An evolving world of digital goods and services

With the young at the helm, rising digital spending is poised to reshape consumers’ wallets.

Leon Pieters

Kasey Lobaugh

Anthony Waelter

Stephen Rogers

Initially confined to a handful of categories like music and eBooks, consumer spending on digital goods and services has come a long way. The rise of digital content stores and streaming platforms has played a pivotal role in bringing digital spending into the mainstream.

Learn more

Now, digital goods and services seem poised to reach a new stage of evolution.

The convergence of cloud, IoT, AI, and other technologies is helping an explosion of new digital goods and services to permeate more corners of everyday life. From personalized health and fitness tech and smart collars that digitally monitor our pets, to premium subscriptions for a world of online content creators, a wave of emerging digital goods and services is helping meet consumer needs and wants in entirely new ways. As daily life becomes more immersed in the growing value that digital goods and services provide, the consumer’s wallet is poised to shift. And that shift brings important implications to the future of the consumer industry.

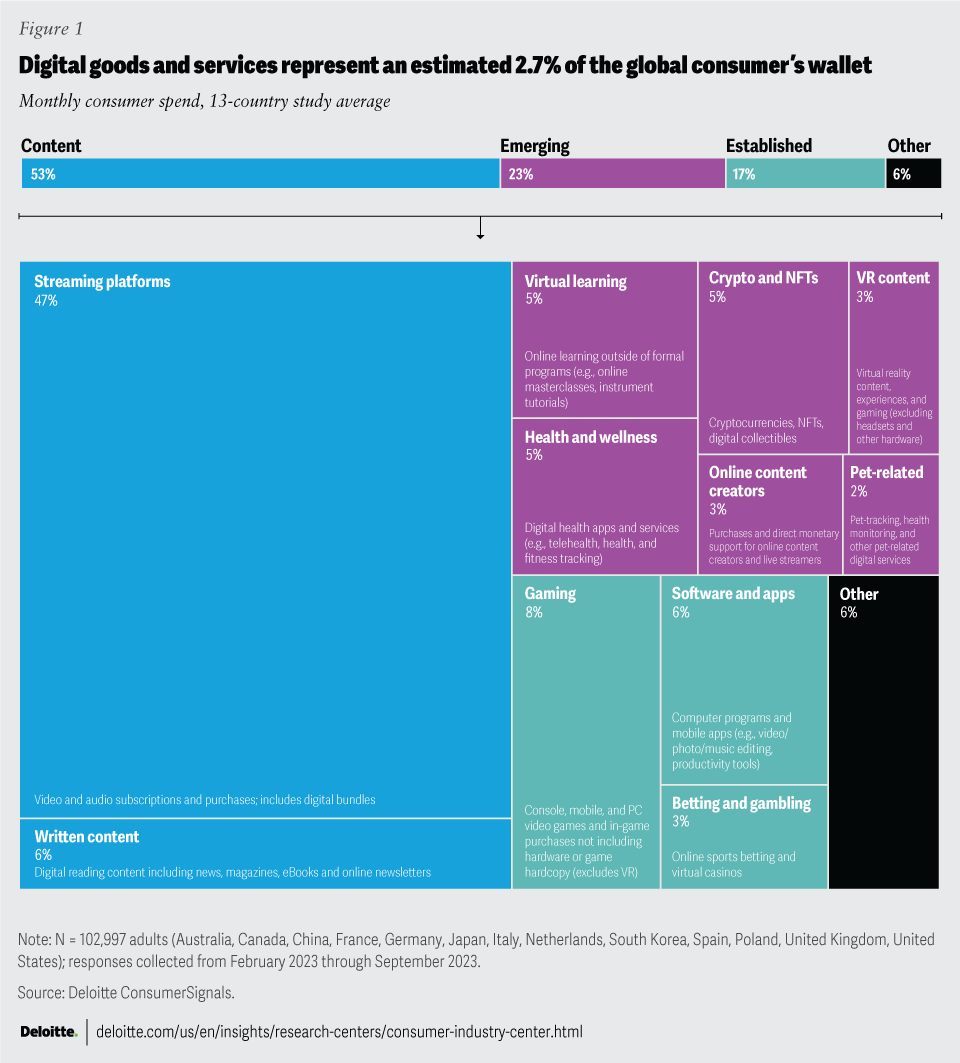

For insights into digital spending behavior, we analyzed the reported monthly spending of over 100,000 consumers surveyed in 13 countries across 12 digital categories (see figure 1 for category definitions).1

