{kind=link}

{kind=link}

{kind=link}

The rise of digital goods and services: Opportunity over threat has been saved

The authors would like to thank Jeff Loucks and Marcello Gasdia for their contributions to the article.

Cover image by: Sofia Sergi

United States

United States

United States

Industry empires already exist on the rise of digital goods and services. From giant streaming media platforms to blockbuster gaming titles and their in-game microtransactions, digital goods and services command billions in annual revenue.

But it all could still be humble beginnings.

Digital offerings are evolving at a lightning pace. From health and fitness apps that personalize to their users, to smart collars that digitally monitor our pets, the convergence of cloud, Internet of Things (IoT), artificial intelligence (AI), and other technologies are helping an explosion of new digital goods and services permeate more corners of everyday life. Looming a bit farther on the horizon, the metaverse could hold even more potential to further blur physical and virtual worlds, possibly with their own digitally native economies, assets, and trade.

For many consumer companies, the ongoing revolution in digital goods and services represents both threat and opportunity. An early wave of digital disruptors already led to the demise of some consumer industry titans. But the risk is likely far from over.

As daily life becomes more immersed in the growing value that digital goods and services provide, the consumer’s wallet may be poised to shift. And that shift is likely well underway.

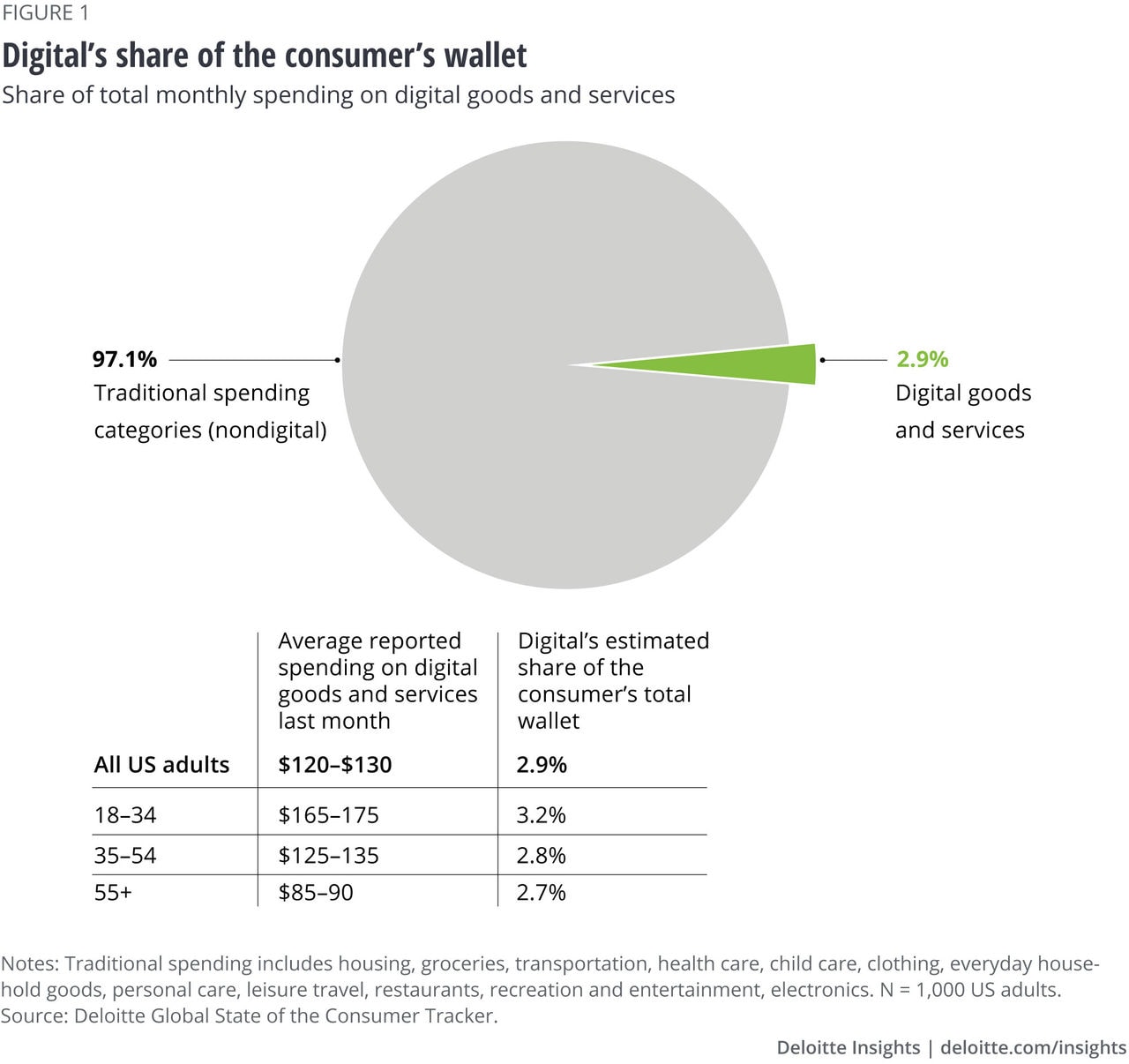

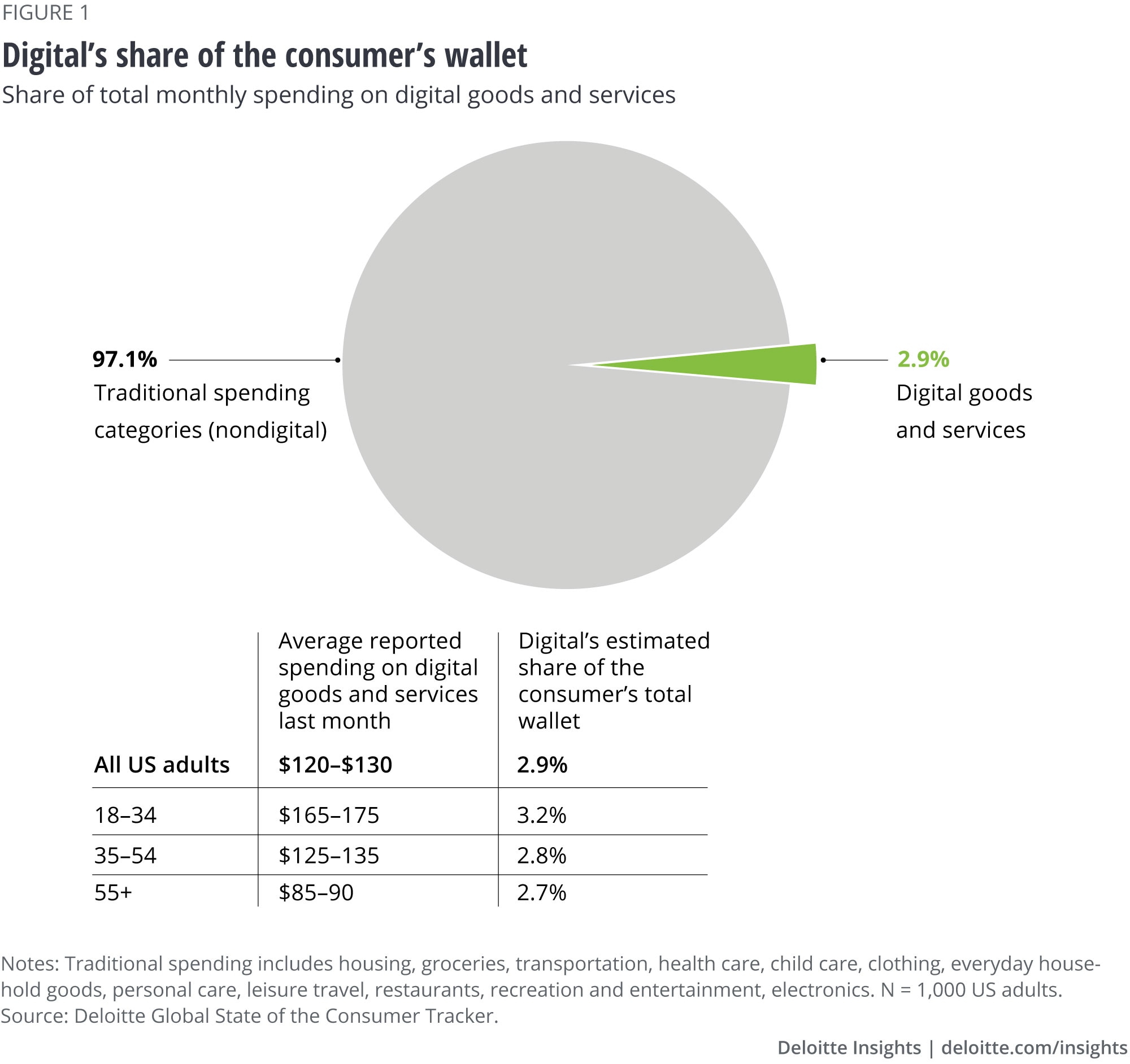

