The tech industry has been in upheaval for the past few quarters, and the uncertainties don’t seem to be getting any more certain in the near term.

United States and European governments are spending over US$100 billion to grow local semiconductor production,1 but macroeconomic factors and a shift from shortage to oversupply are near-term challenges.2 The same global and macroeconomic uncertainties may harry the tech industry as a whole, with the potential to put manufacturing and growth at risk.

Companies can, however, take some steps to reassess their strategies and focus on core capabilities as they work toward recovery.

To explore these considerations in detail, Deloitte’s industry leaders recently discussed their perspectives and outlooks for the semiconductor and technology industries in 2023. Each outlook focuses on important trends and sets out questions for decision-makers to consider when planning for the short and longer terms.

Fundamentals impacting the sector

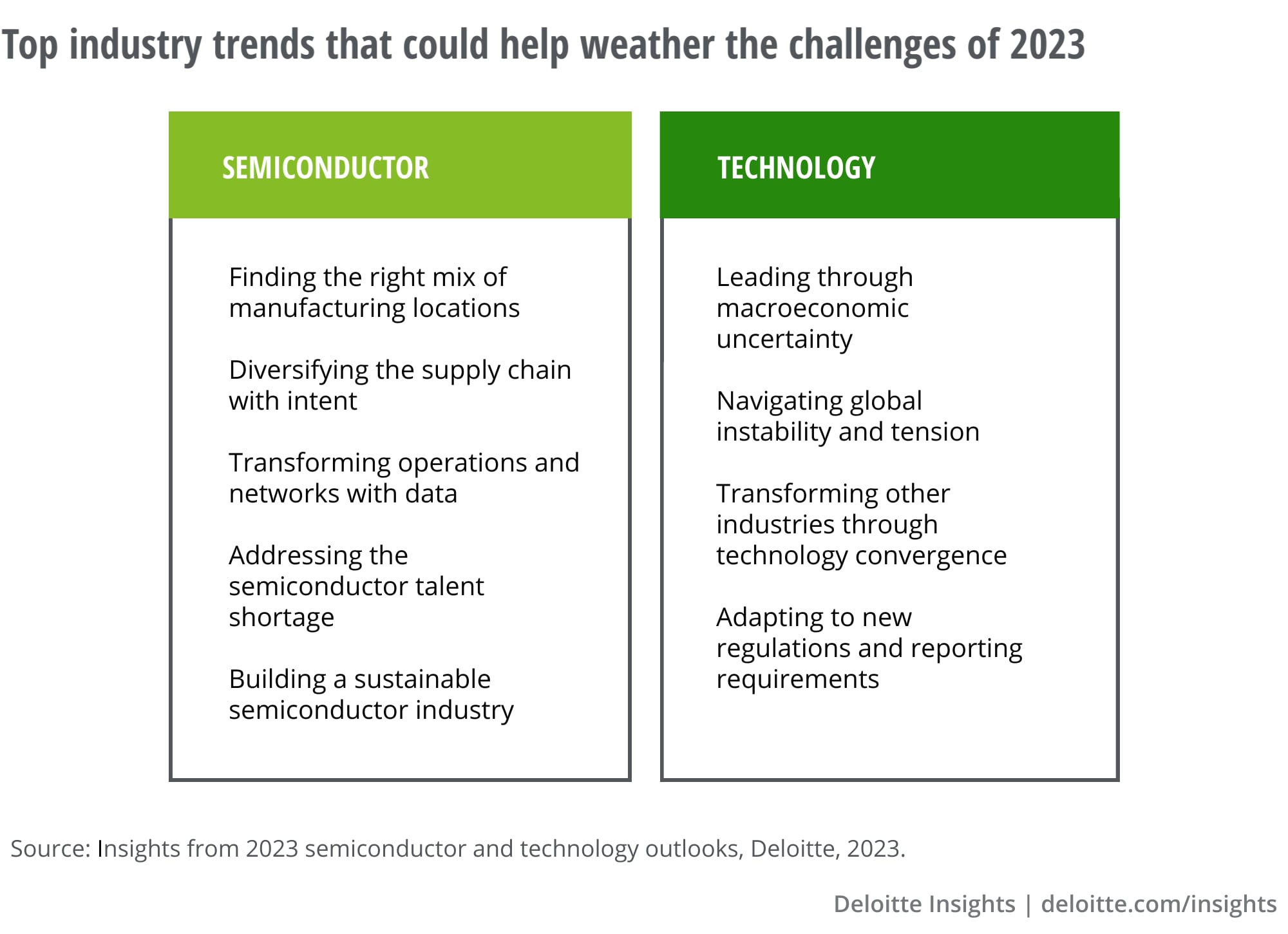

Factors such as the higher cost and uncertainty of capital, inventory drawdowns from customers and the supply chain, and a decline in earnings are leading many chip companies—and technology players in general—to cut costs, reduce employee headcount, and push out capital expenditures.3

This downturn, however, could give the semiconductor industry an opportunity to take a pause and consider five areas that can help fuel growth and efficiency going forward:

- Bringing manufacturing closer to home by expanding current facilities and building new ones.

- Mapping out the complexities of partnering with talent- and investment-friendly localities and locating functions strategically.

- Digitizing and interconnecting processes, such as financial planning and operations, order management, and supply chain.

- Exploring short-term tactics for sizing talent needs and long-term strategies for attracting and developing talent.

- Accelerating efforts around environmental, social, and governance goals.

At the macro level, technology companies may face similar challenges to semiconductor manufacturers and experience enormous pressure to reduce costs and improve profitability. The pandemic may have fueled short-term growth and a massive hiring boom, but now organizations may consider rightsizing strategically so as not to put future growth and innovation at risk. Geopolitical uncertainty and rapidly shifting regulations are two other factors that could create challenges for tech companies this year.

One trend that seems to represent a path forward for technology is transformation of other industries, such as health care, manufacturing, and retail. Technologies such as 5G, AI, edge computing, new devices, and digital processes could have the potential to transform business models and operations across a wide range of fields.

Deloitte’s outlooks encourage leaders in the tech and semiconductor industries to consider important questions such as:

- How can data drive modernization and automation efforts to increase efficiency, reduce waste, and streamline talent utilization? Are there new ways for humans and technology to work together and deliver value?

- Where could mergers and acquisitions make sense to position organizations for optimal growth? How can strategic partnerships reduce friction and drive success for the industry as a whole?

- How should digital software solutions like ERP evolve to meet new regulatory requirements and cyber needs? How can organizations position assets and resources to maximize available credits and incentives?

- What sustainability and net-zero strategies will likely be necessary as companies build out new capacity? How can companies leverage transparency reporting to highlight their dedication to environmental protection?

Economic headwinds may be gathering for business in general and for the tech and semiconductor industries specifically. But there are many regulatory incentives that may spur innovation and growth in 2023 and beyond.4 Organizations should consider critical factors, such as how and where products are manufactured, what operational and infrastructure components could be modernized, and where inorganic growth may be most conducive to long-term success.

{kind=link}