Women in the boardroom, eighth edition

A Deloitte Global report on gender diversity on boards and women in leadership

Executive summary

Gender parity on boards will be elusive without greater focus and action

The business case for diversity has been established for some time. Companies with more diverse boards have shown that they tend to perform better financially.1 What’s more, organizations that are more diverse as a whole with respect to gender—from top executives and board members to managers and employees—tend to outperform those that are less gender-diverse.2

What remains in question, however, is this: With women still underrepresented on company boards globally, why aren’t organizations and investors doing more to realize the benefits that diverse boards bring?

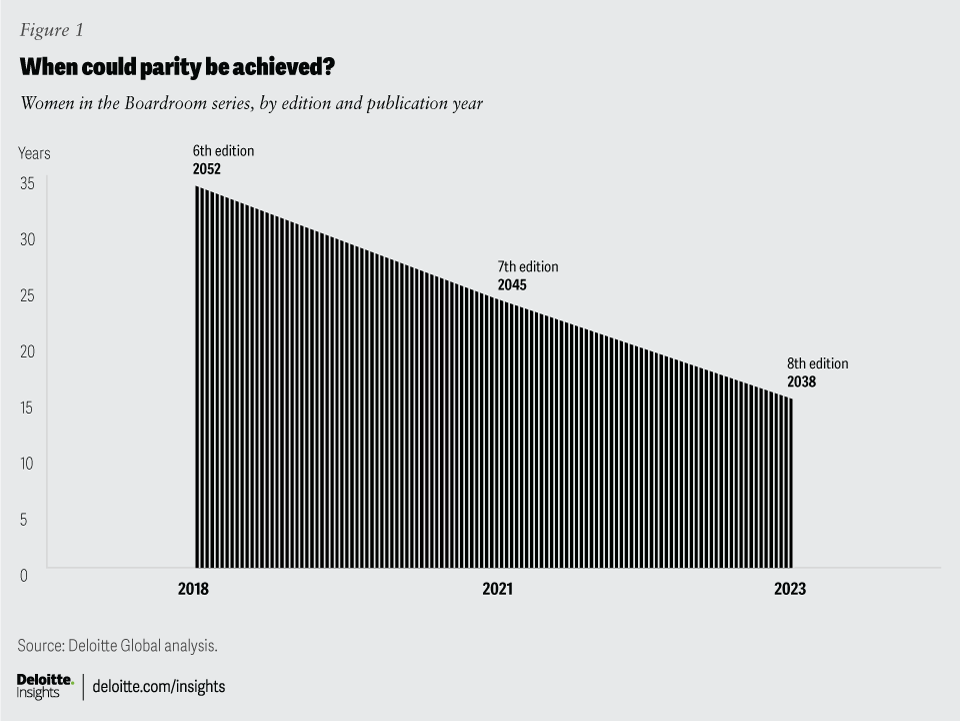

The eighth edition of the Deloitte Global Boardroom Program’s Women in the boardroom: A global perspective finds that women hold less than one-quarter of the world’s board seats (23.3% in 2023).

Continued efforts from a wide range of stakeholders have indeed yielded some positive results toward achieving gender parity: Since 2022, the number of women on boards has risen 3.6%, and the timeline toward achieving parity has dropped by seven years (figure 1).

However, despite the number of initiatives around the world to increase the number of women serving on boards, progress isn’t happening quickly enough. If this rate of change were to hold steady, it is unlikely that gender parity on boards will be reached before 2038—and possibly later. And, there is no clear path to gender parity in the board chair role.

For parity to become a reality, a wide range of stakeholders will need to devote greater focus and action to enable corporate boards to more accurately reflect the societies in which they operate. And boards themselves will need to continue to take action and ask the right questions.

Government action has driven impact at the board level

One thing that has become apparent is that government action yields results. Five of the top six countries with the highest percentage of women serving on boards in our study have some sort of mandatory quota legislation, ranging from around 33% (Belgium and the Netherlands) to 40% (France, Norway, and Italy). And continued government initiatives in the United Kingdom, through the use of targets, for example, (the 2011–2015 Davies Review3 and the 2016–2020 Hampton-Alexander Review4), have also borne fruit: Women now hold over 40% of FTSE100 board seats in the United Kingdom5 and over 34% of all board seats in our sample. Similar efforts in Australia, through voluntary targets and disclosures,6 have also moved the needle—women’s representation on Australian boards has more than doubled since 2014 (15% to 34%). Yet the recent political climate in some geographies may be starting to waiver on diversity, equity, and inclusion initiatives, which could challenge this momentum.

Concerns that quotas drive “overboarding” may not hold water

Some have criticized the practice of implementing gender quotas and targets for boards because they fear it would result in the same small circle of women being “overboarded”: being asked to serve on a large number of boards.7 To assess this concern, in 2014, Deloitte Global developed the “stretch factor,” a research tool that measures the average number of board seats an individual holds in a particular market. The higher the stretch factor, the more seats are held by any single director in a given market. This year’s stretch factor remains unchanged for both women (1.30) and men (1.17) at the global level.