According to Deloitte’s ConsumerSignals, US adults surveyed estimate spending from US$120 to US$130 per month across 12 digital goods and service categories (figure 1). These categories included popular digital goods and services, such as streaming entertainment, gaming, and apps, as well as a slew of more nascent ones such as digital health and wellness, virtual reality content and experiences, virtual learning, cryptocurrencies and digital collectibles, live-streaming platforms, pet technology, and others.

At this level of spend, digital goods and services represent an estimated 2.9% of surveyed consumers’ total wallet (figure 1). The figure may seem insignificant. But for perspective, it’s beginning to stand side by side with major categories such as clothing (3.8%) and electronics (3.4%).1

Economic context is important here too. Digital goods and services tend to fall on the more discretionary side of consumer spending. Over the past year, consumers’ discretionary spending intentions weakened considerably as many grapple with inflation.2 Spending on digital goods and services could very well be higher in better economic conditions. Currently, digital goods and services represent an estimated 12% of respondents’ discretionary spending, including recreation and entertainment, leisure travel, electronics, and restaurants.3

While spending behavior across the broader adult population provides some perspective on the current state of digital spend, younger generations offer insight into where we’re likely headed: more spending across more categories.

At US$165–175 per month, consumers aged 18–34 spend roughly 1.4 times more than average on digital goods and services (figure 1).