Combined with traditional monthly spending (that is, housing, groceries, transportation, and more discretionary categories),2 digital goods and services represent an estimated 2.7% of the consumer’s total wallet.3 The figure may seem insignificant, but for perspective, it’s beginning to stand side-by-side with categories such as clothing (3.9%) and electronics (3.5%).4

Streaming platforms and digital written content still comprise the bulk (53%) of consumers’ digital spending (figure 1). But emerging categories are firmly on the map too. Emerging categories, including health and wellness, virtual learning, virtual reality (VR) content, and online content creators, represent almost a quarter (23%) of digital spending. The trend strongly suggests that digital spending appears to be maturing beyond streaming entertainment.

{kind=link}

The young and the digital

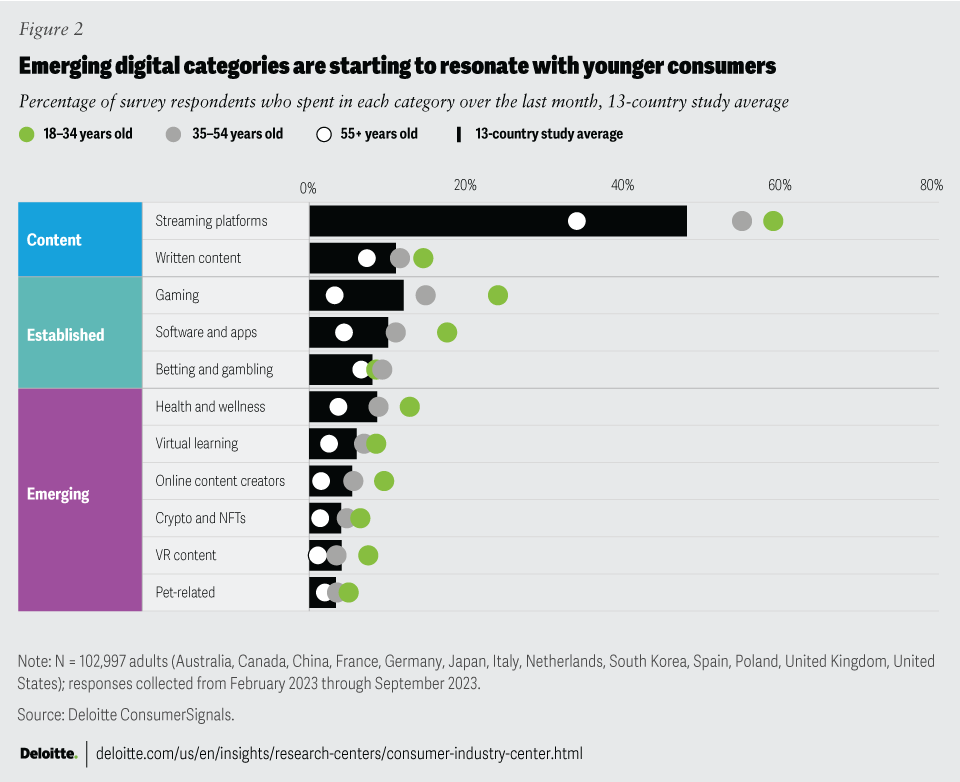

Younger consumers are the driving force behind digital spending. And it's not just about how much they spend but also where they spend. Most 18–34-year-olds surveyed spend monthly on streaming platforms (figure 2). One in four spend on gaming.

{kind=link}

However, their gravitation toward emerging categories appears to be reshaping the digital spending landscape. Roughly one in 10 spent on categories like health and wellness, virtual learning, VR content, and online content creators.