While there is no magic number of board seats an individual director should hold, the geography-level data shows that the movement to increase gender diversity on boards has not caused the kind of overboarding that some may have feared. Of the 20 geographies with the highest stretch factor for women, only four were in a geography with quota legislation for publicly listed companies. In Norway, the first country to introduce gender quota legislation for boards, the stretch factor has steadily declined from 1.15 in 2014, falling to just 1.04, well below the global average. While variations at the geography level do exist, it appears the initial fears have not come to fruition.

Investor voting policies are also motivating action

Government action alone is insufficient to reach parity. Investors need to remain vigilant in setting expectations around gender diversity, despite recent changes in the political climate and the number of matters competing for investor attention.

In looking at the voting policies of over 100 large investors, Deloitte Global8 found that two-thirds of UK and US institutional investors had a voting policy that set a target for gender diversity.

These proxy voting policies may also be creating impact in some markets. In the United Kingdom, for example, the appointment rate for women on FTSE100 boards stood at 47% in 2023, up from just 30% in 2017.9 In the United States, in 2023, across the Russell 3000, 38% of newly joining board members were women.10 Recent subtle language changes in these proxy voting policies, though, may signal a softening of investor expectations. It is important that investors remain clear on their diversity, equity, and inclusion expectations for the companies in which they invest. Continued improvement is needed to change the mathematical implications of current appointment patterns: As long as men hold the majority of board seats and continue to gain the majority of new board seats, parity will continue to be elusive.

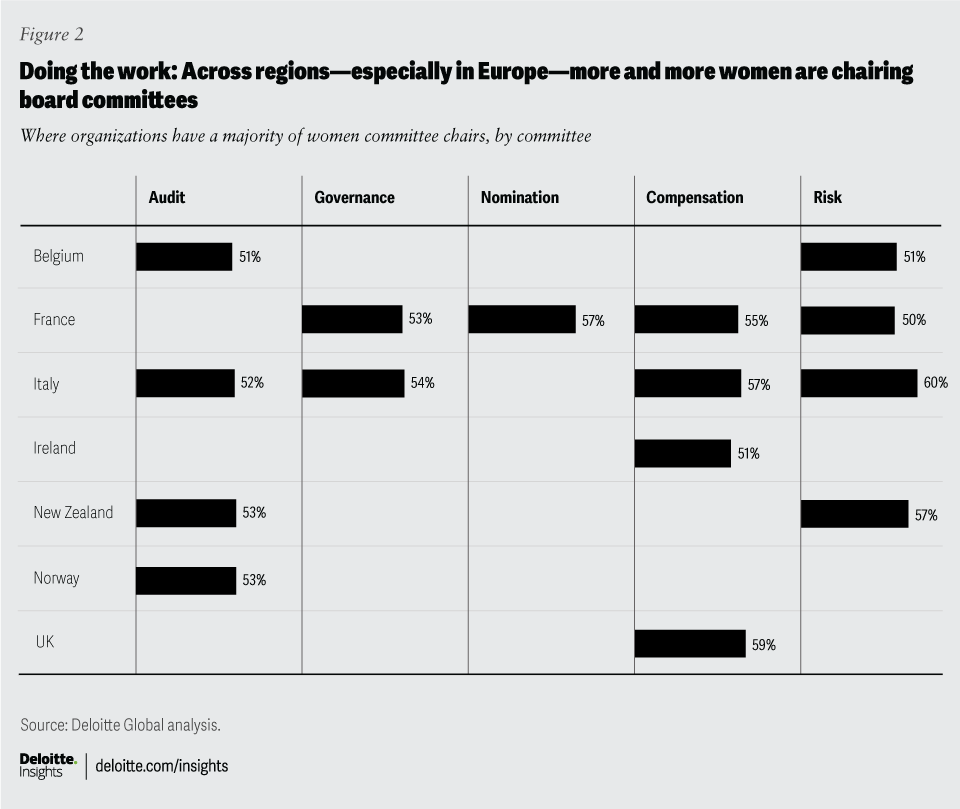

Doing the work: Across regions, particularly Europe, more and more women are chairing board committees

While no country eclipsed the 45% mark for women serving on boards in the sample, in several, women held a majority of board committee seats or committee chair roles (figure 2), particularly in Italy and France.

More than 40% of European compensation committee chairs are women. Comparing compensation committee chair figures in Europe to those in the United States reveals stark differences. Women hold a majority of compensation committee chair roles in the United Kingdom, Italy, France, and Ireland. In the United Kingdom, women hold nearly 60% of these chair positions; in the United States, that figure drops to 27%.

While it is encouraging to see women leading in these positions, more progress needs to be made in leveraging these committee chair roles to ascend to the board chair role.

Among chair and CEO roles, the glass ceiling seems impenetrable

While quotas and targets may help diversify boards, they do not seem to have the same effect on chair and CEO roles. Perhaps surprisingly, five of the top seven countries for women chairs do not have a quota for women serving on boards. Even more striking, 17 of the top 20 countries for women CEOs do not either.

