Navigating an evolving and diverse cloud network

The industry cloud provider network is still evolving. Key players in the network—hyperscalers, enterprise software providers, core banking providers, emerging SaaS providers, and system integrators—are all rapidly developing new offerings. In fact, our interviews with providers revealed a highly varied approach to industry cloud strategies, capabilities, and codevelopment models.

Hyperscalers tend to see industry clouds as a strategic shift. Their approach, largely, is to bundle existing products and customize advance features on their platforms using an industry-specific lens. One of the hyperscalers we spoke to plans to shift focus away from being product-centric to customer-centric. Its current industry cloud portfolio, for instance, pieces together existing capabilities in different combinations to solve specific business use cases, including customer onboarding, financial crime, and regulatory compliance.

Meanwhile, Google is big on using advanced technologies (e.g., AI, ML) to extract data from traditional “line-of-business” applications such as customer relationship management (CRM) to help optimize outcomes to address industry-specific challenges.16

AWS is trying to bolster its sector expertise through strategic hires and market focus but is relying on its network partners to build industry clouds using its platform as the backbone.17 IBM too, has launched a cloud for financial services.18

Enterprise software providers consider industry clouds as the next phase in their evolution. They are typically creating industry-specific customizations on top of existing horizontal applications. SAP’s industry cloud is integral to S/4HANA and is considered a growth driver for the company. SAP and its ecosystem are building deep industry-specific capabilities on SAP Business Technology Platform (BTP), which enables access to SAP’s core business applications, including S/4HANA.19 For instance, SAP leveraged SAP BTP to launch embedded finance as a service recently.20 Salesforce too is seeing significant uptake of industry clouds.21 Salesforce’s acquisition of Vlocity allows it to add industry-specific workflows to its existing products.22

Meanwhile, core banking software providers have or are transitioning to an open architecture and, in some cases, a “cloud-like” operating model, which entails “as-a-service” approach,23 elastic infrastructure, and possibly new pricing models including consumption/subscription billing. For example, Fiserv’s acquisition of Finxact, a cloud native core banking software provider, enables third-party integrations through open APIs.24 Further, core providers are leveraging partnerships with hyperscalers. For example, FIS launched its Modern Banking Platform with one of the hyperscalers.25

Niche emerging SaaS providers, on the other hand, seem to have varied views on industry cloud. Some consider themselves to be industry clouds since they’re exclusively focused on banking and capital markets since inception. Meanwhile, others are indifferent to the concept but hope that industry clouds will shift the conversation away from industry-agnostic products.

That said, they are likely to leverage a “cloud first” approach and emerging technologies to address singular use cases. Further, their deep sector specialization is likely to keep them ahead of the curve, allowing them to build market capabilities faster than providers in other categories. However, since they are often small-scale players, they may look to align with larger players, especially hyperscalers, to expand their reach. These providers can also be attractive acquisition targets.

System integrators too are actively moving into this space. They bring sector expertise along with technology acumen and work across technology providers. Overall, industry cloud is a partner play. Despite different verticalization strategies, vendors from different categories are likely to codevelop industry cloud solutions, in collaboration with system integrators, and in some cases, leading banks, providing monetization opportunities to all.