Interestingly, while emerging categories command smaller audiences, they’re typically an engaged audience of higher spenders. For example, the average monthly spending in the streaming category is roughly US$30. But while significantly fewer spend on content creators, the average spend jumps to US$40 a month. Other emerging categories see similar trends. Spending jumps to about US$50 in digital health services, US$55 in VR content, US$60 in virtual learning, and US$80 in cryptocurrencies and NFTs.5

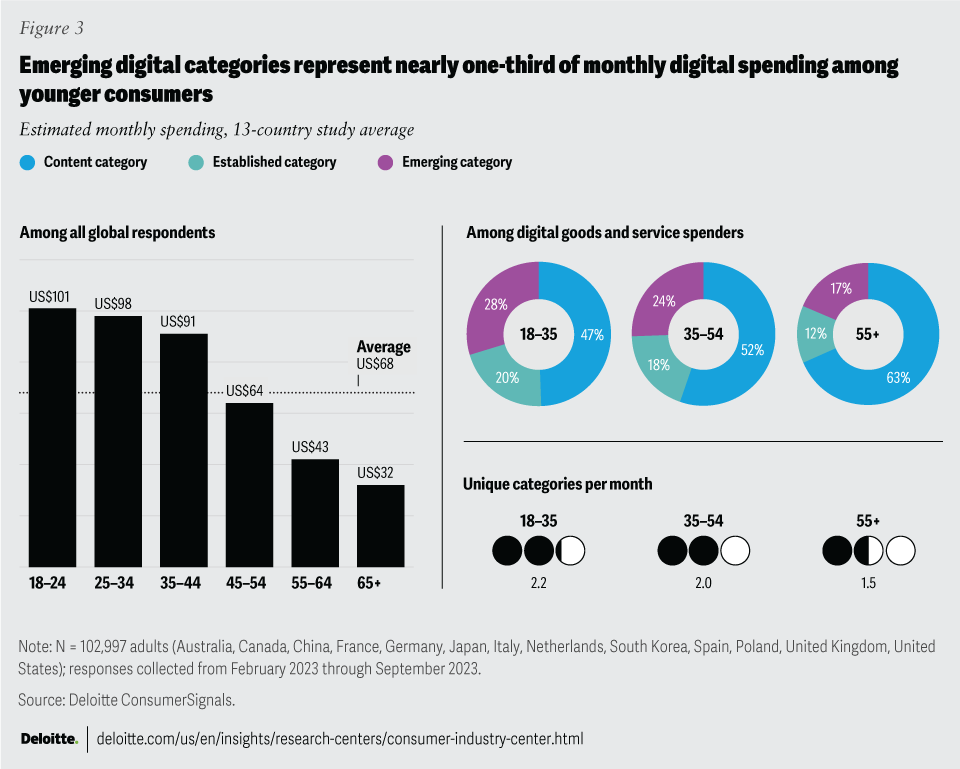

And as younger consumers splurge on more emerging categories, their overall monthly digital spending is also growing (figure 3). Consumers aged 18–34 surveyed spend an estimated US$100 per month across all categories combined, with nearly one-third of that spending going to emerging categories. In stark contrast, consumers 55 years and older surveyed spend US$30–US$40, with the majority of that spending (63%) confined to streaming.

