Exploring 2022’s toll on global financial well-being has been saved

The authors would like to thank Marcello Gasdia for his significant contributions to this article.

Cover image by: Sofia Sergi

As prolonged pandemic concerns eased in early 2022, the year held hope. But with each month, the pandemic's financial aftermath piled up. Headlines reported record inflation, rising interest rates, turbulent equity markets, global energy shocks, looming recession, and geopolitical events of varying scale. These headlines became the 2022 norm.

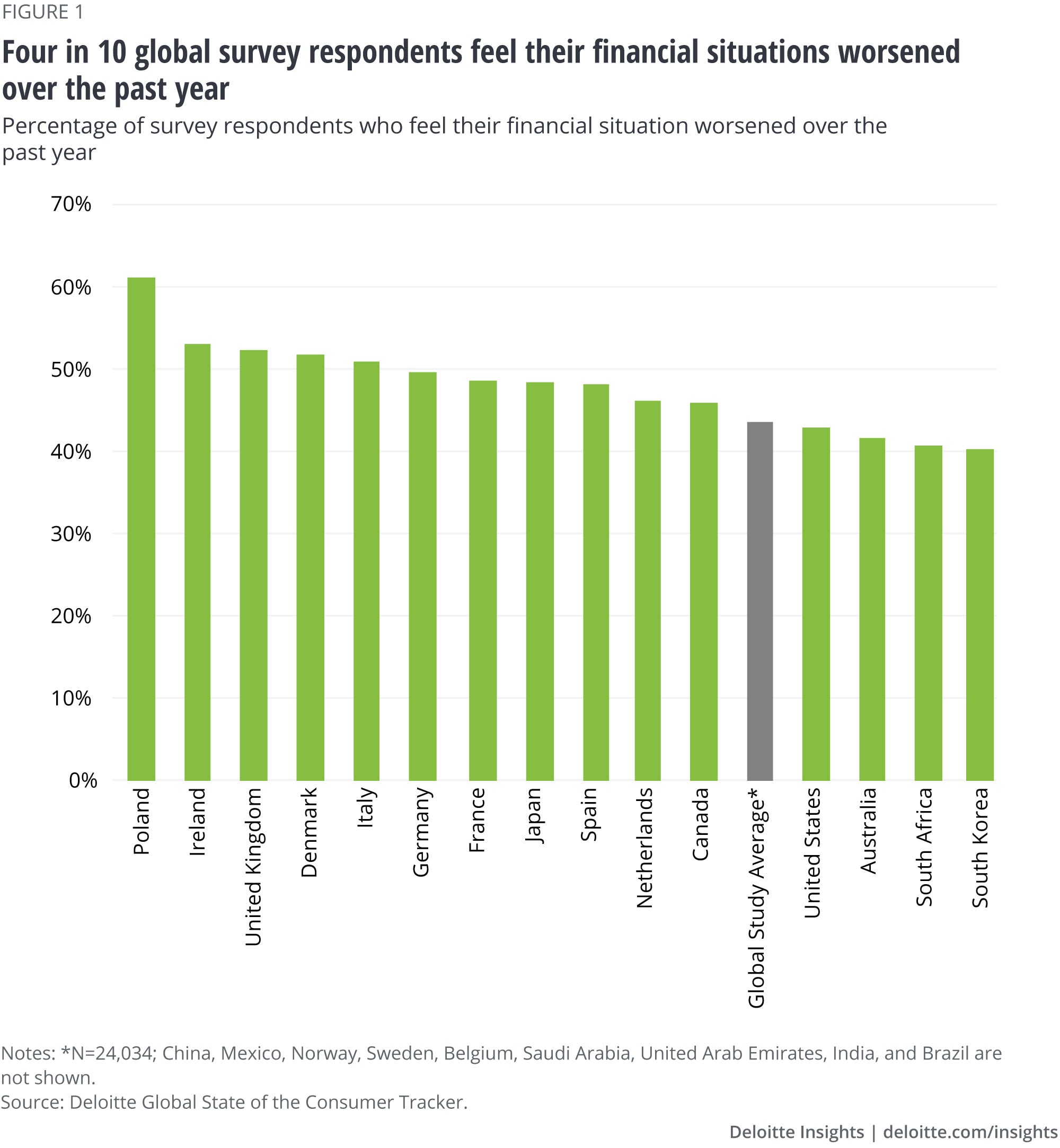

The combined effect left a mark on consumers worldwide—four in 10 respondents to our global survey feel their financial situation worsened in 2022 (figure 1). That number is significant because it has geographic and demographic reach. Worsening personal finances are being felt acutely in Europe; in the United States, it's likely the highest seen in over a decade (figure 1).1