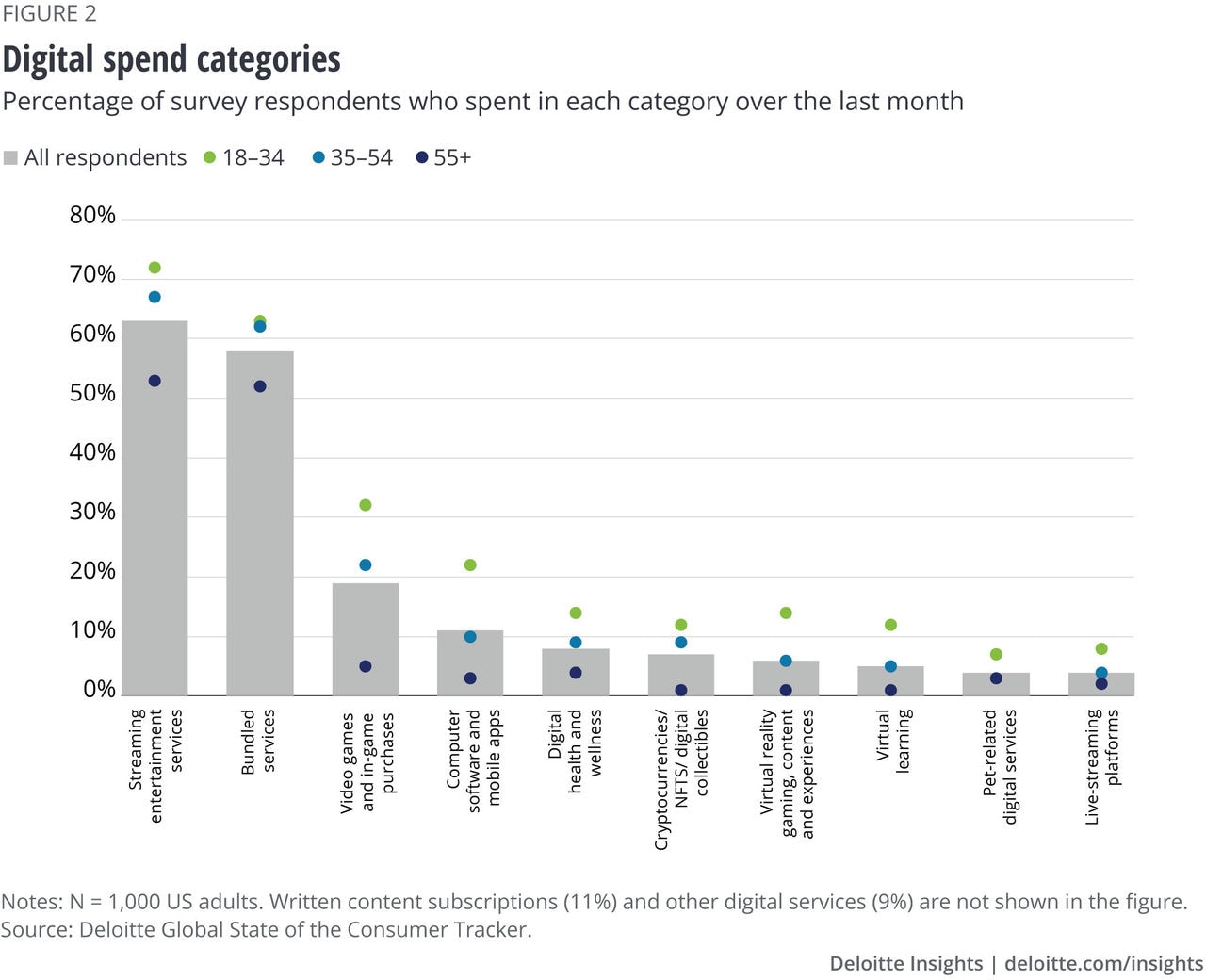

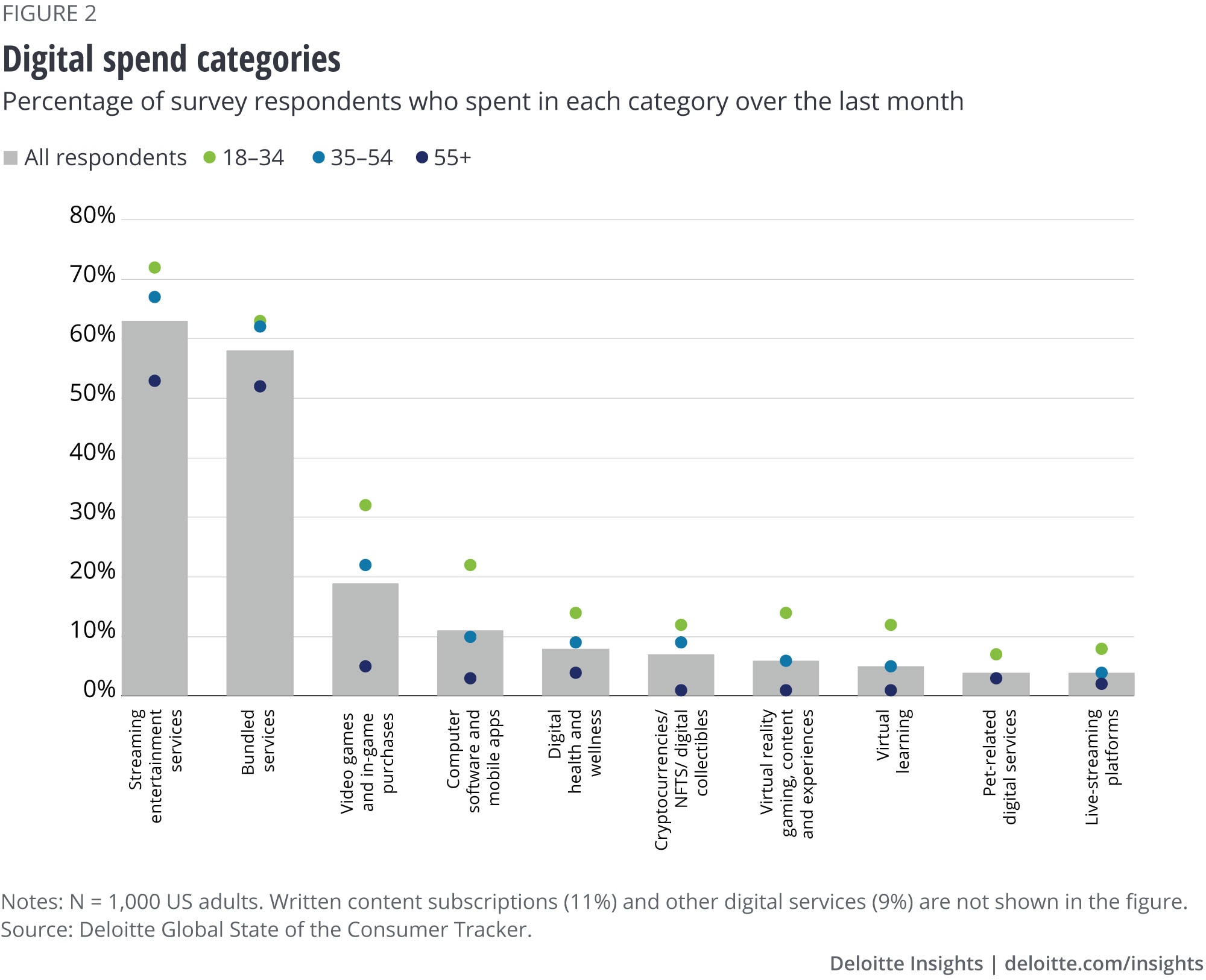

Heavy spending among younger generations could be a bullish signal for digital goods and services. But it’s not just about how much they spend. It’s about where they spend too. Among younger adults, digital spending is beginning to proliferate across more nascent categories (figure 2).

