Easing the semiconductor shortage has been saved

Cover image by: Viktor Koen

Not even industry experts foresaw the worst semiconductor supply chain crunch in years, and it has hit hard, driven by strong COVID-19-driven demand, orders being canceled and then renewed due to fluctuations in end markets, and even fires in some key plants. And with the latest chips increasingly critical to a wide range of products,1 the current chip shortage is affecting manufacturers worldwide. US and global automakers are feeling the pinch and pushing for political action,2 and smartphone providers are warning investors.3

For now, the onus is on chip companies to ramp up production immediately. Building a semiconductor wafer fabrication plant from scratch takes a couple of years, but upgrading certain key pieces of hardware and software, reprioritizing scheduling, and sharpening the pencil on asset utilization can quickly speed production, much to the relief of anxious customers.

Samsung, a top semiconductor supplier as well as a smartphone maker, and others are well aware that serious semiconductor supply shortages cannot be made up quickly.4 Ramping up chip fab capacity involves sourcing a complex mix of ultra-clean factory floorspace, customized capital-intensive equipment, and specialized materials through a complex global supply network.5 And the front-end wafer fab is not the only bottleneck: The back-end chip assembly and test stages also involve challenges,6 including finding leadframe and substrate supply and matching automated test equipment (ATE) configurations to a dynamic demand mix.

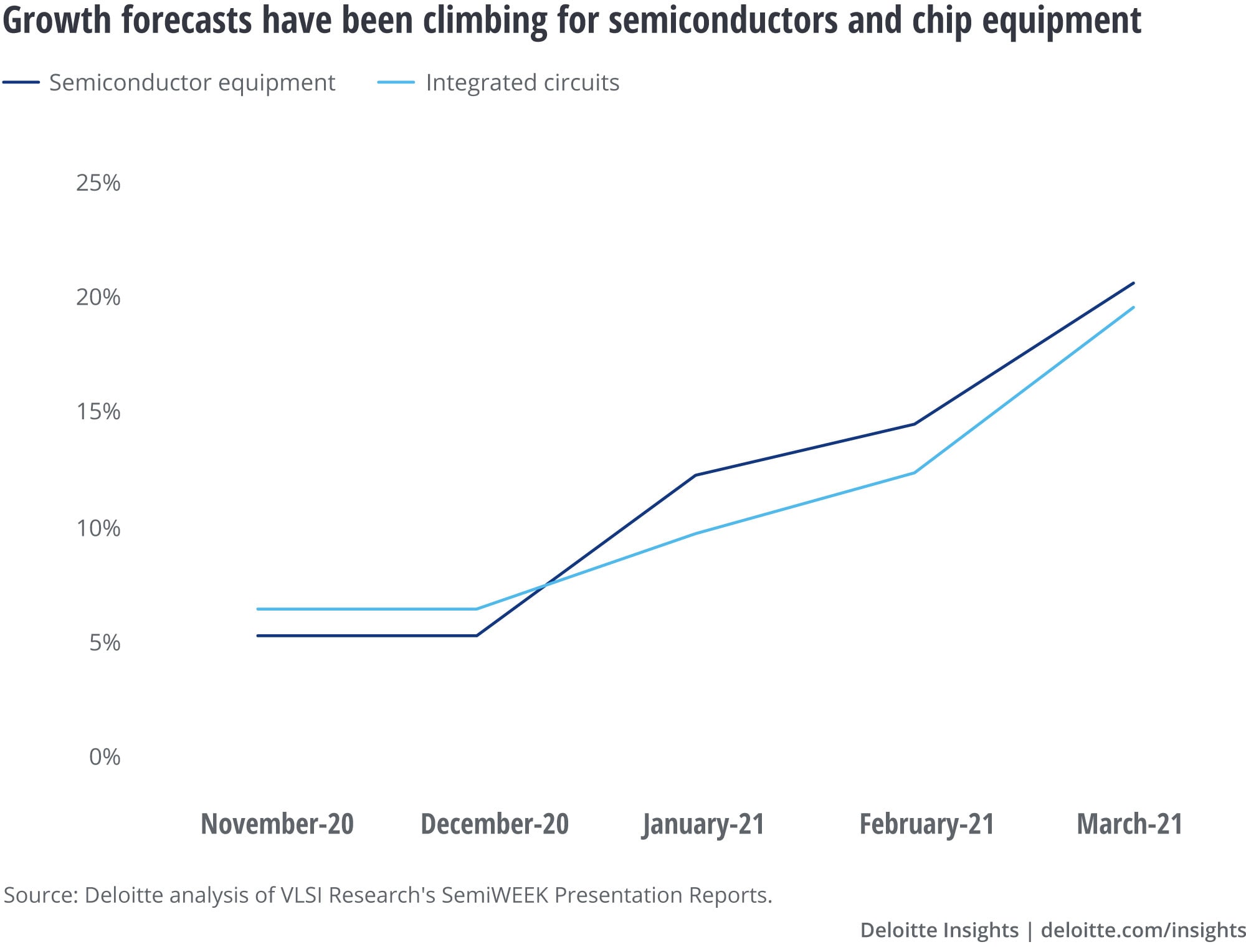

Few predicted the explosion in demand (see figure) that led to the crunch. In December 2020, a leading industry research firm predicted that spending on chips and the equipment for making chips would rise 5–6% in 2021.7 A month later, the same firm ratcheted up the number8—and did so again in February.9 By March, the annual growth forecast had climbed all the way to 19–21%.10

If industry experts are having trouble forecasting the chip industry, it’s no surprise that chip makers, chip buyers, and policymakers are trying to catch up as well.

Still, even if chip makers can’t set up new plants immediately, there are steps that they can quickly take to alleviate this crunch—and, inevitably, future crunches as manufacturers strive to align capacity to a dynamic and uncertain demand outlook.

Equipment upgrades. Companies should focus on upgrades now and new equipment over the longer term. Even with available floor space, procuring and installing new equipment is unlikely to add capacity fast enough to address a near-term surge in demand. Equipment build lead times keep increasing, limited at times by the supply of chips that the equipment itself is used to manufacture. Upgrades (hardware or software) of existing equipment are more quickly obtained and can provide improved throughput or new capabilities over various manufacturing stages. Feature licenses for ATE, for example, can be electronically downloaded and deployed to the ATE to provide more test capacity for, for instance, automotive components that need to be expedited.

Scheduling (re)prioritization. Prioritize chip production and reduce nonproduction activities without sacrificing quality. Opportunities can be identified to eliminate or at least temporarily delay certain engineering lots in fab, noncritical characterization sampling in test, or other nonproduction activities that consume capacity. More aggressive test time reductions at different stages (wafer sort, final test, burn-in test, etc.) may also be pursued—so long as, of course, speed doesn’t jeopardize quality and reliability.

Asset utilization. As with scheduling optimization, semiconductor companies are already focusing on asset utilization. Still, there are some actions to take that may improve constraint utilization by a few points. For instance, companies can refocus operator allocation and scheduling to reduce tool assist response times. An emphasis on resources and supplies being available and staged for use at critical—for example, bottleneck—tools and tool clusters, so those tools can keep running without missing a beat, can also enhance overall production output.

{kind=link}