And unlike some might expect, the trend isn't exclusively concentrated among the less affluent. Globally, one in three higher earners (34%) feel their finances took a turn for the worse in 2022, compared to nearly half of lower earners (47%).2 Investment portfolio performance might inform the former, while the latter sizes up inflation's bite into their paycheck. But while different income groups could be feeling the pinch for different reasons, their general take on 2022 is shared.

Many are heading into 2023 with a gloomier sense of financial well-being. It's a state of mind that's unlikely to disappear overnight. Those who feel their finances worsened cite concerns that could take time to subside—even if stressors like inflation gradually improve. And this sentiment is poised to inform purchase behaviors and spending intentions.

Survey respondents who feel their financial situation worsened in 2022 are:

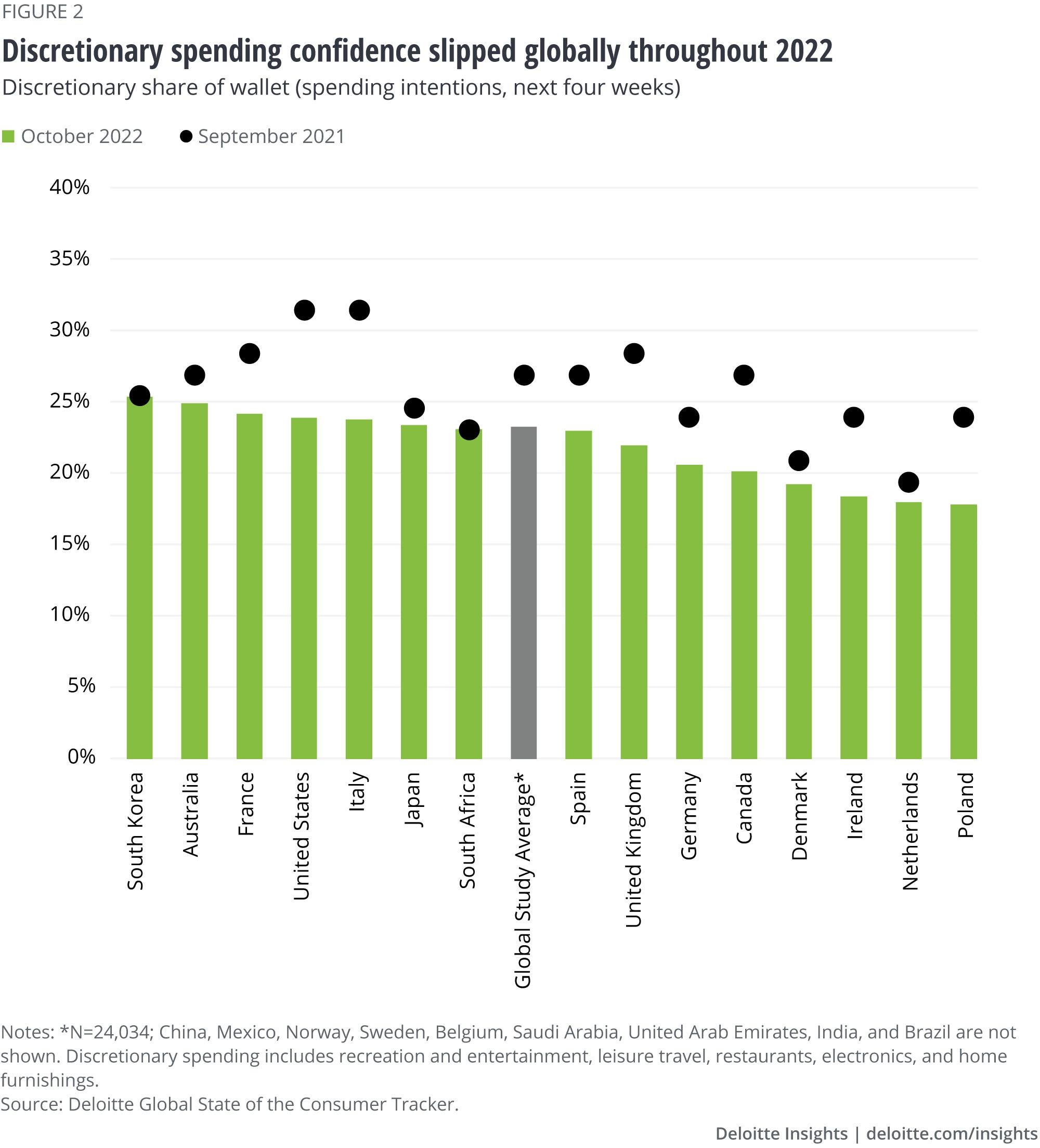

Globally, spending confidence was already showing signs of slipping throughout 2022. In September 2021, consumers estimated spending 26% of their upcoming monthly budgets on more discretionary categories (figure 2). Over the course of the year, that figure slipped to 23%. Recent drops in discretionary spending intentions have been particularly notable in the United States, Italy, the United Kingdom, Poland, Denmark, and Germany.

While the debate around a potential global recession continues, inflation, at the very least, is likely to remain a concern.3 On the bright side, consumer spending intentions have held up reasonably well against historic inflation. Throughout 2022, consumer industry leaders have pointed to resilience in consumer spending to defend more optimistic takes for the 2023 economy.4

But there's a question around how much longer spending confidence can hold up—particularly since some cracks have already started to show.

Many have speculated that massive pandemic savings are providing consumers a lifeline.5 And there's certainly some evidence of this in the data.

Compared to consumers who feel their financial situations are the same or better, those who feel their situations worsened do not plan to replenish their savings at the rate of the other cohorts (figure 3). They appear to be using the savings offset to deal with the disproportionately higher housing, utilities, groceries, and transportation costs. But the savings pullback may also be helping them accommodate more discretionary spending intentions that bring them joy, such as leisure travel, recreation & entertainment, and restaurants.