Globally, the percentage of women chairing boards is nearly three times lower than the percentage of women serving on boards, with just 8.4% of the world’s boards being chaired by women. The numbers are low even in countries with gender quotas. For example, while Norway and France, which were among the first governments to introduce quota legislation (in 2005 and 2010, respectively) are both now approaching parity in the boardroom, fewer than 13% of these women directors have ascended to the chair role. Germany and Switzerland, where quotas were introduced more recently, have women chairing boards at less than a 5% rate.

When it comes to the highest executive roles, women’s representation drops even further: According to our research, only 6% of CEOs in the world are women, representing just a 1% increase from our previous edition. Indeed, in 13 of the geographies in our sample, the number of women CEOs is less than 3%. At the current rate of change, global parity for CEOs wouldn’t be reached until 2111—almost 90 years from now.

Since many companies prefer to recruit board members with CEO experience, these numbers do not paint an optimistic outlook for pipeline development. Companies need to expand their skills profiles to further diversify their boards while shoring up critical skill gaps. As Hina Nagarajan, managing director and chief executive officer, United Spirits Limited (Diageo India); member of the Global Executive Committee, Diageo PLC; and board member, BP PLC, said,11 “In a world where consumers for most companies are moving ahead in such a fast manner, we’ve got to look at the connection with consumers, digital savviness, skill sets other than experience on boards, and we’ve got to take that leap of faith bringing the right skill sets irrespective of age, previous experience, etc. I think boards need to rethink their whole recruitment strategy.”

Male chairs are making a difference. In 2016, we found that companies with a woman chair or CEO have boards that are nearly twice as diverse with respect to gender (~29% women on boards) as those with a male chair or CEO (~15% women on boards). However, today, while that gap still exists, it is shrinking. Companies with a woman chair are now only 1.4 times more diverse than those with male chairs (32.9% vs 22.9%, respectively). The numbers are nearly identical when looking at female CEOs and the number of women serving on their boards as compared to male CEOs (35.3% vs 23.0%, respectively). While there is still serious work to do, progress, regardless of the gender of the leader, is possible.

What is the financial services industry getting right?

Our research shows that, in 30 of the countries analyzed in our sample, the financial services industry was the first or second most gender-diverse industry in that market—nearly double that of the next highest industry.

Why is the financial services industry leading the way in so many of these markets? Deloitte US research on the industry may reveal some clues. Over the past decade, more women have been added to financial services industry’s C-suites than men.12 As boardroom gender diversity in financial firms has also increased during that time span, we may be seeing a virtuous cycle play out across the industry in real time.

Over the past five years, women are also joining financial services’ C-suites through nontraditional C-suite positions13 three times as fast as traditional C-suite roles.14 The research finds a “multiplier effect” exists: For each woman added to the financial services industry’s C-suite, there’s a positive, quantifiable impact on the number of women in senior management roles a level below the C-suite.

However, the current rate of progress may not be sustainable: Women’s representation in senior leadership and next-generation roles has grown at a slower rate than the C-suite, suggesting that the pipeline of future leaders may shrink in the coming years. Organizations in the financial services industry—and beyond—will need to double their efforts to build the pipeline of future women leaders so that progress can be sustained and enhanced into the future.

Boards are critical change agents

Today, board agendas are more packed than ever before—and the challenges and emerging areas boards need to keep abreast of are only increasing. As organizations aim to build more equitable and balanced boardrooms and C-suites, with real diversity of thought, directors need to remain focused on gender parity to advance progress. Key advice for boards as they continue to probe whether, and to what extent, they and management are doing enough to drive change, includes:

- Don’t default to historic experience profiles in selecting board members. Do we have the right mix of experiences, skills, and backgrounds to position ourselves to succeed in light of the complexities of today? To what extent do we, as a board, play it safe with respect to selecting our board or C-suite candidates? Do we default to narrow searches of candidates with a historical record of prior CEO experience, or are we willing to take risks to find leaders of the future? How much emphasis do we place on previous executive or board roles compared to skill sets, capabilities, leadership, and business acumen, which may be inadvertently excluding a range of high-quality women candidates?

- Get creative in building governance experience. What creative solutions can management and the board deploy to provide more opportunities for women to gain governance experience? Have we considered placing high-potential candidates on boards of our subsidiaries or other entities to fuel not only our own board and C-suite pipelines, but also corporate pipelines more broadly?

- Regularly interrogate your pipeline data and progress. Are we spending enough time challenging our data and outcomes? How fast are women being added to our C-suites? Are our pipelines advancing women at the same rates as men? Are we losing women leaders at critical junctures in the pipeline?

These areas are only a start, and boards cannot go at it alone. Business leaders in all markets will need to commit to collaborating on these matters; sharing their challenges as well as their successes, having the courage to ask difficult questions, and doing their part to help accelerate the timeline for achieving gender parity in the world’s boardrooms and C-suites.

{kind=link}

{kind=link}