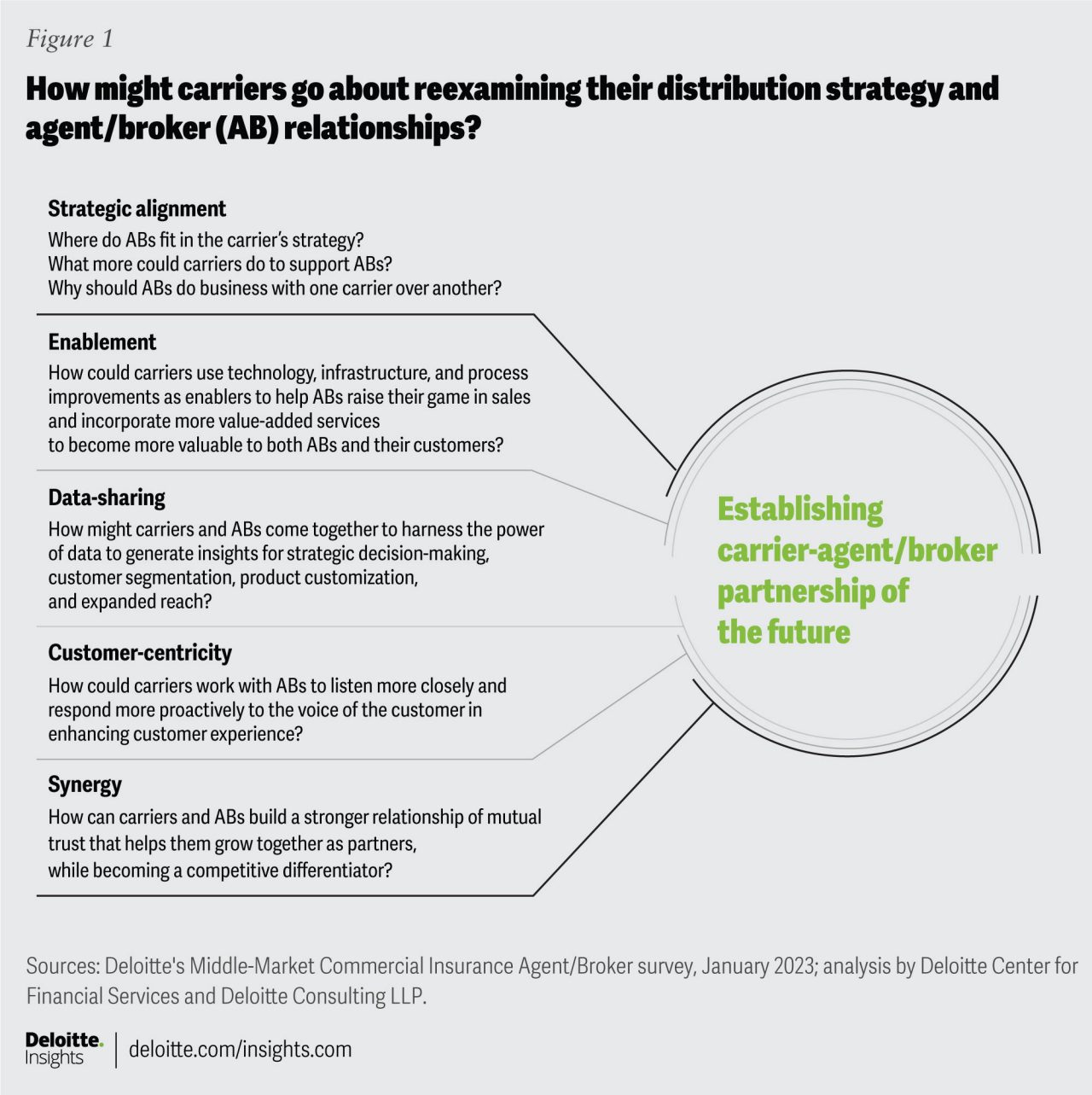

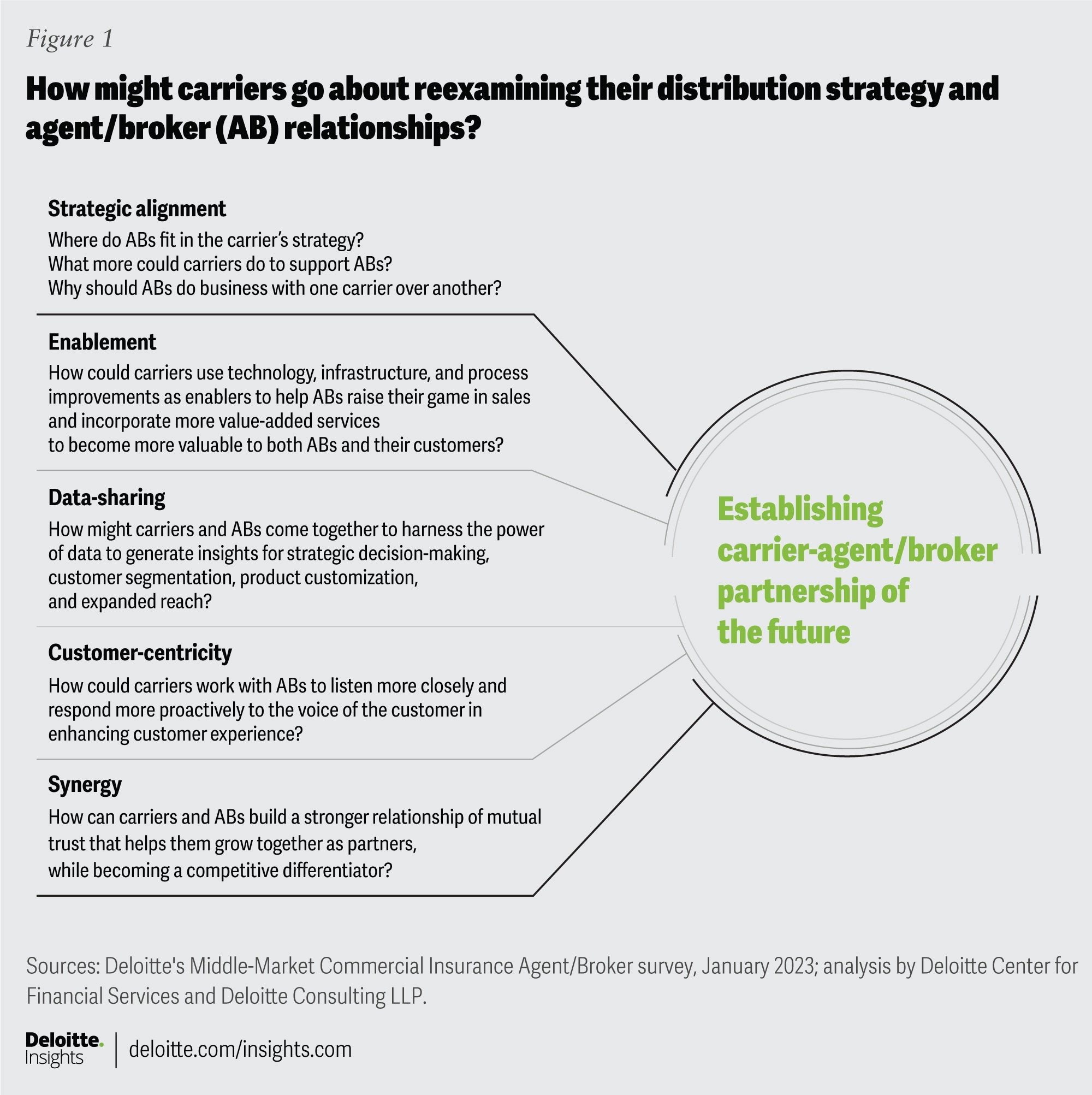

Forging the carrier-agent/broker partnership of the future

The insurance landscape is rapidly evolving, thanks to the development of alternative data sources (such as sensors in buildings, vehicles, and wearables) as well as emerging technology to help make new information streams actionable (such as segmentation algorithms). In increasingly commoditized small-business insurance, advancements in robotic process automation and artificial intelligence are making it easier to bypass purely transactional ABs, helping drive growth in direct-to-consumer sales by carriers and self-service options for policyholders.12

Middle-market commercial accounts, however, should remain impervious to widespread disintermediation for the foreseeable future, given the size and complexity of the risks facing companies generating up to US$1 billion in revenue. The challenge for carriers looking to enter, grow, or at least maintain market share in this increasingly competitive market will therefore likely be in finding ways to strengthen relationships with the ABs who often serve as full-service risk managers rather than simply placing insurance for such clients.

To accomplish this, many carriers will likely have to offer more than just a competitive price quote to attract and retain middle-market business—at least for those looking beyond any purely transactional business they conduct, which is often volatile and expensive to maintain. Having a wide range of risk management and noninsurance services in their repertoire could drive more business their way for collaborative and strategic ABs, while attracting more loss-control-oriented accounts that could translate into lower frequency and severity of claims.

A major differentiator for many carriers, however, is likely to be a better understanding of what motivates different kinds of ABs serving the middle market, and being prepared to fulfill the preferences and priorities of each relationship segment. Such points of distinction should become increasingly important as the middle-market distribution force continues to consolidate and evolve, prompting more carriers to be asked what they are doing to earn the business generated by the most productive and profitable ABs of all types.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}