{kind=link}

The cloud migration forecast: Cloudy with a chance of clouds has been saved

Cover image by: Christian Gralingen

Growth in cloud computing has been a megatrend over the last decade, with the market experiencing triple-digit annual growth as recently as 2015. Even though growth among the largest hyperscale public cloud providers had declined to “only” 31% annually by the end of 2019, and this rate had been projected to (slowly) decline further in 2020 and 2021 as the industry matures, growth in cloud continued to outpace that in many other sectors.

It would have not been surprising to see cloud spending go down a few points in 2020, given the spending reduction in multiple areas driven by the COVID-19 pandemic and the associated global recession. Instead, the cloud market has been remarkably resilient. By some metrics, growth was more or less flat in 2020; by some other ways of measuring growth, it increased faster than in 2019, even in the face of the steepest economic contraction in modern history. The likely reason: COVID-19, lockdowns, and work from anywhere (WFA) have increased demand, and we predict that revenue growth will remain at or above 2019 levels (that is, greater than 30%) for 2021 through 2025 as companies move to cloud to save money, become more agile, and drive innovation.

“We’ve seen two years of digital transformation in two months.” —Microsoft CEO Satya Nadella1

Of course, cloud is not the only solution in play. When viewed at the total company level, very few systems will be only on-premise, only public cloud, or only private cloud. Most deployments will likely use a combination of a public cloud and a private environment that remain distinct entities but are bound together, an approach known as hybrid cloud. Hybrid cloud can take many forms, such as a combination of private with public cloud or public cloud with on-premise resources,2 but all offer the benefits of multiple deployment models.

Clearly, hybrid cloud is the new normal. According to a March 2020 report, more than 90% of global enterprises will rely on hybrid cloud by 2022.3 Another survey from the same month found that 97% of IT managers planned to distribute workloads across two or more clouds in order to maximize resilience, meet regulatory and compliance requirements, and leverage best-of-breed services from different providers.4

But even though many organizations will retain at least some on-premise resources, and even in current economic conditions, cloud providers have much to look forward to as migration to the cloud accelerates. Various tangible and measurable indicators highlight the magnitude of this acceleration, including workload, revenues among public cloud providers, revenues among the semiconductor companies whose chips power the cloud, and growth in cloud traffic across global telecom networks.

As a note, many cloud forecasts are black boxes, based on proprietary information that cannot be replicated.5 However, metrics such as hyperscale cloud revenues, data center chip revenues, and cloud traffic are all publicly available, and anyone can reproduce our work and see the same trends.

An April 2020 survey of 50 CIOs found that respondents expected to see the proportion of total workload done on-premise drop from 59% in 2019 to 38% in 2021, a reduction of 41%.6 Moreover, they expected public cloud’s proportion of total workload to grow from 23% to 35% in the same timeframe, with private and hybrid cloud reaching 20% and 7% of workload, respectively. Sixty-eight percent of the CIOs ranked “migrating to the public cloud and/or expanding private cloud” as the top IT spending driver in 2020, up 20 points from a similar survey only six months earlier.