A deeper dive into industry clouds for banking and capital markets

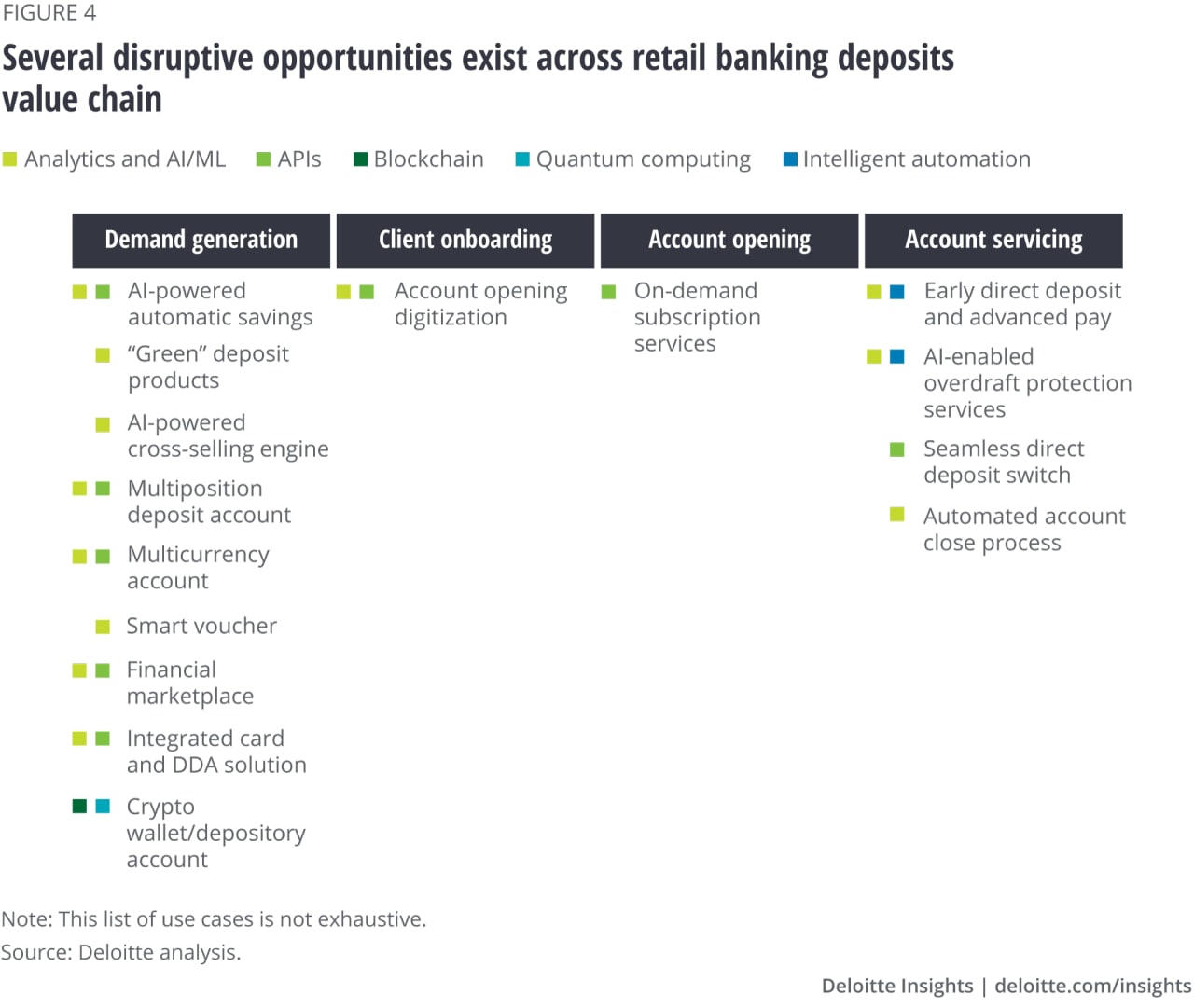

Putting a futuristic lens to the value chain and business issues across B&CM segments can highlight several disruptive industry cloud use cases. Key Bank, for example, uses industry cloud for loan origination. HSBC codeveloped a new risk advisory tool that allows them to run complex simulations 16 times faster than before. The capability was built in less than five months.26 And Goldman Sachs set up a new transaction banking-as-a-service platform in collaboration with AWS.27

Figure 4 illustrates a sample of use cases for potential industry cloud adoption across the retail banking deposits value chain. These industry cloud use cases can bring together emerging technologies to offer a near-ready-to-deploy solution. For instance, banks can use industry clouds to enable automated savings—the ability to sweep spare change into an investment account—built by overlaying AI/ML technologies and API functionality.

Similarly, industry cloud can enable a multiposition deposit account i.e., savings position, transaction position, and line of credit all under one account, which uses analytics and AI/ML, and APIs to move funds in and out of positions depending upon payment sources and customer limits. Other potential industry cloud use cases include digital account opening, on-demand subscription services, and AI-enabled overdraft protection.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}