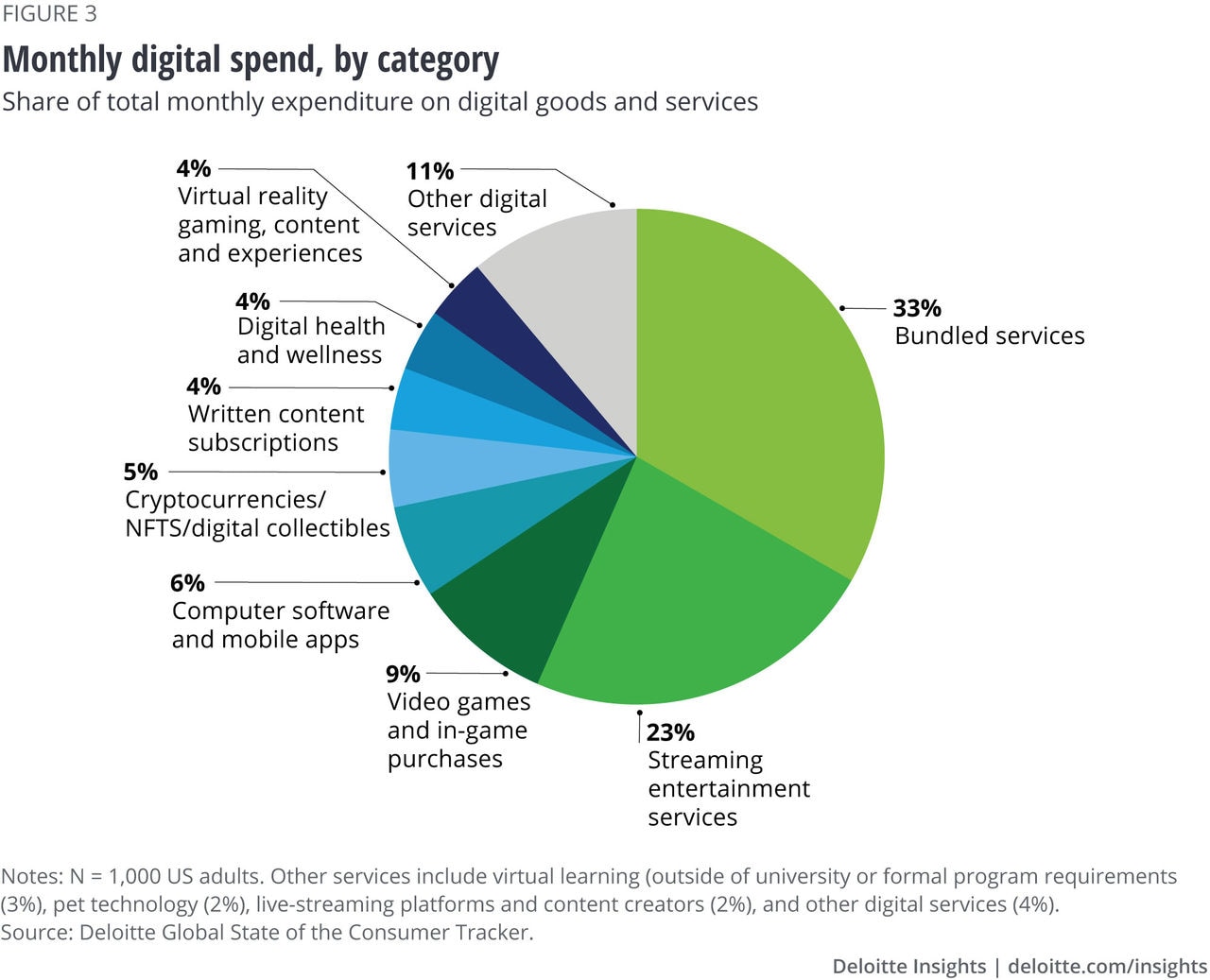

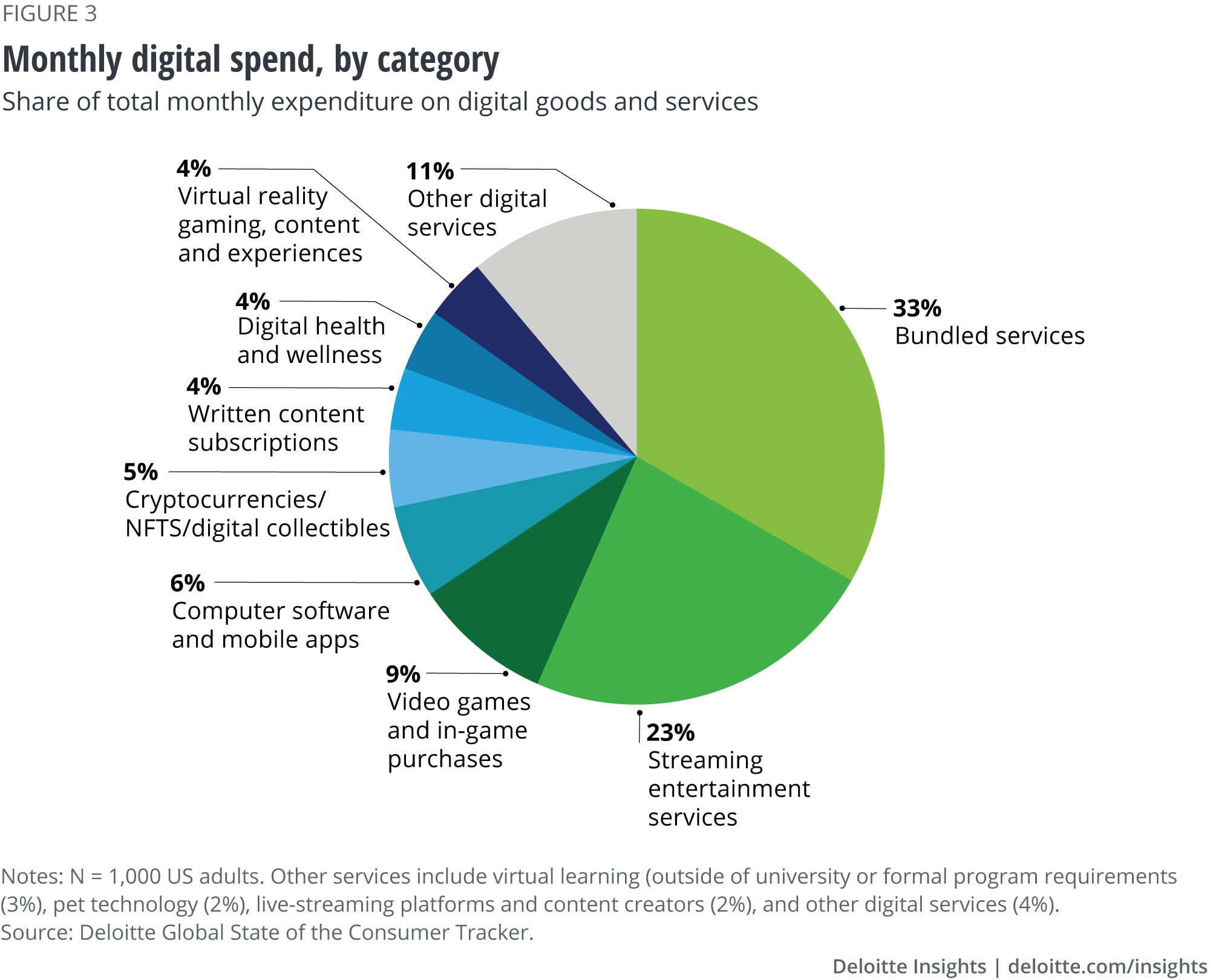

For the average consumer, spending on digital goods and services is still heavily concentrated around streaming entertainment (figure 2). Roughly six in 10 survey respondents cited spending in the category over the past month (figure 2). A comparable number spent on bundled digital services, which also typically focus on packaged streaming entertainment platforms. Alone, these two categories represent more than half (56%) of all spending on digital goods and services (figure 3).

Beyond streaming entertainment, however, purchase activity drops significantly. Categories such as digital health and wellness, virtual reality content and experiences, virtual learning, and cryptocurrencies and digital collectibles only command audiences in the single digits (figure 2).

But that trend shows signs of shifting among younger adults. Across the 12 categories measured, consumers aged 18–24 spent on an average of 3.1 different categories over the past month. In stark contrast, consumers aged 65 and older spent on an average of 1.5.

Several nascent digital categories, including digital health and wellness (14%), virtual reality content and experiences (14%), virtual learning (12%), as well as crypto and digital collectibles/NFTs (12%), are beginning to trend well with younger audiences (figure 2). Unsurprisingly, more mainstream categories such as gaming including in-game purchases (32%) and mobile apps and computer software (22%) are strong drivers behind younger consumers’ higher digital spend.