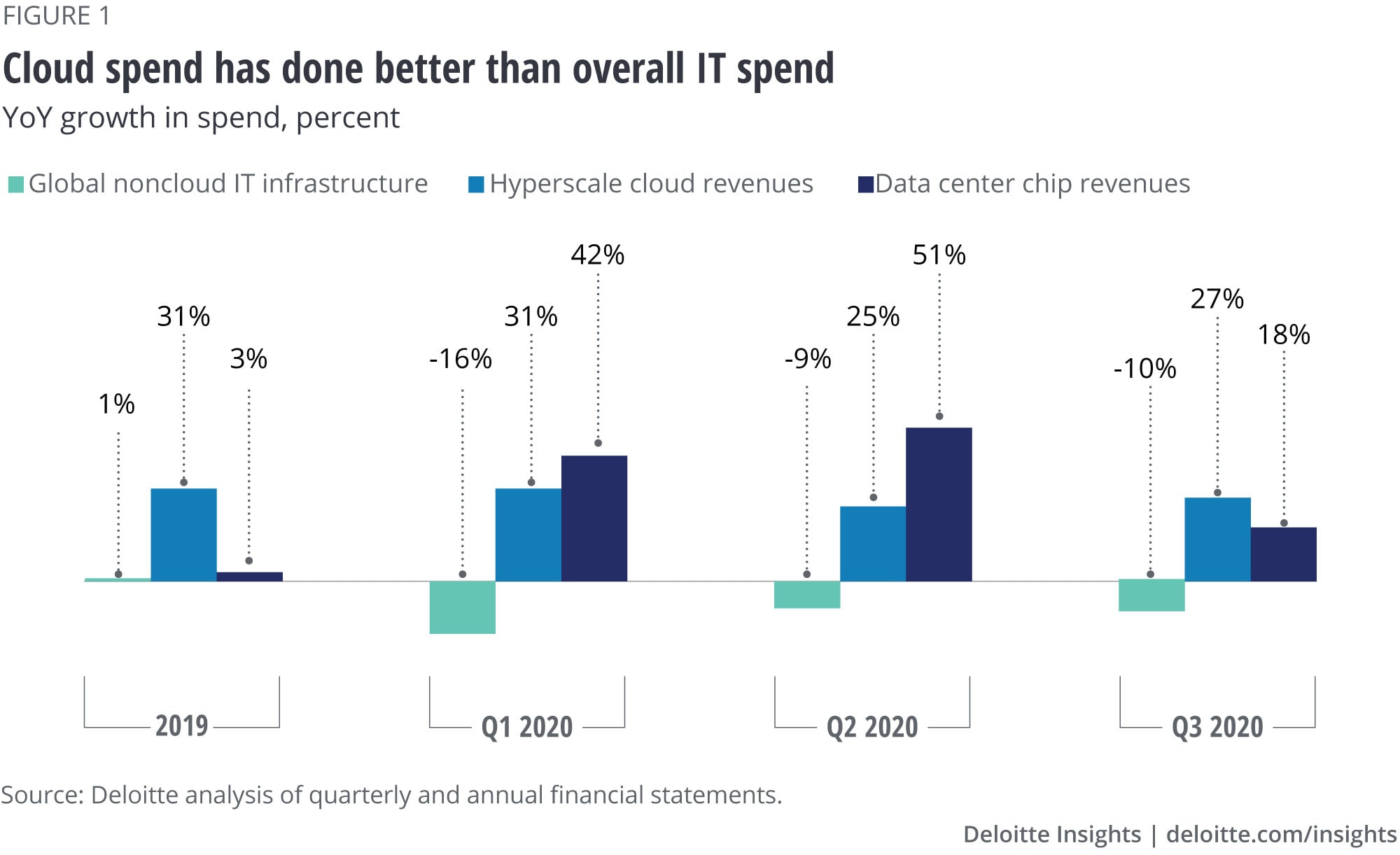

The five largest hyperscale public cloud providers that disclose segmented revenues saw their combined revenues grow by 31% in 2019 to US$94 billion. Despite widespread tech spending weakness in calendar Q1 2020, revenues grew by 31% over the same period in the previous year. In calendar Q2, growth showed a 25% year-over-year increase, which rose slightly to 27% in calendar Q3, resulting in a 28% growth rate over the first nine months of the year. Revenues for 2020 are likely to be over US$125 billion, increasing to more than US$160 billion in 2021.7 And although percentage growth was down three points in the first nine months of 2020 compared to all of 2019, it is worth noting that in absolute dollar terms, the total hyperscale market (not just the five largest) grew more in 2020 than in 2019. The market in the first half of 2019 was about US$40 billion larger than in the first half of 2018, while the market in the first half of 2020 was about US$50 billion larger than in the first half of 2019.

Data center semiconductor revenues

As of mid-2020, there were 541 hyperscale data centers globally, with 26 added in the first half of 2020 and another 176 planned over the next few years.8 All of these data centers need chips. Though chip spending and cloud revenues are not perfectly correlated, they are connected in the long run, with growth in chip revenues usually being a leading indicator: The chips need to be bought and installed in the data centers before the cloud revenues start flowing.9

The three largest semiconductor companies that disclose segmented data center sales saw their combined revenues grow by only 3% in 2019 to just under US$30 billion. In calendar Q1 2020, they saw growth explode by 42% compared to the previous year. In calendar Q2, their revenues grew further to 51% year over year. Although growth declined to 18% in calendar Q3, this still works out to a 36% increase in the first nine months of 2020. Total 2020 revenues are likely to exceed US$35 billion, and could top US$40 billion in 2021.

According to a deep-packet inspection report on network traffic during the period from February 1 to April 19, 2020, global cloud traffic as a percentage of total internet traffic rose from 1.26% to 1.83%, up by 45%.10 Over the same timeframe, overall internet traffic grew by 38%, meaning that cloud traffic, measured by the absolute number of bits per day, rose by almost exactly 100%.