{kind=link}

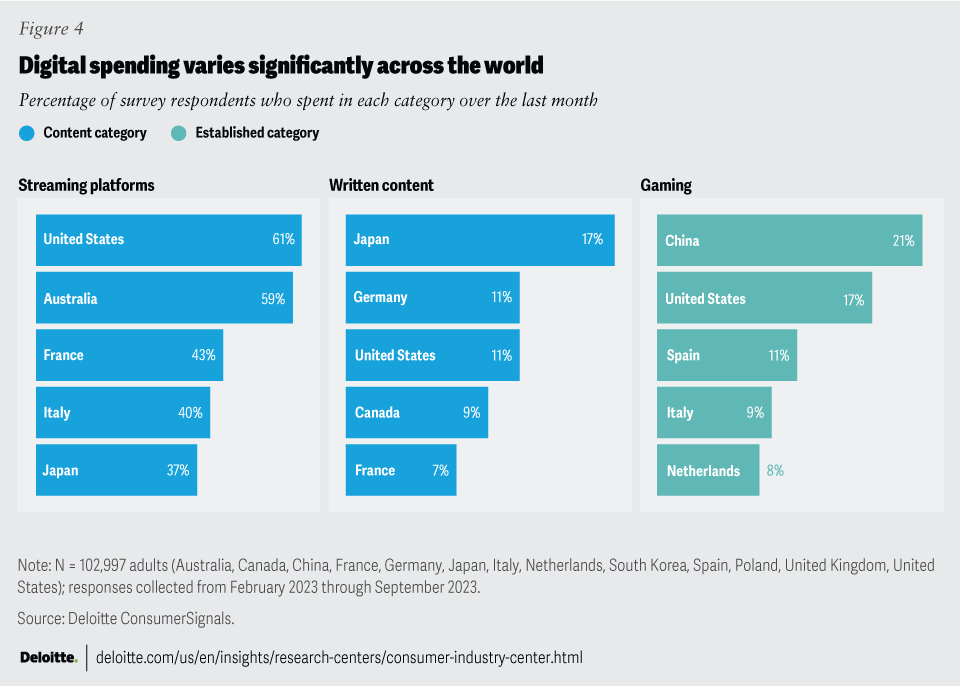

Beyond age, some digital spending categories vary by country, suggesting nuanced market evolution in these categories. Local restrictions in online betting and cryptocurrencies drive some disparity.6 However, significant differences within mature categories like streaming strongly suggest culture and local market dynamics are at play.

Japan offers a good example.

An estimated six in 10 consumers surveyed in the United States and Australia spend on streaming platforms every month (figure 4). In Japan, however, that figure falls sharply to 37%, likely driven by Japan’s enduring tradition of physical media.7 Interestingly, while streaming services lag in Japan, demand for online written content, including news, magazines, eBooks, newsletters, and other readable content, is high (17%).

{kind=link}

A zero-sum game

With rising spending on digital goods and services among the young and the increasing relevance of emerging digital goods and services, there are implications for a broad range of consumer businesses, not just pure technology players. The consumer’s wallet is a zero-sum game, so growth in digital spending will likely come at the expense of traditional spending (or saving) elsewhere.

The zero-sum relationship was often easier to understand in digital’s formative years. In less than two decades, digital downloads and streaming shifted the balance of power in the global music industry.8 During that time, industry revenue went through a trough but eventually recovered to new highs. However, who captured value was vastly altered. With the speed of digital evolution today, spotting emergent competitors for your company’s share of the consumer’s wallet may become more elusive.

Take the gaming industry, for example. The global video game industry commands a staggering US$188 billion in revenue.9 But some of the world's leading titles are free to play, generating revenue through microtransactions (or in-game purchases). Skins and other in-game items and cosmetics are not just a way for gamers to gain the upper hand, but also how many players express themselves within increasingly crowded virtual social spaces. Recent forecasts put the global microtransaction market, including in-game virtual goods and related services, at US$106 billion in 2026, growing at a 12% CAGR.10

The young gamer who typically asked for a new pair of trendy sneakers for their birthday might now turn their attention to a unique skin for their online avatar. Ultimately, the shift in consumer preference translates to a change in spending away from physical clothing and apparel to the gaming industry. And with the average gamer in their mid-30s, this spending behavior could be more prevalent than some might expect.11

Some forward-looking clothing and apparel brands are already leaning into the trend.12 But there’s likely much more change on the horizon. With emerging technologies like generative AI, we’re potentially heading toward a future where digital clothing can be superimposed onto any social media post or digital medium. In theory, consumers could flaunt their favorite brands to friends, family, and followers without buying the physical product.

For traditional apparel companies, stepping in can bring new opportunities, while inaction could reduce the evolving digital world into a competitive threat.