Additionally, many of the categories that younger consumers are spending on, while less popular overall, are high-spend. For example, consumers surveyed estimate spending an average of about US$40 monthly on streaming entertainment platforms.4 But average spending jumps to US$83 in virtual reality content and experiences, US$90 in crypto and digital collectibles, and US$55 in gaming and in-game purchases.5

So while nascent categories currently have smaller audiences, many command strong spending. Together, the emerging categories included in the study, including digital health and wellness, crypto and digital collectibles, virtual learning, live-streaming platforms, and pet technology represented 20% of total digital spending (figure 3). Digital spending is poised to grow if these categories mature and grow their audiences. If younger consumers are any indication of the future, that trend is more likely to strengthen than not.

It doesn't take much to imagine the potential threat digital spending could pose to consumer companies. Perhaps that's because it's likely already happening. And because the consumers' wallet is a zero-sum game. Any new spending on digital goods and services will likely replace spending elsewhere.

The eight-year-old kid who used to ask their parents for their favorite sports team's jersey might now ask for the digital version of that jersey for their online avatar. Some free-to-play video games are already generating billions in annual revenue from this preference shift.6 And the apparel company just lost a sale to a competitor that's potentially not on their radar.

But plenty of traditional consumer companies are leaning into new opportunities. Building on the apparel example above, some of the world's largest clothing and fashion brands are already introducing digital apparel into online worlds.7 These forward-thinking brands are acquiring new capabilities to offer these digital products and services.

These signals should prompt every consumer industry company to understand what's getting digitized in their value chain—or what has the potential to. Businesses that feel shielded from potential disruption likely have the opportunity to disrupt themselves and start moving now.

To meet current and future customers where they are, a growing number of traditional consumer companies will likely find themselves on a journey to reposition themselves as digital brands. And that journey will likely come with new challenges, from gaining access to the right talent and capabilities to licensing and trademark controls, tax implications, and forming the right alliances and partnerships that could offer lower-risk pathways into emerging digital spaces.

Deloitte's ConsumerSignals.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleIbid.

View in ArticleMitchell Clark, “Fortnite made more than $9 billion in revenue in its first two years,” Verge, May 4, 2021.

View in ArticleVanessa Friedman, “What to wear in the metaverse,” New York Times, January 20, 2022.

View in ArticleThe authors would like to thank Jeff Loucks and Marcello Gasdia for their contributions to the article.

Cover image by: Sofia Sergi