Only about 10 large public hyperscale cloud providers and chip companies break out their cloud revenues on a quarterly basis in detail. However, many other companies sell chips, storage, and connectivity solutions into the cloud space. Although these companies are not necessarily providing detailed quarterly numbers, their commentary has been in line with those that do release exact numbers. As just one example, Micron, a supplier of storage for multiple markets, said in Q2 2020 that “Our cloud DRAM sales grew significantly quarter over quarter, with strong demand due to the work-from-home and e-learning economy and significant increases in e-commerce activity around the world."11

Additionally, investors have been pumping funds into the cloud sector, with total assets in the three largest cloud exchange traded funds (ETFs) reaching US$6 billion as of mid-August 2020, US$2 billion more than at the start of the year. Not only were assets up, but so was performance, with the three cloud ETFs yielding an average year-to-date return of 47% as of October 30, compared to only 22% for the NASDAQ and 1% for the S&P 500.12

All the COVID-19–driven interest in cloud is driving mergers and acquisitions as well. In just the first four months of 2020, the value of completed data center acquisitions, at US$7.5 billion in only 28 deals, was greater than in all of 2019.13

Although cloud is growing rapidly overall, it serves multiple industries, many of which have cut spending sharply. This means that while overall growth is strong, it is not uniform. As stated by the industry publication SiliconANGLE: “Because the big cloud players … are so large, they are exposed to industries that have been hard-hit by the pandemic. As a result, we see pockets of spending deceleration even at these companies.”14

Although the growth in cloud in the first nine months of 2020 was very high, many forecasts expected it to slow to some extent in subsequent quarters. However, two factors suggest that this decline in growth could be less than expected. First, although lockdowns are unlikely to be as uniform as they were earlier in 2020, flareups in the pandemic and more-localized lockdowns are still driving WFA and cloud growth. Second, in the longer term, the WFA “forced experiment”15 is being seen as a success by many workers and employers. As an example, Siemens is allowing employees to WFA, where feasible and reasonable, two to three days per week going forward; this policy applies to more than 140,000 employees at about 125 locations in 43 countries.16 Continuing or growing WFA arrangements such as this could strengthen ongoing demand for cloud.

As far as the industry landscape goes, many technology markets see significant concentration with one or two large companies accounting for almost all of the market, and cloud is no exception. The two largest hyperscale providers accounted for 78% of all revenues among the top five hyperscale providers in 2019, and the largest chip company accounted for 82% of total data center semiconductor revenue in the same year.17 At least so far, the effect of COVID-19 has not led to increasing concentration; indeed, the leading hyperscale providers’ market share declined slightly (by two to seven percentage points) during the pandemic-related surge in cloud growth. Longer term, as growth returns to historical rates, it seems likely, based on the history of technology, that market concentration will increase again. Economies of scale usually matter, and while it isn’t necessarily “winner take all,” it may be “winner take most.”

The market for hyperscale cloud services might be shifting from a global market to a decoupled market split between China, served mainly by China-based providers, and the rest of the world (ROW), served primarily by US-owned hyperscale companies. Based on limited data, it appears that the Chinese cloud market grew faster than the ROW hyperscale market through September 2020, and we would predict that decoupling would continue, if not increase.18

Finally, it is worth noting that in addition to the pandemic, the move to cloud has a long-running tailwind in terms of demand. Flexible consumption models, also known as “everything (or anything) as a service” or XaaS, have become an increasingly important strategic shift for enterprises across all industries. This market draws on more than just cloud, but cloud is a critical enabler. As of 2018, the XaaS market was nearly US$94 billion, and a pre–COVID-19 forecast predicted a five-year annual growth rate of 24%, resulting in a market of over US$340 billion by 2024.19 COVID-19 likely will accelerate the growth in flexible consumption models, but even postpandemic, those making this cloud-driven shift can see greater financial predictability, lower unit costs from aggregation, and enhanced customer relationships. Companies that have shifted their offerings to an XaaS model have already experienced considerable success with both consumers and investors, challenging conventional valuations and placing pressure on industry players that are retaining traditional business models such as perpetual licensing and long-term contracts.20

Cloud providers can take several steps to support their continued growth.