But how long is the fuse before something more explosive ignites? In countries like the United States, observers have estimated Americans have roughly nine to 12 months to spend through US$1.2–US$1.8 trillion in excess pandemic savings.6

A year is long. But there's growing consensus that many consumers around the world are on borrowed time.

Of course, some observers offer more positive views. Some speculate that consumers could be due a lifeline in the form of rising wages.7 Examining wage behavior in past inflationary episodes, research suggests that the price of labor will take more time to adjust to new circumstances than the prices of goods and services. If so, this could be good news for households who’ve experienced their purchasing power erode as inflation has outpaced wage growth.

There is much discussion on the possible depth and duration of a coming downturn and when it might begin. Rather than guess what might happen, the more critical task for consumer companies is to focus on what leaders can do today to sustain enterprise value regardless of any potential challenges ahead.

What we know:

Recent headlines don’t tell the full story of what's ahead.

Elements of a downturn will likely be different than what we've seen in the past. The business environment has changed post-COVID, and many enterprises have evolved as they've adapted to the significant shocks of recent years.

Companies can do more than brace for economic headwinds.

The characteristics of companies outperforming their peers point to strategic and operational choices that help companies succeed—even amid challenging times. Deloitte examined the performance of 500 large-cap public companies since 2016,8 and found that long-term success is linked to the degree to which enterprises exhibit strength along two dimensions.

Leaders can prepare for a downturn and pave a path toward future success.

While businesses will act to cut costs, manage cash flows, and invest in essential strategic initiatives, proactive moves can be made to focus on long-term value and market leadership. To prepare to find the tailwinds that could help propel performance beyond the current cycle, leaders can explore a range of opportunities—from cost transformation and talent and organizational assessment, to M&A readiness, and market sensing and scenario planning.

Read Facing headwinds, finding tailwinds: How companies can build enduring value and stability through an economic downturn to learn more.

{kind=link}

{kind=link}

{kind=link}