Stepping in

The path forward can look uncertain for many consumer companies, particularly those centered around physical products and experiences.

Companies are increasingly stepping in. For example, several auto OEMs have launched paid subscriptions for premium vehicle features with differing success.13 But with each success or failure, these innovative auto companies can learn more about how a digitally evolving world of consumers may want to engage with their favorite brands.

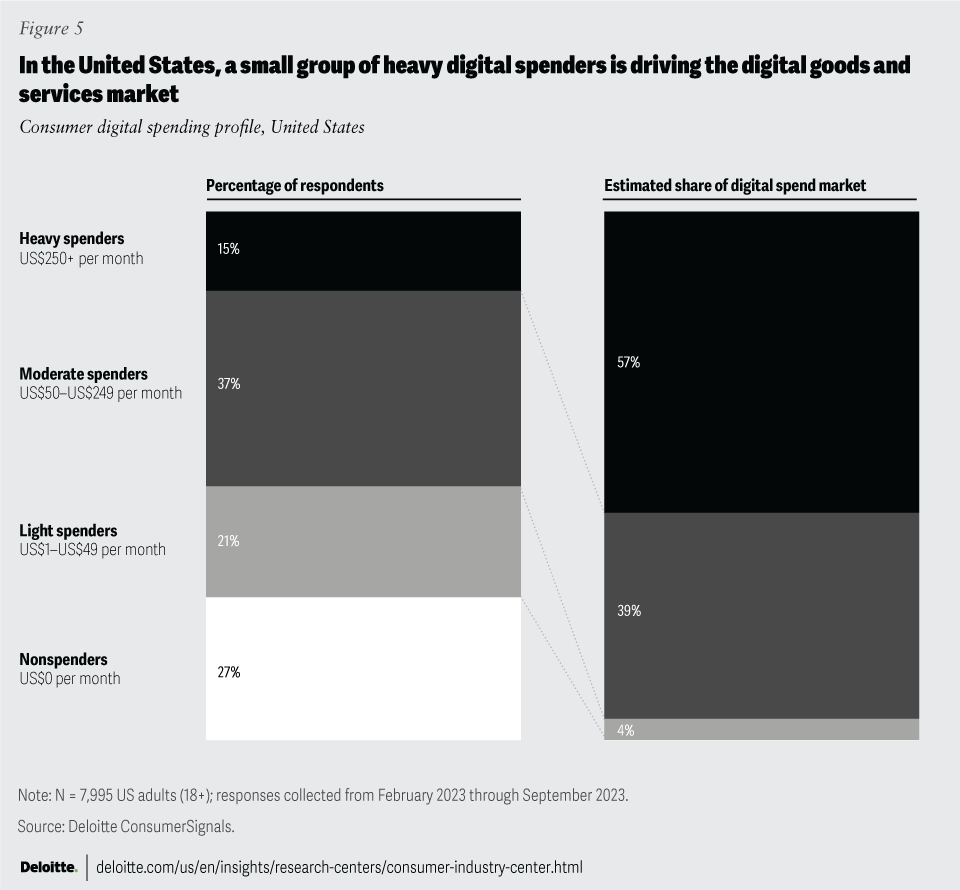

Consumer companies looking to innovate likely have a solid consumer segment to target. A relatively small but engaged group is driving the digital spending market in most countries. In the United States, for example, 15% of adults surveyed spend US$250 or more per month on digital goods and services (figure 5). These heavy digital spenders account for an estimated 54% of the digital goods and services market.

{kind=link}

This group of heavy spenders could signal what’s to come. At the very least, they’re consumers who could be receptive to innovative engagement strategies.

For companies looking to step into the digital goods and services space, here are some questions to consider:

- Where are the new threats (that is, alternative players, IP protection, etc.) and opportunities (that is, complementing physical products or new service offerings)?

- What’s your organization's virtualization strategy, and what capabilities are needed?

- How will new capabilities be acquired? And how might technologies like AI help reduce the cost of copy, code, and content to support new digital services?