First, to paraphrase Spider-Man, “With great growth comes great capital expenditures.” Higher-than-expected growth is good news, but to keep up with it, cloud providers will likely need to spend more on capex. In 2019, total hyperscale spending on capex (which includes both IT infrastructure and physical infrastructure spend) was over US$120 billion.21 Given the continued growth in revenues, it seems likely that hyperscale capex will continue to grow at double digits, reaching US$150 billion by 2022. Additionally, investment isn’t needed just for capex. For cloud providers, artificial intelligence (AI) apps and dev tools are critical to attracting and maintaining enterprise customers and require investment or acquisition.22

Also, as cloud moves from roughly one-third of enterprise workflow to roughly two-thirds, and that more quickly than expected, concerns around privacy and security should urgently be addressed. As just one example, the health care industry, which has been among the fastest to shift to cloud during the pandemic, will likely increase its exposure to new vulnerabilities, especially if the migration is not done properly. As articulated by Healthcare IT News: “While cloud computing better optimizes the use of resources in health care, it also creates significant risks. This is especially true when cloud adoption happens faster than proper due diligence can be applied by information security personnel. This trend will persist well after the pandemic.”23

One emerging development for hyperscale cloud providers is the intelligent edge. The intelligent edge places computing power, specifically AI computing power, not in centralized data centers but closer to the end user, typically less than 50 kilometers. The intelligent edge is not a replacement for enterprise and hyperscale cloud data centers, but a way to distribute tasks across the network to increase timeliness, connectivity, and security.24 In the intelligent edge model, much of the data that used to always go to the data center doesn’t go there anymore, and hyperscale providers should make sure this data finds its way back to centralized clouds for analysis and AI training—and ensure that they’re not cut out of access to this data. Another goal for cloud providers is to develop vertical-specific apps that must reside at the edge due to latency requirements and other factors. One way that hyperscalers can deal with both data transfer and app development is through partnerships.25

For their part, cloud users should consider the following factors as they continue to migrate to cloud:

The cloud migration strategy. Cloud migration isn’t just about moving to the cloud; it entails a state of continuous reinvention if cloud is to reduce costs and create new opportunities. Prepandemic, cloud migration was already often complex. Even a single application could be tied to multiple business processes, affecting vendors, balance sheets, and regulatory compliance, and different stakeholders could have different motives and expectations from the migration. A simple process could often turn into a fog of conflicting goals, broken dependencies, and cost overruns. Postpandemic, all of these factors will likely be even more challenging. It is critical to “disrupt your market without interrupting your business” during the migration.26

Cloud, security, and COVID-19. As noted above, increases in cloud usage mean increases in the cyberattack surface, making security more important than ever—especially given the growth in usage driven by COVID-19. In an April 2020 survey of security professionals, 94% believed that the pandemic increases the level of cyberthreat. Almost a quarter said that the increased threat is “critical and imminent.” Only 15% believed that the cyberthreat will return to previous levels postpandemic, while five out of six believed that the new threat level is permanent.27

Cloud costs and benefits. As multiple enterprises shifted rapidly to cloud during the pandemic, some saw costs balloon. Some companies saw costs rise by 20% to 50% just from the increase in usage, even without adding in the cost of new applications or data.28 As organizations migrate, there is also a cost of duplication, with organizations paying for both cloud and legacy systems at the same time as well as the cost of synchronizing data between them.29 Going forward, companies should think about cost planning (for instance, to take advantage of reserving instances at a discount), which can reduce expensive fixes due to rushed deployments. Cost governance systems can also help maintain control over expenses. To conduct a cost-benefit analysis, companies can use a cloud value calculator to evaluate the gaps between the current state and potential future opportunities. This can help optimize infrastructure, increase staff productivity, and enhance business value.30

New opportunities for value.Moving to the cloud is not only allowing organizations to recover but positioning them to thrive postpandemic, increasing resilience and supporting business continuity at first, and then allowing to them to do new things and offer new services. Going forward, cloud can support benefits including collaboration, automation, scale, innovation, and agility.31 For example, with regard to innovation, two-thirds of respondents in a 2018 Deloitte survey said that cloud fully allowed them access to the newest technologies.32 Another study showed that 93% of companies surveyed used the cloud for some or all of their AI needs, requiring less investment in infrastructure and expertise.33

Thanks to COVID-19 driving enterprises toward cloud, the cloud market will likely emerge from the pandemic stronger than ever. Cloud providers and others in the ecosystem have the opportunity to capitalize on increased usage to grow and flourish, while cloud users can seek to explore new ways for cloud to create value. Already, cloud has become much more than an alternative computing approach; in the near future, it is poised to become standard operating procedure for all types of businesses.